Unexpected bank charges can be frustrating and costly. This guide explains how to challenge an unfair foreign transaction fee by understanding your consumer rights and the specific terms of your credit card agreement. Learn how to communicate effectively with your financial institution to secure a refund. To help you take action immediately, below are some ready to use template.

Image cover: Reclaim Your Money: Unfair Foreign Transaction Fee Dispute Guide and Templates

Letter Samples List

- Letter of Dispute Regarding Unfair Foreign Transaction Fee

- Formal Complaint Letter for Unauthorized Foreign Transaction Charges

- Request Letter for Reversal of Undisclosed Foreign Exchange Fees

- Bank Dispute Letter Concerning Erroneous International Transaction Fee

- Consumer Appeal Letter for Waiving Unfair Foreign Transaction Fees

- Notice Letter of Dispute for Hidden Foreign Transaction Assessments

- Account Holder Letter Contesting Unfair Foreign Transaction Fee

- Grievance Letter Addressing Unjustified Foreign Transaction Fees

- Resolution Request Letter for Contested Foreign Transaction Fee

- Official Letter of Protest Against Unfair Foreign Transaction Fee

- Demand Letter for Refund of Unfair Foreign Transaction Fee

- Escalation Letter for Unresolved Foreign Transaction Fee Dispute

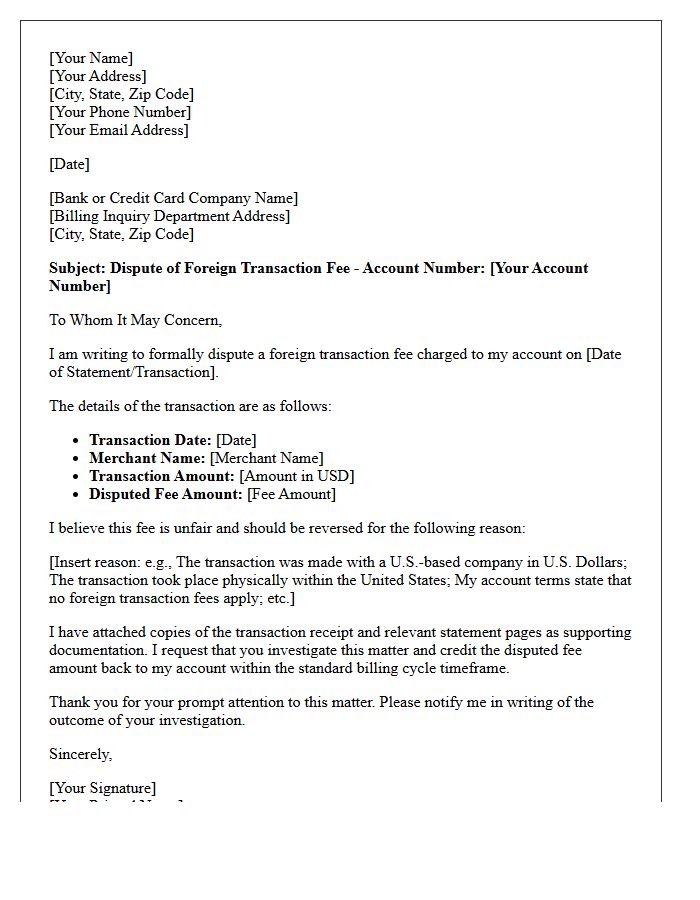

Letter of Dispute Regarding Unfair Foreign Transaction Fee

A Letter of Dispute is a formal request to challenge unfair foreign transaction fees charged by your bank. If you were billed for an international purchase despite being in your home country, or if the fee contradicts your account agreement, you must act quickly. Clearly state the transaction date, amount, and the specific reason the charge is invalid. Submitting this written notice helps protect your consumer rights and facilitates a refund of unauthorized costs, ensuring your financial institution adheres to its stated fee disclosure policies.

