An Internal Control Assessment Engagement Letter formalizes the agreement between an auditor and a client. It outlines the scope, objectives, and responsibilities involved in evaluating financial safeguards and operational efficiencies. This document ensures legal clarity and professional standards are met before the review begins. To help you get started, below are some ready to use template options.

Image cover: Professional Engagement Letter Templates for Internal Control Assessments

Letter Samples List

- Internal Control Assessment Engagement Letter

- Management Representation Letter

- Internal Control Deficiency Communication Letter

- Significant Deficiency and Material Weakness Letter

- Internal Audit Reliance Letter

- Process Walkthrough Confirmation Letter

- Draft Findings Communication Letter

- Management Response and Action Plan Letter

- Audit Committee Status Update Letter

- Remediation Testing Engagement Letter

- Final Internal Control Assessment Letter

- Engagement Termination Letter

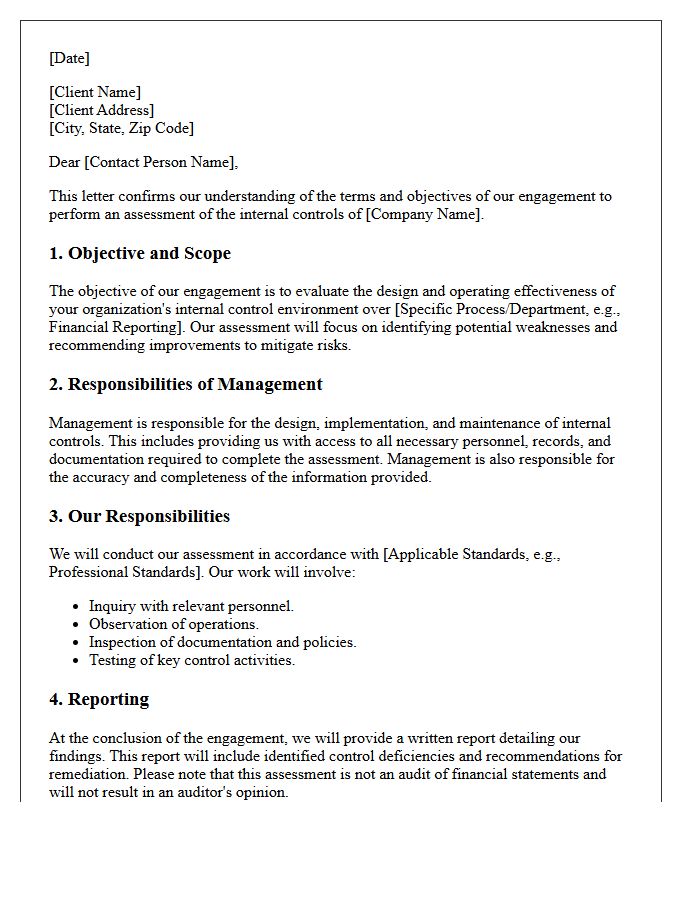

Internal Control Assessment Engagement Letter

An Internal Control Assessment Engagement Letter is a formal contract between a business and an auditor. It outlines the scope of work, objectives, and responsibilities for evaluating the organization's financial reporting and operational safeguards. This document prevents misunderstandings by detailing reporting requirements, fee structures, and the methodology used to identify internal weaknesses. Signing this letter is a critical first step to ensure legal compliance and establish clear expectations for strengthening risk management frameworks and safeguarding company assets through objective, third-party verification.

