If you have been charged for a transaction you did not authorize or a service that was never delivered, you may need to file a Request for Chargeback Initiation with your bank. This formal process helps recover your funds by disputing the transaction directly through your card issuer. To simplify the process, below are some ready to use template.

Image cover: Streamlined Guide to Requesting a Chargeback: Templates and Best Practices

Letter Samples List

- Letter for Fraudulent Transaction Chargeback Initiation

- Chargeback Initiation Request Letter for Undelivered Goods

- Letter of Request for Duplicate Billing Chargeback Initiation

- Defective Merchandise Chargeback Initiation Request Letter

- Letter for Canceled Subscription Chargeback Initiation

- Incorrect Transaction Amount Chargeback Initiation Request Letter

- Letter of Chargeback Initiation for Unrecognized Account Charge

- Service Not Rendered Chargeback Initiation Request Letter

- Letter for Chargeback Initiation Regarding Unprocessed Refund

- ATM Dispense Error Chargeback Initiation Request Letter

- Letter Requesting Chargeback Initiation for Counterfeit Items

- Unauthorized Recurring Payment Chargeback Initiation Letter

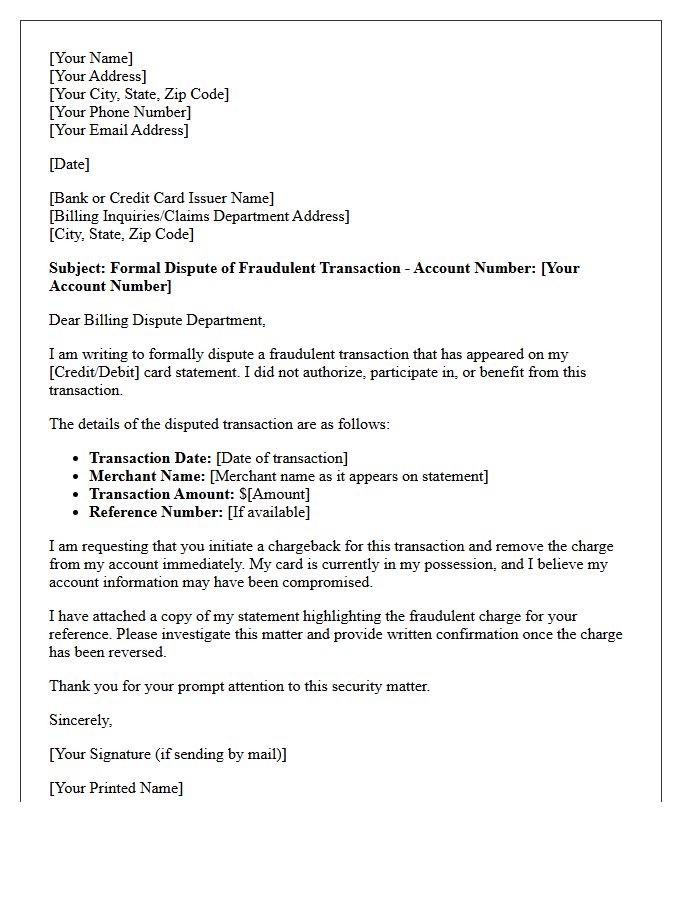

Letter for Fraudulent Transaction Chargeback Initiation

When drafting a letter for a fraudulent transaction chargeback initiation, clearly state you are disputing unauthorized activity. Include your account details, the specific transaction date, and the exact merchant name. Under federal law, your legal protection often limits liability for unauthorized charges if reported promptly. Attach supporting evidence, such as a police report or screenshots of the suspicious activity, to strengthen your claim. Explicitly request a permanent credit to your account and a formal investigation. Send the notice via certified mail to ensure a documented paper trail of your dispute with the financial institution.

