A Notice of Offset is a legal action where a financial institution seizes funds from a client's deposit account to cover an outstanding debt. This process, often called the right of set-off, typically occurs without prior court intervention when loan payments are delinquent. Understanding your rights and the necessary documentation is essential. To assist you, below are some ready to use templates.

Image cover: Official Notice of Offset: Debt Collection Templates and Samples for Deposit Accounts

Letter Samples List

- Official Bank Institution Letterhead

- Date of Notice Letter Generation

- Primary Accountholder Name and Address

- Reference to Delinquent Loan Account Number

- Reference to Active Deposit Account Number

- Subject Letter Notice of Administrative Offset

- Declaration of Executed Funds Transfer

- Exact Monetary Amount Deducted from Deposit

- Remaining Outstanding Balance on Unpaid Debt

- Available Ledger Balance in Depository Account

- Statutory Right of Offset Clause Citation

- Customer Service Contact for Dispute Resolution

- Authorized Collections Officer Signature

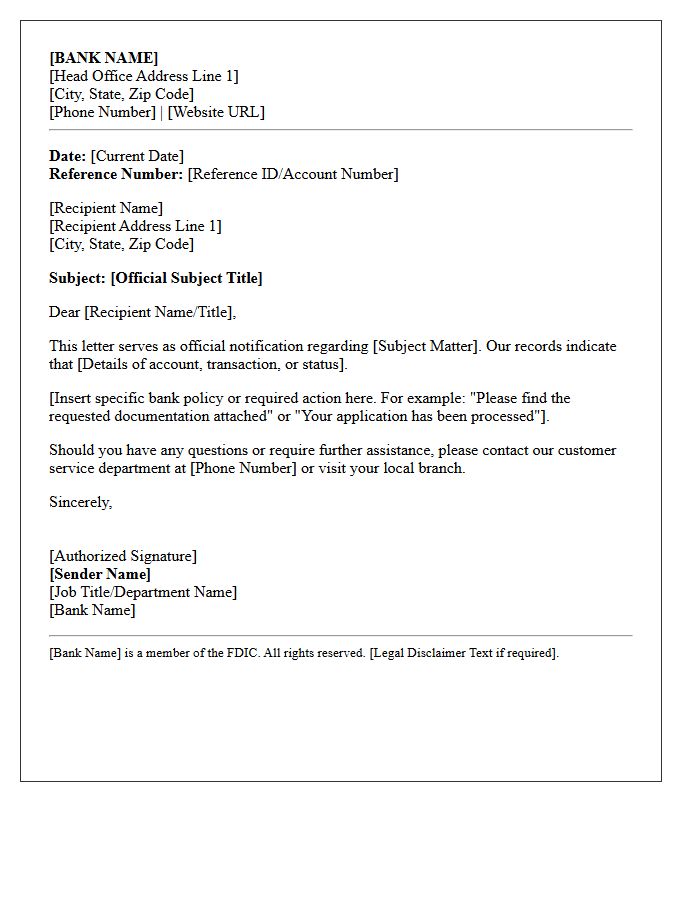

Official Bank Institution Letterhead

An Official Bank Institution Letterhead serves as a critical authentication tool for financial documents. It must feature the bank's legal name, logo, and contact details to ensure validity. Most institutions require this format for proof of funds, loan approvals, or account verification. When submitting paperwork for legal or immigration purposes, ensuring the letterhead includes an authorized signature and official stamp is essential. This standardized format protects against fraud and confirms that the information originates directly from a regulated financial entity, maintaining the document's integrity and professional credibility.