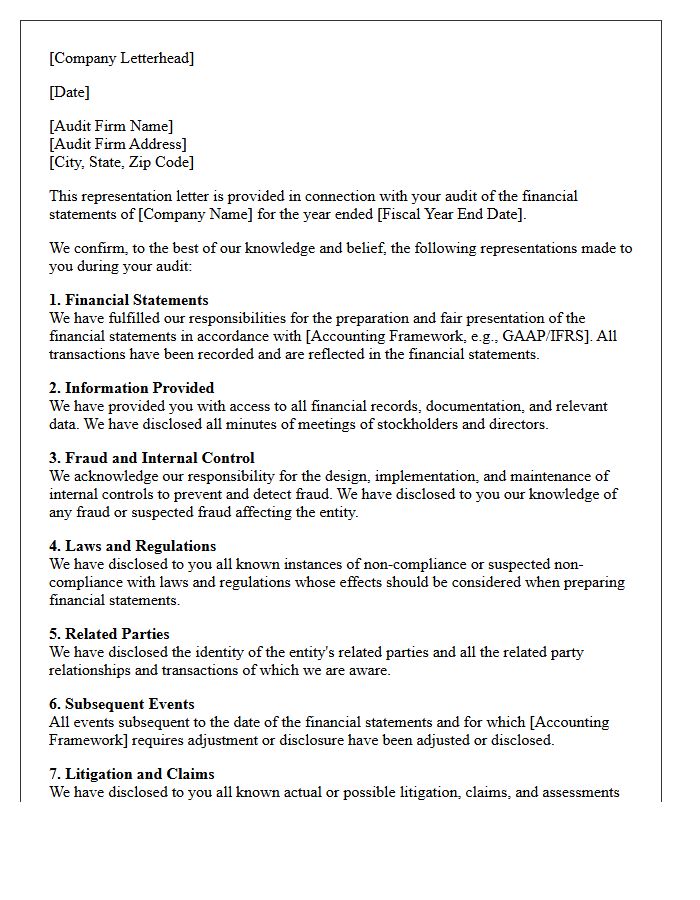

Management Representation Letter

A Management Representation Letter is a formal document provided by company executives to external auditors. It confirms the accuracy and completeness of the financial statements and internal controls discussed during an audit. This letter serves as legal evidence that management has disclosed all relevant facts, including potential liabilities and fraud risks. By signing this document, management accepts primary responsibility for the financial data, protecting auditors from liabilities related to misrepresentation. It is a mandatory requirement for completing an audit and ensures transparency between the organization and its stakeholders.

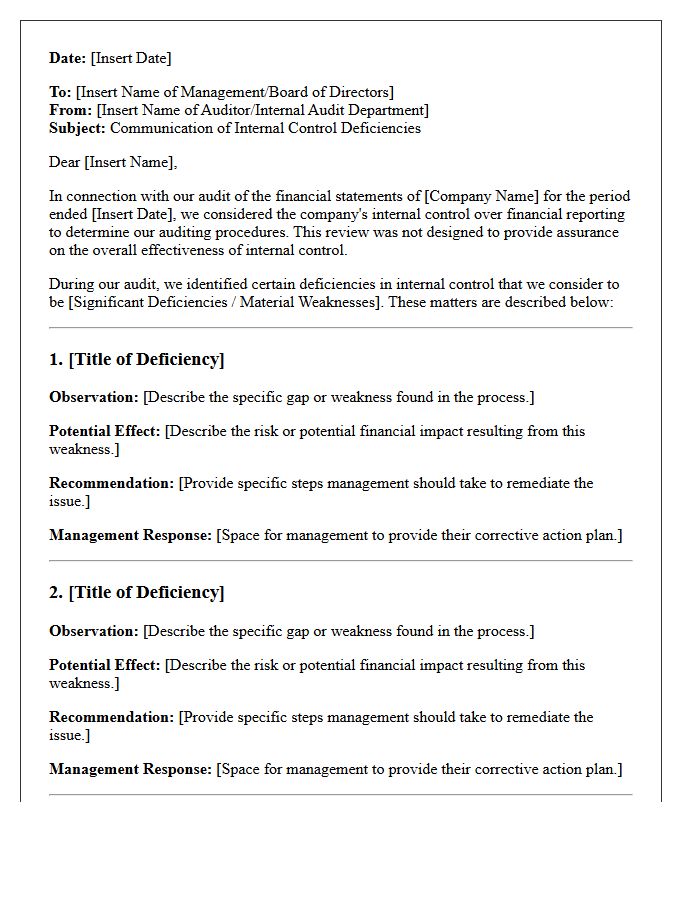

Internal Control Deficiency Communication Letter

An Internal Control Deficiency Communication Letter is a formal document issued by auditors to management and those charged with governance. It identifies material weaknesses or significant deficiencies discovered during a financial audit. The primary purpose is to highlight operational risks and provide remediation recommendations to strengthen the organization's control environment. Timely communication ensures that leadership can address security gaps, prevent fraud, and improve the accuracy of financial reporting. This letter serves as a critical tool for maintaining regulatory compliance and enhancing overall corporate governance through transparent reporting of systemic vulnerabilities.

Significant Deficiency and Material Weakness Letter

A Significant Deficiency and Material Weakness Letter is a formal communication from auditors to management identifying internal control failures. A material weakness represents the most severe risk, indicating a reasonable possibility that a financial misstatement will not be prevented or detected. A significant deficiency is less severe but still warrants attention from those charged with governance. These letters are critical for regulatory compliance and financial integrity, as they highlight systemic vulnerabilities that require immediate remediation to ensure accurate reporting and protect stakeholder interests.

