A Homeowners Association Audit Engagement Letter serves as a formal contract between an HOA board and an independent CPA. It outlines the scope, objectives, and limitations of the financial audit to ensure transparency and legal compliance. This document protects both parties by defining responsibilities and fee structures. To help you draft your own, below are some ready to use template.

Image cover: Essential Templates and Samples for Your HOA Audit Engagement Letter

Letter Samples List

- Homeowners Association Audit Engagement Letter Date and Addressee

- Objective of the Homeowners Association Audit Engagement Letter

- Scope of the Accounting Firm Audit Letter

- Auditor Responsibilities Outlined in the Letter

- Homeowners Association Management Responsibilities Letter Clause

- Audit Engagement Letter Inherent Limitations

- Fraud and Error Detection Letter Provisions

- Financial Reporting Framework Letter Agreement

- Audit Engagement Letter Timing and Deliverables

- Accounting Firm Fees and Billing Letter Terms

- Audit Engagement Letter Dispute Resolution

- Acknowledgment and Acceptance Letter Signatures

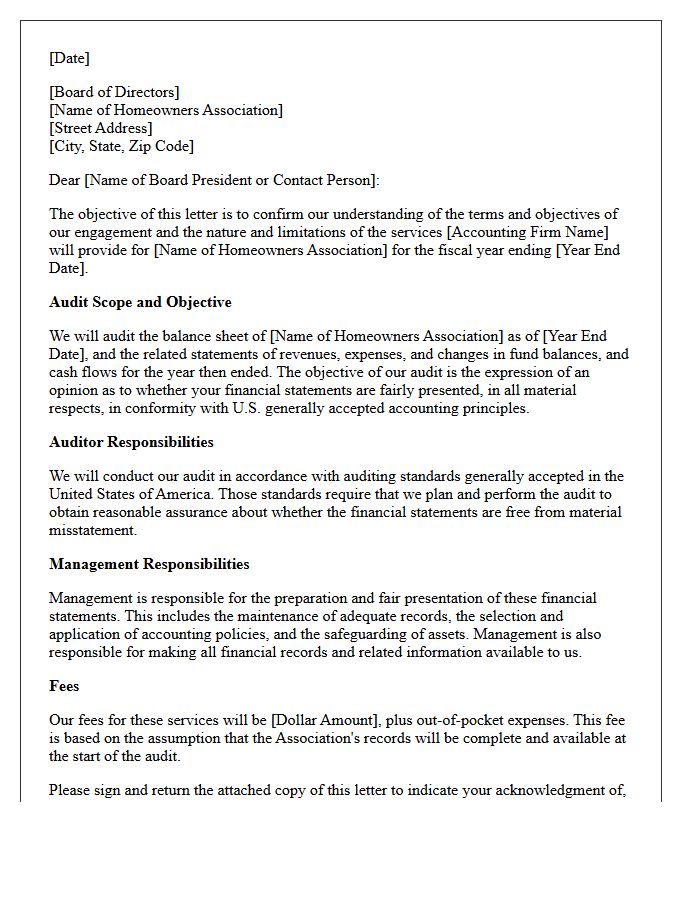

Homeowners Association Audit Engagement Letter Date and Addressee

The Homeowners Association Audit Engagement Letter must clearly state the Date and Addressee to establish a legal timeline and identify responsible parties. The date signifies the official start of the contractual agreement between the CPA and the HOA board. The addressee should specifically be the Board of Directors or the designated audit committee. Accurate details ensure that the scope of work is formally authorized for the correct fiscal period, protecting the association's legal interests while ensuring transparent communication between auditors and homeowners.

