An Unqualified Audit Opinion is the highest level of assurance a CPA provides, confirming that financial statements are presented fairly and follow GAAP standards. Often called a "clean report," it signals transparency and reliability to investors and lenders. Understanding its components is essential for corporate compliance and financial reporting accuracy. To help you get started, below are some ready to use template.

Image cover: Standard Templates and Examples for Unqualified Audit Opinion Letters

Letter Samples List

- Standard Unqualified Audit Opinion Letter

- Public Company Unqualified Audit Opinion Letter

- Private Entity Unqualified Audit Opinion Letter

- Consolidated Unqualified Audit Opinion Letter

- Comparative Unqualified Audit Opinion Letter

- Single Year Unqualified Audit Opinion Letter

- Statutory Unqualified Audit Opinion Letter

- Emphasis of Matter Unqualified Audit Opinion Letter

- Internal Control Unqualified Audit Opinion Letter

- Supplementary Information Unqualified Audit Opinion Letter

- Explanatory Paragraph Unqualified Audit Opinion Letter

- Joint Unqualified Audit Opinion Letter

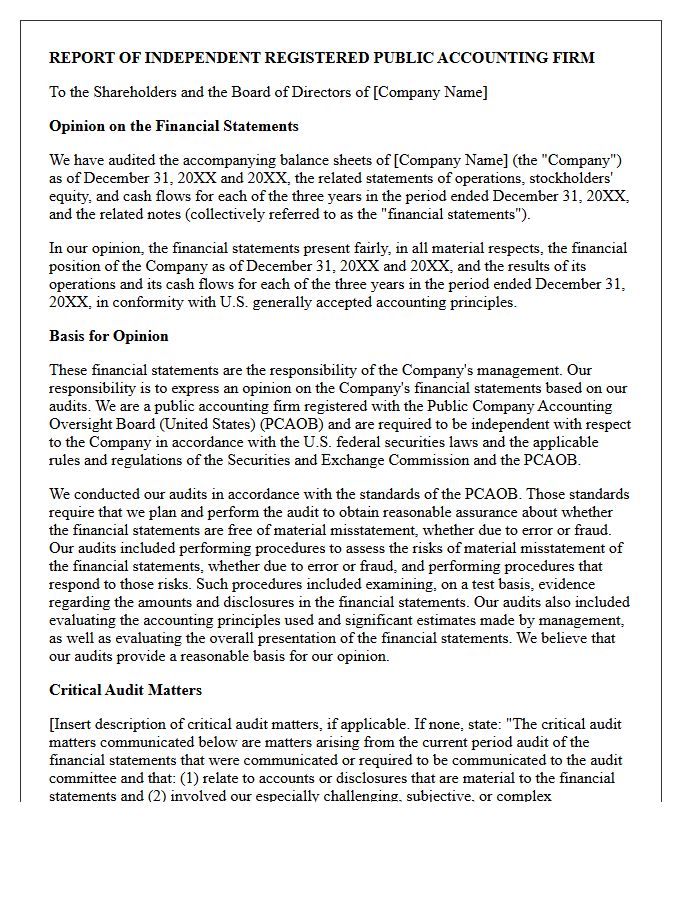

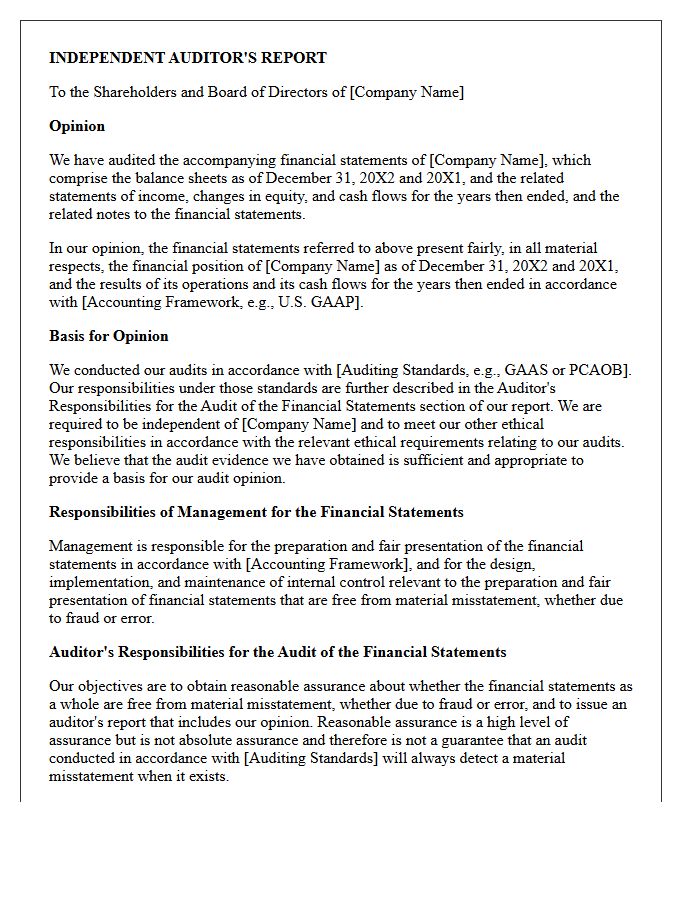

Standard Unqualified Audit Opinion Letter

A Standard Unqualified Audit Opinion Letter is the most favorable report an auditor issues. It confirms that a company's financial statements are presented fairly and comply with Generally Accepted Accounting Principles (GAAP). This "clean" opinion indicates that the financial records are free from material misstatements, providing stakeholders with high assurance regarding the entity's fiscal health. Investors and lenders rely on this document to verify transparency and accuracy before making financial decisions, as it signifies a transparent representation of the company's true economic position.

Public Company Unqualified Audit Opinion Letter

A Public Company Unqualified Audit Opinion Letter is the most favorable report a business can receive. It signifies that independent auditors have examined the financial statements and found them to be presented fairly in all material respects. This "clean" opinion confirms compliance with GAAP standards and provides investors with confidence in the data's reliability. It suggests no significant discrepancies or legal deviations were discovered during the audit process, ensuring transparency and building essential trust within the global capital markets.

