Protecting your financial reputation is essential when creditors report errors. If a lender provides false data, you must file a dispute of inaccurate credit information to ensure your profile reflects the truth. Correcting these reporting mistakes can significantly improve your score and borrowing potential. To help you start the formal notification process, below are some ready to use template.

Image cover: Effective Dispute Letters for Removing Credit Report Inaccuracies: Templates and Guide

Letter Samples List

- Letter Of Dispute Regarding Inaccurate Account Balance Reporting

- Letter To Dispute Erroneous Late Payment History Furnished To Bureaus

- Letter Of Dispute Concerning Closed Bank Account Reported As Open

- Letter To Dispute Unauthorized Hard Credit Inquiry By Banking Institution

- Letter Of Dispute Regarding Fraudulent Account Opened Due To Identity Theft

- Letter To Dispute Incorrect Charge-Off Status Furnished To Credit Bureaus

- Letter Of Dispute Concerning Duplicate Bank Account Reporting

- Letter To Dispute Settled Credit Account Displaying As Unpaid

- Letter Of Dispute Regarding Erroneous Bankruptcy Association On Account

- Letter To Dispute Incorrect Personal Demographic Information Attached To Loan

- Letter Of Dispute Concerning Unauthorized Joint Account Status Reporting

- Letter To Dispute Delinquency Furnished Due To Misapplied Bank Payment

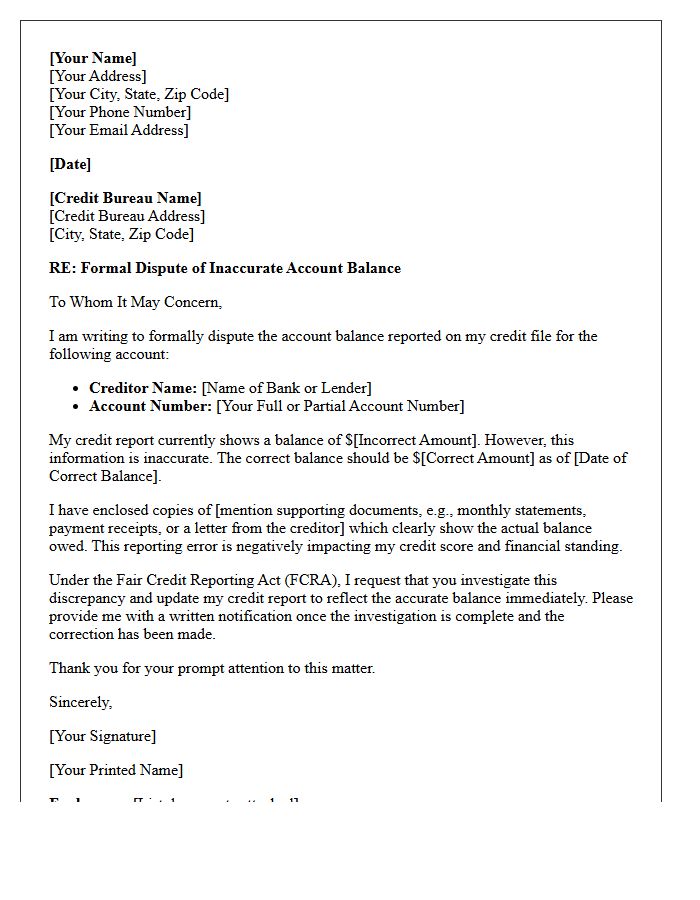

Letter Of Dispute Regarding Inaccurate Account Balance Reporting

A Letter of Dispute is a formal legal tool used to correct financial errors under the Fair Credit Reporting Act. When a creditor or credit bureau displays an inaccurate account balance, you must provide written evidence, such as payment receipts or bank statements, to challenge the discrepancy. Clearly state why the reported figure is wrong and request an immediate investigation. Sending this document via certified mail ensures a paper trail, protecting your credit score and consumer rights while forcing institutions to verify or remove the misinformation from your record.

