A Financial Statement Audit Engagement Letter is a formal contract between an auditor and a client. It defines the scope of work, professional standards, and the responsibilities of both parties to ensure transparency throughout the auditing process. Establishing these terms prevents misunderstandings and sets clear expectations for the financial review. To assist your process, below are some ready to use template.

Image cover: Professional Audit Engagement Letter Templates and Financial Statement Samples

Letter Samples List

- Financial Statement Audit Engagement Letter

- Management Representation Letter

- Legal Counsel Audit Inquiry Letter

- Internal Control Deficiencies Letter

- Auditor Independence Confirmation Letter

- Predecessor Auditor Communication Letter

- Audit Committee Communication Letter

- Going Concern Evaluation Letter

- Related Party Transaction Inquiry Letter

- Uncorrected Misstatements Letter

- Audit Strategy Communication Letter

- Post-Audit Findings Letter

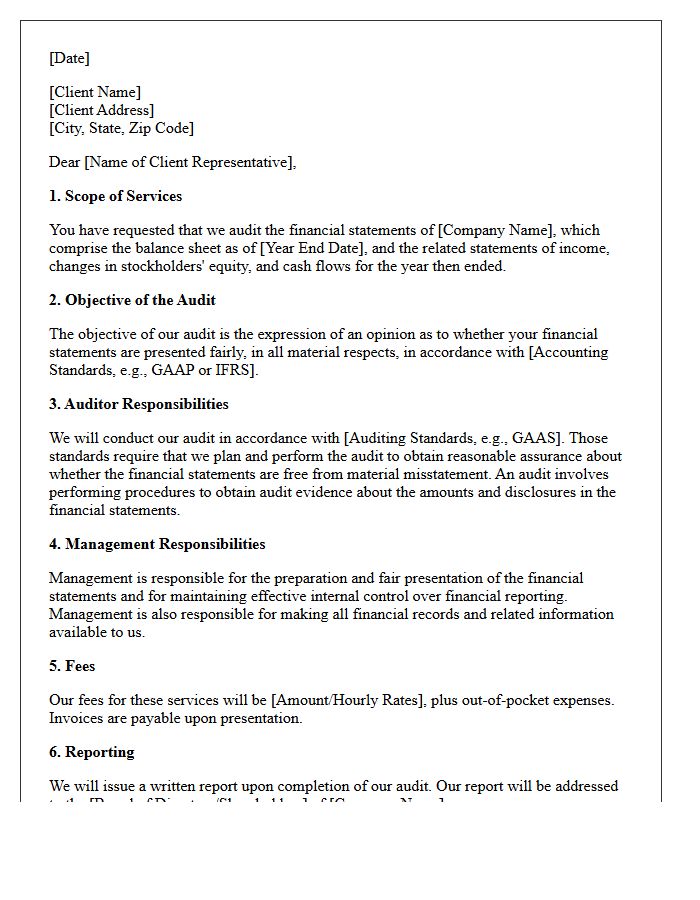

Financial Statement Audit Engagement Letter

A financial statement audit engagement letter is a formal contract that defines the scope, objectives, and limitations of the auditing process. It clarifies the responsibilities of management, such as maintaining internal controls and providing accurate financial records. This document establishes the auditor's obligations and the agreed-upon fee structure to prevent misunderstandings. By signing, both parties acknowledge the legal framework and professional standards, such as GAAS, that govern the relationship. It serves as a critical legal safeguard that ensures transparency and sets clear expectations before the audit fieldwork begins.