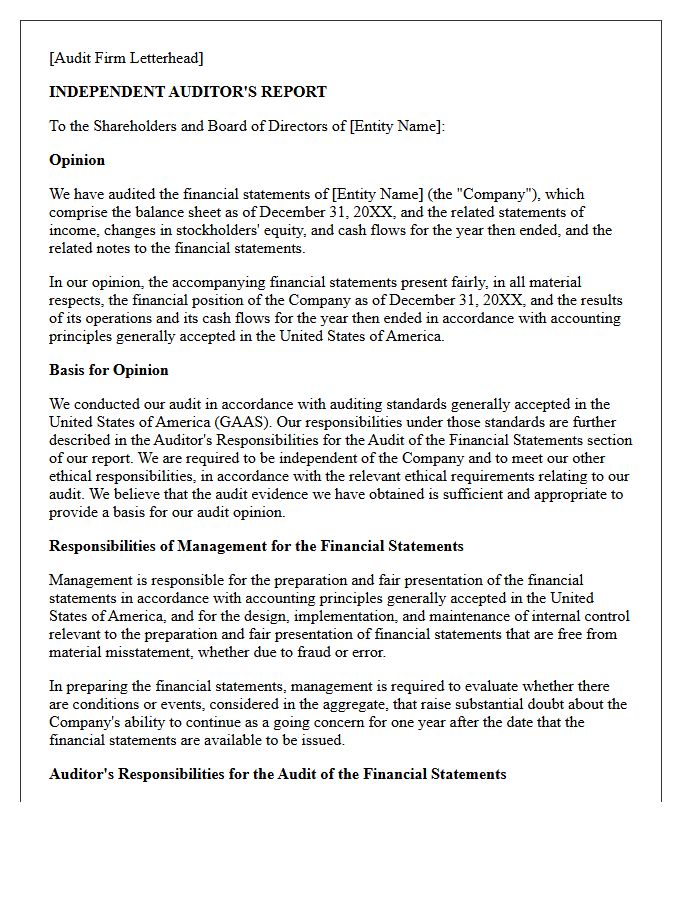

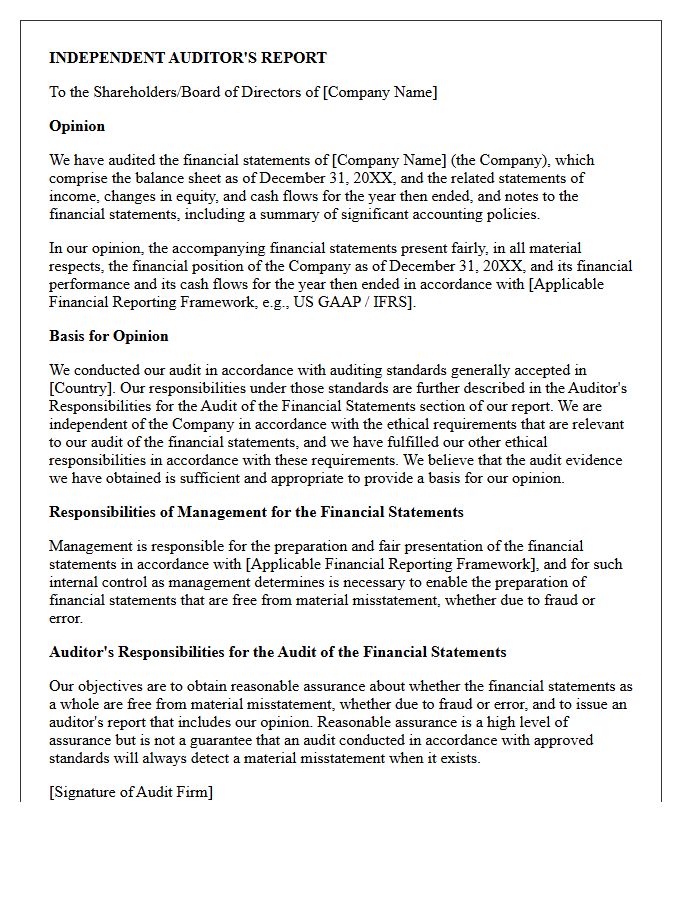

Private Entity Unqualified Audit Opinion Letter

A private entity unqualified audit opinion letter is a formal document issued by an independent auditor confirming that financial statements are presented fairly in all material respects. This clean report signifies that the company's accounting records adhere to GAAP standards without significant discrepancies. For private firms, this letter is crucial for maintaining financial credibility with lenders, investors, and stakeholders. It provides assurance that the entity's reported data is reliable, enhancing transparency and supporting informed business decisions during valuations or credit assessments.