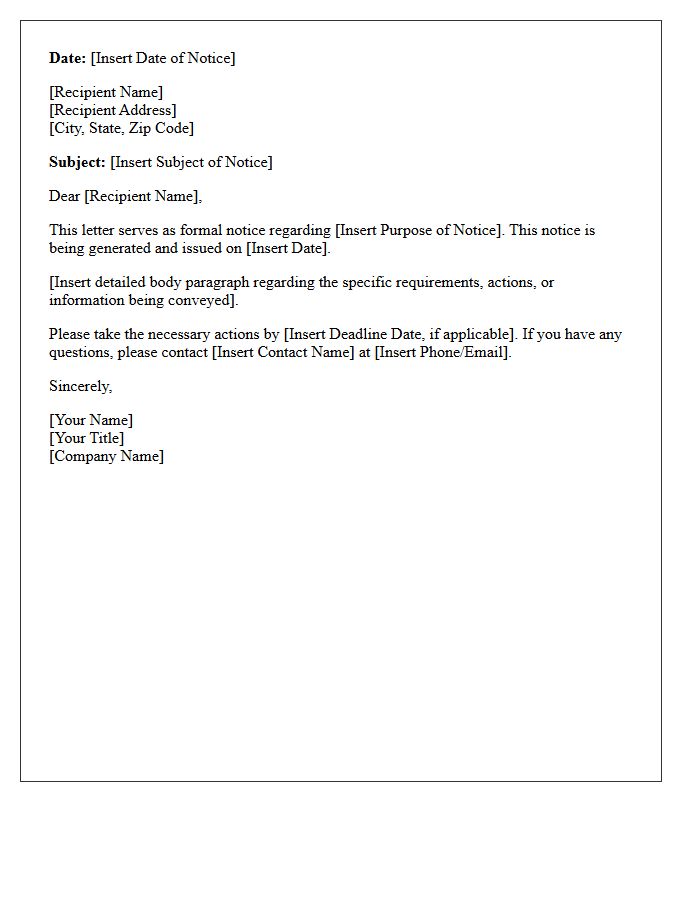

Date of Notice Letter Generation

The Date of Notice Letter Generation marks the official moment a document is created within a system. This specific date is critical for compliance and legal timelines, as it often triggers the start of dispute periods or payment deadlines. It may differ from the postmark or delivery date, making it the primary reference point for administrative tracking. Understanding this date ensures you meet essential regulatory requirements and respond to notifications within the mandated timeframe to avoid penalties or loss of rights.

