A Notice of Failure to Apply Loan Payment Correctly is a formal dispute letter sent to lenders when your installment is misapplied or not credited. Ensuring your payment history remains accurate is vital for maintaining your financial standing and credit score. To help you resolve these billing errors efficiently, below are some ready to use template options.

Image cover: Resolving Payment Errors: Sample Letters for Misapplied Loan Credits

Letter Samples List

- Notice of Failure to Apply Loan Payment Correctly Letter

- Request for Correction of Misapplied Loan Funds Letter

- Notification of Uncredited Mortgage Installment Letter

- Formal Dispute of Unapplied Auto Loan Payment Letter

- Commercial Loan Payment Allocation Dispute Letter

- Demand for Account Adjustment and Fee Reversal Letter

- Escalated Complaint of Unprocessed Bank Remittance Letter

- Notice of Improper Principal and Interest Application Letter

- Proof of Cleared Payment and Application Request Letter

- Final Warning Before Regulatory Banking Complaint Letter

- Request for Audit of Unapplied Loan Installment Letter

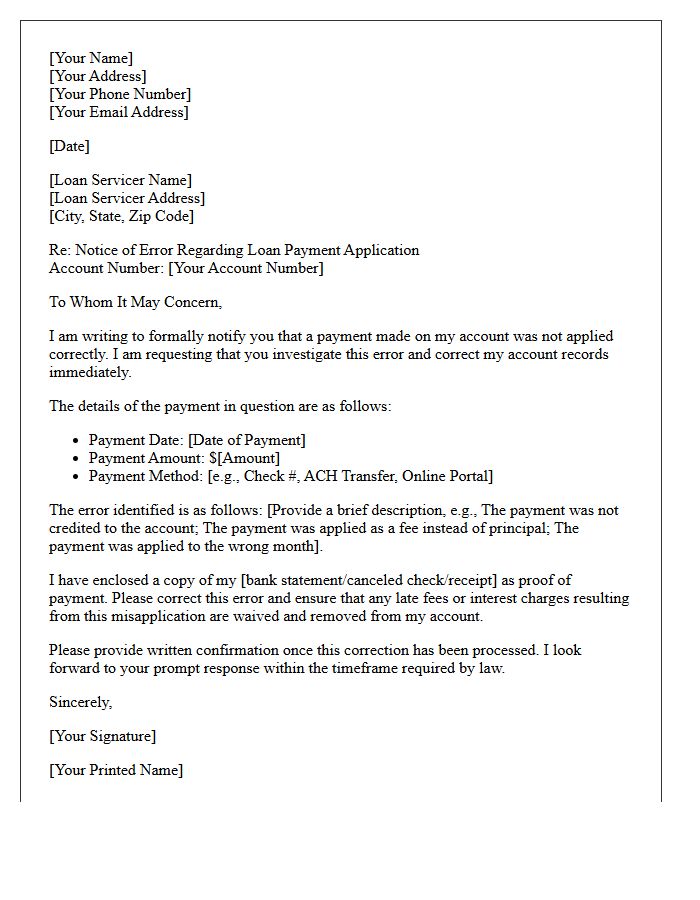

Notice of Failure to Apply Loan Payment Correctly Letter

A Notice of Failure to Apply Loan Payment Correctly Letter is a formal document sent to a lender to resolve billing errors. It serves as a legal record when your payment is misallocated, missing, or applied to the wrong account. Under the Real Estate Settlement Procedures Act (RESPA), lenders are required to investigate and correct these discrepancies within specific timeframes. Including proof of payment, such as a cleared check or receipt, ensures the servicer rectifies the principal balance and removes any unfair late fees or negative credit reporting.