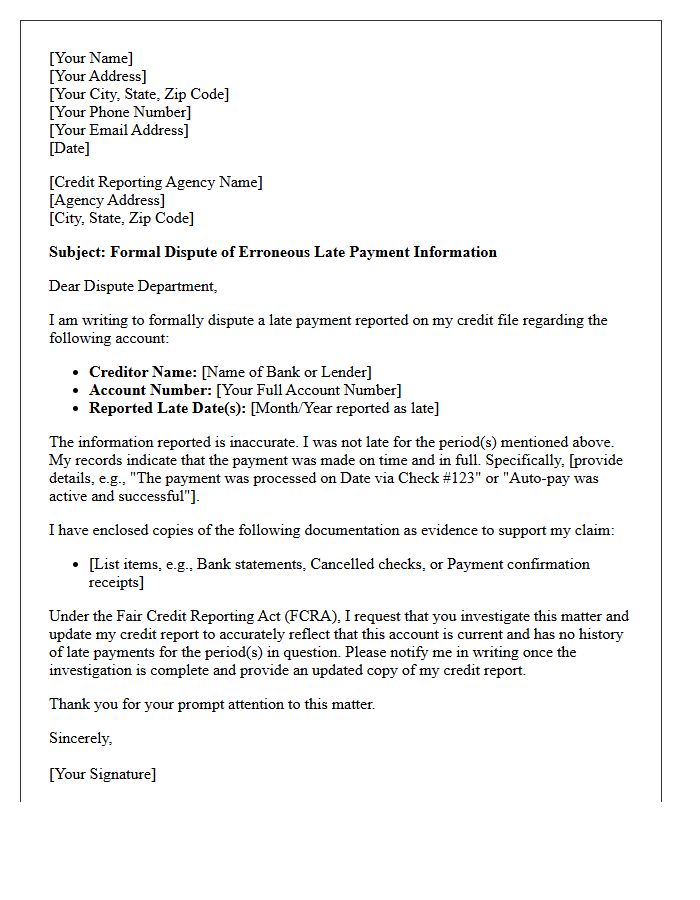

Letter To Dispute Erroneous Late Payment History Furnished To Bureaus

To correct your credit profile, send a formal dispute letter to the credit bureaus and the reporting creditor. This document must clearly identify the inaccurate late payment and provide evidence, such as bank statements or payment receipts, to prove timeliness. Under the Fair Credit Reporting Act (FCRA), bureaus are legally obligated to investigate and remove unverified information within 30 days. Accurate reporting is essential because payment history is the most significant factor in calculating your credit score. Always send your request via certified mail to maintain a paper trail.

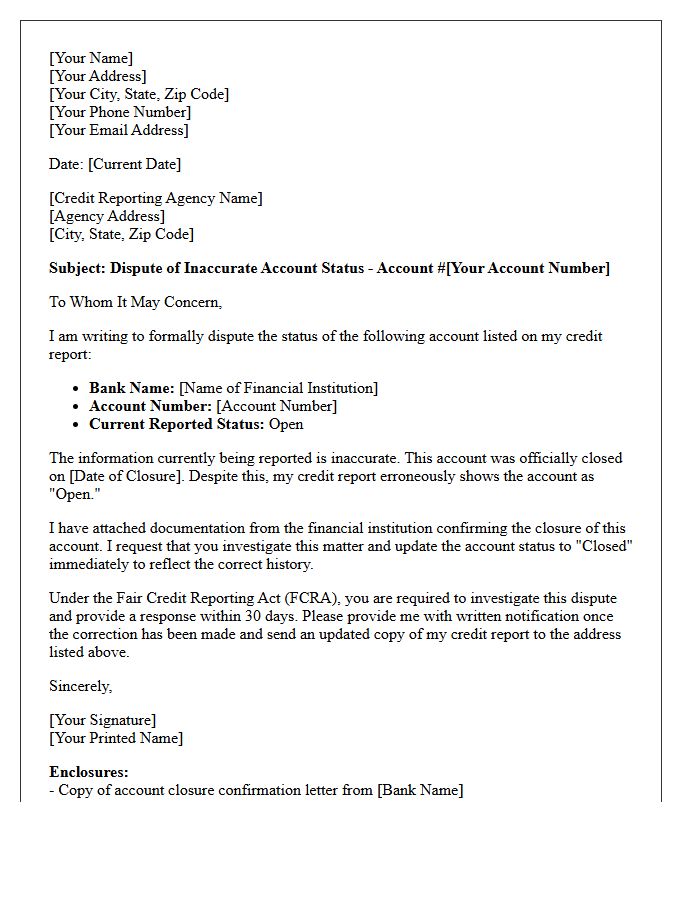

Letter Of Dispute Concerning Closed Bank Account Reported As Open

If a credit report inaccurately lists a closed bank account as open, you must submit a formal letter of dispute to the credit bureaus. Clearly state that the account status is incorrect and provide official documentation from the financial institution confirming the closure date. This error can negatively impact your debt-to-income ratio or suggest potential identity theft. Under the Fair Credit Reporting Act, agencies are legally required to investigate and correct these discrepancies within thirty days to ensure your financial profile remains accurate and secure.