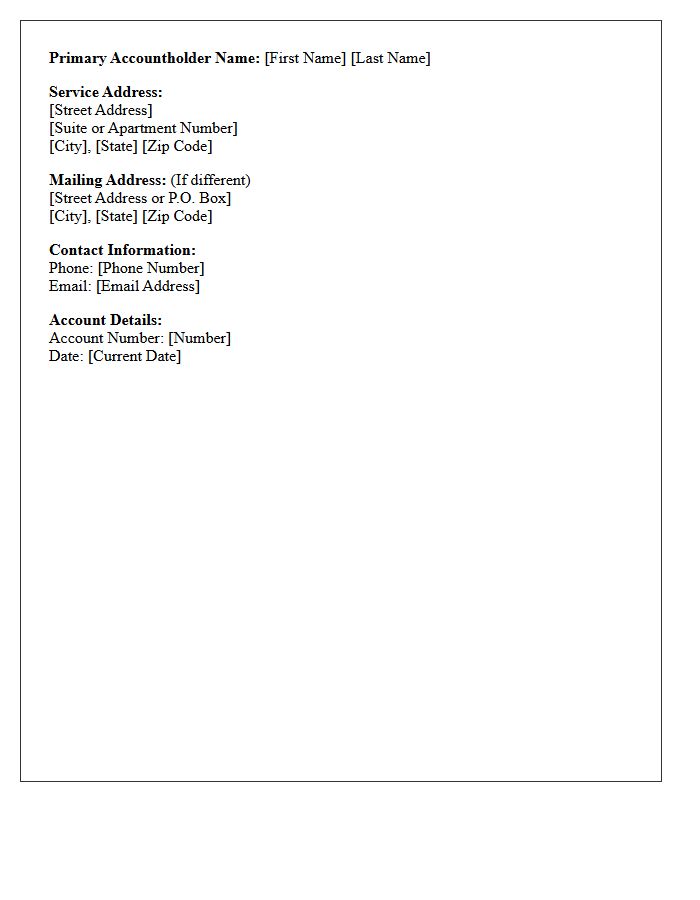

Primary Accountholder Name and Address

The Primary Accountholder Name and Address represent the legal identity responsible for a financial or service contract. This individual serves as the main point of contact and carries full legal liability for all transactions, fees, and account management. Accuracy is vital, as this information determines where official correspondence, tax documents, and billing statements are delivered. Ensuring these details match valid government identification is essential for identity verification and maintaining account security across all platforms.

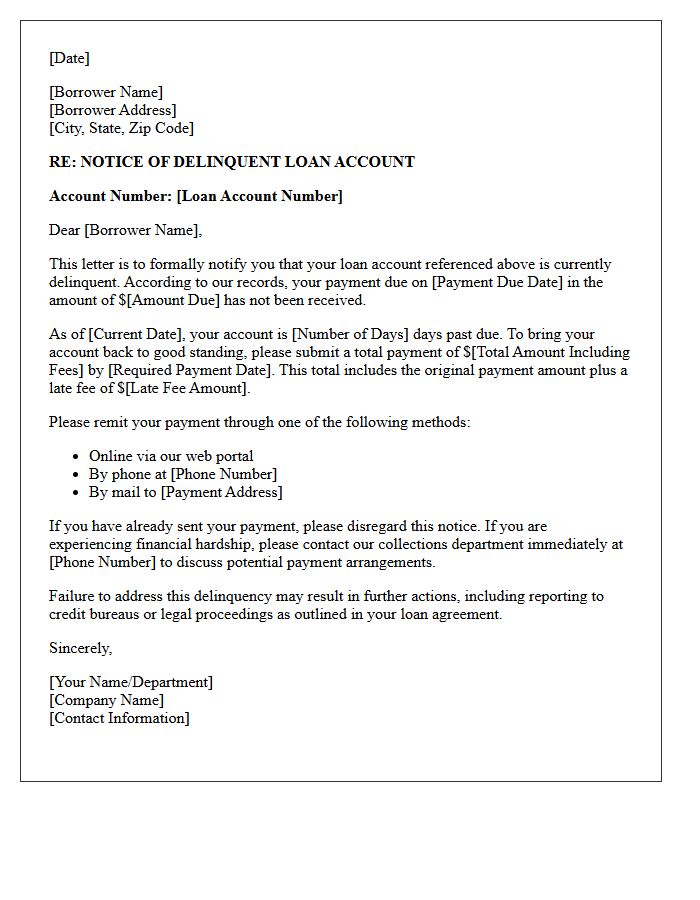

Reference to Delinquent Loan Account Number

A Delinquent Loan Account Number is the unique identifier used to track credit obligations that have missed scheduled payments. When an account enters delinquency, providing this reference number is essential for communicating with lenders or debt recovery agencies. It ensures that payments are applied correctly to the specific debt and helps borrowers verify the legitimacy of collection notices. Keeping this number accessible allows for faster resolution of past-due balances and aids in protecting your overall credit health from further negative reporting.