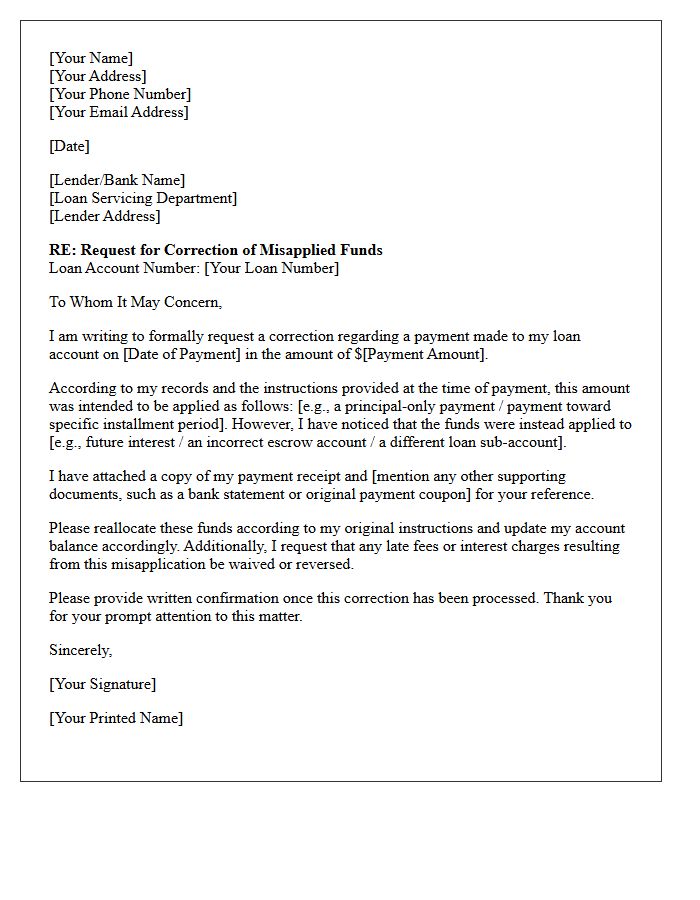

Request for Correction of Misapplied Loan Funds Letter

A Request for Correction of Misapplied Loan Funds Letter is a formal notice sent to a lender when a payment is incorrectly allocated. To ensure accuracy, clearly state your account details, the specific transaction date, and the payment amount involved. Explicitly instruct the servicer to move the funds to the correct balance, such as the principal or a specific loan sequence. Attaching proof of payment helps expedite the resolution process and ensures your credit standing remains protected while correcting administrative accounting errors.

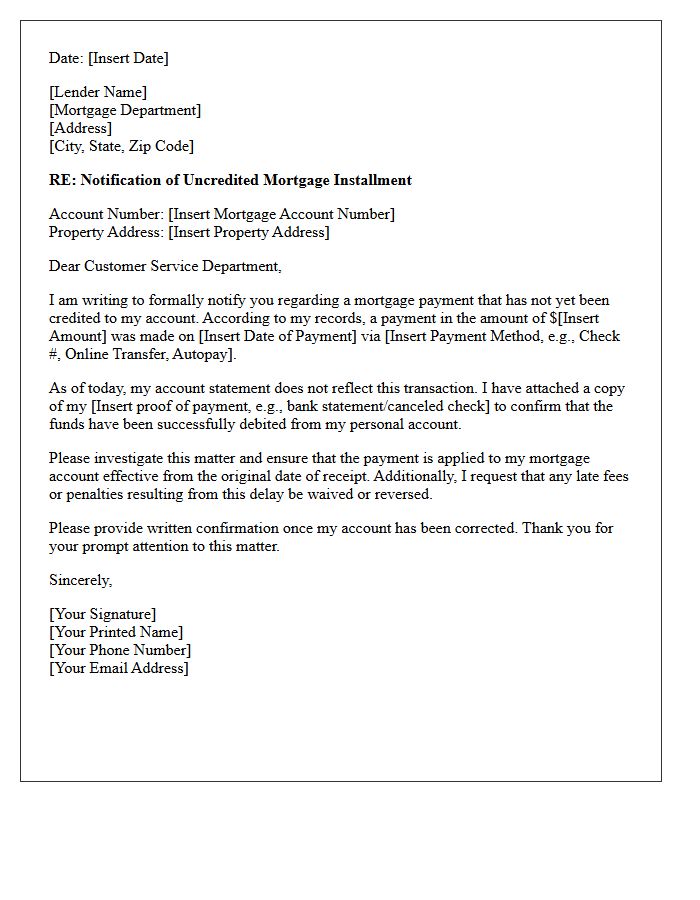

Notification of Uncredited Mortgage Installment Letter

A Notification of Uncredited Mortgage Installment Letter is a formal alert from a lender stating that a payment was not applied to your account. This issue often occurs due to technical errors, incorrect account details, or processing delays. It is crucial to respond immediately by providing proof of payment, such as a bank statement, to avoid late fees or credit score damage. Resolving this payment discrepancy quickly ensures your mortgage remains in good standing and prevents the commencement of unnecessary foreclosure proceedings or penalty charges.