Internal Audit Reliance Letter

An Internal Audit Reliance Letter is a formal document used by external auditors to confirm their intent to utilize the work performed by a company's internal audit function. This letter establishes the scope and reliability of internal controls testing to reduce duplicative efforts. It outlines the specific audit procedures, professional standards, and levels of independence required for the external firm to trust internal findings. Understanding this coordination is essential for improving audit efficiency and ensuring a seamless regulatory compliance process during year-end financial reporting.

Process Walkthrough Confirmation Letter

A Process Walkthrough Confirmation Letter serves as a formal verification document between auditors and management. It outlines the specific steps of a business procedure to ensure internal controls are functioning as designed. By signing this document, stakeholders confirm that the documented workflow accurately reflects real-world operations, identifying potential gaps or risks early in the audit process. This step is essential for maintaining compliance and providing a clear audit trail for regulatory standards, ensuring that all parties agree on the operational facts before testing begins.

Draft Findings Communication Letter

A Draft Findings Communication Letter is a formal document used during audits to present preliminary observations to management. It ensures transparency by allowing stakeholders to review, validate, and provide feedback on potential issues before the final report is issued. This collaborative process helps verify factual accuracy, clarifies complex findings, and facilitates the development of effective management action plans. Timely review of this letter is critical for maintaining audit integrity and ensuring that all identified control weaknesses are addressed accurately within the organizational context.

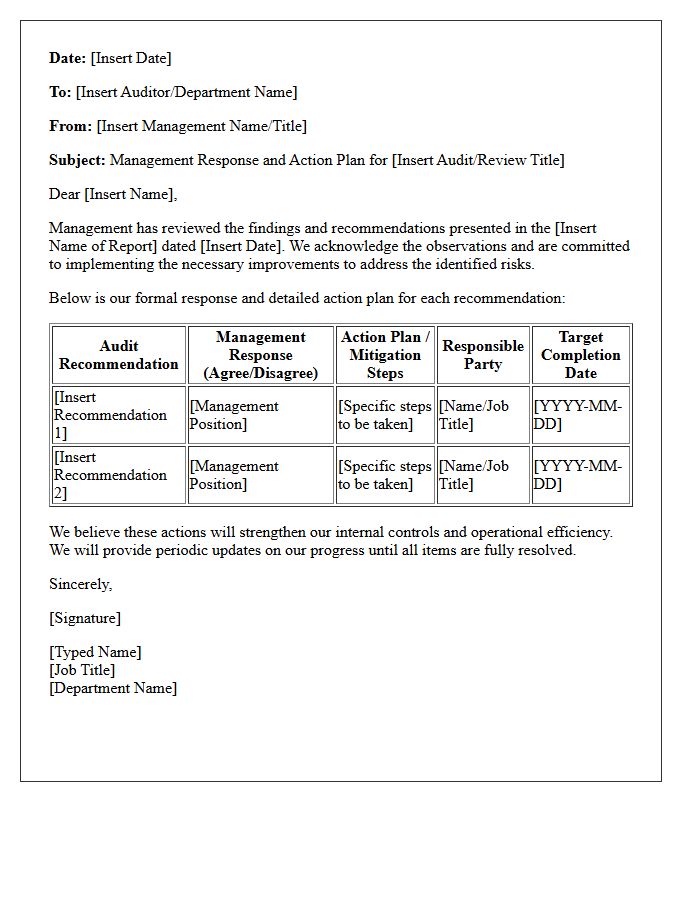

Management Response and Action Plan Letter

A Management Response and Action Plan (MRAP) letter is a formal document addressing audit findings. It outlines how leadership intends to resolve identified risks through specific remediation strategies. Each response must include a clear timeline and assign responsibility to a designated official. This ensures accountability and transparency throughout the corrective process. By detailing concrete steps to improve internal controls, the MRAP serves as a roadmap for organizational improvement and demonstrates a commitment to operational excellence and regulatory compliance.