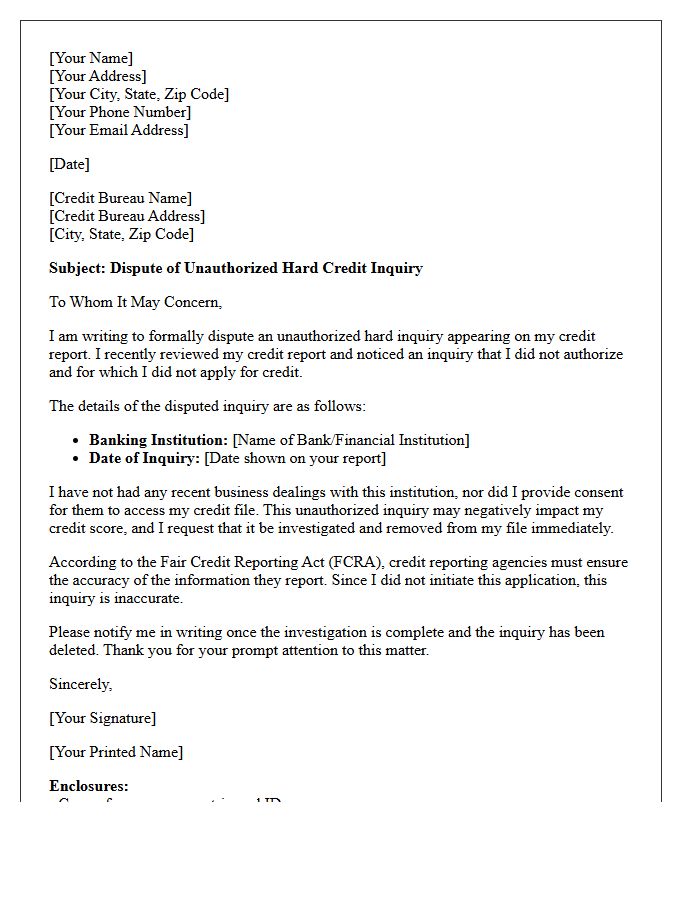

Letter To Dispute Unauthorized Hard Credit Inquiry By Banking Institution

A formal dispute letter is essential for removing an unauthorized hard credit inquiry from your report. Hard pulls occur when a banking institution reviews your credit for lending, potentially lowering your score. If you did not apply for credit, you must notify both the bank and credit bureaus in writing. State clearly that you did not authorize the check and demand its immediate deletion under the Fair Credit Reporting Act. Protecting your credit integrity ensures better interest rates and financial health by eliminating inaccurate, fraudulent activity from your history.

