Financial institutions are legally required to transfer unclaimed property to the state through a process called dormant account escheatment. Before this occurs, banks must send a formal notice to account holders to prevent the loss of funds. Understanding these legal requirements ensures compliance and protects customer assets. To help you draft these critical communications, below are some ready to use template.

Image cover: Final Notice: Protecting Your Dormant Account from Escheatment and State Transfer

Letter Samples List

- Initial Notification Letter for Dormant Account Status

- Warning Letter of Pending Account Escheatment

- Customer Response Letter for Account Reactivation

- Final Notice Letter Before Escheatment Processing

- Escheatment Due Diligence Letter to Account Holder

- Returned Mail Letter for Unclaimed Property Tracking

- State Remittance Letter for Escheated Funds

- Post-Escheatment Information Letter to Customer

- Beneficiary Claim Letter for Dormant Banking Assets

- Legal Compliance Letter for Escheatment Operations

- Internal Audit Letter for Unclaimed Bank Accounts

- Escheatment Exemption Request Letter for Active Customers

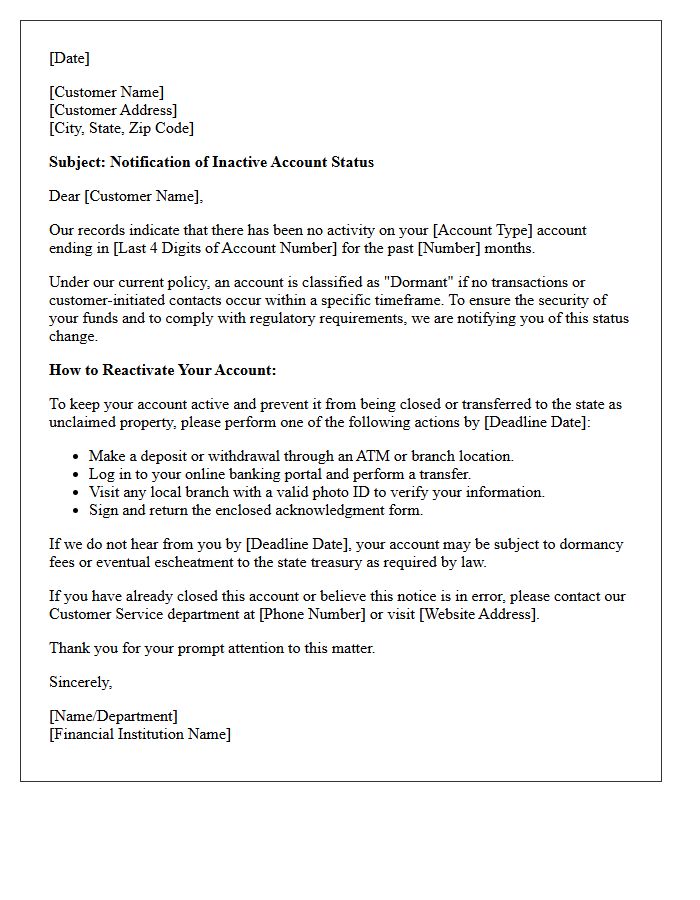

Initial Notification Letter for Dormant Account Status

An Initial Notification Letter is a formal notice sent by financial institutions to inform you that your account is nearing dormant status due to prolonged inactivity. This document serves as a final warning to prevent your assets from being classified as abandoned property. To stop the escheatment process and ensure your funds are not transferred to the state treasury, you must perform a qualifying transaction or contact your bank immediately to verify your current contact information and confirm your ownership of the account.

Warning Letter of Pending Account Escheatment

A Warning Letter of Pending Account Escheatment is a legal notice sent when your financial assets are considered unclaimed property due to prolonged inactivity. It warns that your funds will be transferred to the state government unless you take immediate action to reactivate the account. To prevent this, you must contact your bank or financial institution to verify your identity and confirm ownership. Ignoring this notice results in the permanent loss of direct access, requiring a formal claims process with the state treasury to recover your missing money.

