Protect your financial rights by formalizing your dispute through a written grievance letter. If you identify unauthorized charges or calculation errors on your statement, a professional notification ensures your claim is documented under consumer protection laws. This guide explains how to effectively challenge inaccuracies and reclaim your funds. To help you get started immediately, below are some ready to use template options.

Image cover: Effective Credit Card Billing Dispute Letter Templates and Samples

Letter Samples List

- Grievance Letter for Unauthorized Credit Card Transaction

- Grievance Letter for Double Billing Discrepancy

- Grievance Letter for Unrecognized Subscription Charge

- Grievance Letter for Incorrect Transaction Amount

- Grievance Letter for Missing Refund Credit

- Grievance Letter for Unjustified Late Fee Assessment

- Grievance Letter for Overcharge on Foreign Exchange Transaction

- Grievance Letter for Uncredited Payment Discrepancy

- Grievance Letter for Cancelled Service Recurring Billing

- Grievance Letter for Fraudulent Charge Dispute

- Grievance Letter for Interest Charge Calculation Error

- Grievance Letter for Unapplied Promotional Cash Back

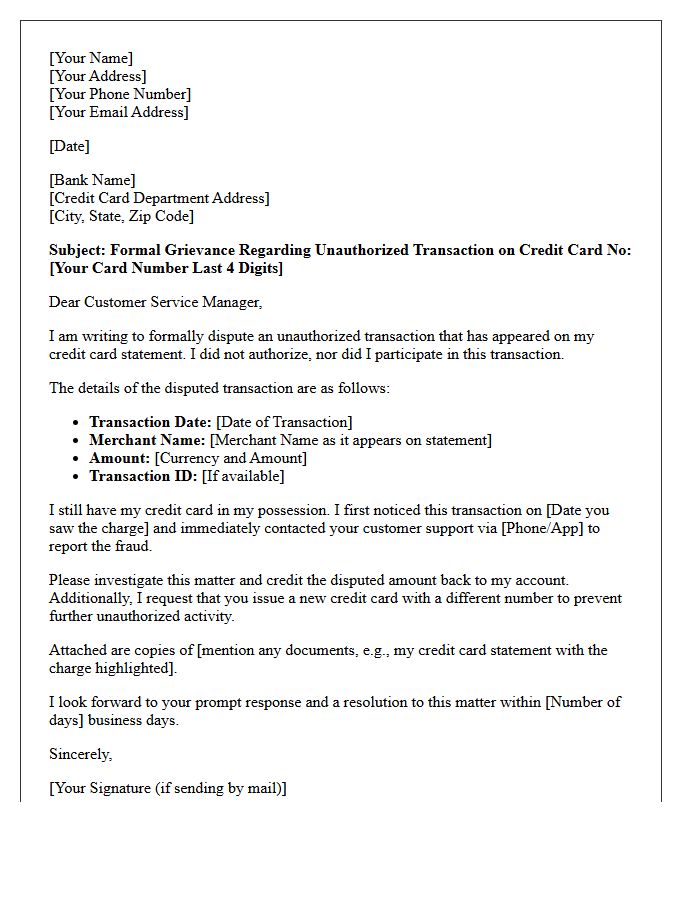

Grievance Letter for Unauthorized Credit Card Transaction

When drafting a grievance letter for an unauthorized credit card transaction, time is critical. Clearly state your account details, the specific date, and the exact amount of the fraudulent charge. Explicitly mention that you did not authorize the payment and request an immediate reversal of funds. Attach supporting evidence, such as transaction logs or police reports, to strengthen your claim. Sending this formal notice via certified mail ensures a documented trail, protecting your consumer rights under fair billing regulations while preventing long-term damage to your credit score.