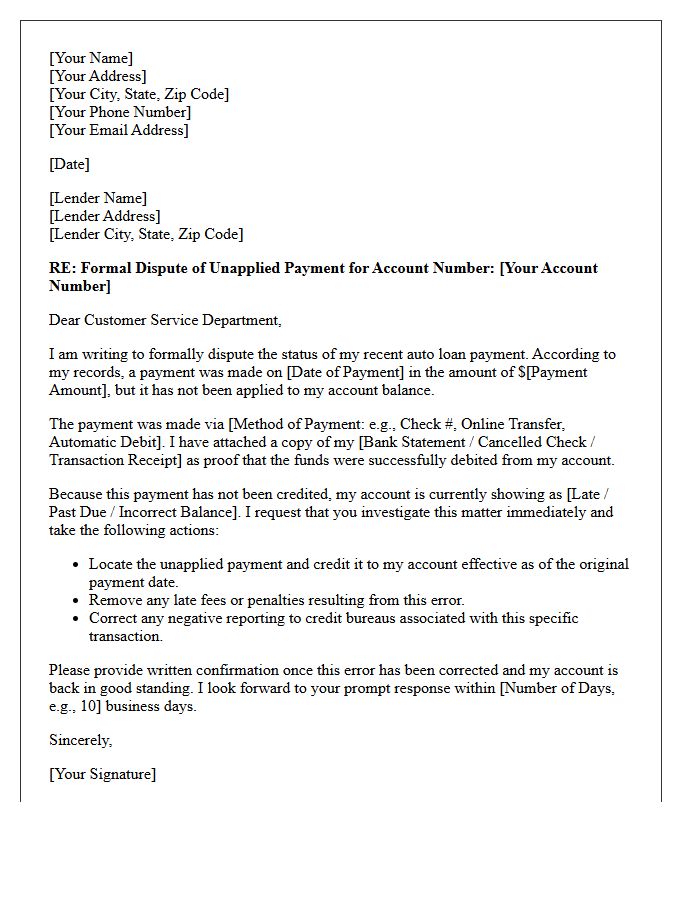

Formal Dispute of Unapplied Auto Loan Payment Letter

A formal dispute letter for an unapplied auto loan payment is a critical legal tool used to correct accounting errors. When a lender fails to credit your account despite proof of payment, you must submit a written notice including your account number, payment date, and transaction receipts. This document triggers a formal investigation under consumer protection laws, ensuring the lender rectifies the balance and prevents negative credit reporting. Sending this via certified mail creates a paper trail, protecting your financial standing and ensuring your legal rights are upheld during the dispute process.

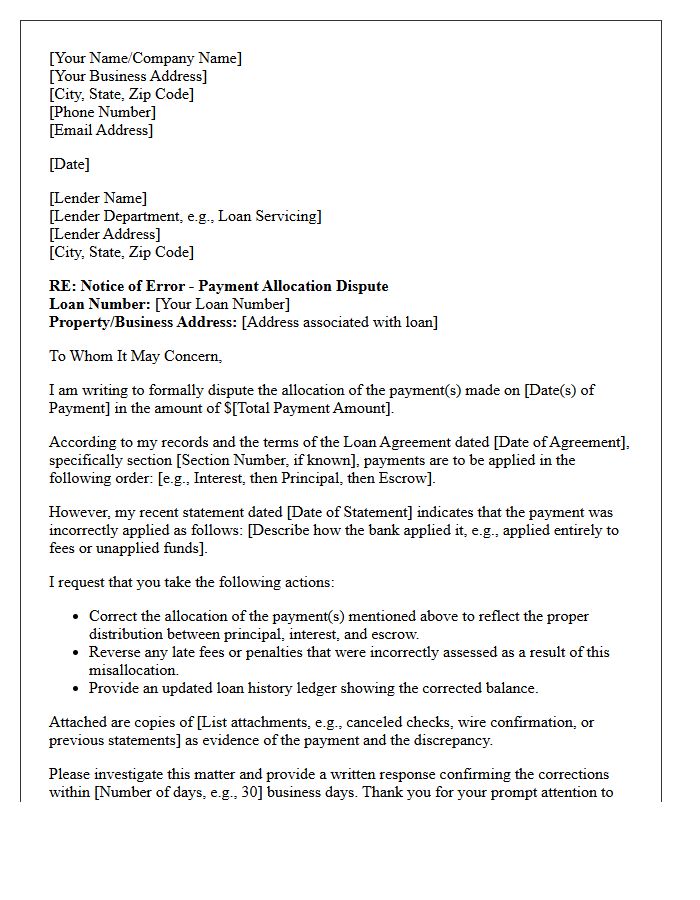

Commercial Loan Payment Allocation Dispute Letter

A Commercial Loan Payment Allocation Dispute Letter is a formal notice sent to lenders when funds are applied incorrectly across principal, interest, or escrow accounts. It is crucial to clearly identify the specific transaction date and reference the exact loan agreement terms being violated. Providing evidence, such as payment receipts or updated ledgers, helps resolve discrepancies quickly. Properly documenting this misallocation protects your business credit score and prevents unjustified late fees or default notices resulting from accounting errors during the amortization process.