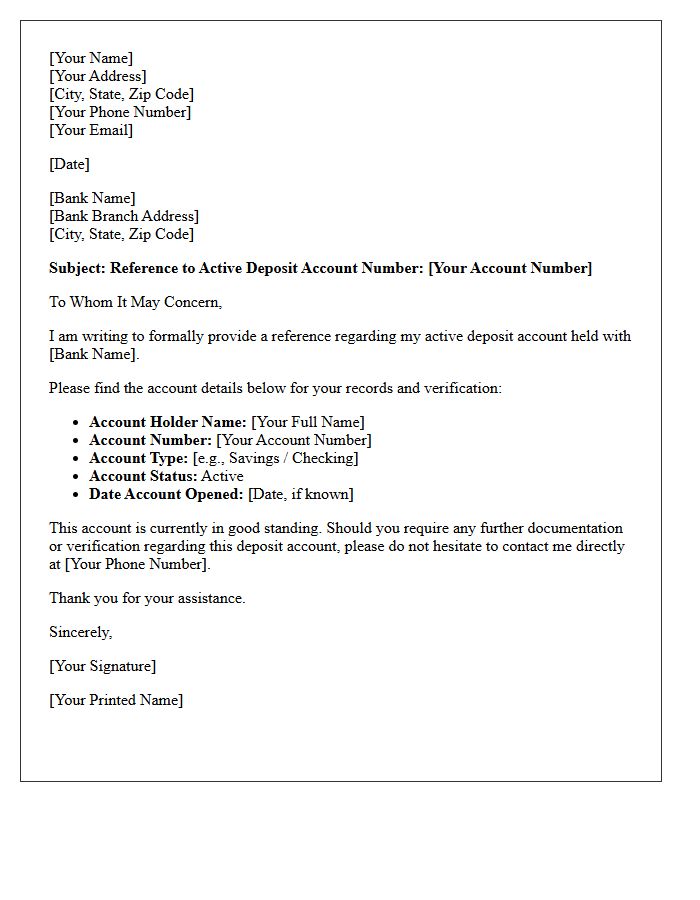

Reference to Active Deposit Account Number

A Reference to Active Deposit Account Number is a unique identifier used by financial institutions to link transactions, such as automated clearing house (ACH) transfers or direct deposits, to a specific customer's holdings. Ensuring the accuracy of this number is critical to prevent processing delays or misdirected funds. It serves as the primary link between your liquid assets and external payment systems, facilitating secure electronic movement of capital. Always verify this information against your official bank statements to maintain seamless financial connectivity and account security.