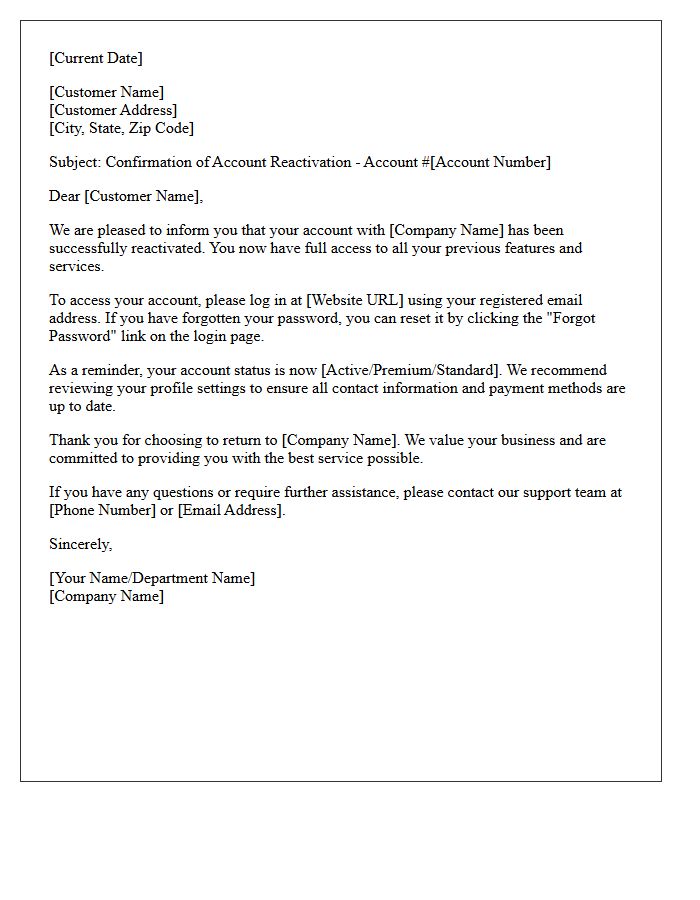

Customer Response Letter for Account Reactivation

A customer response letter for account reactivation is a formal document designed to restore access to a suspended or inactive service. It must clearly state the account identification details and the specific reason for the request. To ensure a professional outcome, verify that any previous compliance issues or outstanding balances are resolved before submission. Providing accurate documentation helps expedite the reinstatement process, ensuring a seamless return to service. Always maintain a polite tone to foster a positive long-term relationship with the provider's support team.