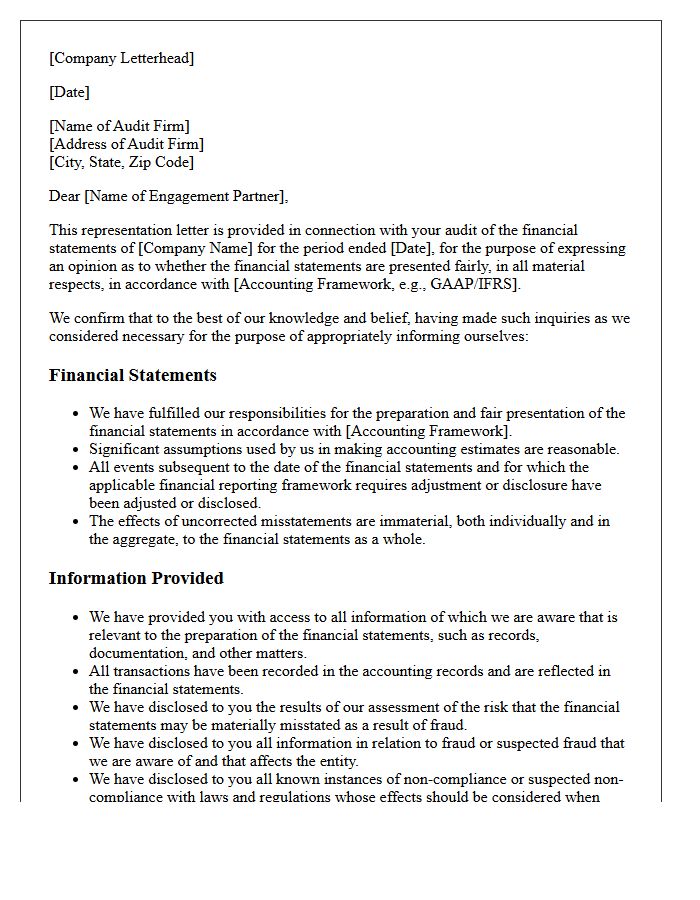

Management Representation Letter

A Management Representation Letter is a formal document provided by company executives to external auditors. It confirms the accuracy and completeness of the financial statements and the internal controls maintained during the period. This letter serves as critical audit evidence, documenting that management has disclosed all relevant liabilities, assets, and potential legal contingencies. By signing, leadership accepts primary responsibility for the financial data, reducing the auditor's risk of material misstatement and ensuring transparency throughout the verification process.

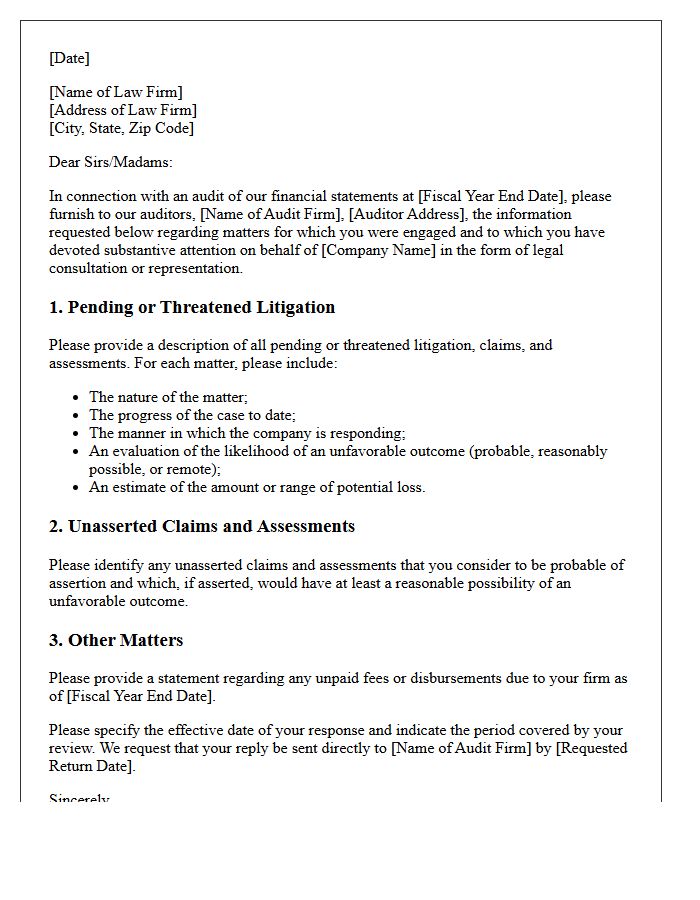

Legal Counsel Audit Inquiry Letter

A Legal Counsel Audit Inquiry Letter is a formal request sent by a company to its external legal counsel at the behest of independent auditors. Its primary purpose is to identify contingent liabilities, such as pending or threatened litigation, that could materially affect financial statements. This communication ensures financial transparency and compliance with accounting standards like ASC 450. Counsel must evaluate the probability of an unfavorable outcome and provide loss estimates, helping auditors verify that all potential legal risks are accurately disclosed to stakeholders and regulators.