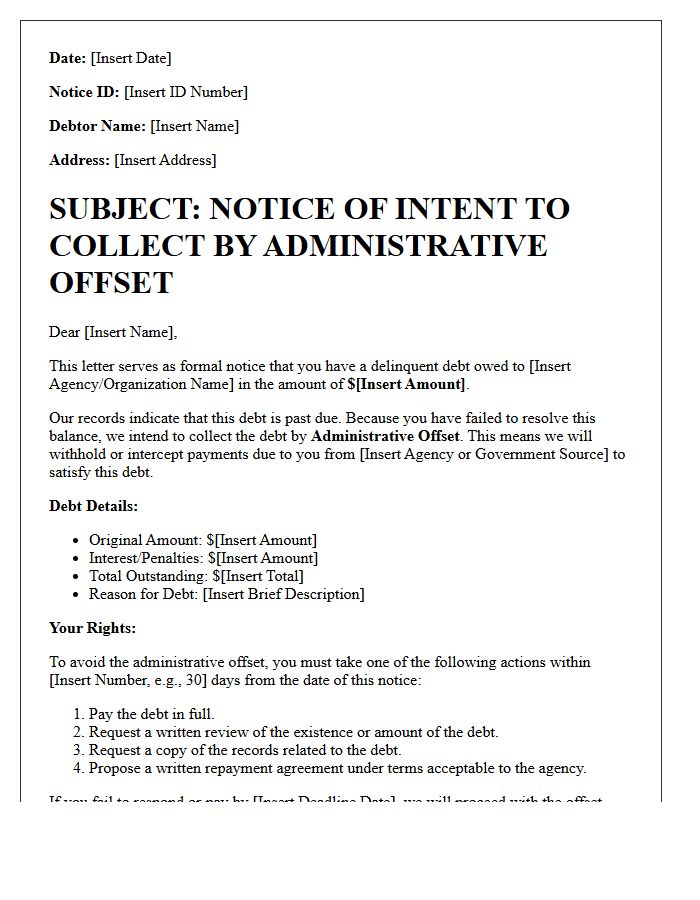

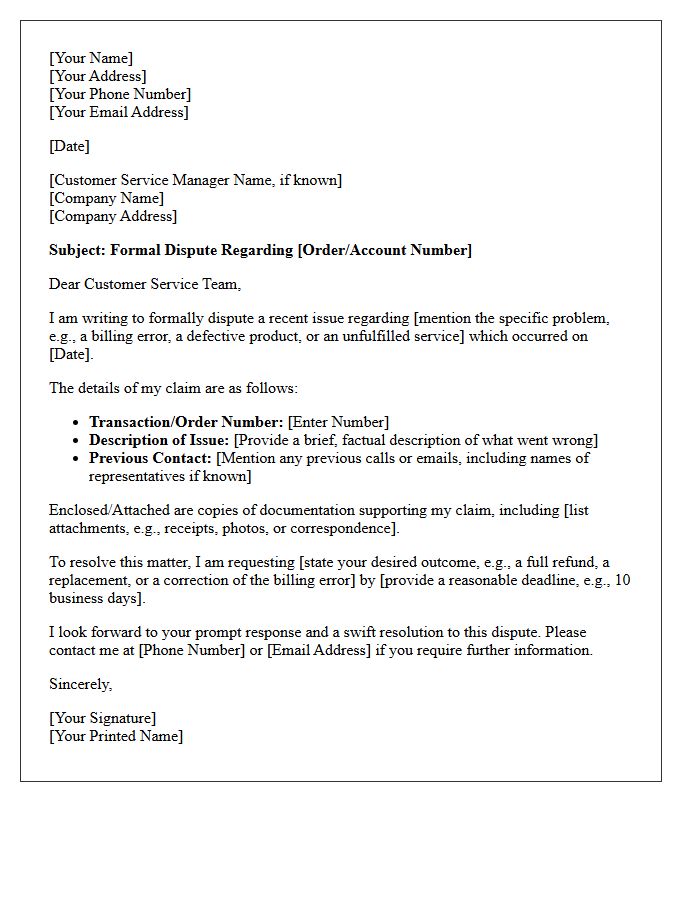

Subject Letter Notice of Administrative Offset

A Notice of Administrative Offset is a critical legal warning that the government intends to withhold federal payments, such as tax refunds or Social Security benefits, to satisfy a delinquent debt. Upon receipt, you have a limited window to pay the balance or request a review. Ignoring this letter may result in automatic debt collection through the Treasury Offset Program. To prevent immediate financial loss, you should verify the debt accuracy or establish a repayment agreement with the issuing agency as soon as possible to stop the offset process.