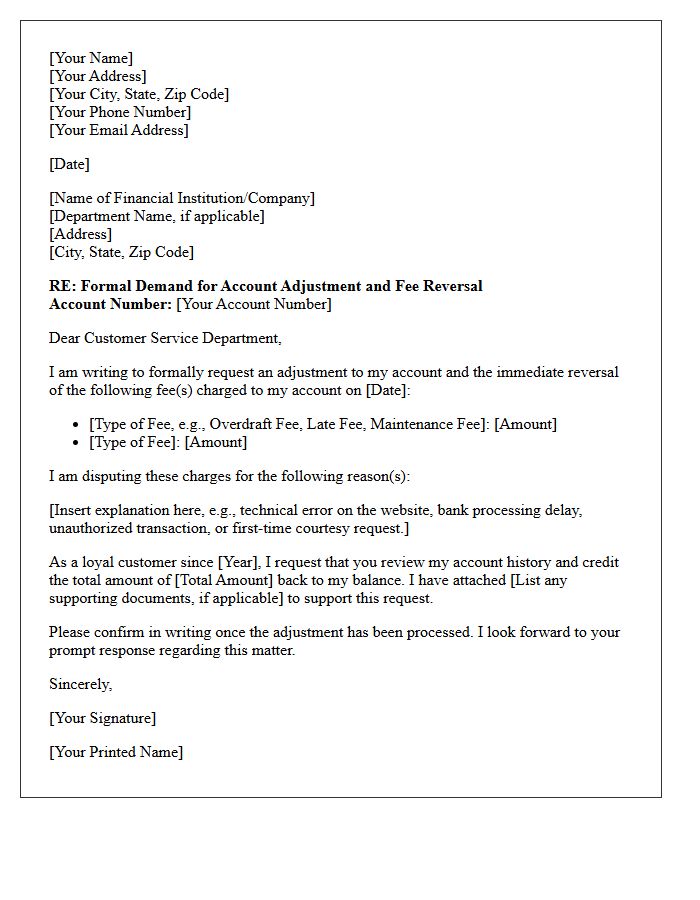

Demand for Account Adjustment and Fee Reversal Letter

A Demand for Account Adjustment and Fee Reversal Letter is a formal request sent to a financial institution to correct errors or waive unjustified charges. This document should clearly state the specific transaction details, the reason for the dispute, and the desired resolution. Utilizing this written record helps protect your consumer rights under banking regulations. By professionally outlining discrepancies such as late fees, overcharges, or interest miscalculations, you increase the likelihood of a successful refund and ensure your financial statements accurately reflect your true balance.