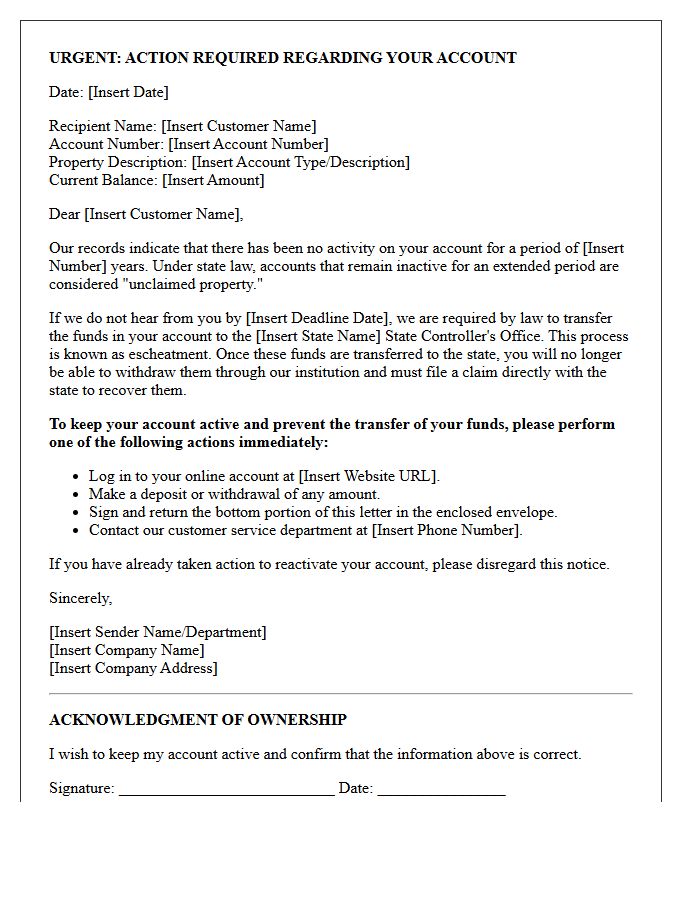

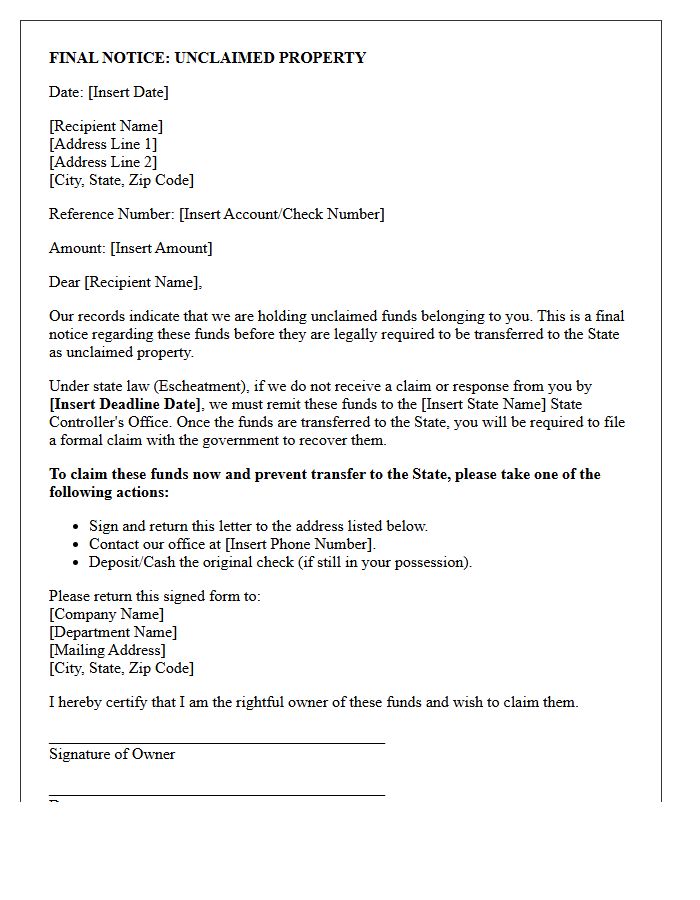

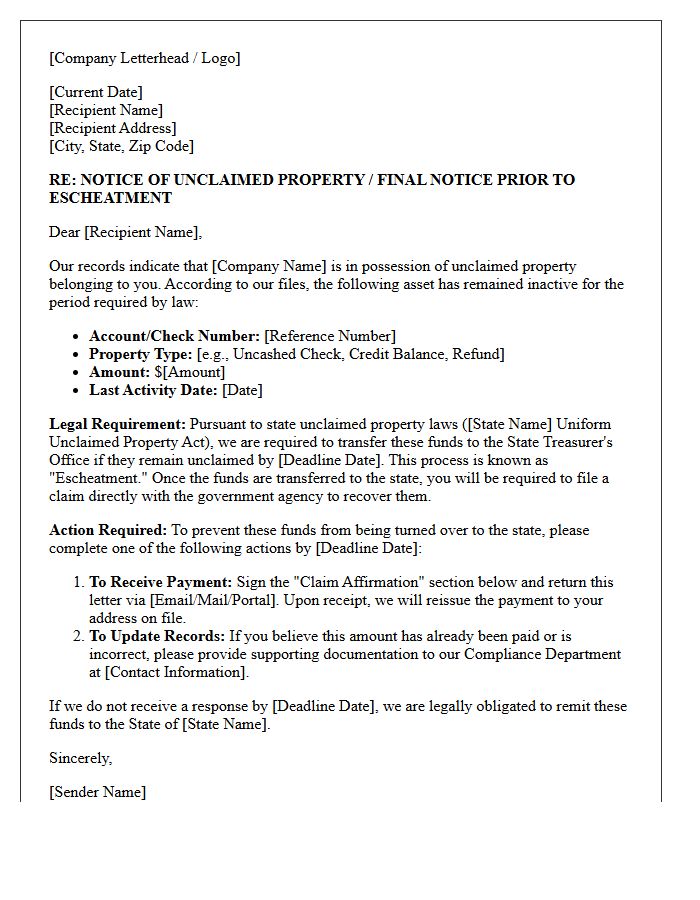

Final Notice Letter Before Escheatment Processing

A final notice letter is a critical warning that your unclaimed property is at risk of being transferred to the state. This legal document alerts owners that inactive financial accounts, such as bank balances or uncashed checks, are nearing the statutory deadline for dormancy. To prevent this escheatment process, you must respond immediately by contacting the holder to verify your identity and account activity. Failing to act before the specified date will result in the assets being surrendered to government custody, requiring a formal state claim to recover them.