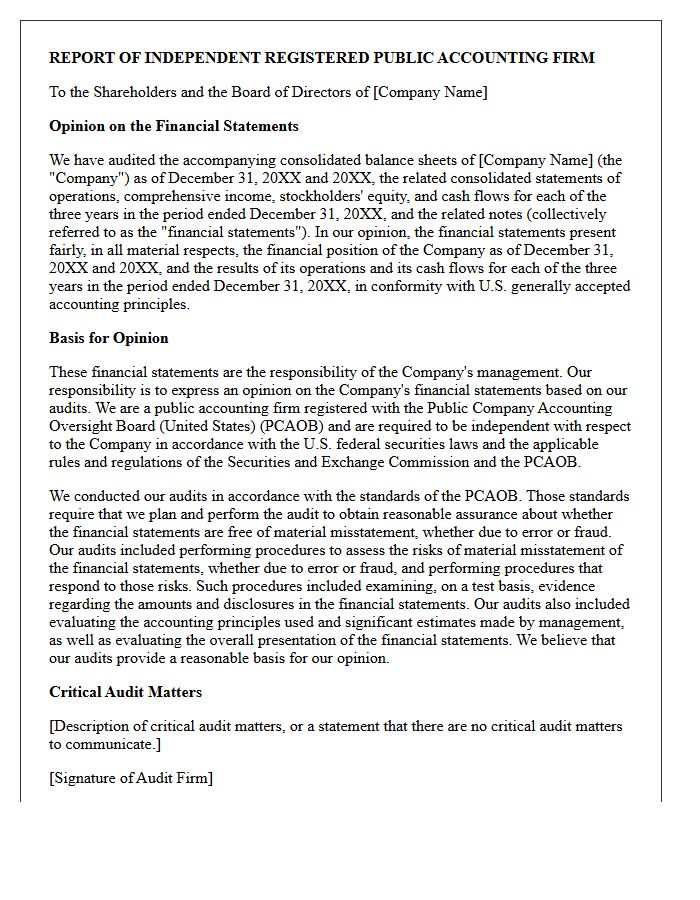

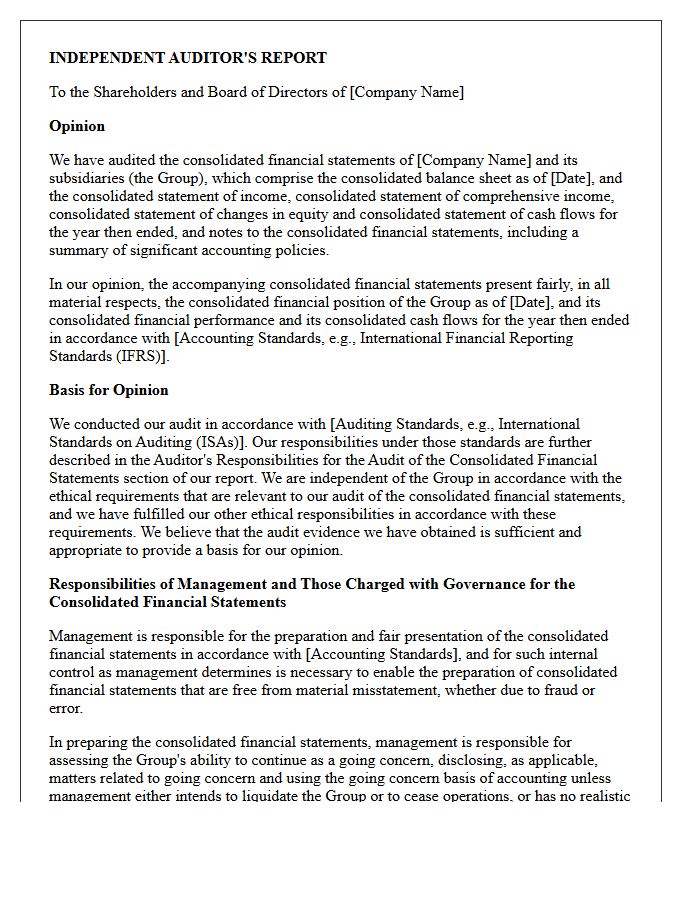

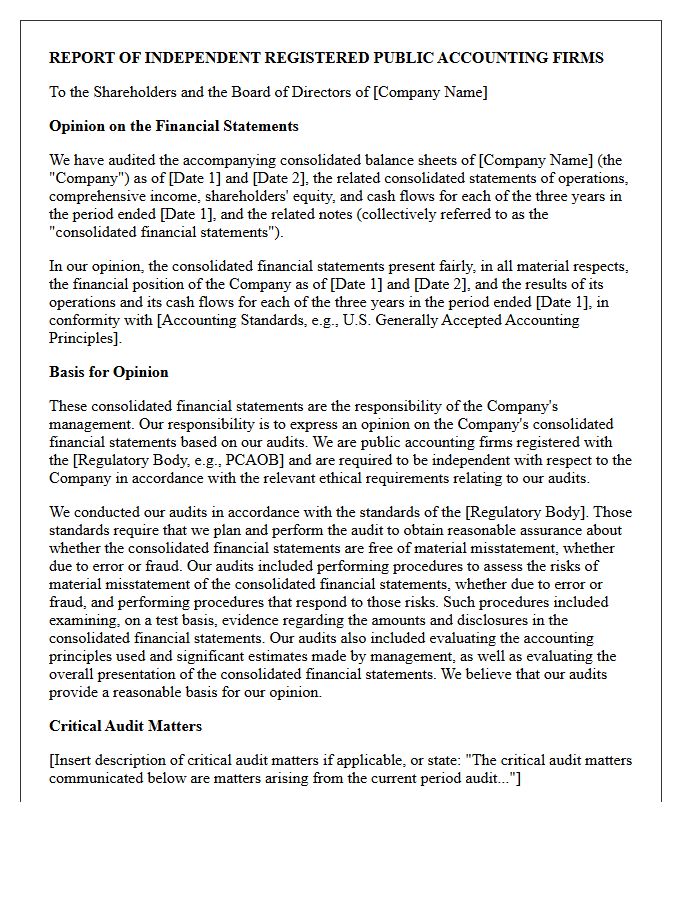

Consolidated Unqualified Audit Opinion Letter

A Consolidated Unqualified Audit Opinion Letter is the highest level of assurance an auditor provides. It signifies that a company's consolidated financial statements, including all subsidiaries, are presented fairly and comply with GAAP or IFRS standards. This "clean report" indicates no material misstatements were found across the entire corporate structure. For investors and lenders, this document is essential for verifying financial transparency and institutional credibility, confirming that the reported data is reliable for making informed economic decisions regarding the organization's overall health.

Comparative Unqualified Audit Opinion Letter