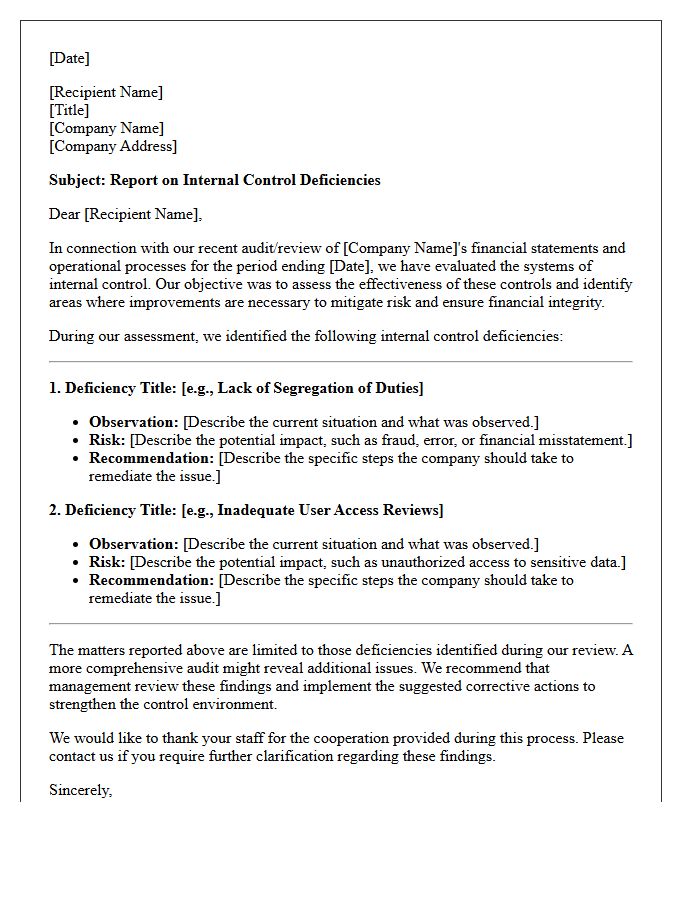

Internal Control Deficiencies Letter

An Internal Control Deficiencies Letter is a formal communication from auditors to management identifying weaknesses in financial reporting processes. It categorizes issues as significant deficiencies or material weaknesses that could lead to errors. Understanding this document is crucial for risk management and regulatory compliance. Organizations must address these findings promptly to improve operational integrity, protect assets, and ensure accurate financial disclosures. Proactive remediation strengthens internal governance and builds stakeholder confidence by demonstrating a commitment to sound financial oversight and accountability.

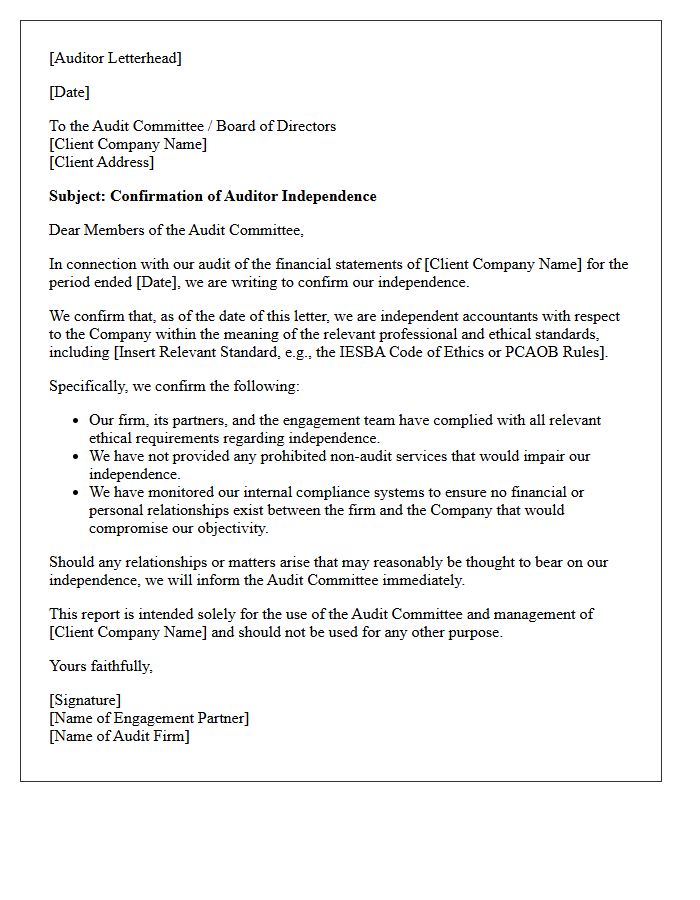

Auditor Independence Confirmation Letter

An Auditor Independence Confirmation Letter is a formal document issued by an external auditor to a company's audit committee. It confirms that the auditing firm remains objective and free from conflicts of interest that could bias their financial evaluation. This letter ensures compliance with regulatory standards like SOX or ethics codes. It typically details any relationships or non-audit services provided, verifying that the auditor's integrity is maintained. Receiving this confirmation is a critical step in the annual audit process to guarantee the reliability of financial reporting for stakeholders.