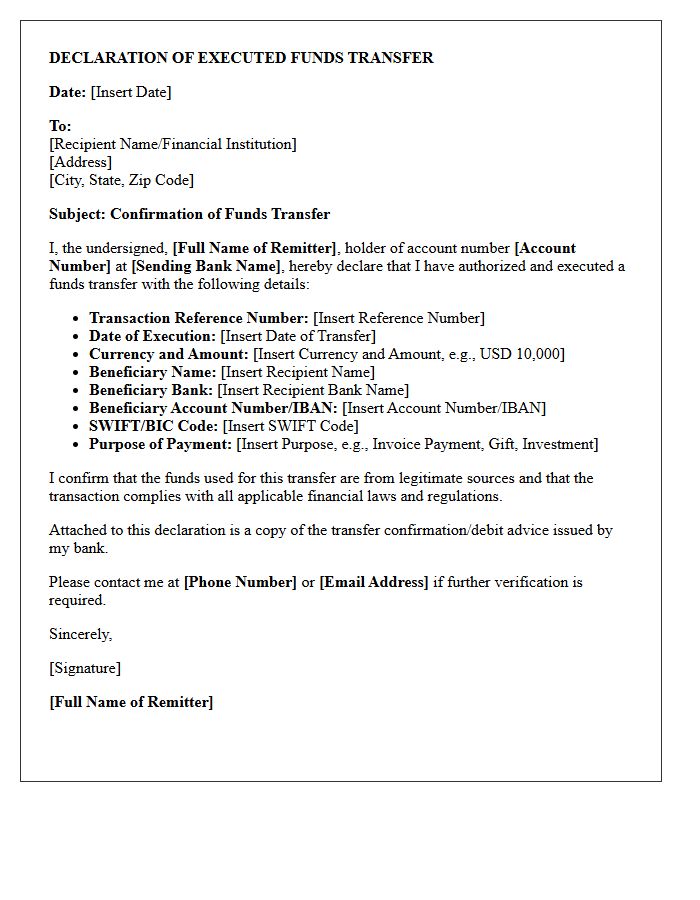

Declaration of Executed Funds Transfer

A Declaration of Executed Funds Transfer is a legal certification confirming that a specific payment has been successfully processed and settled. It serves as formal proof for financial institutions, tax authorities, and regulatory bodies to verify the legitimacy of high-value transactions. This document ensures compliance with Anti-Money Laundering (AML) protocols by detailing the sender, recipient, and purpose of the transfer. Accurate reporting is essential to mitigate financial liability and provide a transparent audit trail for international or commercial capital movements.

Exact Monetary Amount Deducted from Deposit

When ending a lease, your landlord must provide an itemized statement detailing the exact monetary amount deducted from your security deposit. This document should specify costs for repairs beyond normal wear and tear or unpaid rent. Most jurisdictions require this written notice within a strict legal timeframe, typically 14 to 30 days. Always request copies of original receipts or invoices to verify that each deduction is reasonable and accurate. Understanding these figures ensures your financial rights are protected and helps resolve potential disputes regarding your remaining balance.

Remaining Outstanding Balance on Unpaid Debt

The remaining outstanding balance represents the total unpaid portion of a debt, excluding future interest. It is the specific amount a borrower must repay to satisfy the obligation. Monitoring this figure is crucial for effective financial planning and debt management. Accurate tracking ensures you understand how payments reduce the principal over time. For many loans, this balance dictates the interest accrued in the next cycle, making it the most vital metric for achieving debt freedom and maintaining a healthy credit profile through consistent monitoring.