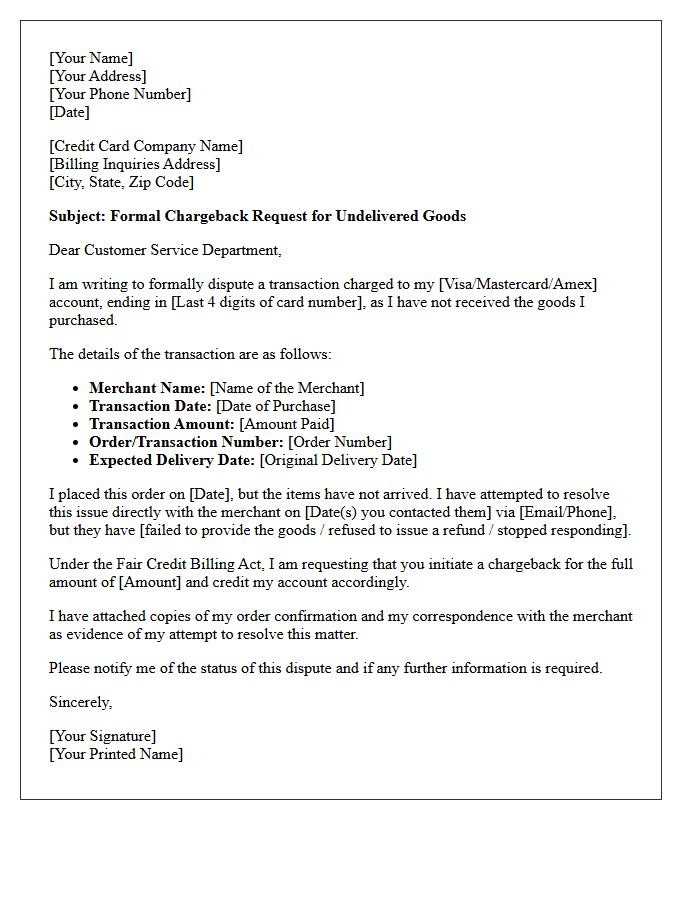

Chargeback Initiation Request Letter for Undelivered Goods

A Chargeback Initiation Request Letter is a formal document sent to your bank to dispute a transaction for undelivered goods. It must clearly state the transaction date, amount, and merchant details. Providing evidence that the delivery deadline passed and that you attempted to resolve the issue directly with the seller is essential. This letter invokes your consumer rights under banking regulations to secure a refund. Timeliness is critical, as most financial institutions enforce strict deadlines for filing disputes following the expected delivery date.

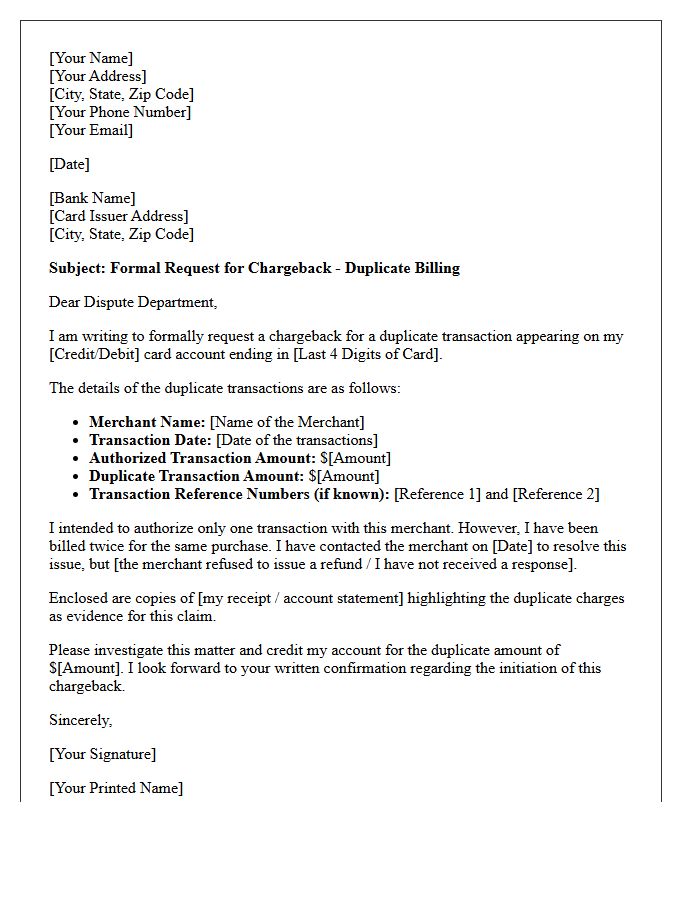

Letter of Request for Duplicate Billing Chargeback Initiation

A Letter of Request for Duplicate Billing Chargeback Initiation is a formal notification sent to a bank to dispute multiple charges for a single transaction. To ensure success, clearly state the transaction date, amount, and merchant name while providing evidence of the double payment. Acting quickly is vital, as most financial institutions impose a strict 60-day deadline for filing disputes under consumer protection laws. Including a copy of your billing statement highlighting the repetitive entries will expedite the recovery of your funds and resolve the clerical error efficiently.