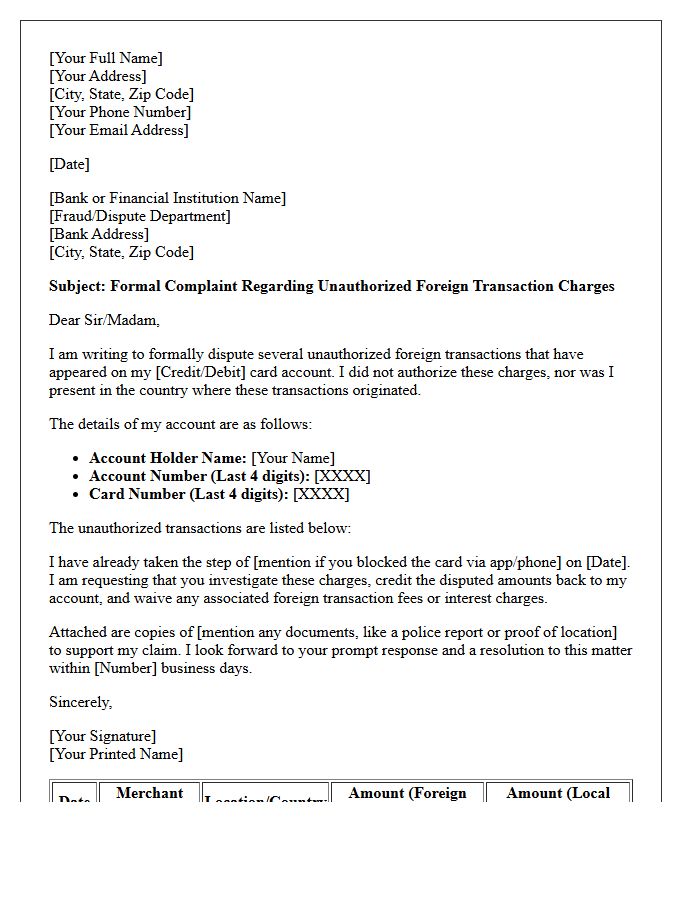

Formal Complaint Letter for Unauthorized Foreign Transaction Charges

When drafting a Formal Complaint Letter for Unauthorized Foreign Transaction Charges, clearly state your intent to dispute specific line items. Provide your account details, transaction dates, and the exact amounts involved. Explicitly mention that you did not authorize these international payments and request an immediate reversal of funds. It is essential to cite your consumer rights under the Fair Credit Billing Act or local banking regulations to ensure legal compliance. Attach supporting evidence, such as bank statements, and send the document via certified mail to maintain a verifiable paper trail for your financial protection.

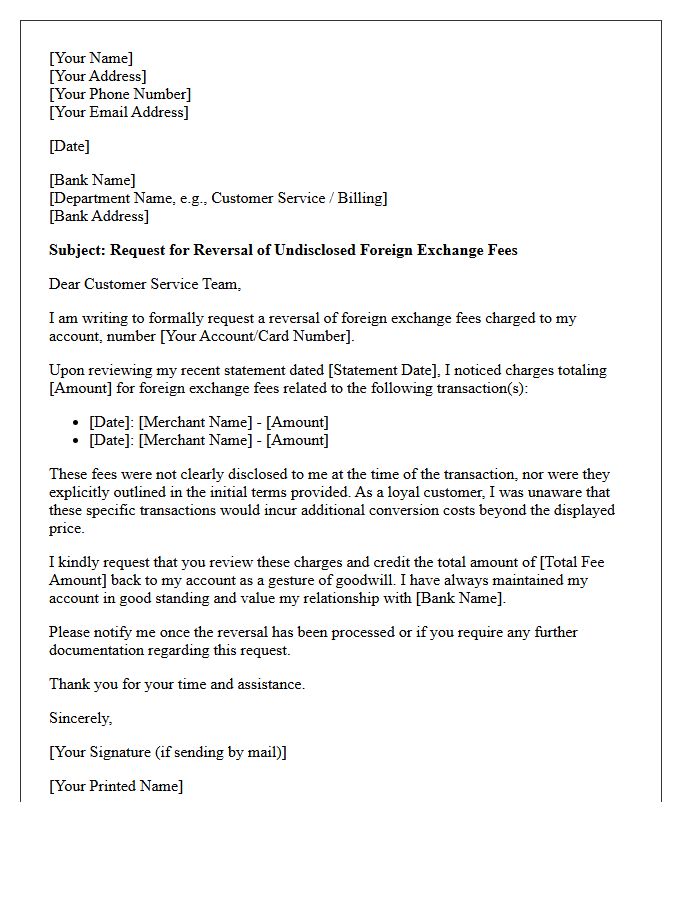

Request Letter for Reversal of Undisclosed Foreign Exchange Fees

When drafting a Request Letter for Reversal of Undisclosed Foreign Exchange Fees, you must clearly identify the unauthorized transactions. Formally demand a refund by highlighting the lack of transparency regarding markup rates or conversion costs not disclosed during the initial agreement. Attach relevant bank statements as evidence to strengthen your claim. Explicitly state that these hidden charges violate consumer disclosure standards. A professional tone ensures the financial institution treats your fee dispute as a priority for immediate rectification and credit adjustment.

