An Employee Benefit Plan Audit Engagement Letter is a formal contract between an organization and an independent auditor. It outlines the scope, objectives, and responsibilities of both parties to ensure compliance with ERISA and DOL regulations. Establishing clear terms prevents misunderstandings and ensures a smooth audit process for plan sponsors. To simplify your documentation, below are some ready to use template options.

Image cover: Essential Guide to Employee Benefit Plan Audit Engagement Letters and Templates

Letter Samples List

- Full Scope Employee Benefit Plan Audit Engagement Letter

- ERISA Section 103(a)(3)(C) Employee Benefit Plan Audit Engagement Letter

- Defined Contribution Employee Benefit Plan Audit Engagement Letter

- Defined Benefit Employee Benefit Plan Audit Engagement Letter

- Health and Welfare Employee Benefit Plan Audit Engagement Letter

- Multi-Employer Employee Benefit Plan Audit Engagement Letter

- Multiple-Employer Employee Benefit Plan Audit Engagement Letter

- Terminated Employee Benefit Plan Audit Engagement Letter

- First-Year Employee Benefit Plan Audit Engagement Letter

- Short-Year Employee Benefit Plan Audit Engagement Letter

- Form 11-K Employee Benefit Plan Audit Engagement Letter

- Master Trust Employee Benefit Plan Audit Engagement Letter

- Successor Auditor Employee Benefit Plan Audit Engagement Letter

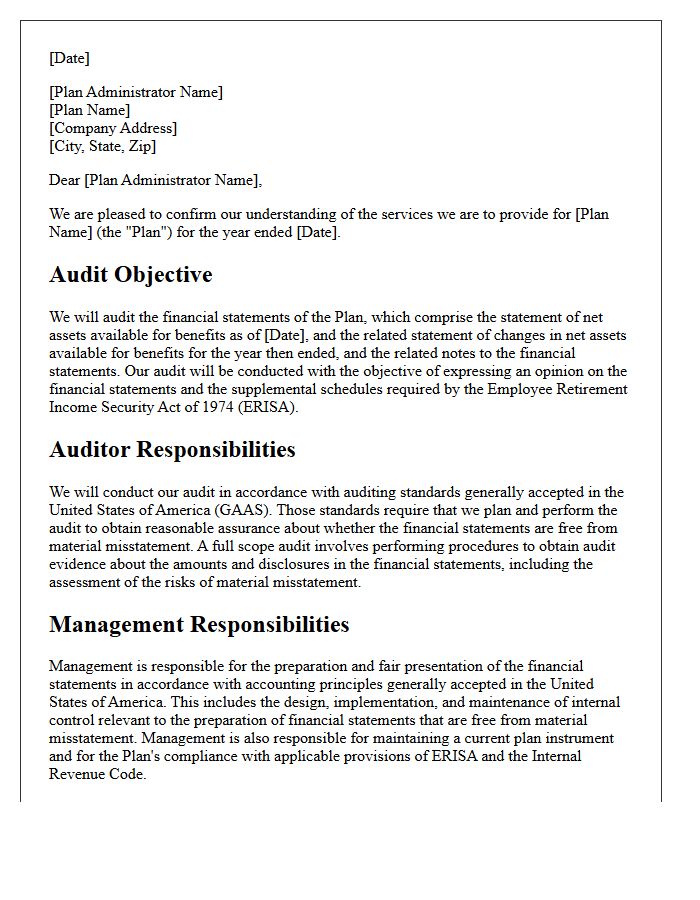

Full Scope Employee Benefit Plan Audit Engagement Letter

A full scope employee benefit plan audit engagement letter is a legally binding contract that outlines the responsibilities between a plan sponsor and an independent auditor. It defines the scope of work, reporting objectives, and fee structures while ensuring compliance with ERISA and DOL regulations. This document confirms that the auditor will examine all plan assets, including investments and participant data, without relying on certified bank statements. It serves as a critical risk management tool, establishing clear expectations for financial statement accuracy and fiduciary accountability to protect plan participants.