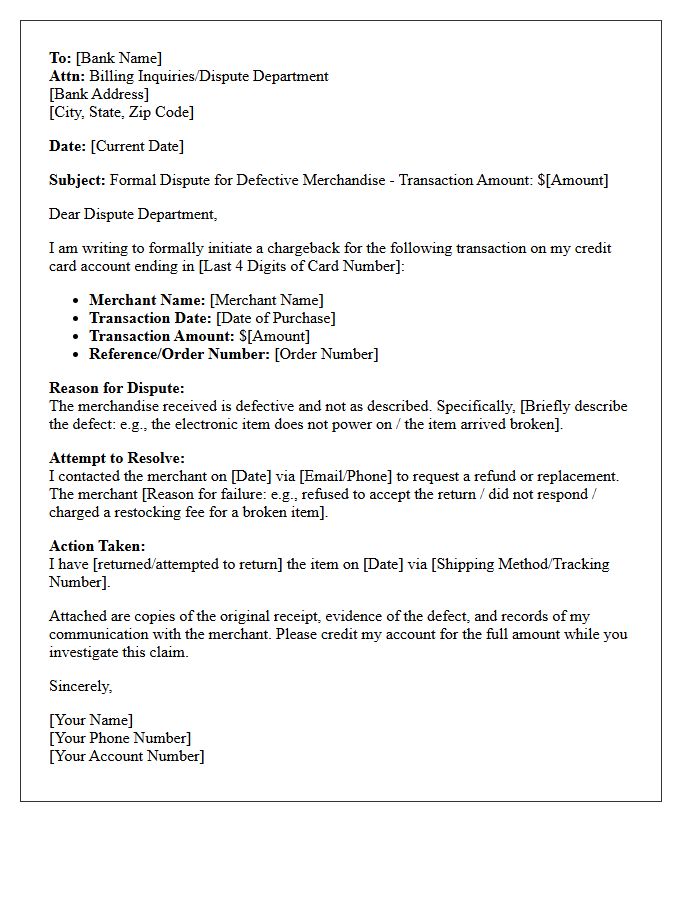

Defective Merchandise Chargeback Initiation Request Letter

A Defective Merchandise Chargeback Initiation Request Letter is a formal document sent to your bank to dispute a transaction. It is essential when a merchant refuses to refund items that are damaged, malfunctioning, or not as described. To be effective, the letter must include specific transaction details, evidence of the defect, and proof of your attempted resolution with the seller. Timeliness is critical, as most financial institutions require these requests within 60 to 120 days of purchase to protect your consumer rights and recover lost funds.