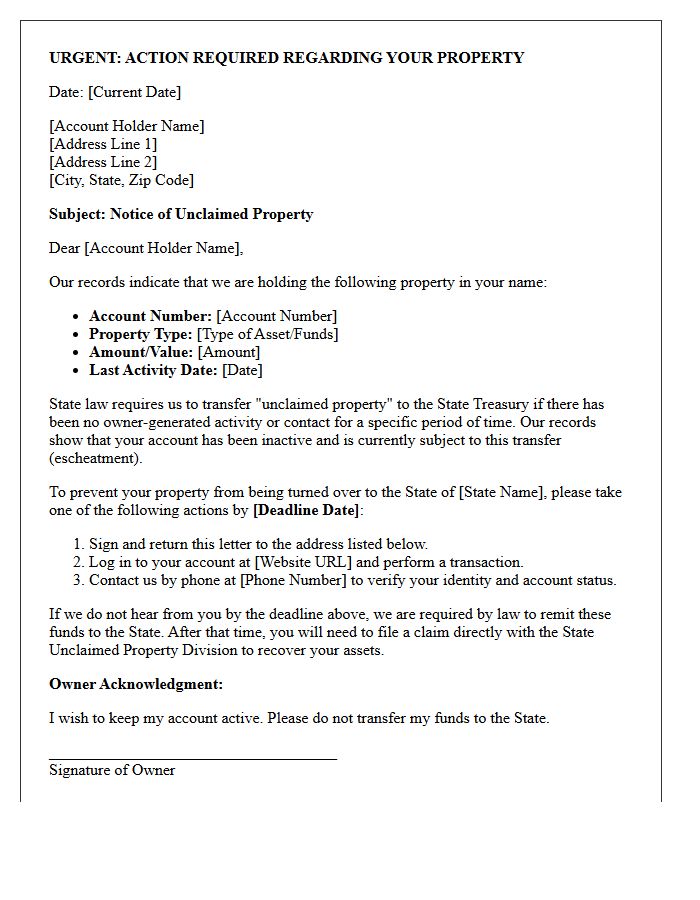

Escheatment Due Diligence Letter to Account Holder

An escheatment due diligence letter is a final legal notice sent to account holders before their unclaimed property is transferred to the state. This statutory requirement aims to protect consumers by offering a last chance to reactivate dormant accounts. Recipients must respond by the specified deadline to prevent assets from being deemed abandoned. To maintain ownership, you must typically sign the document or perform an account action. Ignoring this letter results in the state taking custody of your funds, requiring a formal claims process to recover your money.

Returned Mail Letter for Unclaimed Property Tracking

Receiving a Returned Mail Letter indicates that a state's unclaimed property division attempted to contact an owner but the mail was undeliverable. This triggers a legal requirement for businesses to perform due diligence and eventually escheat the funds to the government. To prevent loss, owners must ensure their current mailing address is updated with financial institutions. If you receive a notice regarding escheatment, act immediately to claim your assets before they are transferred to the state treasury for safekeeping. Monitoring your mail helps maintain ownership rights over dormant accounts and forgotten refunds.