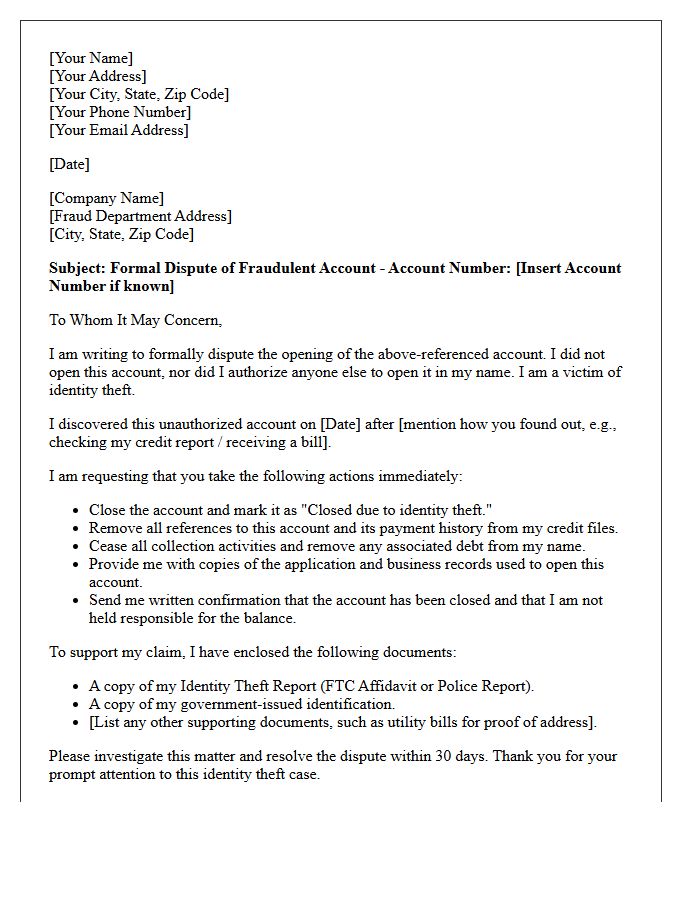

Letter Of Dispute Regarding Fraudulent Account Opened Due To Identity Theft

If you discover an unauthorized line of credit, immediately send a Letter of Dispute to the relevant credit bureau and financial institution. This formal document must state that the account was opened due to identity theft. Include a copy of your FTC Identity Theft Report or a police report to validate your claim. Explicitly request the removal of fraudulent data and a complete block of the information from your credit profile. This essential step protects your legal rights under the Fair Credit Reporting Act and helps restore your financial standing.

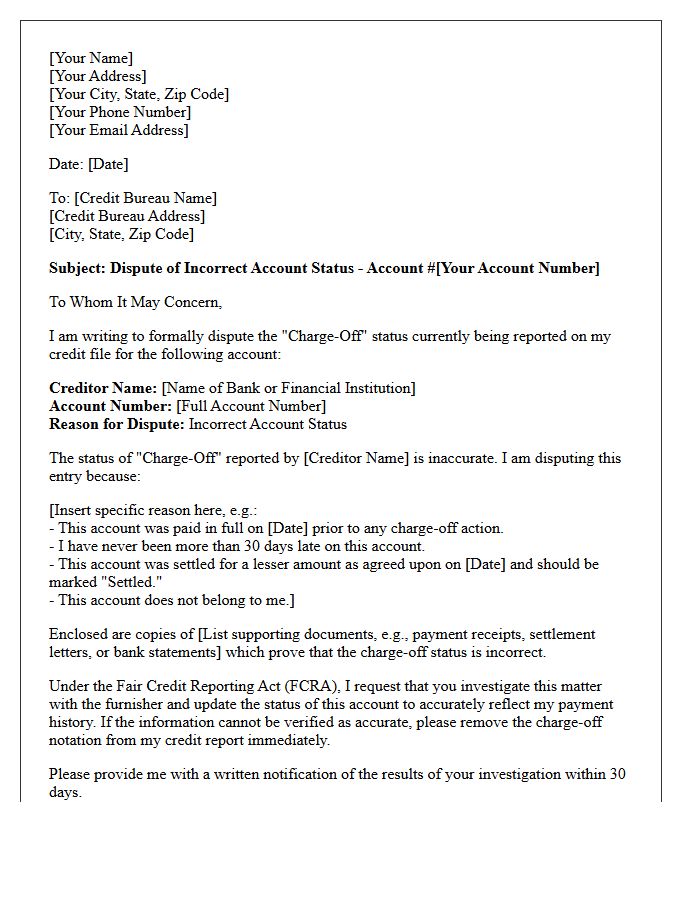

Letter To Dispute Incorrect Charge-Off Status Furnished To Credit Bureaus

A formal dispute letter is essential to correct an inaccurate charge-off status on your credit report. You must clearly identify the erroneous account and provide specific evidence, such as payment receipts or settlement agreements, proving the status is incorrect. Under the Fair Credit Reporting Act, bureaus must investigate and remove inaccurate data within 30 days. Highlighting these discrepancies protects your credit score from undue harm. Always send your correspondence via certified mail to maintain a paper trail and ensure the financial institution updates their records with all major credit agencies.