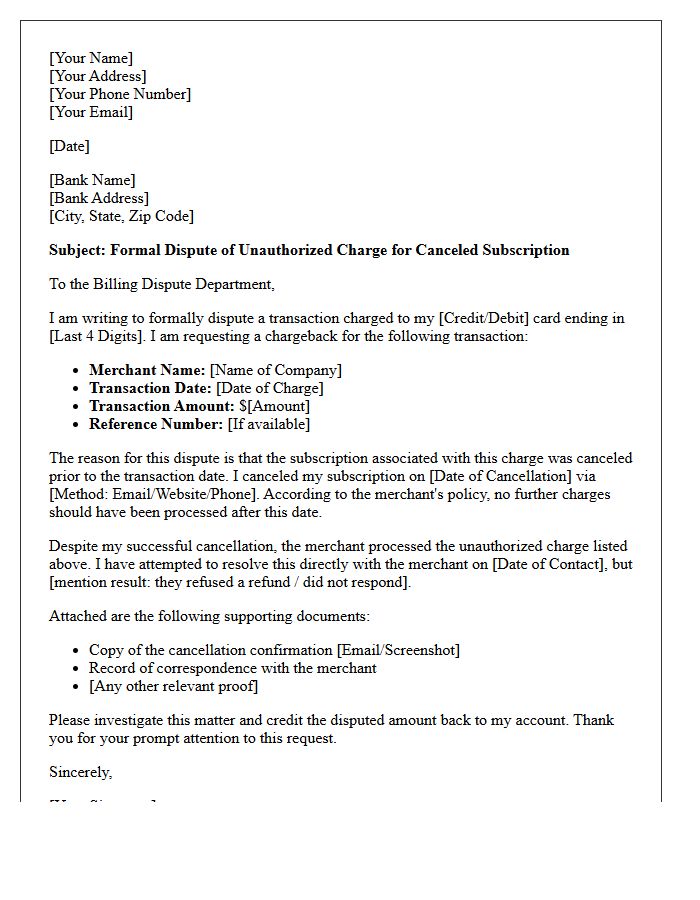

Letter for Canceled Subscription Chargeback Initiation

A formal letter for a canceled subscription chargeback initiation serves as documentary evidence to prove a merchant processed an unauthorized transaction after a service was terminated. This communication must clearly state the cancellation date, include the confirmation number, and provide proof of the original request. Banks prioritize these records to verify that the consumer attempted to resolve the issue directly before disputing the fee. Ensuring your cancellation policy compliance is documented significantly increases the likelihood of a successful refund through the financial institution's formal dispute resolution process.

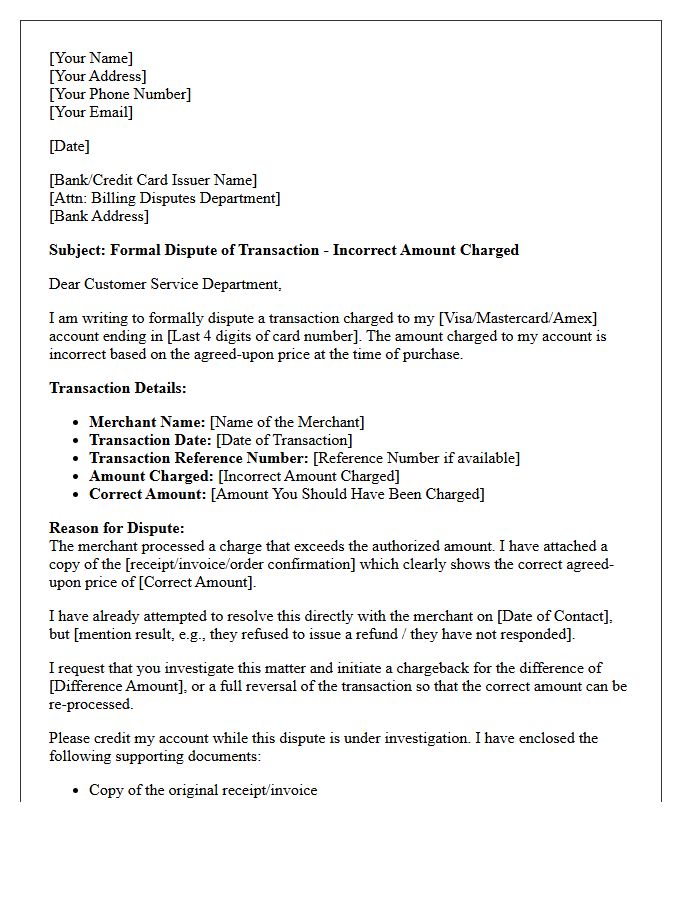

Incorrect Transaction Amount Chargeback Initiation Request Letter

An Incorrect Transaction Amount chargeback letter is a formal dispute initiation used when a merchant processes a payment for the wrong total. To ensure a successful claim, you must provide compelling evidence, such as an itemized receipt or invoice, showing the agreed-upon price versus the actual charge. Clearly state the transaction date, reference number, and the specific discrepancy amount. This document serves as legal proof that the billing error occurred, helping your bank recover the overcharged funds through the card network's protection policies.