A comparative unqualified audit opinion letter confirms that a company's financial statements for multiple years are fairly presented in all material respects. This "clean" report signifies that the data follows Generally Accepted Accounting Principles (GAAP) without significant deviations. It provides stakeholders with assurance regarding the consistency and reliability of historical financial performance. By comparing the current period with previous years, the auditor verifies that accounting methods remain stable, allowing investors to make informed decisions based on credible, transparent, and standardized financial reporting across consecutive reporting cycles.

Single Year Unqualified Audit Opinion Letter

A Single Year Unqualified Audit Opinion Letter is the most favorable result in financial reporting. It signifies that an independent auditor found the financial statements to be presented fairly in all material respects. This clean bill of health confirms compliance with GAAP standards and validates the accuracy of the data. For stakeholders, this letter provides essential assurance regarding the entity's fiscal transparency. Obtaining an unqualified opinion is a critical benchmark for maintaining institutional credibility and securing future funding or investment opportunities.

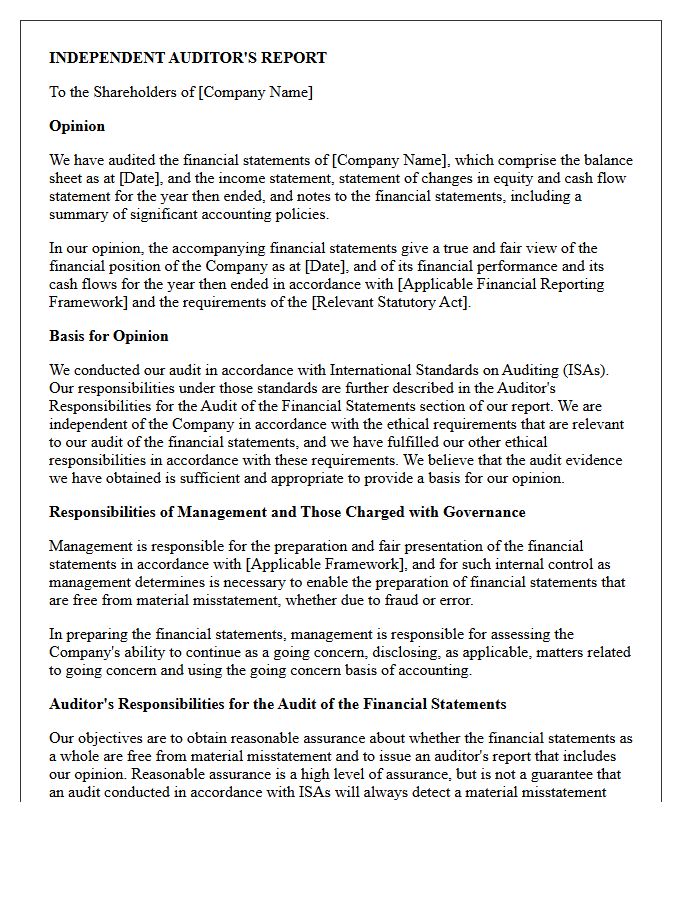

Statutory Unqualified Audit Opinion Letter

A Statutory Unqualified Audit Opinion Letter is the most favorable result of a financial examination. It confirms that an organization's financial statements are presented fairly and comply with Generally Accepted Accounting Principles (GAAP) or relevant legal frameworks. This "clean" report signifies that auditors found no material misstatements or compliance violations. For stakeholders and regulators, this document serves as a critical assurance of financial transparency and institutional integrity, indicating that the reported data is reliable and free from significant errors or fraudulent activities.