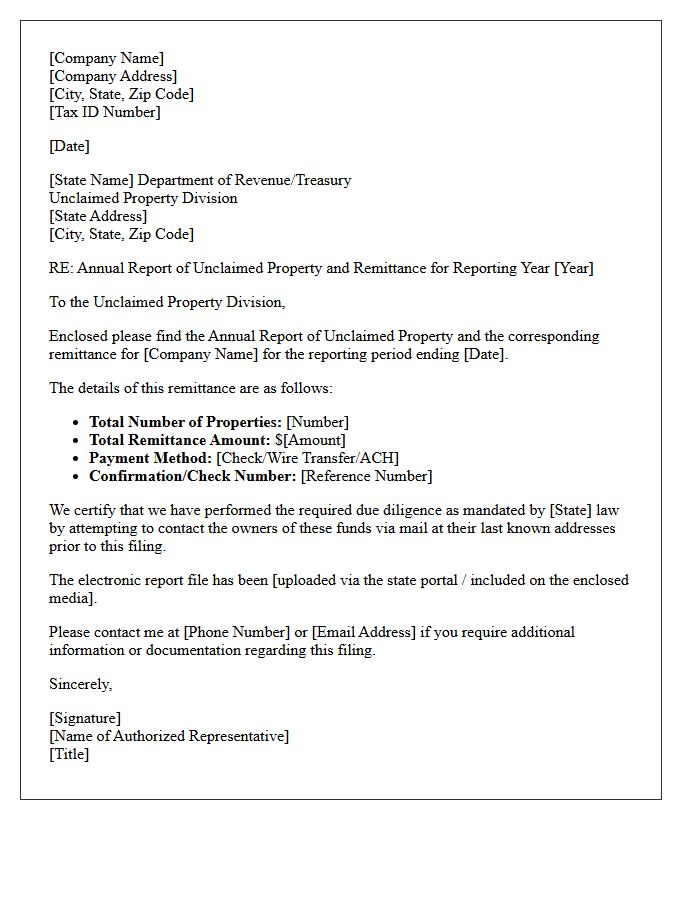

State Remittance Letter for Escheated Funds

A State Remittance Letter is a formal document notifying unclaimed property administrators that assets are being transferred to the government. When accounts remain inactive beyond the statutory dormancy period, holders must perform escheatment to comply with legal requirements. This letter details the owner's identity, the specific value of funds, and confirms that due diligence efforts were made to contact the rightful owner. Accurate reporting is essential to avoid state audits, penalties, and interest charges, ensuring that escheated funds are securely held by the state until claimed.

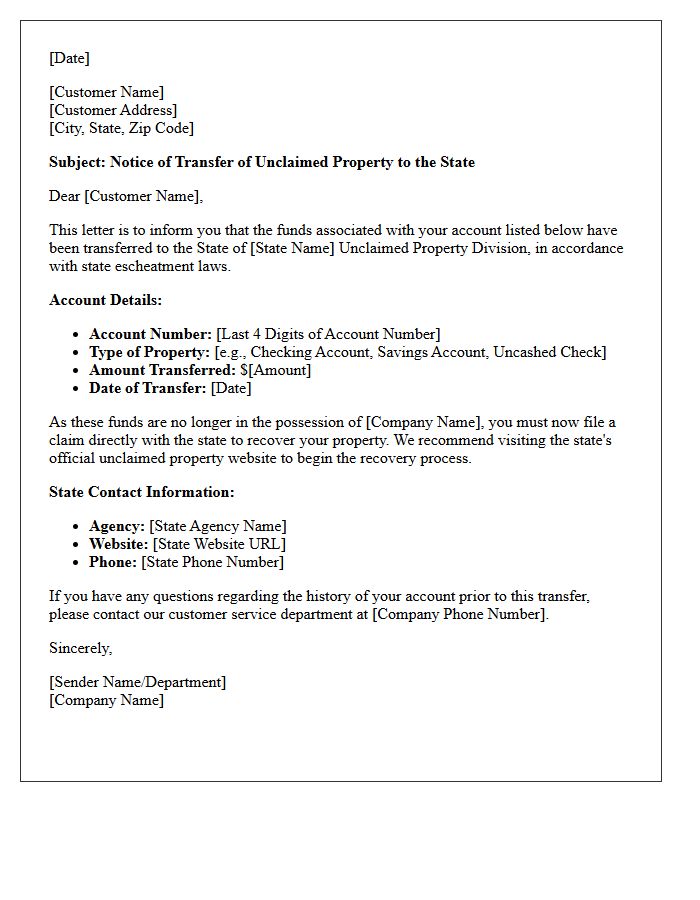

Post-Escheatment Information Letter to Customer

A post-escheatment information letter notifies owners that their unclaimed property has been transferred to state custody. This critical document explains that your funds are no longer held by the financial institution and provides instructions on how to initiate a claim with the government. It typically includes the property type, amount, and reference numbers needed for recovery. Acting promptly is essential to verify your identity and successfully reclaim your assets from the state's unclaimed property division, ensuring you maintain ownership of your forgotten or abandoned financial holdings.