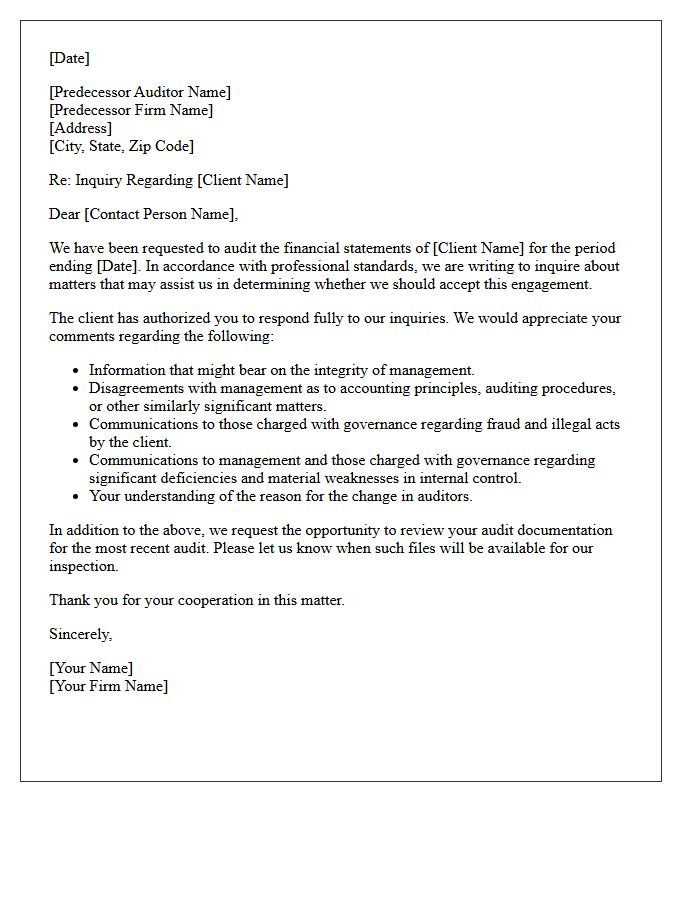

Predecessor Auditor Communication Letter

A Predecessor Auditor Communication Letter is a mandatory ethical requirement under auditing standards before accepting a new engagement. The successor auditor must initiate professional inquiries to identify any integrity issues, disagreements with management regarding accounting principles, or evidence of fraud. This process ensures transparency and helps the new auditor assess if there are reasons to decline the appointment. Obtaining the client's written consent is essential to authorize this exchange of confidential information between the previous and prospective audit firms.

Audit Committee Communication Letter

The Audit Committee Communication Letter, often referred to as the SAS 114 or AU-C 260, serves as a vital bridge between external auditors and those charged with governance. This document ensures transparency regarding the financial reporting process, internal control deficiencies, and any disagreements with management. It outlines the auditor's responsibilities, the planned scope of the audit, and significant findings. Understanding this letter is essential for oversight, as it highlights potential risks and provides independent insights into the integrity of an organization's financial health and regulatory compliance.

Going Concern Evaluation Letter

A Going Concern Evaluation Letter is a critical audit document assessing if a company can sustain operations for the next twelve months. It highlights potential liquidity risks, substantial operating losses, or loan defaults that may threaten business continuity. If auditors doubt a firm's survival, they issue a qualified opinion. This evaluation is essential for investors and creditors to gauge financial stability and long-term viability. Understanding these disclosures is vital for risk management, as they signal whether a company requires urgent restructuring or additional capital to remain functional and avoid insolvency.

Related Party Transaction Inquiry Letter

A Related Party Transaction Inquiry Letter is a formal audit procedure used to identify conflicts of interest between a company and its internal affiliates. It requires directors and management to disclose financial dealings with family members, subsidiaries, or entities they control. This document is essential for financial transparency and ensures that all material transactions are conducted at arm's length. Accurate responses are critical to prevent fraud, meet regulatory compliance standards, and maintain investor confidence by revealing potential self-dealing or hidden liabilities that could impact the entity's true financial position.