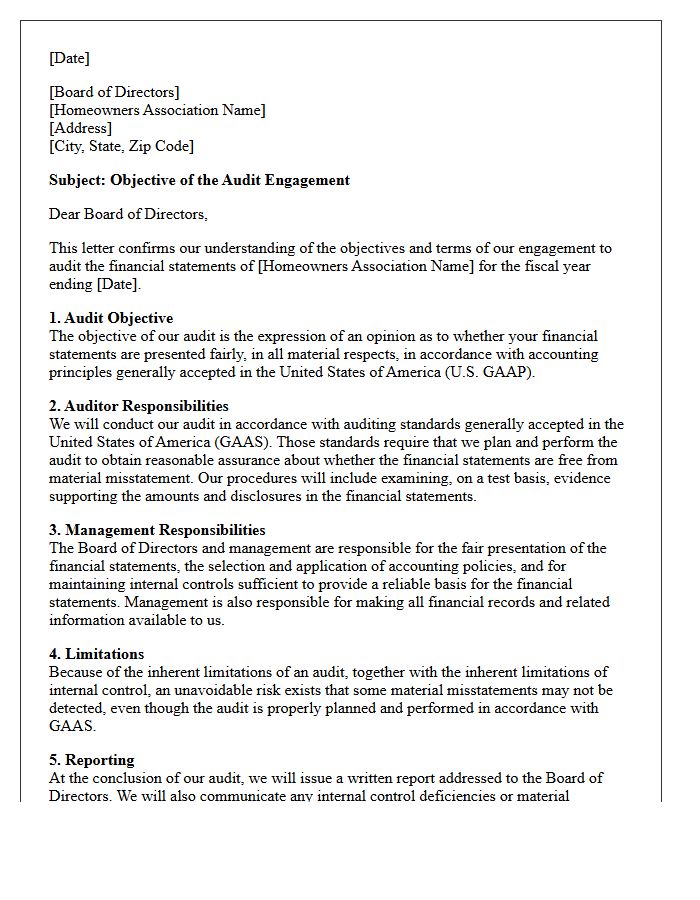

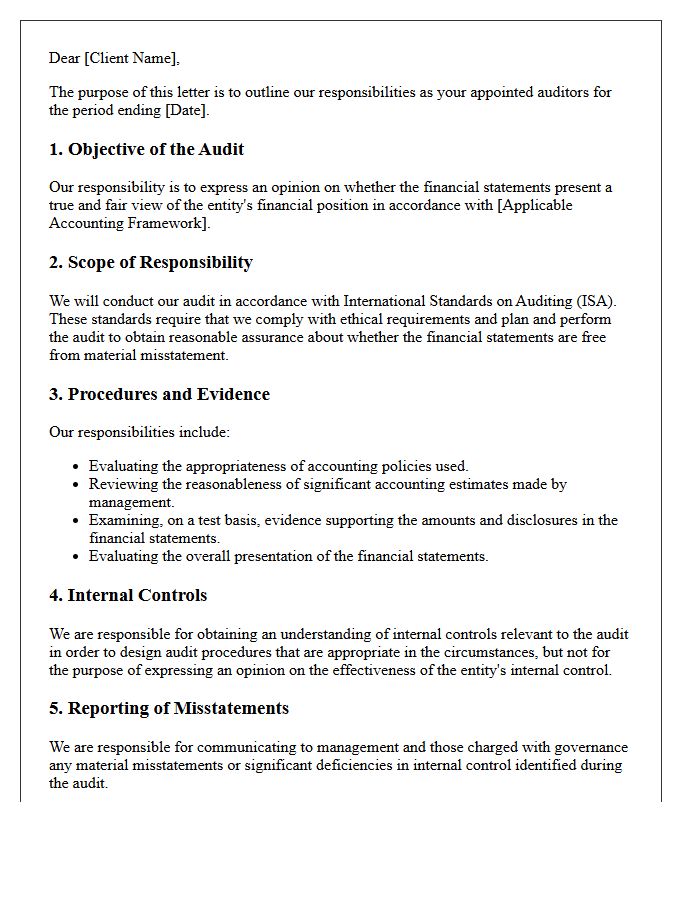

Objective of the Homeowners Association Audit Engagement Letter

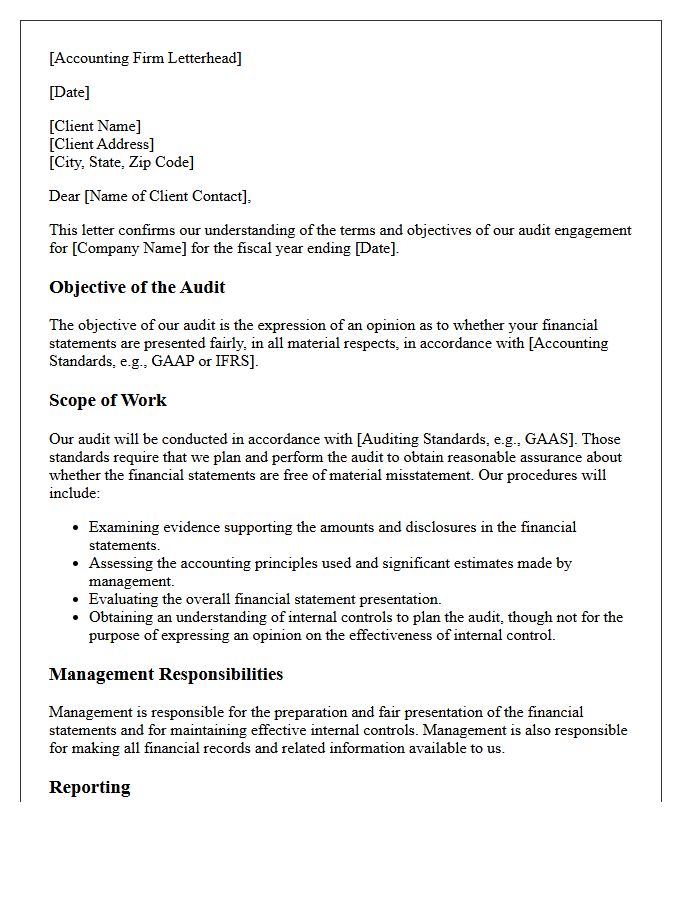

The primary objective of a Homeowners Association Audit Engagement Letter is to establish a formal agreement between the board and the auditor. It defines the scope of services, ensuring both parties understand the financial examination process. This document clarifies management's responsibilities regarding financial statements and internal controls while outlining the auditor's duty to report irregularities. By setting clear expectations for fees and deadlines, it minimizes legal risks and prevents misunderstandings, ensuring a transparent independent audit that maintains the fiscal integrity of the community association.

Scope of the Accounting Firm Audit Letter

The audit inquiry letter is a critical communication sent from a client to its legal counsel at the auditor's request. Its primary scope is to identify potential legal liabilities, pending litigation, and unasserted claims that could materially impact financial statements. This process ensures transparency regarding financial risks and guarantees that all significant contingencies are accurately disclosed to stakeholders. By confirming the status of legal matters, the letter provides essential audit evidence to verify the integrity and completeness of a company's reported financial position.

