A First Notice of Overdue Payment serves as a professional reminder to clients regarding unpaid invoices. It is essential for maintaining healthy cash flow and clear communication without damaging business relationships. Addressing late payments promptly ensures financial stability and encourages timely settlements. To help you streamline your collection process, below are some ready to use template.

Image cover: Friendly Payment Reminder: Professional Notice Templates and Examples

Letter Samples List

- First Notice of Overdue Payment Letter for Credit Card Accounts

- Friendly Reminder Letter for Missed Mortgage Payment

- Initial Overdue Payment Letter for Personal Loans

- Auto Loan First Notice of Past Due Payment Letter

- Commercial Loan Missed Payment Notification Letter

- First Overdue Payment Warning Letter for a Line of Credit

- Retail Banking Letter for Initial Overdue Installment

- Student Loan First Notice of Overdue Payment Letter

- Small Business Loan Initial Missed Payment Letter

- Overdrawn Account Balance First Notice Letter

- Equipment Financing First Overdue Payment Letter

- Home Equity Loan Initial Past Due Warning Letter

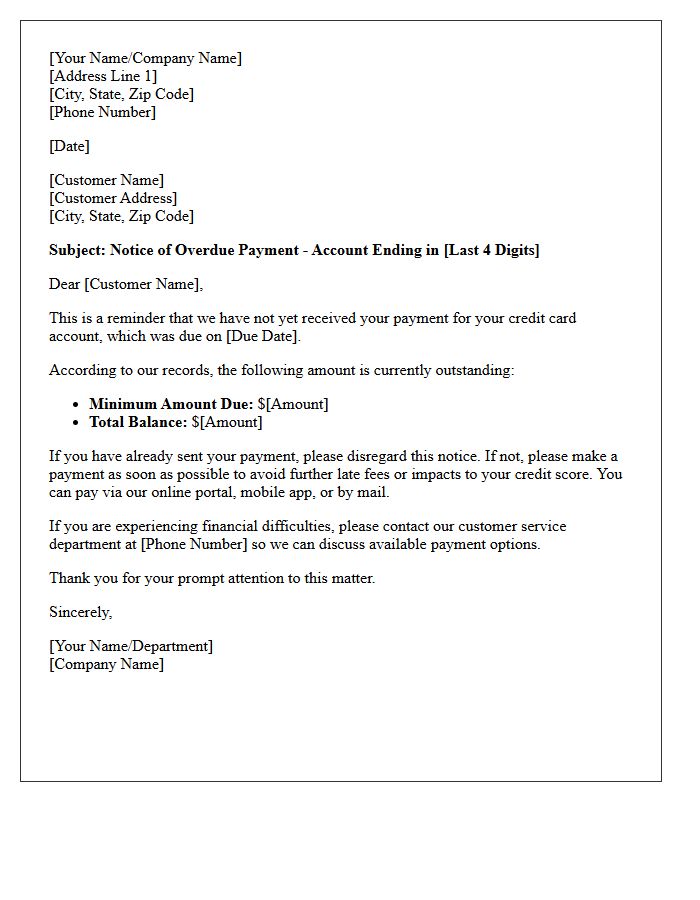

First Notice of Overdue Payment Letter for Credit Card Accounts

A First Notice of Overdue Payment is a formal reminder sent when a credit card bill misses its due date. This initial letter serves as a courtesy alert to help cardholders avoid escalating penalties. It typically outlines the total amount owed, any applicable late fees, and the potential impact on your credit score if left unpaid. Addressing this notice immediately is crucial to maintain a positive payment history and prevent the account from moving into formal debt collection or facing interest rate hikes.