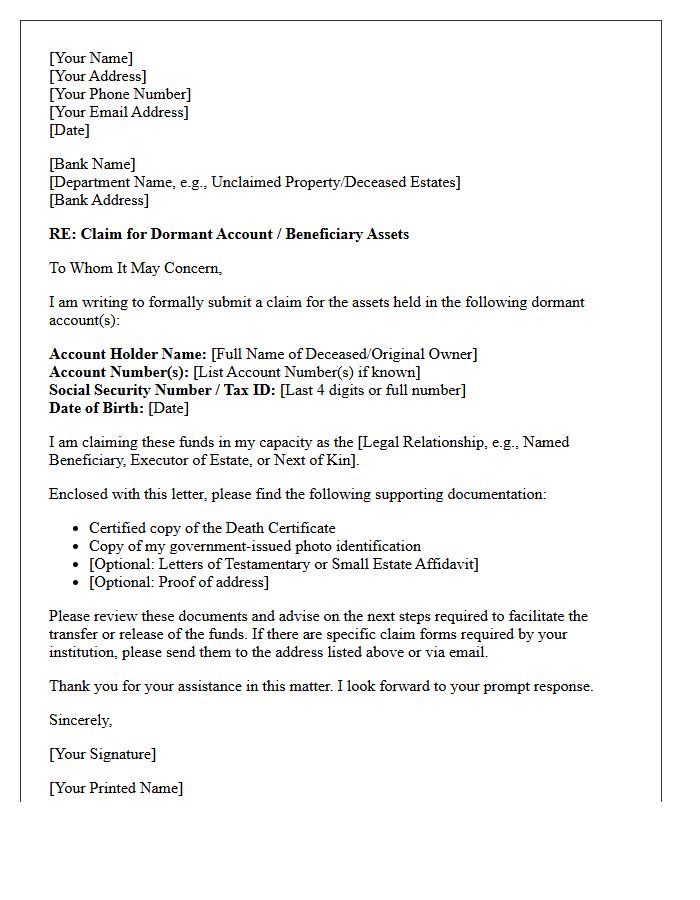

Beneficiary Claim Letter for Dormant Banking Assets

A Beneficiary Claim Letter is a formal request sent to a financial institution to recover funds from dormant banking assets. These accounts become inactive after long periods of no transaction activity. To successfully reclaim the balance, you must provide clear proof of identity and legal entitlement, such as a death certificate or probate documents if the original owner is deceased. Submitting an accurate claim letter ensures the bank initiates the verification process to release unclaimed property to its rightful legal heirs or designated beneficiaries.

Legal Compliance Letter for Escheatment Operations

A legal compliance letter for escheatment operations is a critical notice sent to owners of unclaimed property before it is transferred to the state. This process, known as due diligence, is legally mandated to protect consumer rights and ensure businesses adhere to escheatment laws. The letter must clearly outline the property value, the deadline for response, and the consequences of inaction. Maintaining accurate records and timely communication is essential for regulatory compliance, helping organizations avoid significant penalties, audits, and legal liabilities while reuniting rightful owners with their forgotten assets.

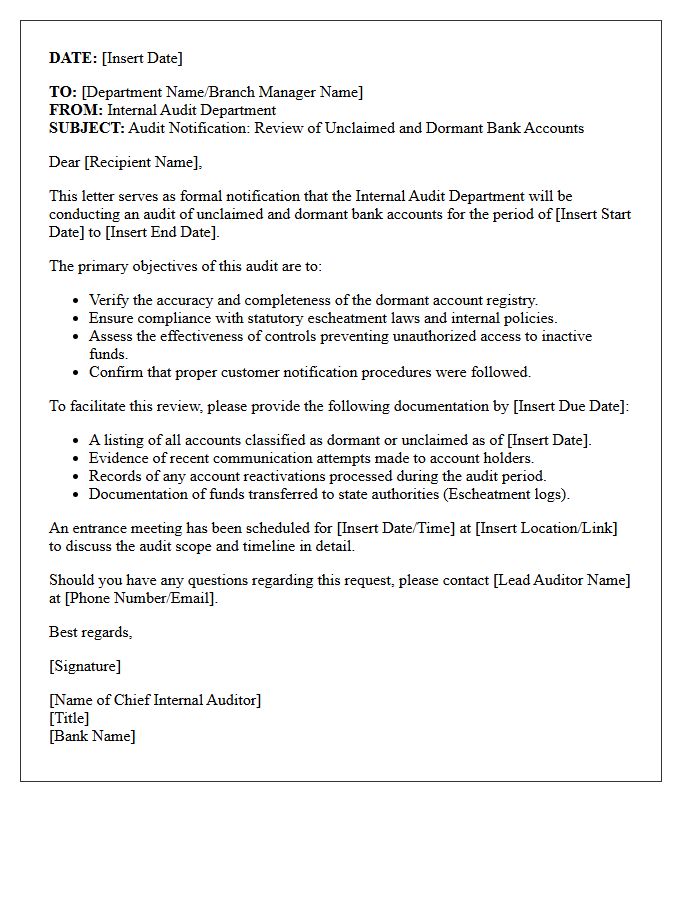

Internal Audit Letter for Unclaimed Bank Accounts

An Internal Audit Letter for unclaimed bank accounts is a critical notification sent to customers before funds are declared escheatment property. This document serves as a final attempt to re-establish contact with the account holder to prevent the balance from being transferred to the state government. Receiving this letter indicates your account is classified as dormant due to inactivity. To maintain control of your assets, you must respond immediately by signing the form or performing a transaction, thereby ensuring your financial holdings remain active and accessible within the banking institution.