Auditor Responsibilities Outlined in the Letter

The engagement letter serves as a formal contract defining the auditor responsibilities during a financial review. It specifies that auditors must perform procedures to obtain reasonable assurance about whether financial statements are free from material misstatement. A critical highlighted term is professional skepticism, which auditors must maintain throughout the process. They are responsible for evaluating internal controls and reporting significant deficiencies. However, the letter clarifies that the audit is not a guarantee against fraud, emphasizing that primary responsibility for financial integrity remains with management while auditors provide an independent opinion.

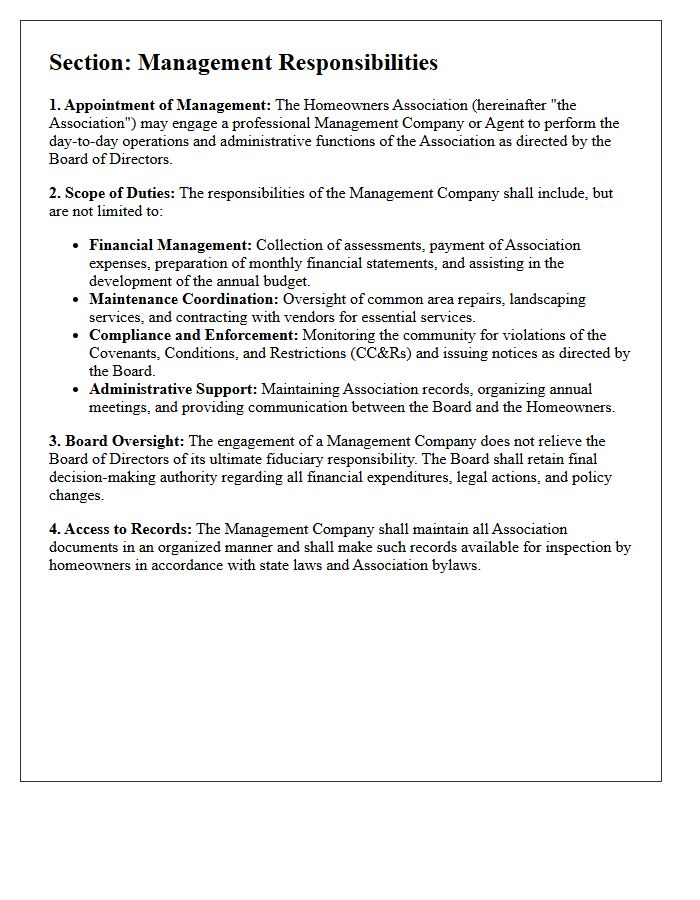

Homeowners Association Management Responsibilities Letter Clause

A Homeowners Association Management Responsibilities clause clearly defines the legal obligations of the management company versus the board. It typically outlines essential tasks such as financial reporting, maintenance supervision, and rule enforcement. Understanding this clause is vital for ensuring accountability and preventing service overlaps. Property owners should verify specific performance standards and notice requirements within the text to protect the community's interests. This legal provision serves as the primary framework for operational transparency and efficient neighborhood governance.