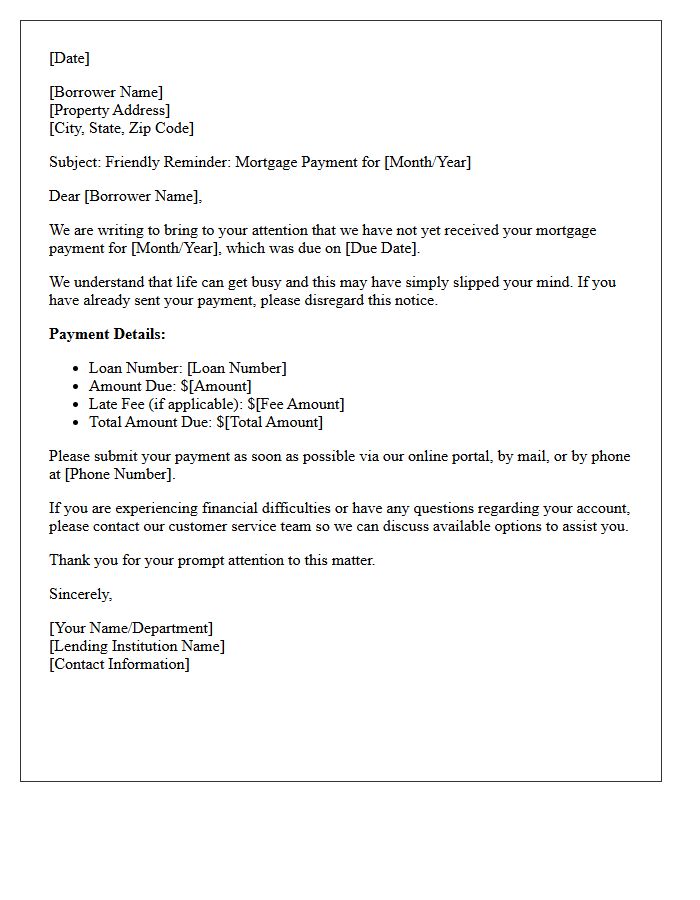

Friendly Reminder Letter for Missed Mortgage Payment

A friendly reminder letter for a missed mortgage payment is a proactive communication sent by lenders to address an overdue balance before late fees accrue. The most important goal is to reestablish a regular payment schedule to protect your credit score. These notices often serve as a helpful nudge for accidental oversights, providing clear instructions on how to remit funds immediately. Open communication with your loan servicer at this stage is essential to explore repayment options and prevent the situation from escalating into formal default or foreclosure proceedings.

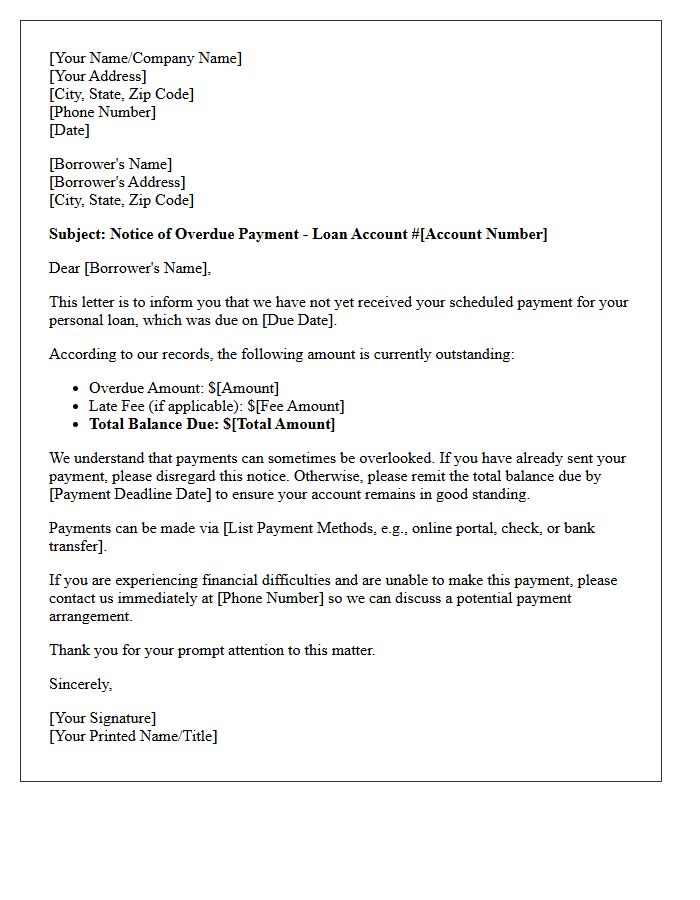

Initial Overdue Payment Letter for Personal Loans

An initial overdue payment letter serves as a formal notice sent by lenders when a personal loan installment is missed. Its primary purpose is to remind the borrower of their missed obligation and request immediate rectification to avoid penalties. Key details usually include the exact amount owed, the due date, and potential late fees. Promptly addressing this notice is essential to protect your credit score and maintain a positive relationship with your financial institution. Open communication with the lender at this stage can often prevent further debt escalation or legal action.