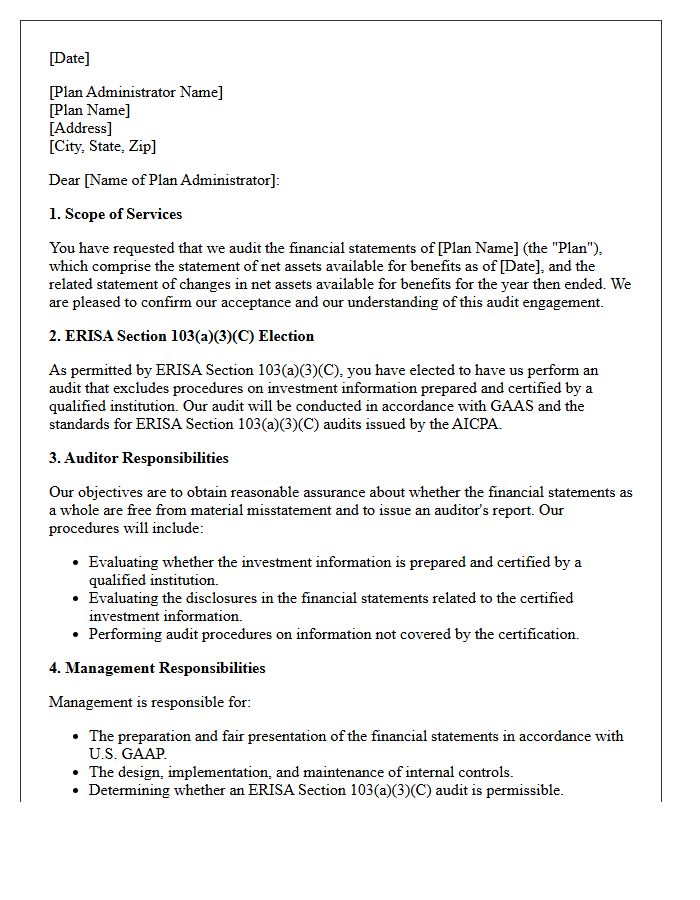

ERISA Section 103(a)(3)(C) Employee Benefit Plan Audit Engagement Letter

The ERISA Section 103(a)(3)(C) audit engagement letter defines the scope for specialized employee benefit plan audits. It confirms that management elects to exclude investment information certified by a qualified institution from the auditor's testing. This document outlines the responsibilities of both plan sponsors and auditors, ensuring compliance with Department of Labor regulations. It specifically addresses the auditor's duty to evaluate the certification's validity and report on the plan's financial health, making it a critical legal contract for maintaining fiduciary transparency and regulatory alignment.

Defined Contribution Employee Benefit Plan Audit Engagement Letter

A Defined Contribution Employee Benefit Plan Audit Engagement Letter is a legally binding contract that establishes the scope, objectives, and limitations of an audit. It clearly outlines the responsibilities of management, such as maintaining internal controls and providing accurate financial statements. The document also details the auditor's obligations to report findings according to professional standards. Formalizing this agreement is essential to ensure regulatory compliance, prevent misunderstandings regarding fiduciary duties, and establish the fee structure before the audit process begins for plans like 401(k)s.

Defined Benefit Employee Benefit Plan Audit Engagement Letter

A Defined Benefit Employee Benefit Plan Audit Engagement Letter is a legally binding contract between plan sponsors and independent auditors. It formally establishes the audit scope, objective, and specific responsibilities of both parties under ERISA standards. Key components include reporting deadlines, fee structures, and management's obligation to provide accurate financial records. This document ensures regulatory compliance with Department of Labor requirements, protecting the plan's tax-exempt status while minimizing fiduciary liability. Reviewing these terms is essential for maintaining transparent financial oversight and meeting annual Form 5500 filing mandates.

Health and Welfare Employee Benefit Plan Audit Engagement Letter

A Health and Welfare Employee Benefit Plan Audit Engagement Letter is a formal agreement between a plan sponsor and an independent auditor. It establishes the scope of services, management's responsibilities, and reporting requirements for the audit. This document is crucial for ensuring compliance with ERISA and Department of Labor regulations. It outlines the objective to detect material misstatements and specifies financial statement accuracy. Understanding this letter ensures both parties agree on audit objectives, limitations, and the legal framework necessary to protect plan participants and maintain fiduciary oversight.

Multi-Employer Employee Benefit Plan Audit Engagement Letter

A Multi-Employer Employee Benefit Plan Audit Engagement Letter is a legally binding contract defining the scope between the auditor and plan trustees. It outlines critical responsibilities regarding financial statement accuracy and compliance with ERISA standards. This document specifies reporting deadlines, fee structures, and the auditor's duty to evaluate internal controls. Understanding this letter ensures fiduciary accountability and clarifies the division of tasks to prevent misunderstandings during the audit process, ultimately protecting the interests of all participating employers and plan members.