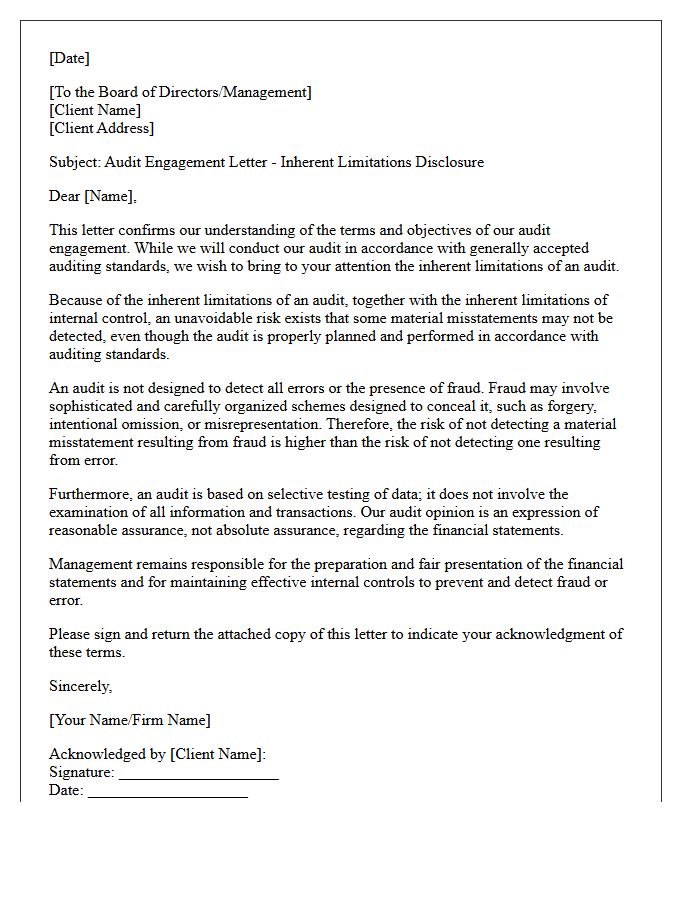

Audit Engagement Letter Inherent Limitations

An audit engagement letter formalizes the contractual relationship while explicitly outlining inherent limitations. Even a properly planned audit cannot guarantee the discovery of all material misstatements due to the nature of financial reporting. Limitations arise from the use of selective testing, the use of professional judgment, and the possibility of collusion or management override of controls. Consequently, an audit provides reasonable assurance rather than an absolute guarantee. Understanding these constraints is essential to managing expectations regarding the auditor's responsibility for detecting fraud or errors within the financial statements.