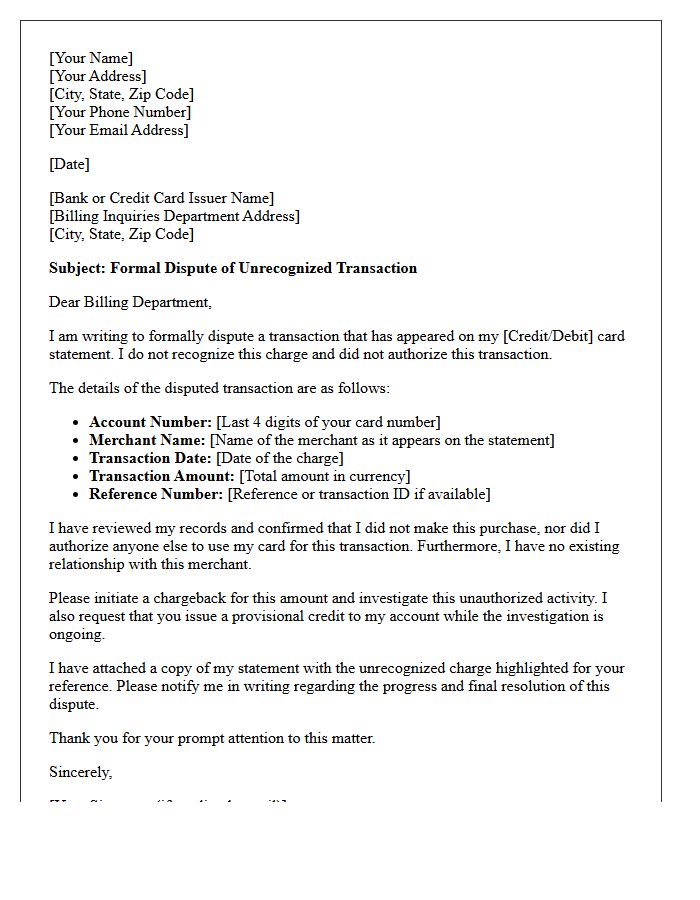

Letter of Chargeback Initiation for Unrecognized Account Charge

When disputing an unrecognized account charge, your letter must include the specific transaction date, amount, and merchant name. Clearly state that you did not authorize the payment and request a formal investigation. To protect your rights under the Fair Credit Billing Act, send this Letter of Chargeback Initiation to your bank within 60 days of the statement date. Providing clear evidence that the transaction was unsolicited or fraudulent helps expedite the reversal of funds. Always maintain a copy of the correspondence for your personal financial records.