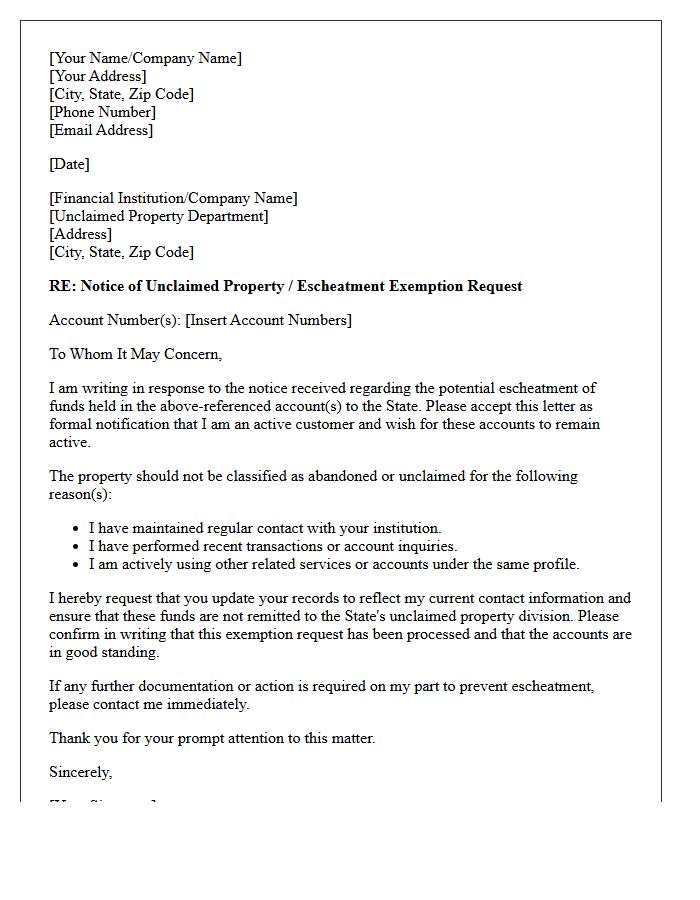

Escheatment Exemption Request Letter for Active Customers

An Escheatment Exemption Request Letter is a formal notice sent to state authorities or financial institutions to prevent the seizure of active customer accounts. Its primary purpose is to prove ongoing engagement, such as recent logins or transactions, to stop assets from being classified as unclaimed property. By submitting this document, businesses verify that a client relationship remains current, effectively halting the legal transfer of funds to the state. Timely filing is essential to maintain account security and avoid the complex administrative burden of recovering escheated assets later.

What is a dormant account escheatment notification?

A dormant account escheatment notification is a formal legal notice sent to account holders informing them that their property is classified as inactive and is at risk of being transferred to the state treasury as unclaimed property if no action is taken.

Why did I receive a notice about my account being turned over to the state?

You received this notice because there has been no documented activity or contact regarding your account for a specific period, known as the dormancy period. State laws require financial institutions to report and remit abandoned property to the government after this timeframe expires.

How can I stop my funds from being sent to the state's unclaimed property division?

To prevent escheatment, you must establish contact with the financial institution immediately. This is typically done by logging into your online portal, making a deposit or withdrawal, calling customer service to verify your identity, or signing and returning the response form included with your notification.

What is the deadline for responding to a dormant account notice?

The deadline is specified in the letter you received, usually ranging from 30 to 60 days from the date of the notice. If the institution does not receive a response by this date, they are legally obligated to close the account and transfer the balance to the state of your last known residence.

How can I recover my money if it has already been escheated?

Once funds are escheated, the financial institution can no longer return them to you. You must file a formal claim with the State Controller's Office or the Unclaimed Property Division in the state where the account was held. You will be required to provide proof of ownership and valid identification to recover the assets.

Comments