Bank Dispute Letter Concerning Erroneous International Transaction Fee

When drafting a Bank Dispute Letter, clearly state that you are contesting an erroneous international transaction fee. Explicitly mention that the merchant is domestic and no currency conversion occurred. Include your account number, transaction date, and the specific amount charged. Demand a full reversal based on your bank's fee schedule. Under the Fair Credit Billing Act, you must submit this formal written notice within sixty days of the statement date to protect your consumer rights and ensure a timely investigation and refund.

Consumer Appeal Letter for Waiving Unfair Foreign Transaction Fees

When drafting a consumer appeal letter to waive unfair foreign transaction fees, focus on your loyalty as a long-standing customer. Clearly state that the charges were unexpected or poorly disclosed, and highlight your consistent payment history. Using a professional tone increases your chances of a courtesy credit. Explicitly request a manual review of the transaction and mention any competing credit cards that offer fee-free international spending. A well-structured request emphasizes your value to the bank, often resulting in a successful fee reversal or a permanent account upgrade.

Notice Letter of Dispute for Hidden Foreign Transaction Assessments

A Notice Letter of Dispute is a critical legal tool used to challenge hidden foreign transaction assessments imposed by financial institutions without clear disclosure. Consumers must submit this formal written objection to exercise their rights under banking regulations and consumer protection laws. The letter should detail specific unauthorized fees, demanding a full refund and correction of billing errors. Timely submission is essential to preserve your legal standing, ensure transparency, and prevent predatory hidden charges on international purchases from depleting your account balance unfairly.

Account Holder Letter Contesting Unfair Foreign Transaction Fee

When drafting an Account Holder Letter to contest an unfair foreign transaction fee, clearly state that the purchase was made in domestic currency or via a local merchant. Explain that the charge violates your cardholder agreement or was processed without prior disclosure. Attach relevant transaction receipts as supporting evidence to substantiate your claim. Formally request a reversal of the fee and a corrected billing statement. Sending this formal written notice protects your consumer rights under federal banking regulations and ensures a documented paper trail for the dispute resolution process.

Grievance Letter Addressing Unjustified Foreign Transaction Fees

When drafting a grievance letter for unjustified foreign transaction fees, clearly outline the specific disputed charges and provide evidence that the transactions were domestic or exempt. Explicitly state your demand for a full refund and reference your consumer rights or credit card agreement terms. Using a professional tone and a formal structure ensures your complaint is taken seriously by the financial institution. Submit the letter via a trackable method to maintain a documented record of your dispute, which is essential if you need to escalate the matter to regulatory bodies.

Resolution Request Letter for Contested Foreign Transaction Fee

A Resolution Request Letter is a formal document used to dispute unauthorized or incorrect foreign transaction fees with your financial institution. Clearly state your account details, the specific transaction date, and the exact amount in question. Attach supporting evidence, such as travel receipts or proof of original currency conversion, to justify your claim. Emphasize that the charge violates your cardholder agreement or was processed incorrectly. Sending this letter via certified mail ensures a paper trail, compelling the bank to investigate and potentially refund the contested fees under consumer protection regulations.

Official Letter of Protest Against Unfair Foreign Transaction Fee

An official letter of protest against an unfair foreign transaction fee is a formal dispute document sent to your bank. It challenges unauthorized or undisclosed charges applied to international purchases. To be effective, the letter must include your account details, the specific transaction date, and evidence of why the fee violates your cardholder agreement. Clear documentation helps you exercise your consumer rights to secure a refund or correction. Sending this protest promptly is essential for resolving billing errors and holding financial institutions accountable for hidden costs.

Demand Letter for Refund of Unfair Foreign Transaction Fee

A Demand Letter for Refund of Unfair Foreign Transaction Fee is a formal legal notice sent to a financial institution to dispute unauthorized or hidden charges. It serves as essential evidence that you attempted to resolve the billing error through direct communication before pursuing legal action. The document should clearly state the specific transaction dates, the exact amount of overcharges, and a firm deadline for reimbursement. Providing a detailed account of the discrepancy helps consumers assert their rights under consumer protection laws to recover undisclosed fees efficiently.