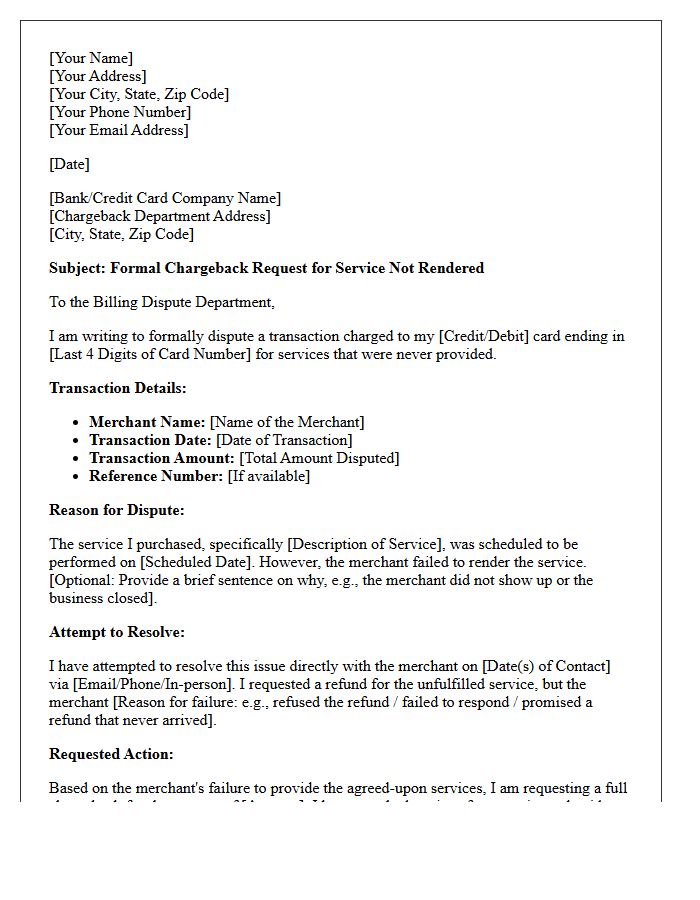

Service Not Rendered Chargeback Initiation Request Letter

A Service Not Rendered Chargeback Initiation Request Letter is a formal document sent to your bank to dispute a transaction when a merchant fails to deliver promised services. To ensure success, clearly state the transaction date, merchant name, and the specific amount. You must provide evidence that you attempted to resolve the issue directly with the provider first. Including cancellation confirmations or contracts is vital. This letter invokes your consumer rights under the Fair Credit Billing Act to recover funds for unfulfilled obligations efficiently.

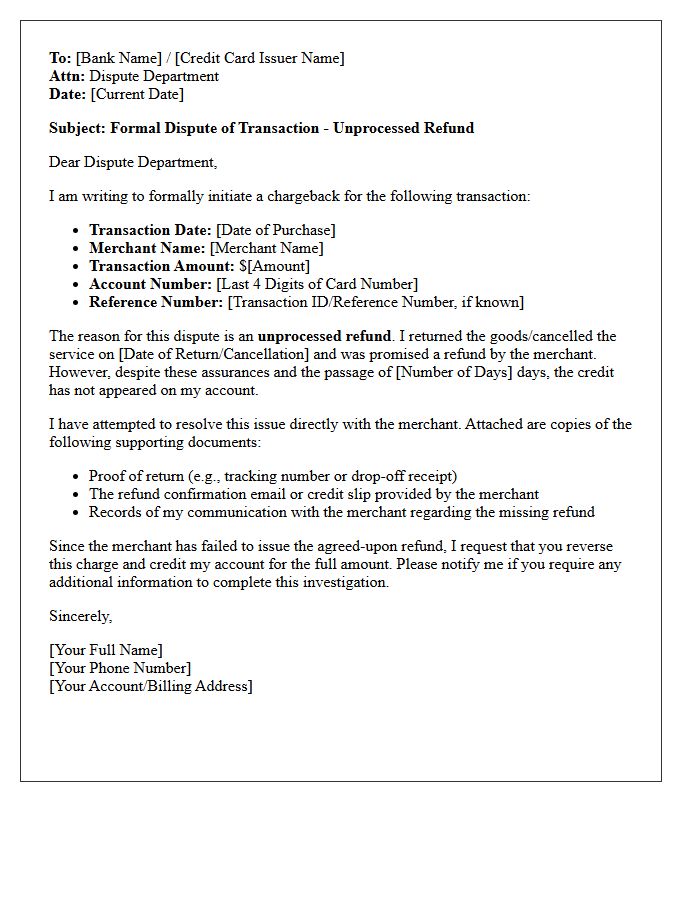

Letter for Chargeback Initiation Regarding Unprocessed Refund

When writing a chargeback initiation letter for an unprocessed refund, clarity is essential. Formally document that the merchant failed to issue a credited reversal despite a valid cancellation or return. Include your transaction date, reference number, and specific evidence of the refund promise. Explicitly state that you are disputing the charge under Fair Credit Billing Act guidelines due to a "credit not processed" error. Providing clear proof of communication helps the bank resolve the dispute quickly, ensuring you recover your rightful funds effectively.