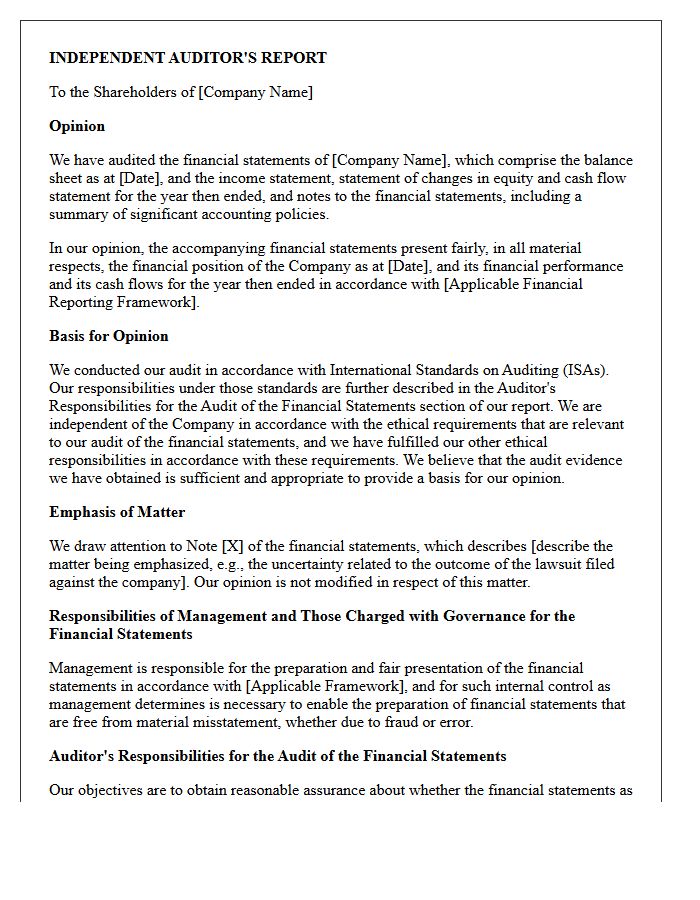

Emphasis of Matter Unqualified Audit Opinion Letter

An Emphasis of Matter is a specific paragraph added to an unqualified audit opinion to highlight a significant issue already disclosed in the financial statements. While the auditor still believes the reports are fairly presented, they use this section to draw attention to fundamental uncertainties, such as major litigation, catastrophes, or going concern doubts. It serves as a vital communication tool, ensuring stakeholders do not overlook critical information that is essential for a proper understanding of the company's financial position without modifying the overall clean audit result.