Multiple-Employer Employee Benefit Plan Audit Engagement Letter

A Multiple-Employer Employee Benefit Plan Audit Engagement Letter is a legally binding contract defining the scope between the auditor and plan sponsors. It outlines fiduciary responsibilities, financial reporting frameworks, and auditor duties under ERISA standards. This document is essential because it specifies fee structures, objective limitations, and management's obligation to provide accurate participant data. Ensuring all participating employers are acknowledged prevents compliance gaps and clarifies accountability for internal controls, safeguarding the plan's integrity and regulatory standing with the Department of Labor.

Terminated Employee Benefit Plan Audit Engagement Letter

A Terminated Employee Benefit Plan Audit Engagement Letter is a legally binding contract that defines the scope and responsibilities during a final plan audit. It is crucial to outline the liquidation process, distribution of assets, and final filing requirements for the Department of Labor. This document protects both the auditor and the plan sponsor by clarifying fiduciary obligations and reporting deadlines. Ensuring the letter specifies the termination date and final valuation prevents compliance gaps and potential penalties during the plan's ultimate dissolution phase.

First-Year Employee Benefit Plan Audit Engagement Letter

A First-Year Employee Benefit Plan Audit Engagement Letter is a legally binding contract establishing the scope and objectives between the plan sponsor and the auditor. It is crucial to outline management's responsibility for maintaining internal controls and preparing financial statements under ERISA standards. This document clarifies fee structures, reporting deadlines, and the specific audit procedures to be performed. Establishing these compliance expectations early ensures a transparent relationship, mitigates professional liability, and ensures the retirement plan meets Department of Labor filing requirements accurately and timely.

Short-Year Employee Benefit Plan Audit Engagement Letter

A short-year employee benefit plan audit engagement letter is a legally binding contract defining the scope and terms of a financial oversight period lasting less than twelve months. This document establishes fiduciary responsibilities, auditor duties, and management obligations during plan transitions, such as mergers, terminations, or fiscal year changes. It ensures compliance with ERISA and DOL reporting standards while clarifying fee structures and reporting deadlines. Professional clarity in this letter prevents regulatory penalties and ensures the plan's tax-exempt status remains protected during brief reporting cycles.

Form 11-K Employee Benefit Plan Audit Engagement Letter

A Form 11-K engagement letter is a formal agreement between a plan sponsor and an independent auditor for an Employee Benefit Plan Audit. This document outlines the scope of work, management's responsibilities, and auditor obligations under PCAOB standards. It is a critical legal requirement for plans filing with the Securities and Exchange Commission (SEC). The letter ensures clarity regarding financial statement integrity and compliance with ERISA regulations. Establishing this contract is the first step in maintaining plan transparency and protecting participant interests through rigorous regulatory oversight.