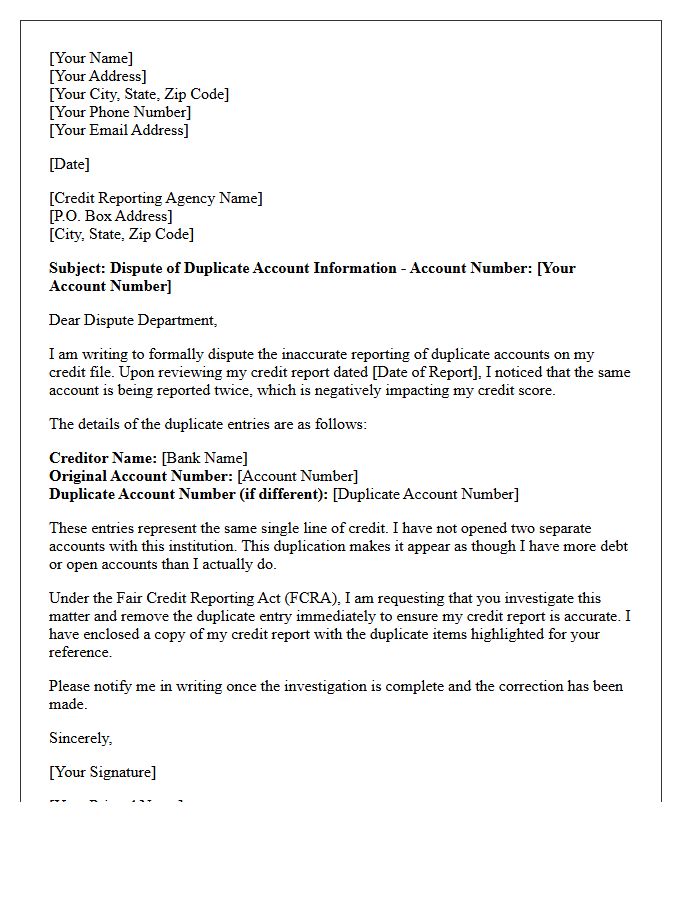

Letter Of Dispute Concerning Duplicate Bank Account Reporting

A letter of dispute concerning duplicate bank account reporting is a formal request sent to credit bureaus to rectify redundant entries on your credit report. These errors can artificially inflate your debt-to-income ratio and negatively impact your credit score. In your letter, clearly identify the repeating accounts and provide supporting bank documentation. Ensuring the removal of duplicate data is essential for maintaining accurate financial records and securing better interest rates. Timely action protects your consumer rights and ensures your credit profile reflects your true financial standing without unfair penalties.

Letter To Dispute Settled Credit Account Displaying As Unpaid

When drafting a dispute letter for a settled credit account appearing as unpaid, accuracy is vital. Clearly state that the debt was resolved and include your settlement agreement or payment confirmation as evidence. Request that the credit bureau updates the status to reflect the account settled in full. Under the Fair Credit Reporting Act, agencies must investigate and correct these inaccuracies within 30 days. Ensuring your credit report is truthful protects your financial reputation and prevents artificial drops in your credit score caused by reporting errors.

Letter Of Dispute Regarding Erroneous Bankruptcy Association On Account

A Letter of Dispute is a formal legal tool used to correct credit reports when an account is falsely linked to a bankruptcy filing. It is essential to include specific account numbers and official court documentation proving the error. Under the Fair Credit Reporting Act, agencies must investigate and remove these erroneous associations within 30 days. Resolving this inaccuracy is vital, as a misreported bankruptcy significantly lowers your credit score and restricts your ability to secure future loans or competitive interest rates.

Letter To Dispute Incorrect Personal Demographic Information Attached To Loan

A formal dispute letter is essential to correct inaccurate demographic data on your loan records. Errors in your name, address, or social security number can lead to identity confusion or lower credit scores. Explicitly state the incorrect information and provide supporting documentation, such as a driver's license or utility bill, to prove the correct details. Under the Fair Credit Reporting Act, lenders must investigate and rectify these discrepancies promptly. Ensuring your personal profile is accurate maintains your financial credibility and protects you against potential identity theft or administrative processing errors.

Letter Of Dispute Concerning Unauthorized Joint Account Status Reporting

A letter of dispute regarding unauthorized joint account status is essential for correcting identity theft or reporting errors on your credit profile. If a creditor incorrectly labels you as a joint account holder for a debt you did not authorize, you must formally notify credit bureaus to protect your credit score. Clearly state that you never signed a contractual agreement for the account. Demand an immediate investigation and the removal of inaccurate data to ensure your financial records remain accurate and prevent unlawful collection activities against your personal assets.