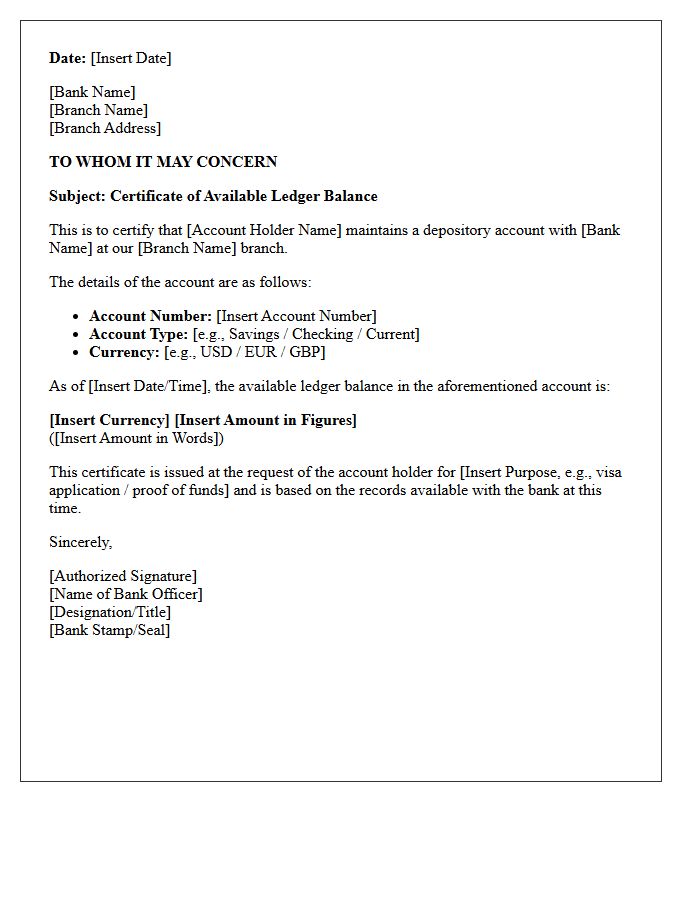

Available Ledger Balance in Depository Account

The available ledger balance represents the total amount of funds present in a depository account at the start of a business day. While it includes all settled transactions, it may not reflect pending withdrawals or uncollected funds. Therefore, this figure differs from the available balance, which indicates the actual money ready for immediate use. Understanding this distinction is crucial for effective cash management to avoid potential overdraft fees or transaction declines when processing payments against Uncleared deposits.

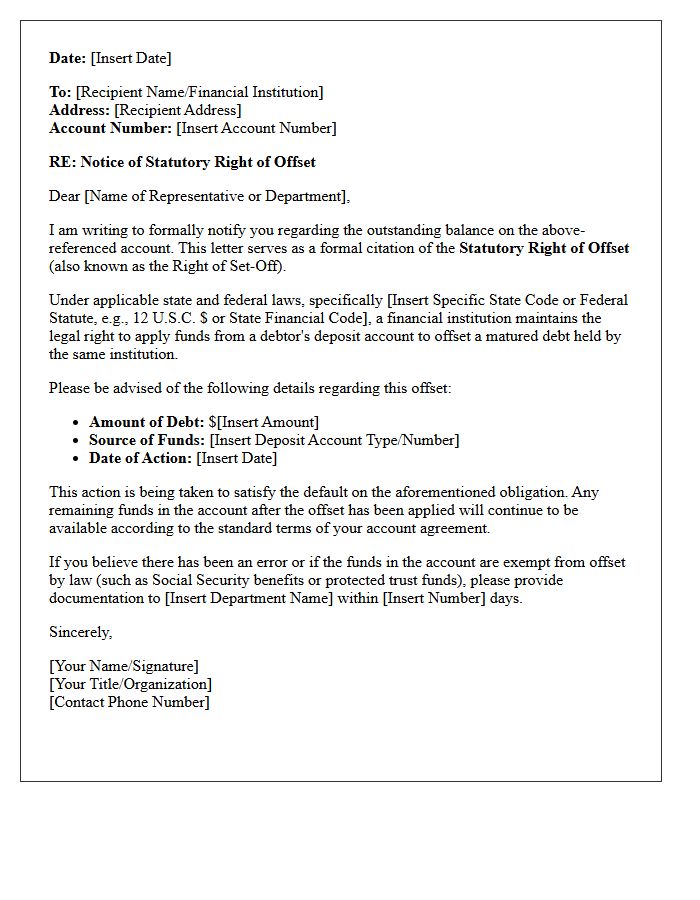

Statutory Right of Offset Clause Citation

A Statutory Right of Offset is a legal provision, often cited under 11 U.S.C. § 553 in bankruptcy contexts, allowing a creditor to cancel mutual debts owed to and from a debtor. This equitable remedy permits a bank or entity to apply a customer's deposited funds to satisfy an outstanding defaulted loan balance. It functions as a form of security, ensuring debt recovery without separate litigation. Understanding this offset clause is essential for managing credit risk and protecting assets during insolvency proceedings or contractual disputes.

Customer Service Contact for Dispute Resolution

When seeking dispute resolution, your primary point of contact is the customer service department. To ensure a swift outcome, maintain a detailed record of all communications, including dates and representative names. Clearly state your issue and provide supporting documentation, such as receipts or order numbers. If initial support cannot resolve the matter, politely request a supervisor or formal escalation. Clear, documented communication is the most effective way to reach a fair settlement and protect your consumer rights during any formal dispute process.