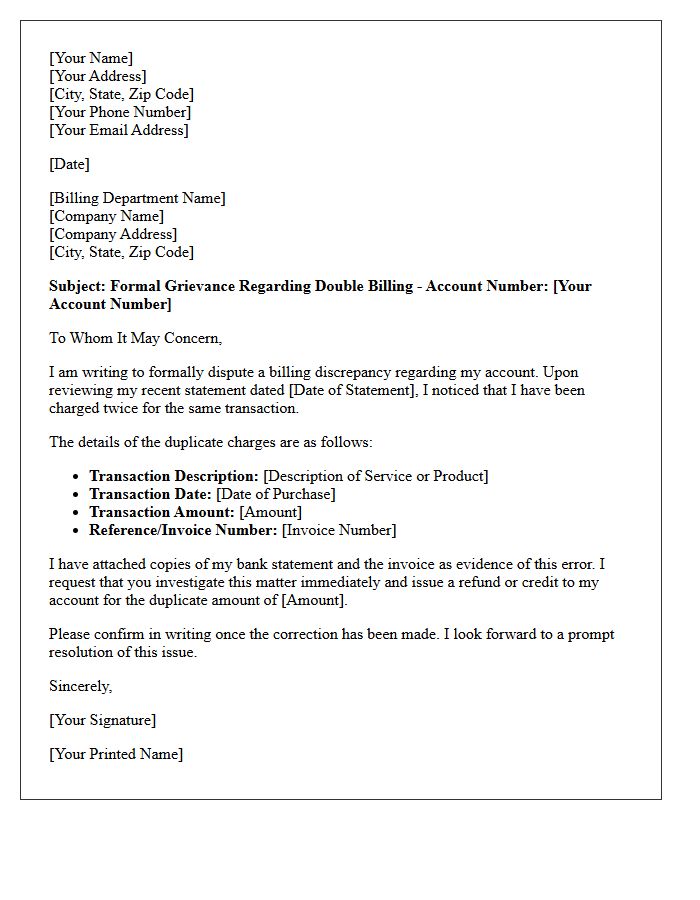

Grievance Letter for Double Billing Discrepancy

A grievance letter for a double billing discrepancy is a formal document used to dispute erroneous charges. To ensure a quick resolution, clearly state your account details, the specific transaction dates, and the exact overcharged amount. Attach supporting evidence, such as bank statements or receipts, to prove the duplication. Expressly request a refund or billing correction within a specific timeframe. Maintaining a professional tone while documenting every communication creates a vital paper trail for your financial records and consumer protection rights.

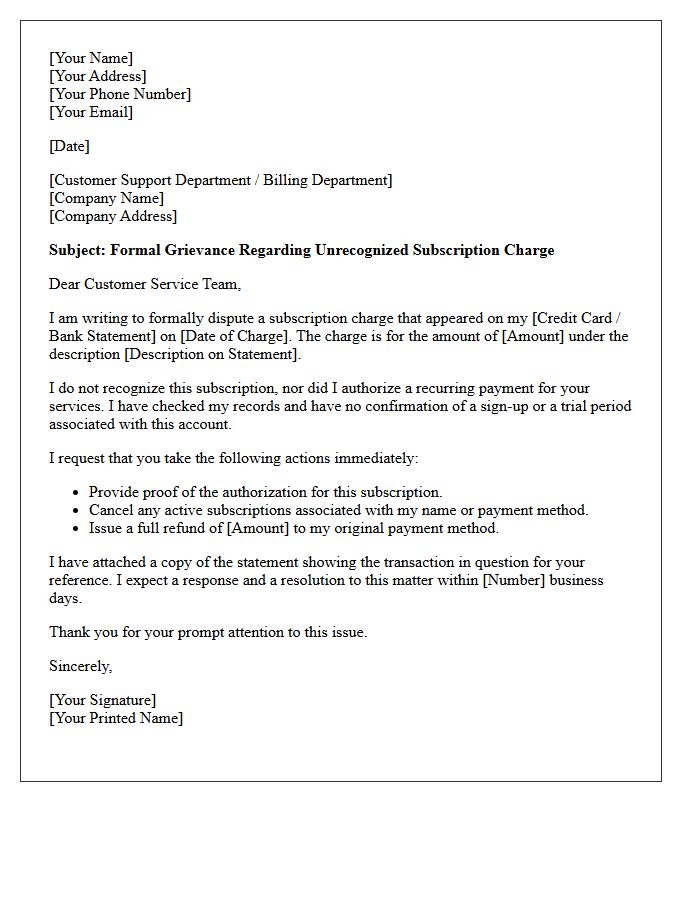

Grievance Letter for Unrecognized Subscription Charge

When drafting a grievance letter for an unrecognized subscription charge, clearly state the transaction date, amount, and merchant name. Explicitly request an immediate refund and the formal cancellation of any active accounts. Attach a bank statement screenshot as evidence and mention your right to a chargeback if the issue remains unresolved. Sending this written notice promptly creates a vital paper trail for your financial institution, ensuring consumer protection laws cover your claim against unauthorized billing and potential recurring fees.