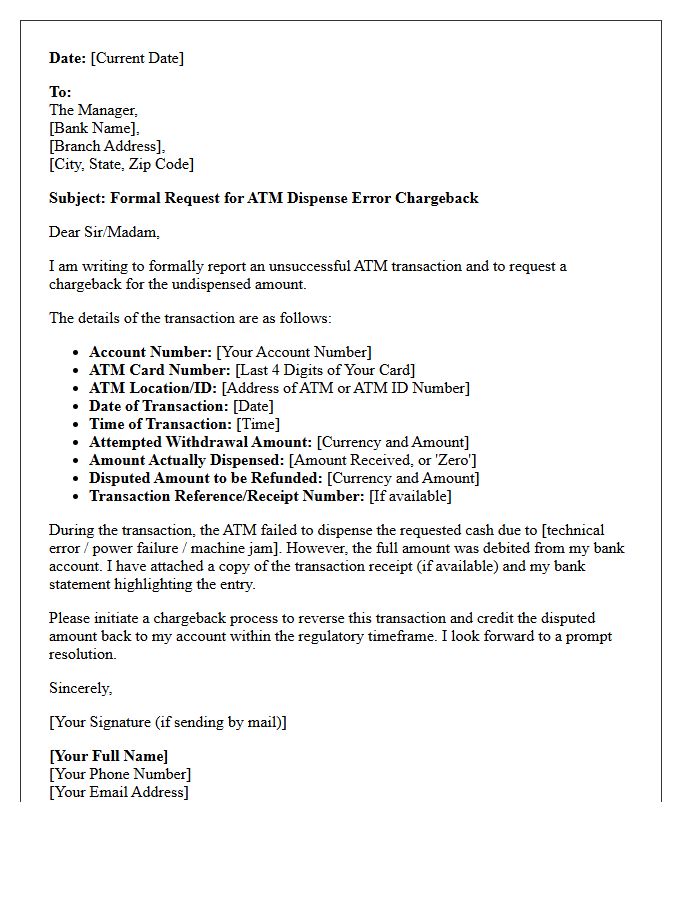

ATM Dispense Error Chargeback Initiation Request Letter

An ATM Dispense Error Chargeback request is a formal letter sent to your bank when an automated teller machine fails to provide the requested cash but still debits your account. To initiate this, you must clearly state the transaction date, exact location, and amount. Attaching the discrepancy receipt or a copy of your bank statement is vital evidence. This letter ensures a legal record of the dispute, compelling your financial institution to investigate the technical failure and reverse the incorrect charge promptly under consumer protection regulations.

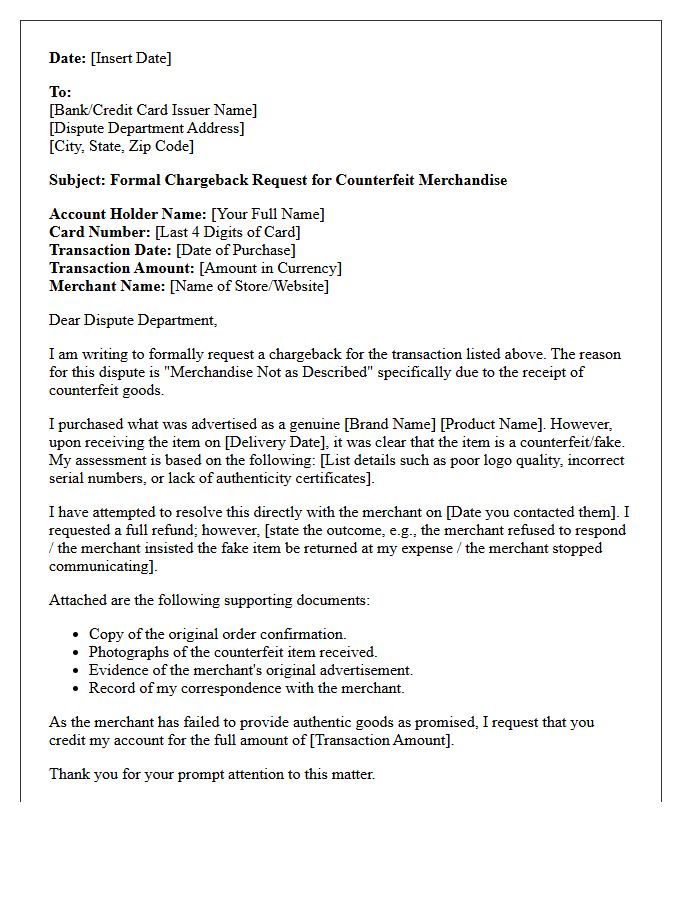

Letter Requesting Chargeback Initiation for Counterfeit Items

When drafting a letter to request a chargeback for counterfeit goods, clearly state that the item received is a replica or unauthorized imitation. Explicitly mention that the product violates the original manufacturer's intellectual property and differs significantly from the description. Include your order number, date of purchase, and documentation showing you attempted to resolve the issue with the merchant first. Providing evidence of the counterfeit nature, such as photos or expert assessments, strengthens your claim under consumer protection regulations and credit card issuer policies for non-conforming merchandise.