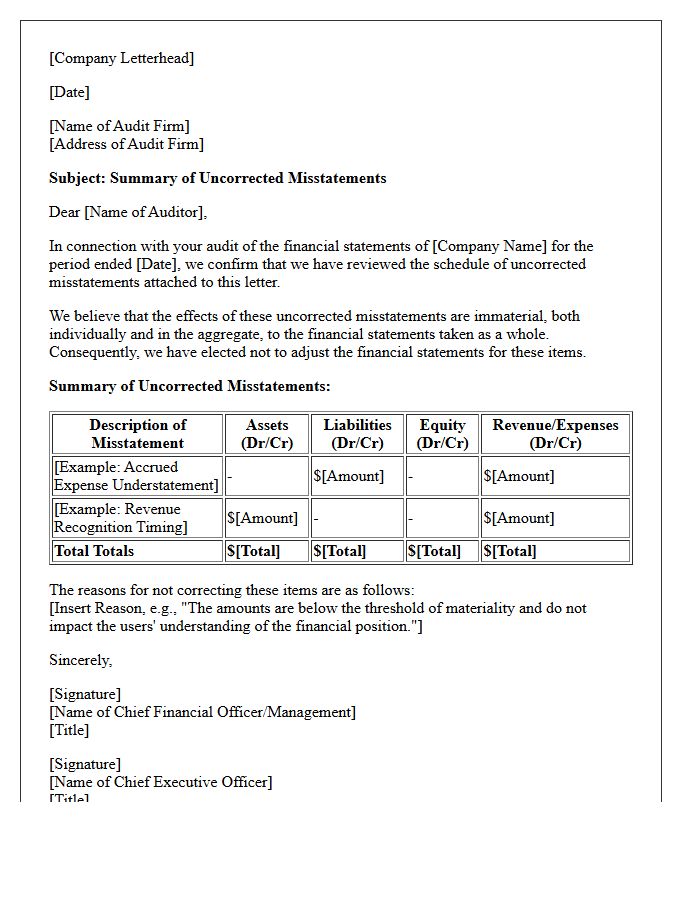

Uncorrected Misstatements Letter

An Uncorrected Misstatements Letter, often called a Summary of Uncorrected Misstatements, is a critical document provided by auditors to management. It lists identified financial errors that were not adjusted in the books. To finalize the audit, management must sign a representation letter confirming these discrepancies are immaterial, both individually and in aggregate. This process ensures transparency and confirms that any remaining inaccuracies do not mislead stakeholders or significantly impact the overall fairness of the entity's financial statements.

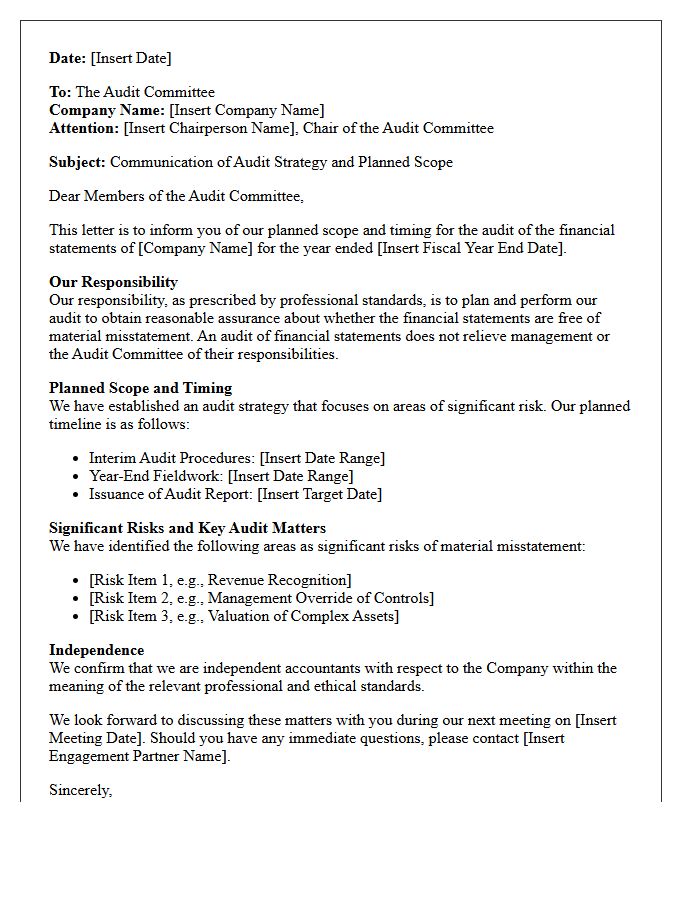

Audit Strategy Communication Letter

The Audit Strategy Communication Letter is a mandatory document sent by auditors to those charged with governance. It outlines the planned scope and timing of the audit, ensuring transparency regarding significant risks and the overall approach. This formal communication establishes an effective two-way dialogue, helping directors understand the auditor's responsibilities while identifying potential issues early. By detailing the resource allocation and audit methodology, it ensures that all parties are aligned, ultimately enhancing the integrity and efficiency of the financial reporting process.