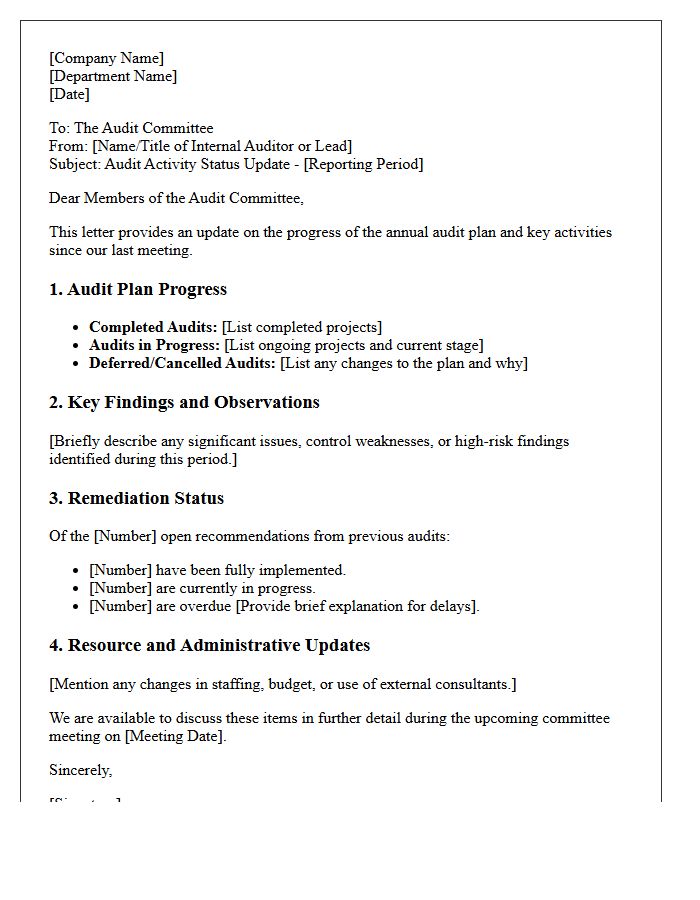

Audit Committee Status Update Letter

An Audit Committee Status Update Letter is a vital communication tool used to inform oversight bodies about the progress of internal or external reviews. It outlines completed milestones, identified risks, and any significant findings requiring immediate attention. This document ensures transparency, maintains accountability, and allows stakeholders to monitor whether the audit aligns with the established timeline and scope. By providing a clear roadmap of pending tasks and potential roadblocks, the update letter facilitates proactive decision-making and strengthens the organization's overall governance and financial integrity protocols.

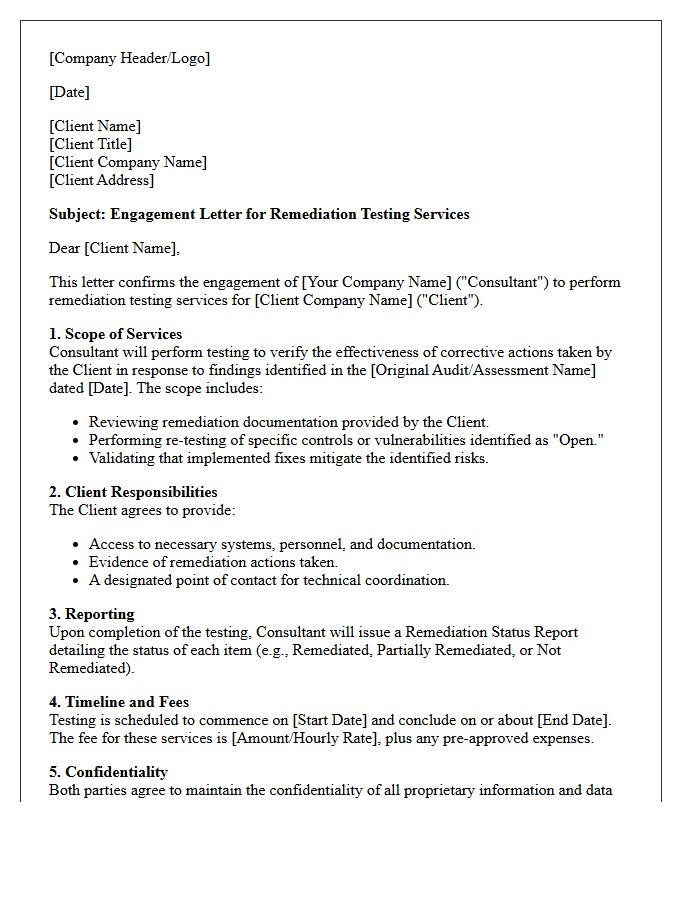

Remediation Testing Engagement Letter

A Remediation Testing Engagement Letter is a formal contract defining the scope and objectives of re-evaluating security vulnerabilities after corrective actions. It ensures both parties agree on the validation methodology, timelines, and specific systems to be re-tested. This document is essential for compliance and risk management, as it legally protects the service provider while documenting the effectiveness of implemented fixes. Establishing clear liability boundaries and reporting expectations within this letter guarantees a transparent process for confirming that identified threats have been successfully mitigated.