Auto Loan First Notice of Past Due Payment Letter

An Auto Loan First Notice of Past Due Payment serves as a formal reminder that your installment is late. This letter outlines the outstanding balance, including any applicable late fees, and provides a deadline to avoid further penalties. Timely communication is essential to protect your credit score and prevent repossession risks. If you face financial hardship, contacting your lender immediately upon receiving this notice can help you negotiate a repayment plan or deferment to keep your account in good standing.

Commercial Loan Missed Payment Notification Letter

A Commercial Loan Missed Payment Notification Letter is a formal document sent by lenders to business borrowers who default on scheduled installments. It serves as legal notice that an account is delinquent, outlining the outstanding balance, late fees, and required rectification deadlines. Timely response is critical to avoid default acceleration, where the entire loan balance becomes due immediately. Borrowers should review their contract to understand grace periods and potential impacts on corporate credit scores or collateral seizure risks. Professional communication following this notice can often facilitate loan restructuring or forbearance agreements.

First Overdue Payment Warning Letter for a Line of Credit

A first overdue payment warning letter for a line of credit is a formal notice sent when a borrower misses a scheduled repayment. Its primary purpose is to request immediate payment to avoid late fees or penalty interest rates. This letter serves as a crucial compliance step, documenting the breach of contract. To protect your credit score, you should address the arrears quickly. Contacting the lender promptly to discuss a repayment plan can prevent the account from escalating to collections or impacting your future borrowing capacity.

Retail Banking Letter for Initial Overdue Installment

A retail banking letter for an initial overdue installment serves as a formal payment reminder to resolve a missed debt obligation. Its primary purpose is to notify the borrower of a delinquency before late fees or credit score penalties apply. The document clearly outlines the outstanding balance, the original due date, and available repayment methods to restore the account to good standing. Prompt communication is essential to maintain a positive credit history and prevent the escalation of the collection process into more serious legal or financial recovery actions.

Student Loan First Notice of Overdue Payment Letter

Receiving a Student Loan First Notice of Overdue Payment is a critical warning that your account has entered delinquency. This formal letter indicates you missed a scheduled payment deadline, which could lead to late fees and negative credit reporting if ignored. It is essential to contact your loan servicer immediately to discuss repayment options, such as deferment or forbearance, to protect your financial standing. Addressing this notice promptly prevents the debt from entering default, ensuring you maintain eligibility for future federal aid and protecting your long-term credit score.

Small Business Loan Initial Missed Payment Letter

A Small Business Loan Initial Missed Payment Letter is a formal notification sent by lenders when a borrower fails to make a scheduled payment. This document serves as a critical compliance step, detailing the overdue amount, applicable late fees, and the original due date. It is essential to respond promptly to avoid negative credit reporting or default status. Open communication with the lender at this stage can often lead to restructuring options or temporary relief, preventing further legal action and protecting your company's financial reputation.

Overdrawn Account Balance First Notice Letter

An Overdrawn Account Balance First Notice Letter is a formal notification from a financial institution alerting you that your account has a negative balance. It is crucial to repay the deficit immediately to avoid mounting overdraft fees or potential account closure. This letter serves as a legal record of the bank's attempt to collect outstanding funds. Pay close attention to the deadline provided to restore a positive balance and protect your credit score from negative reporting. Reviewing your recent transactions can help identify errors or unauthorized charges during this grace period.