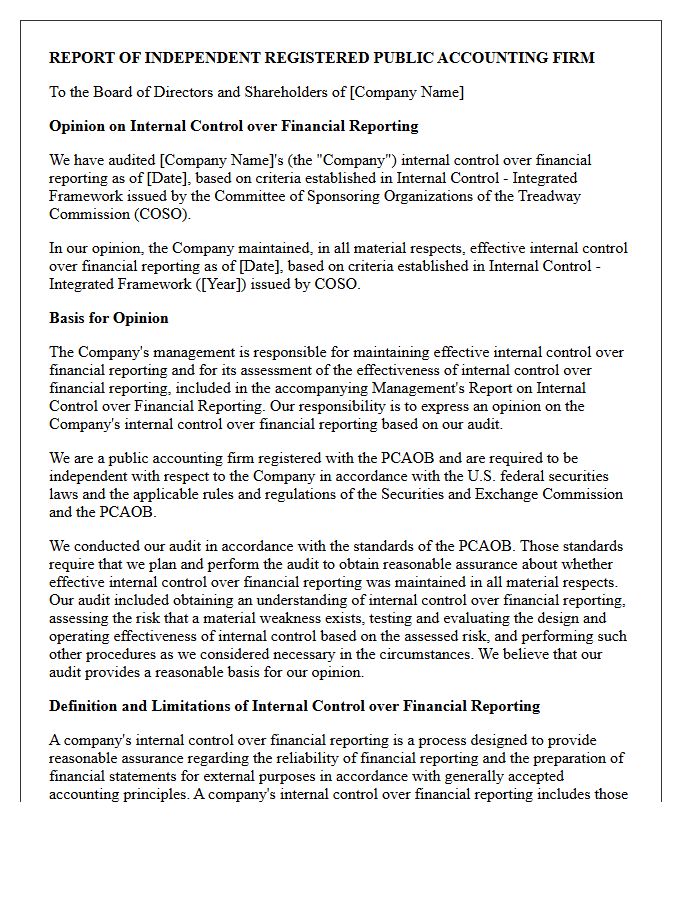

Internal Control Unqualified Audit Opinion Letter

An Internal Control Unqualified Audit Opinion Letter is a formal document issued by an independent auditor. It provides reasonable assurance that a company's internal controls over financial reporting are designed and operating effectively. This "clean" opinion indicates no material weaknesses were identified during the assessment. For investors and stakeholders, this letter is a critical indicator of financial integrity, transparency, and the reliability of a corporation's financial statements under regulatory frameworks like Sarbanes-Oxley.

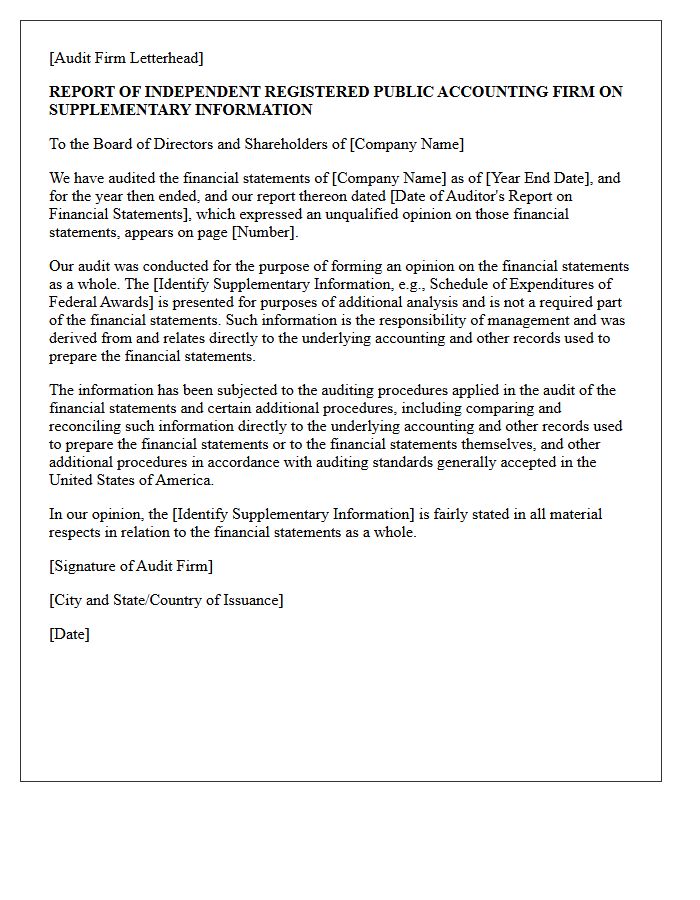

Supplementary Information Unqualified Audit Opinion Letter

A supplementary information unqualified audit opinion letter confirms that additional financial data is fairly stated in all material respects. This document verifies that secondary disclosures, which accompany the main financial statements, align with the audited records and professional standards. It provides stakeholders with assurance that the supplemental schedules, such as consolidating balances or analysis of expenses, are reliable and consistent with the overall audit findings. This letter is essential for maintaining transparency and enhancing the credibility of comprehensive financial reporting packages.