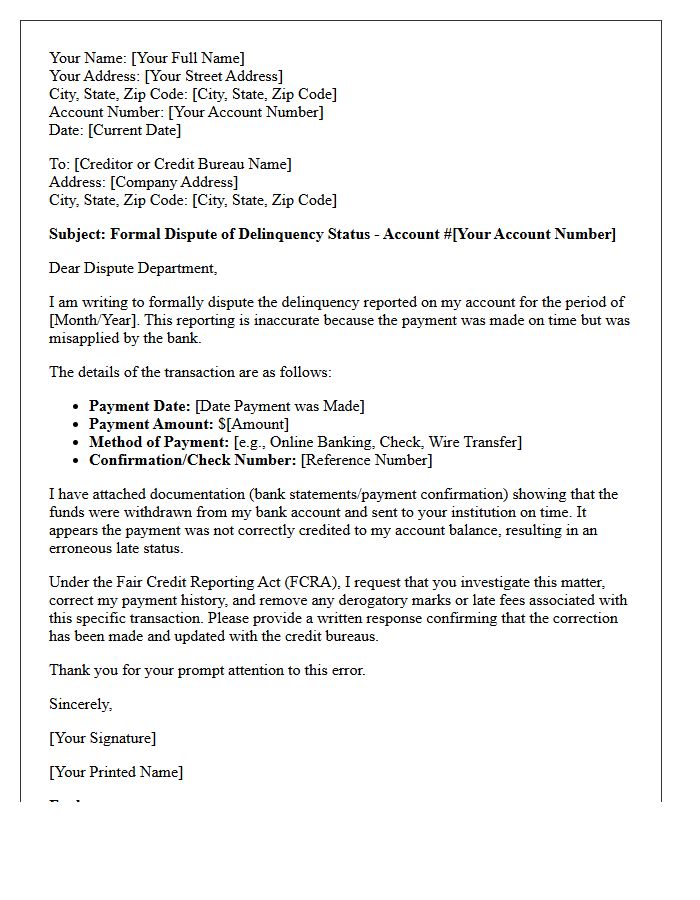

Letter To Dispute Delinquency Furnished Due To Misapplied Bank Payment

If a bank misapplied your payment, you must send a formal Letter to Dispute Delinquency to both the lender and credit bureaus. Clearly state that the late status resulted from a clerical error rather than a lack of funds. Attach copies of your bank statement and payment confirmation as proof of timely submission. Under the Fair Credit Reporting Act, furnishers are legally obligated to investigate and correct inaccuracies. Promptly disputing this ensures your credit score is protected from unjust penalties caused by administrative mistakes.

How do I dispute inaccurate information reported to credit bureaus?

To dispute inaccurate data, you should submit a formal written dispute to the credit bureau reporting the error (Equifax, Experian, or TransUnion) and the data furnisher who provided the information. Your request should include your contact details, a clear identification of the specific error, documentation supporting your claim, and a request for the information to be corrected or deleted.

What is the legal timeframe for credit bureaus to investigate a dispute?

Under the Fair Credit Reporting Act (FCRA), credit reporting agencies generally have 30 days to investigate your dispute. This period can be extended to 45 days if you provide additional information during the investigation process. Once the investigation is complete, the bureau must notify you of the results within five business days.

What should I do if a creditor continues to report incorrect information after a dispute?

If a furnisher continues to report inaccurate data after a formal dispute, you should file a secondary dispute directly with the furnisher's "Notice of Dispute" address. If the error persists despite evidence of inaccuracy, you may file a complaint with the Consumer Financial Protection Bureau (CFPB) or consult a consumer law attorney regarding a potential FCRA violation.

Can I remove accurate but negative information from my credit report?

No, credit bureaus are legally allowed to report accurate, verifiable information for a specific period-typically seven years for most negative items and ten years for bankruptcies. Legitimate disputes only result in removal if the information is proven to be inaccurate, incomplete, or cannot be verified by the furnisher.

What documentation is needed to support a credit dispute claim?

Strong supporting documentation includes copies of bank statements, canceled checks showing payments, court documents for settled debts, or correspondence from the creditor acknowledging an error. Always send copies rather than original documents and use certified mail with a return receipt to maintain a paper trail of your dispute.

Comments