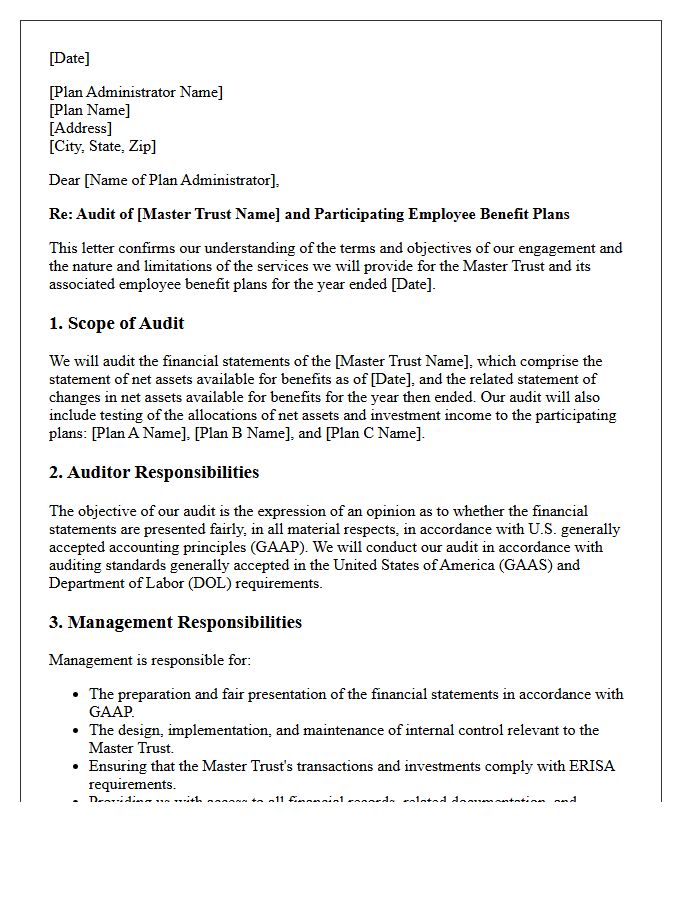

Master Trust Employee Benefit Plan Audit Engagement Letter

A Master Trust Employee Benefit Plan Audit Engagement Letter is a formal contract between an independent auditor and plan management. It outlines the scope of work, legal responsibilities, and reporting requirements for auditing assets held in a centralized trust. This document ensures compliance with ERISA and DOL standards by clarifying the audit objectives and fee structures. Proper execution is vital to confirm that the auditor can accurately verify the financial health of multiple participating plans while maintaining strict regulatory oversight and accountability.

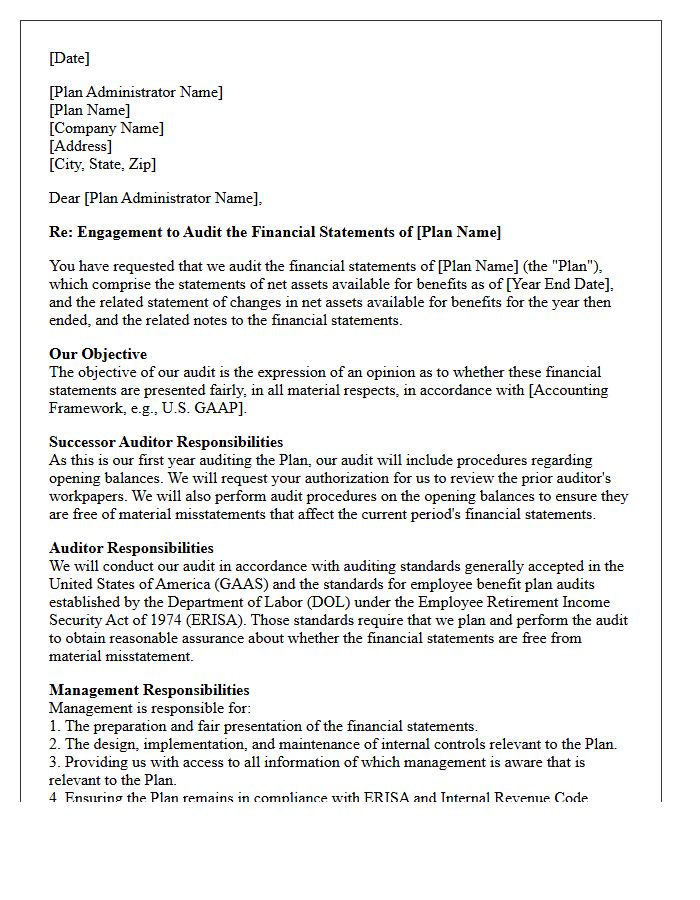

Successor Auditor Employee Benefit Plan Audit Engagement Letter

A successor auditor must obtain a signed engagement letter before starting an employee benefit plan audit to establish the scope, responsibilities, and fees. This legal contract clarifies that management is responsible for the financial statements and internal controls. It also outlines the transition process, including the review of the predecessor auditor's working papers. For ERISA compliance, the letter must specify whether the audit is a section 103(a)(3)(C) audit. Ensuring this document is precise protects both the auditor and the plan sponsor while meeting Department of Labor standards.

What is an Employee Benefit Plan (EBP) audit engagement letter?

An EBP audit engagement letter is a formal contract between an employee benefit plan administrator and an independent CPA firm that outlines the scope, objectives, responsibilities, and limitations of the audit engagement.

Who is responsible for signing the EBP audit engagement letter?

The engagement letter is typically signed by the plan sponsor or the designated plan administrator, who holds the fiduciary responsibility for the management and oversight of the employee benefit plan.

What specific responsibilities are assigned to plan management in the engagement letter?

Plan management is responsible for maintaining effective internal controls, preparing financial statements in accordance with GAAP or ERISA requirements, and providing the auditor with all necessary records and participant data.

Does an EBP audit engagement letter cover the detection of fraud?

The engagement letter states that while the audit is designed to provide reasonable assurance against material misstatements, it is not specifically designed to detect all instances of fraud, errors, or illegal acts.

Why are ERISA Section 103(a)(3)(C) audits mentioned in the engagement letter?

The letter specifies if the audit is a Section 103(a)(3)(C) engagement, which allows the auditor to limit testing of investment information certified by a qualified institution, such as a bank or insurance carrier.

Comments