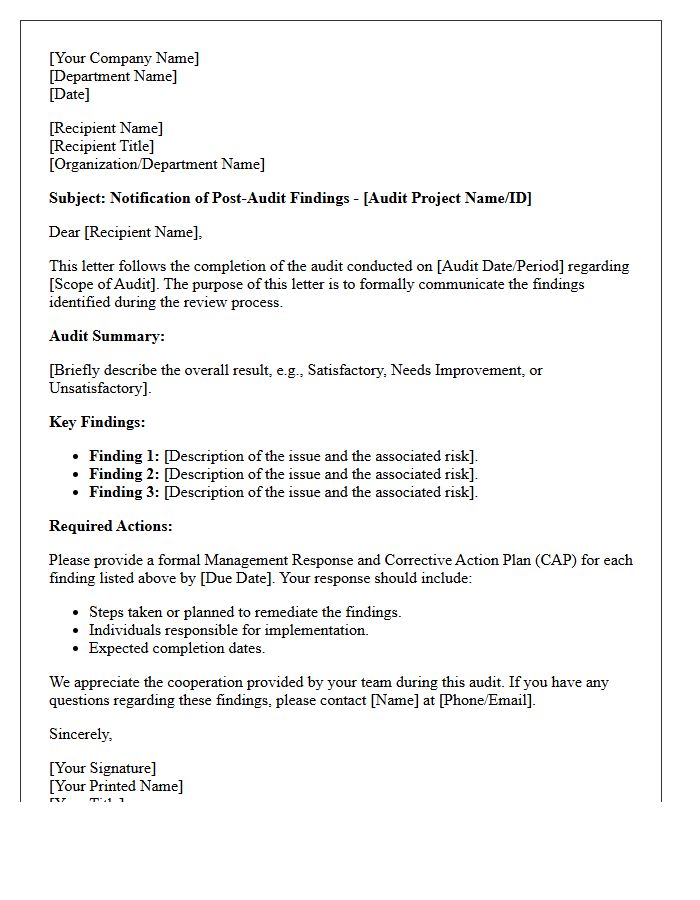

Post-Audit Findings Letter

A Post-Audit Findings Letter is a formal document issued by auditors after completing an examination of financial records. It outlines specific deficiencies, material weaknesses, or non-compliance issues identified during the process. This letter serves as a critical communication tool for management to understand internal control gaps and operational risks. Recipients must provide a timely management response detailing corrective actions. Understanding these findings is essential for improving financial integrity, ensuring regulatory adherence, and strengthening organizational governance to prevent future discrepancies or legal complications.

What is a Financial Statement Audit Engagement Letter?

An engagement letter is a legally binding contract that outlines the scope, objective, and terms of an audit agreement between a client and an independent public accounting firm. It defines the responsibilities of both management and the auditor to ensure mutual understanding before the audit begins.

What are the primary objectives of an audit engagement letter?

The primary objectives are to document the agreed-upon terms of the audit, specify the financial reporting framework being used (such as GAAP or IFRS), and limit potential legal liability by clearly defining the services to be performed and the limitations of the audit process.

What responsibilities of management are outlined in the engagement letter?

Management is responsible for the preparation and fair presentation of financial statements, maintaining effective internal controls, and providing the auditor with unrestricted access to all personnel, records, and relevant documentation required to complete the audit.

Does an audit engagement letter guarantee the detection of fraud?

No, the engagement letter states that while an audit is designed to provide reasonable assurance against material misstatements, it is not specifically designed to detect all instances of fraud or internal control deficiencies due to the inherent limitations of audit testing.

What fee structures and payment terms are included in the letter?

The letter typically specifies the estimated professional fees, billing arrangements, and reimbursement policies for out-of-pocket expenses. It may also include clauses regarding additional costs if the scope of work changes or if management fails to provide necessary documentation in a timely manner.

Comments