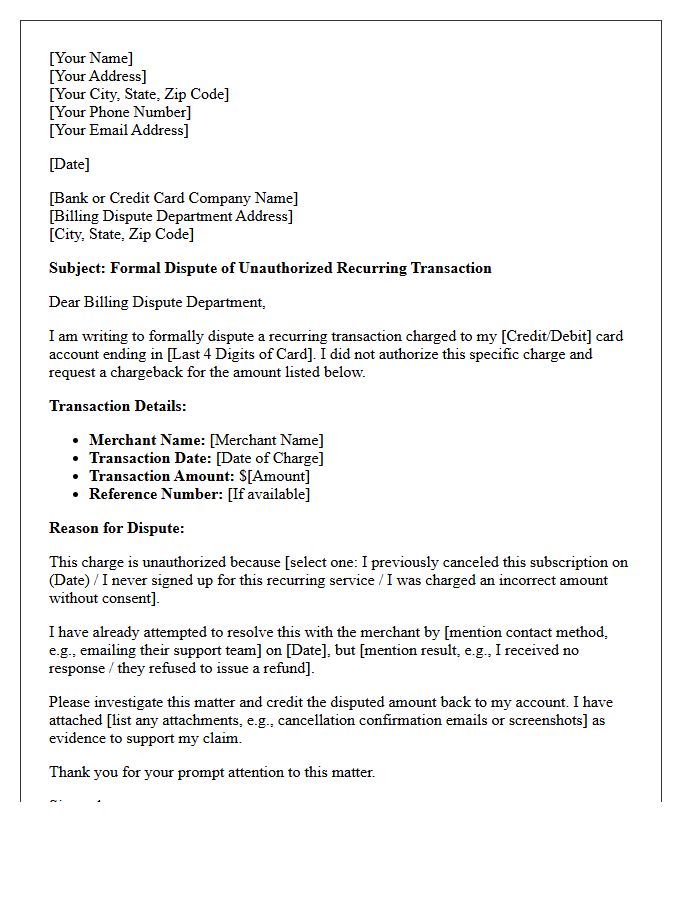

Unauthorized Recurring Payment Chargeback Initiation Letter

An Unauthorized Recurring Payment Chargeback Initiation Letter is a formal notification sent to a financial institution to dispute automated billing errors. This document must clearly state that the merchant lacked valid authorization or failed to honor a cancellation request. Providing specific transaction details and evidence of communication with the vendor is essential to recover funds. Timely submission is critical under banking regulations to protect your consumer rights and successfully reverse fraudulent or erroneous subscription fees during the formal dispute process.

How do I initiate a chargeback request for a transaction?

To initiate a chargeback, you must contact your issuing bank or credit card provider directly. You will need to provide the transaction details, the reason for the dispute, and any supporting documentation, such as receipts or correspondence with the merchant.

What are the valid reasons for requesting a chargeback?

Common valid reasons for a chargeback initiation include unauthorized fraudulent transactions, items not received, services not rendered as described, duplicate billing, or instances where a refund was promised by the merchant but never processed.

How long do I have to file a chargeback after a purchase?

Typically, cardholders have 120 days from the transaction date or the expected delivery date to initiate a chargeback. However, these timeframes can vary depending on the card network (Visa, Mastercard, Amex) and the specific reason code for the dispute.

What documentation is required to support a chargeback claim?

To strengthen your chargeback request, provide copies of order confirmations, tracking numbers, screenshots of the product description, and evidence of your attempts to resolve the issue with the merchant before contacting the bank.

What is the difference between a refund and a chargeback?

A refund is initiated voluntarily by the merchant to return funds to the customer. A chargeback is a forced reversal of funds initiated by the bank after a customer disputes a charge, often resulting in additional fees for the merchant.

Comments