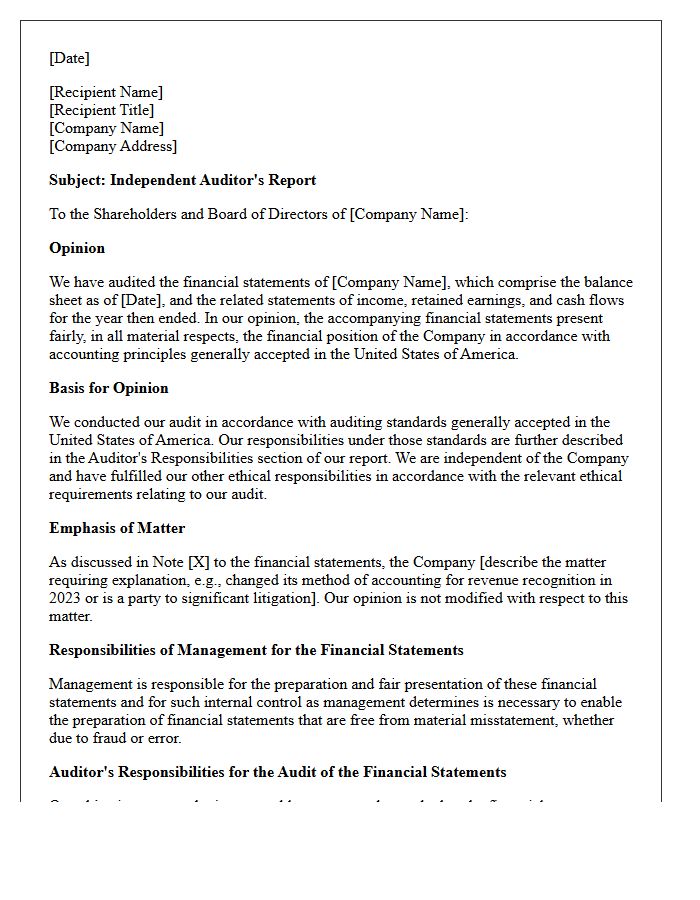

Explanatory Paragraph Unqualified Audit Opinion Letter

An unqualified audit opinion is the highest level of assurance, confirming that financial statements present a fair and accurate view of a company's position. An explanatory paragraph is added when the auditor needs to highlight significant matters without modifying the overall clean opinion. This typically addresses issues like going concern uncertainties, a change in accounting principles, or major litigation. It ensures transparency for stakeholders by providing critical context while maintaining the validity of the financial reports according to GAAP standards.

Joint Unqualified Audit Opinion Letter

A Joint Unqualified Audit Opinion Letter is a formal document issued when two or more independent CPA firms collaborate to examine a company's financial records. It signifies a "clean" report, confirming the statements are fairly presented in all material respects according to GAAP or IFRS. This joint certification enhances financial transparency and stakeholder confidence, often used in large-scale international markets or complex regulatory environments. It serves as the highest level of assurance, proving that no material misstatements were found during the rigorous, multi-firm examination process.

What is an unqualified audit opinion letter?

An unqualified audit opinion letter is an independent auditor's report stating that an organization's financial statements are presented fairly, in all material respects, and comply with Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS).

Why is an unqualified audit opinion considered a "clean" report?

It is considered a "clean" report because the auditor has found no significant discrepancies, material misstatements, or violations of accounting standards, signaling to investors and lenders that the financial data is reliable and transparent.

What are the primary components of an unqualified audit report?

The primary components include the title, the addressee, the auditor's opinion, the basis for the opinion, management's responsibility for the financial statements, the auditor's responsibilities, and the auditor's signature and date.

What is the difference between a qualified and an unqualified audit opinion?

An unqualified opinion confirms that financial statements are fully compliant with accounting standards, whereas a qualified opinion indicates that the financial statements are fairly presented "except for" a specific area or limited issue that does not invalidate the entire report.

How does an unqualified audit opinion benefit a business?

An unqualified audit opinion enhances a company's credibility, simplifies the process of securing business loans, attracts potential investors, and ensures compliance with regulatory requirements for publicly traded companies.

Comments