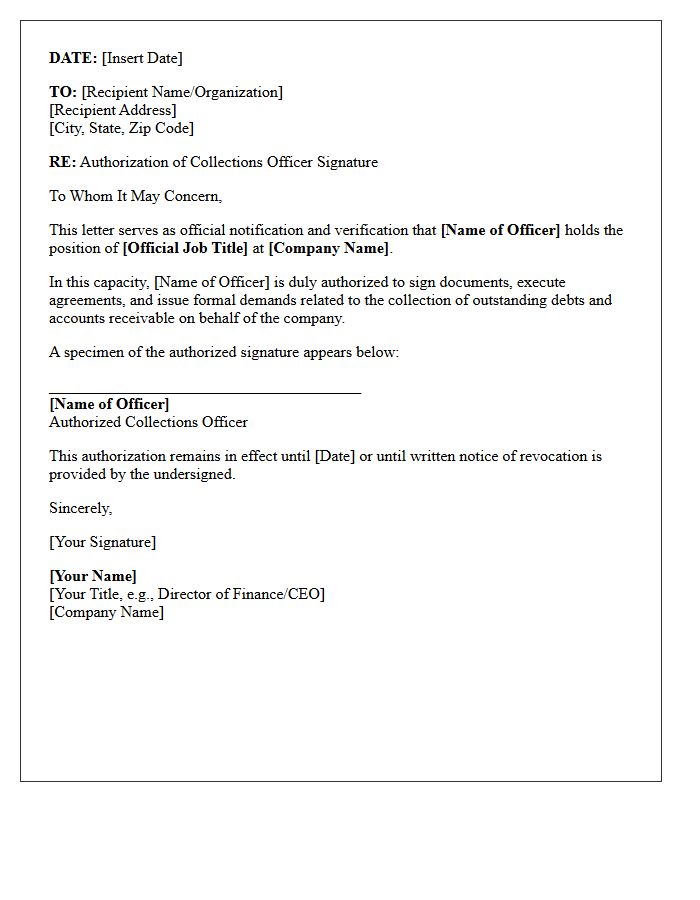

Authorized Collections Officer Signature

An Authorized Collections Officer Signature is a critical legal validation on official debt recovery documents. This signature confirms that the individual has the legal power to act on behalf of a creditor or government agency to collect outstanding balances. It ensures the authenticity of the notice and protects the rights of both parties by adhering to regulatory standards. Without this formal authorization, collection actions or garnishment orders may be considered invalid. Always verify this signature to ensure you are dealing with a legitimate authority during financial disputes.

What is a Notice of Offset Against Deposit Accounts?

A Notice of Offset is a formal notification informing a bank account holder that the financial institution has seized funds from their deposit account to cover a delinquent debt, such as an unpaid loan, credit card balance, or overdrawn account, owed to that same institution.

Under what legal right can a bank seize funds from my account?

Banks typically exercise the "Right of Setoff," a legal principle often included in account agreement contracts. This allows the bank to apply funds from a customer's checking or savings account to satisfy a matured or defaulted debt without seeking a prior court judgment.

Are certain types of income protected from a bank offset?

Yes, federal law generally prohibits banks from offsetting "protected" funds such as Social Security benefits, Supplemental Security Income (SSI), Veterans benefits, and federal student aid, provided these funds are clearly identifiable in the account.

Will I receive a warning before a bank offset occurs?

In most jurisdictions, banks are not required to provide advance notice before performing an offset. However, they are legally obligated to send a written Notice of Offset to the account holder immediately after the funds have been seized to explain the action taken.

How can I stop or reverse a Notice of Offset Against Deposit Accounts?

To challenge an offset, you should immediately contact the financial institution to prove the funds were exempt (such as Social Security), demonstrate that the debt was already paid, or negotiate a repayment plan to have the seized funds released back into your account.

Comments