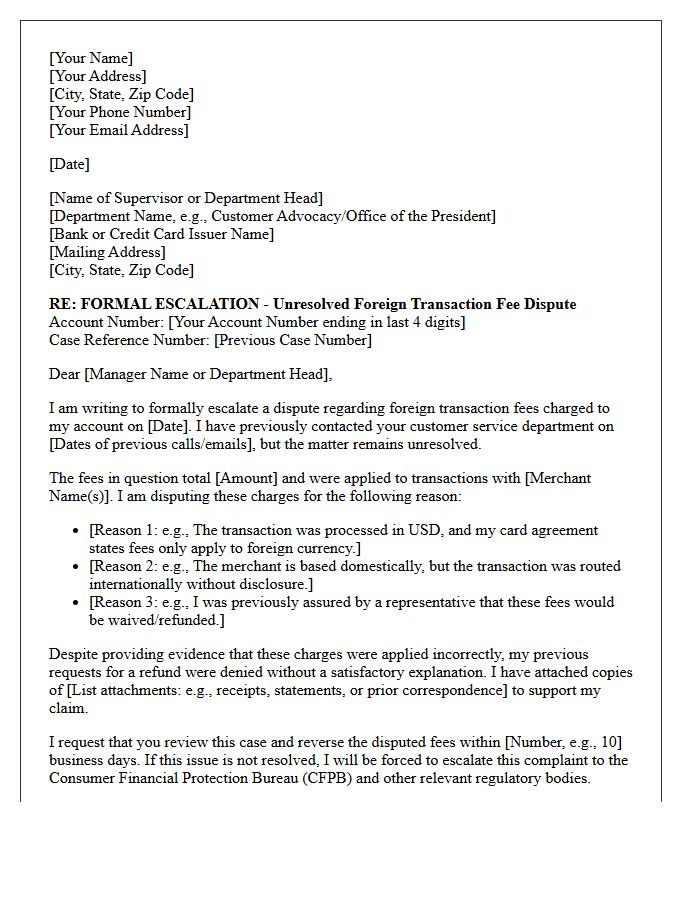

Escalation Letter for Unresolved Foreign Transaction Fee Dispute

When an initial dispute fails, an escalation letter is essential to resolve a foreign transaction fee error. Clearly cite your credit card agreement terms and provide evidence that the transaction occurred domestically or was exempt. Formally demand a managerial review of the case to address the billing discrepancy. Mentioning your intent to contact the Consumer Financial Protection Bureau often encourages banks to expedite a correction. Always include your case number, transaction dates, and specific amounts to ensure a binding resolution for your financial records.

How do I dispute an unfair foreign transaction fee on my billing statement?

To dispute an unfair foreign transaction fee, you should contact your bank or credit card issuer immediately to file a formal billing error claim. You can typically do this through your online banking portal, by calling the customer service number on the back of your card, or by sending a certified letter explaining that the transaction was domestic or that the fee was not disclosed in your cardholder agreement.

What are the valid grounds for disputing a foreign transaction fee?

Valid grounds for a dispute include being charged a fee for a transaction made within your home country, being charged for a purchase made in your local currency, or if the merchant's payment processor incorrectly flagged a domestic purchase as international. You may also dispute the fee if your bank failed to disclose these charges in your account's terms and conditions.

Can I get a refund for a foreign transaction fee if I paid in my local currency?

Yes, if you chose to pay in your local currency via Dynamic Currency Conversion (DCC) at the point of sale, you may still be charged a foreign transaction fee by your bank. However, if you believe this fee was applied in error to a strictly domestic transaction, you have the right to request a refund by providing a receipt showing the transaction originated within your home country.

How long do I have to dispute an incorrect foreign transaction charge?

Under the Fair Credit Billing Act (FCBA), consumers generally have 60 days from the date the statement containing the error was mailed to them to file a formal dispute. It is recommended to initiate the process as soon as you notice the unauthorized or unfair fee to increase the likelihood of a successful reversal.

What evidence is needed to win a dispute over an unfair international fee?

To support your claim, you should provide a copy of the transaction receipt showing the merchant's location and the currency used. Additionally, providing a copy of your cardholder agreement highlighting the fee schedule and any correspondence with the merchant confirming the domestic nature of the purchase will strengthen your case during the bank's investigation.

Comments