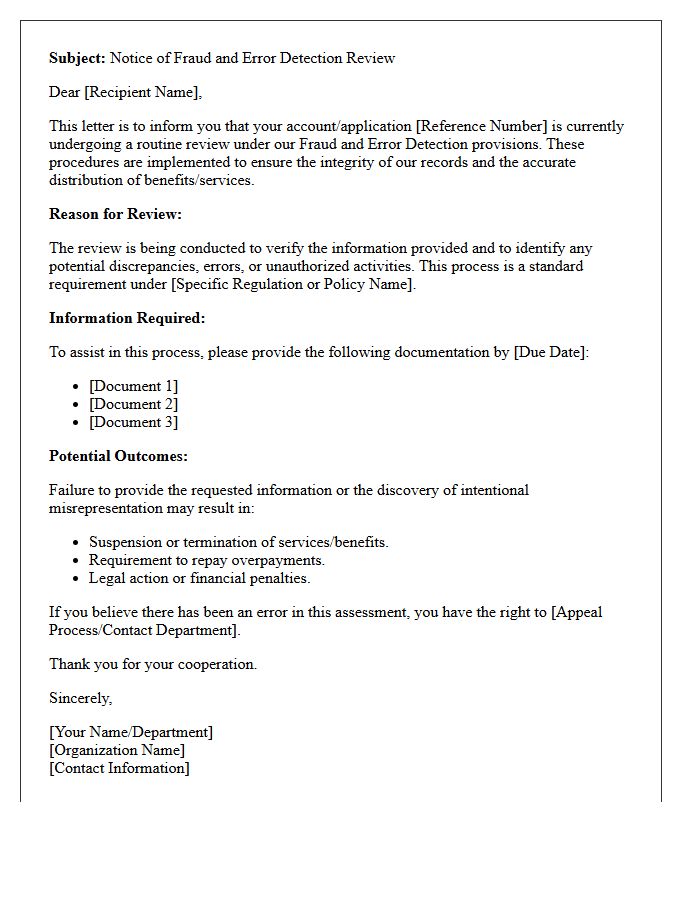

Fraud and Error Detection Letter Provisions

The Fraud and Error Detection Letter is a formal notice issued when authorities identify discrepancies in reported financial data or eligibility claims. These provisions require recipients to provide verifiable evidence to reconcile information gaps. Failure to respond within the specified timeframe can lead to the suspension of benefits, financial penalties, or legal action. It is essential to review the specific compliance deadlines mentioned in the letter to ensure accuracy and avoid accusations of intentional misrepresentation. Promptly addressing these inquiries protects your legal standing and ensures continued access to authorized services or funds.

Financial Reporting Framework Letter Agreement

A Financial Reporting Framework Letter Agreement is a formal contract between a lender and a borrower that specifies the accounting standards used to prepare financial statements. It ensures consistent data presentation, typically requiring compliance with GAAP or IFRS. This agreement is crucial for credit monitoring, as it dictates how financial covenants are calculated. If a borrower changes their reporting methods, they must notify the lender to prevent technical defaults. Understanding these requirements is essential for maintaining regulatory transparency and ensuring ongoing loan compliance throughout the life of the debt facility.

Audit Engagement Letter Timing and Deliverables

An audit engagement letter must be signed before any fieldwork begins to establish a formal legal contract between the auditor and client. This timing ensures both parties agree on the scope of work and responsibilities from the start. Key deliverables specified in the document include the independent auditor's report, management letters, and required internal control communications. Adhering to these timelines prevents compliance risks and ensures the timely filing of financial statements with regulatory bodies. Clear expectations regarding deadlines and reporting formats are essential for a successful audit process.

Accounting Firm Fees and Billing Letter Terms

When reviewing an engagement letter, it is crucial to understand the billing structure to avoid unexpected costs. Most accounting firms utilize fixed-fee arrangements for standard compliance or hourly rates for complex advisory work. Key terms often include retainer requirements, payment deadlines, and out-of-pocket expense reimbursements. Always verify the scope of work to ensure additional services do not trigger extra charges. Clear communication regarding late payment penalties and dispute resolution processes ensures a transparent financial relationship between the client and the firm.

Audit Engagement Letter Dispute Resolution

An Audit Engagement Letter must clearly define dispute resolution mechanisms to mitigate legal risks. These clauses typically specify whether conflicts will be settled through binding arbitration, mediation, or court litigation. Establishing a predetermined venue and governing law ensures both the auditor and the client understand their rights and obligations should a disagreement arise regarding fees, professional standards, or liability limits. Proactively addressing these terms helps maintain professional relationships and minimizes costly legal exposure during financial oversight engagements.

Acknowledgment and Acceptance Letter Signatures

An acknowledgment and acceptance letter serves as a binding confirmation that a party has received, understood, and agreed to specific terms or conditions. For these documents to be legally enforceable, the authorized signatures must be applied by individuals with the legal capacity to enter into agreements. Proper execution ensures clarity, prevents future disputes, and provides a formal audit trail of consent. Always verify that all dates and names match the underlying contract to maintain full legal validity and professional compliance within any formal business or legal transaction.

What is a Homeowners Association (HOA) audit engagement letter?

An HOA audit engagement letter is a formal contract between a homeowners association's board of directors and a Certified Public Accountant (CPA) that defines the scope, objectives, and limitations of the financial audit services to be performed.

Why is an engagement letter required before starting an HOA audit?

The engagement letter is required by professional accounting standards to establish a clear legal agreement, ensuring both the HOA board and the auditor understand their respective responsibilities, the timeline for completion, and the fee structure.

What specific information should be included in an HOA audit engagement letter?

The letter should detail the period being audited, the financial reporting framework used (such as GAAP), the auditor's responsibility to detect material misstatements, and the board's duty to provide access to all financial records and meeting minutes.

Can an engagement letter protect the HOA board from liability?

While the letter outlines the auditor's duties, its primary purpose is to clarify that the board remains responsible for the association's internal controls and the accuracy of the financial statements, thereby preventing misunderstandings regarding the audit's scope.

Does the HOA audit engagement letter cover tax preparation services?

Not necessarily. Tax preparation and the annual financial audit are separate services; therefore, the engagement letter must explicitly state whether tax filing (Form 1120-H) is included or if it requires a separate agreement.

Comments