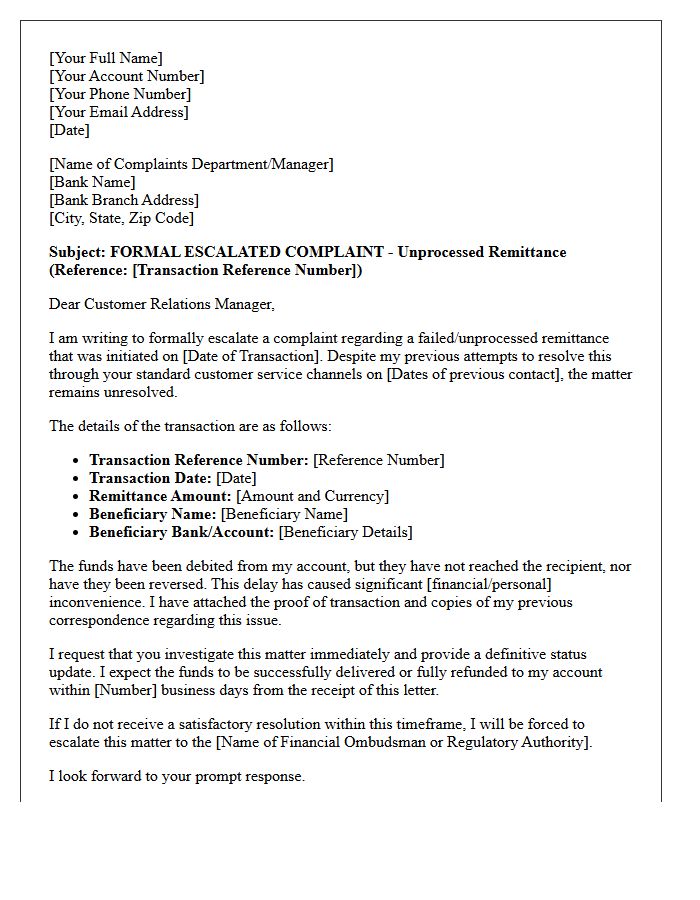

Escalated Complaint of Unprocessed Bank Remittance Letter

An Escalated Complaint of Unprocessed Bank Remittance Letter is a formal formal demand sent to senior management or regulatory bodies when a wire transfer remains pending without resolution. This document should clearly state the transaction reference number, exact amount, and the duration of the delay. To ensure regulatory compliance, emphasize the financial impact of the missing funds. Attaching original transfer receipts provides essential evidence, forcing the financial institution to prioritize your case and expedite the funds recovery process through their highest internal review channels.

Notice of Improper Principal and Interest Application Letter

A Notice of Improper Principal and Interest Application Letter is a formal document used to dispute how a lender allocates your mortgage payments. This notice is essential if you suspect an accounting error where funds were incorrectly applied to fees rather than reducing your loan balance. Under federal law, sending this qualified written request forces the servicer to investigate and correct misapplied payments. Timely action ensures your amortization schedule remains accurate, preventing unnecessary interest charges and protecting your home equity from being eroded by systemic servicing mistakes.

Proof of Cleared Payment and Application Request Letter

A Proof of Cleared Payment serves as definitive evidence that funds have successfully moved from the sender to the recipient's bank. When paired with an Application Request Letter, it validates your financial commitment to a specific transaction or service. This formal correspondence should clearly state the purpose of the payment, provide transaction reference numbers, and include authenticated bank receipts. Providing these documents together ensures transparency, prevents processing delays, and provides legal protection by confirming that all fiscal obligations have been met for your pending application.

Final Warning Before Regulatory Banking Complaint Letter

Before submitting a formal banking complaint to a regulator, you must issue a Final Warning letter to your financial institution. This document serves as a "Letter Before Action," providing the bank a last opportunity to resolve the dispute internally. It should clearly outline the unresolved issues, specify your requested redress, and state a firm deadline for their response. Demonstrating that you have exhausted the bank's internal grievance process is essential for regulatory bodies to accept and investigate your case, ensuring your legal standing is protected throughout the escalation process.

Request for Audit of Unapplied Loan Installment Letter

A Request for Audit of Unapplied Loan Installment Letter is a formal document used to dispute payment discrepancies. This letter instructs your lender to investigate why specific installments were not credited to your balance. It is a crucial consumer right that ensures financial transparency and prevents unfair late fees. By requesting a detailed transaction history, you can identify misapplied funds and verify that every payment was correctly allocated toward principal or interest, protecting your credit score from errors caused by administrative oversight or technical glitches.

What is a Notice of Failure to Apply Loan Payment Correctly?

This notice is a formal communication sent to a financial institution informing them that a submitted payment was not credited to the loan account accurately, was applied to the wrong balance, or was not processed according to the loan agreement terms.

How do I dispute a misapplied loan payment?

To dispute a misapplied payment, you should send a written notice to your lender's "Error Resolution" or "Qualified Written Request" address. Include your account number, the payment date, the specific amount in question, and a copy of your proof of payment such as a bank statement or canceled check.

What details should be included in a payment error notice?

The notice should include your full name, account number, the transaction date, the specific dollar amount involved, and a clear explanation of why you believe the payment was applied incorrectly, such as funds being applied to late fees instead of the principal balance.

How long does a lender have to respond to a payment error notice?

Under federal regulations like the Real Estate Settlement Procedures Act (RESPA), lenders generally must acknowledge receipt of your notice within five business days and must resolve the error or provide a justification for the application of funds within 30 business days.

Can a misapplied payment affect my credit score?

Yes, if a payment is applied incorrectly, the lender may erroneously report the account as delinquent. If you provide a Notice of Failure to Apply Loan Payment Correctly, the lender is often prohibited from reporting negative information to credit bureaus regarding that specific payment until the investigation is complete.

Comments