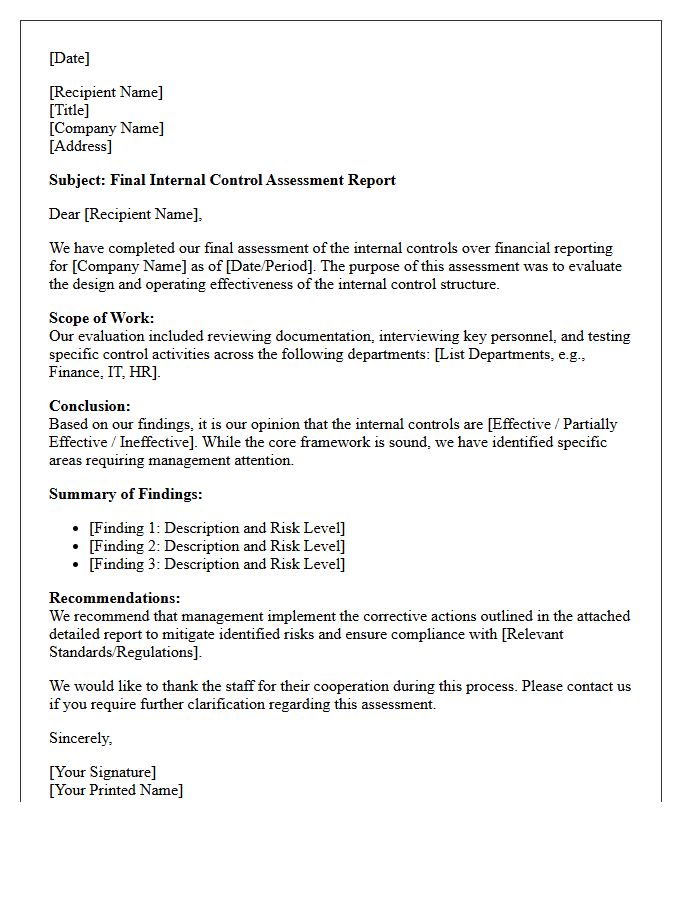

Final Internal Control Assessment Letter

The Final Internal Control Assessment Letter represents the definitive conclusion of an audit regarding an organization's financial oversight. It provides a formal evaluation of the effectiveness of internal protocols, identifying any material weaknesses or significant deficiencies. Stakeholders rely on this document to confirm that risk management processes are robust and compliant with regulatory standards. Understanding this letter is essential for ensuring operational integrity and facilitating transparent communication between management and auditors concerning necessary corrective actions to safeguard corporate assets.

Engagement Termination Letter

An Engagement Termination Letter is a formal document used to legally conclude a professional relationship between a service provider and a client. It clearly defines the effective end date, outlines outstanding obligations, and specifies the status of final payments or deliverables. Providing this written notice is essential for risk management, as it establishes a clear timeline and prevents future misunderstandings regarding project scope or liability. Using a professional tone ensures that the disengagement process remains respectful while protecting both parties' legal interests and ensuring a structured transition of responsibilities.

What is the primary purpose of an Internal Control Assessment Engagement Letter?

The engagement letter serves as a formal contract that defines the scope of the internal control review, establishes the responsibilities of both management and the practitioner, and outlines the objectives to prevent misunderstandings regarding the assessment's boundaries.

What are the key components included in an internal control engagement letter?

Essential components include the objective of the assessment, the specific internal control frameworks to be used (such as COSO), the responsibilities of management for maintaining controls, the limitations of the engagement, and the reporting deliverables.

How does the engagement letter define management's responsibility?

The letter explicitly states that management is responsible for the design, implementation, and maintenance of internal controls relevant to financial reporting, compliance, and operational efficiency, as well as providing the assessor with unrestricted access to records and personnel.

Does an Internal Control Assessment guarantee the detection of all fraud?

No, the engagement letter typically includes a limitation of liability clause stating that because of the inherent limitations of internal controls, including the possibility of management override or collusion, an assessment cannot provide absolute assurance that all errors or fraud will be detected.

When should an Internal Control Assessment Engagement Letter be updated?

The letter should be reviewed and updated annually or whenever there is a significant change in the scope of work, changes in regulatory requirements, or shifts in the organizational structure to ensure the terms remain accurate and legally binding.

Comments