Equipment Financing First Overdue Payment Letter

An Equipment Financing First Overdue Payment Letter serves as a formal notification when a borrower misses their initial repayment deadline. This document is critical because it protects the lender's interest in the collateral while providing the client a professional reminder to rectify the delinquency. Timely communication helps avoid default, additional late fees, or potential repossession of the machinery. To maintain a positive business relationship, the letter should clearly state the outstanding balance, due date, and available payment methods to ensure immediate account reconciliation and continued asset operation.

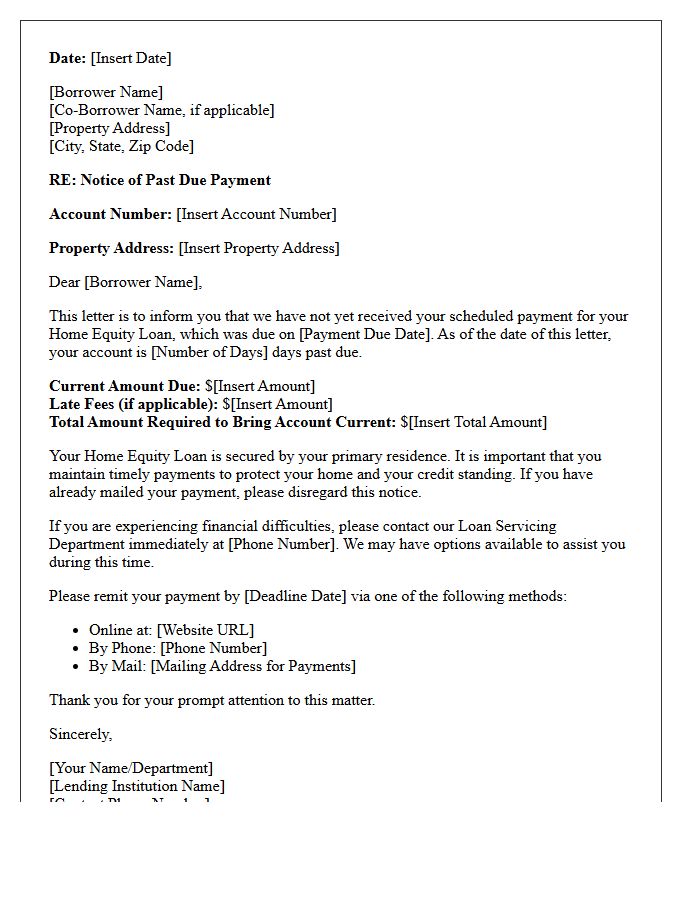

Home Equity Loan Initial Past Due Warning Letter

A Home Equity Loan Initial Past Due Warning Letter is a formal notification issued by lenders when a borrower misses a payment. This document serves as a critical preliminary notice to prevent further financial consequences. It outlines the specific amount overdue, applicable late fees, and a deadline for restitution. Ignoring this warning can negatively impact your credit score and may eventually lead to foreclosure proceedings. It is essential to contact your loan servicer immediately to discuss repayment options or hardship programs to protect your home's equity and maintain financial stability.

What is a First Notice of Overdue Payment?

A First Notice of Overdue Payment is a formal reminder sent to a client or customer when an invoice has passed its specific due date without being settled. It serves as a professional nudge to encourage immediate payment and to ensure there are no issues with the billing process.

When is a First Notice of Overdue Payment typically sent?

Most businesses issue a first notice 1 to 7 days after the payment deadline has passed. This initial reminder is generally polite and assumes the late payment may be due to an oversight or a delayed bank processing time.

What information should be included in an overdue payment notice?

The notice should clearly state the invoice number, the original due date, the total outstanding balance, and the available payment methods. It is also helpful to attach a copy of the original invoice to simplify the payment process for the recipient.

Are late fees applied during the first overdue payment notice?

Whether late fees are applied depends on your original terms and conditions. While many companies waive fees for a first notice to maintain goodwill, others may automatically calculate interest or penalties as specified in the signed contract.

What should I do if I receive a First Notice of Overdue Payment?

Upon receiving a notice, you should verify your records to confirm if the payment was made. If it was missed, settle the balance immediately; if the payment was already sent, contact the creditor to provide the transaction details and ensure your account is updated.

Comments