Grievance Letter for Incorrect Transaction Amount

When drafting a grievance letter for an incorrect transaction amount, clarity is essential. Clearly state the exact disputed amount, transaction date, and merchant details. Attach supporting evidence like bank statements or receipts to validate your claim. Explicitly request a formal reversal or correction of the error within a specific timeframe. Using a professional tone helps ensure your complaint is prioritized. This formal record serves as vital documentation if further legal escalation or credit card chargeback procedures become necessary to recover your funds.

Grievance Letter for Missing Refund Credit

When drafting a grievance letter for a missing refund, clearly state your original transaction details, including order numbers and dates. Explicitly mention the expected refund amount and the payment method used. Attach supporting evidence, such as return receipts or previous email correspondence, to validate your claim. Formally request a specific resolution timeframe and mention potential further actions if the issue remains unresolved. Maintaining a professional tone ensures your complaint is handled effectively by customer service departments or financial institutions during the dispute process.

Grievance Letter for Unjustified Late Fee Assessment

When drafting a grievance letter for an unjustified late fee assessment, you must clearly state the disputed charge and provide factual evidence of timely payment. Reference your account details, the specific transaction date, and include copies of receipts or bank statements as proof. Formally request an immediate fee waiver and a corrected account statement. Sending this document via certified mail ensures a paper trail for legal compliance and consumer protection. A professional tone helps expedite the resolution process and protects your credit rating from negative reporting errors.

Grievance Letter for Overcharge on Foreign Exchange Transaction

When drafting a grievance letter for a foreign exchange overcharge, you must clearly identify the specific transaction details, including the date and reference number. Explicitly state the expected exchange rate versus the rate applied to prove the discrepancy. Attach supporting documentation, such as receipts or bank statements, to validate your claim. Formally request a refund of the overcharged amount and a correction of any associated fees. Sending this letter promptly to the financial institution ensures your consumer rights are protected under banking regulations regarding transparent pricing and fair currency conversion.

Grievance Letter for Uncredited Payment Discrepancy

A grievance letter for an uncredited payment serves as formal evidence of a financial discrepancy. When a payment is made but not reflected in your account, you must clearly state the transaction date, amount, and reference number. Attaching a proof of payment, such as a bank receipt or screenshot, is essential for a swift resolution. Clearly define the expected outcome, such as an immediate account update or refund. Maintaining a professional tone ensures your claim is documented legally, protecting your consumer rights while demanding a formal investigation into the missing funds.

Grievance Letter for Cancelled Service Recurring Billing

When drafting a grievance letter for recurring billing after a service cancellation, clearly state your intent to dispute unauthorized charges. Explicitly mention the cancellation date and any prior confirmation numbers received. Demand an immediate refund for payments taken after the contract ended. It is essential to include your account details and attach proof of your cancellation request to ensure consumer protection. This formal written notice serves as vital evidence if you need to escalate the matter to your bank or a regulatory body to resolve the billing error.

Grievance Letter for Fraudulent Charge Dispute

A grievance letter for a fraudulent charge dispute is a formal written statement sent to your bank to contest unauthorized transactions. To protect your consumer rights under the Fair Credit Billing Act, you must submit this notice within 60 days. Clearly list the merchant name, transaction date, and the specific amount being challenged. Use supporting evidence, such as police reports or account statements, to strengthen your case. Explicitly state that you did not authorize the purchase to ensure a thorough fraud investigation and a timely reversal of the charges.

Grievance Letter for Interest Charge Calculation Error

A grievance letter for an interest charge calculation error must clearly state the billing discrepancy identified in your statement. Formally request a manual recalculation of the principal and accrued interest to ensure alignment with your agreed APR. Include specific dates, transaction amounts, and evidence of previous payments to support your claim. Under the Fair Credit Billing Act, submitting this written notice protects your consumer rights and compels the creditor to investigate and correct financial inaccuracies promptly. Always specify a resolution deadline to ensure a timely response and account adjustment.

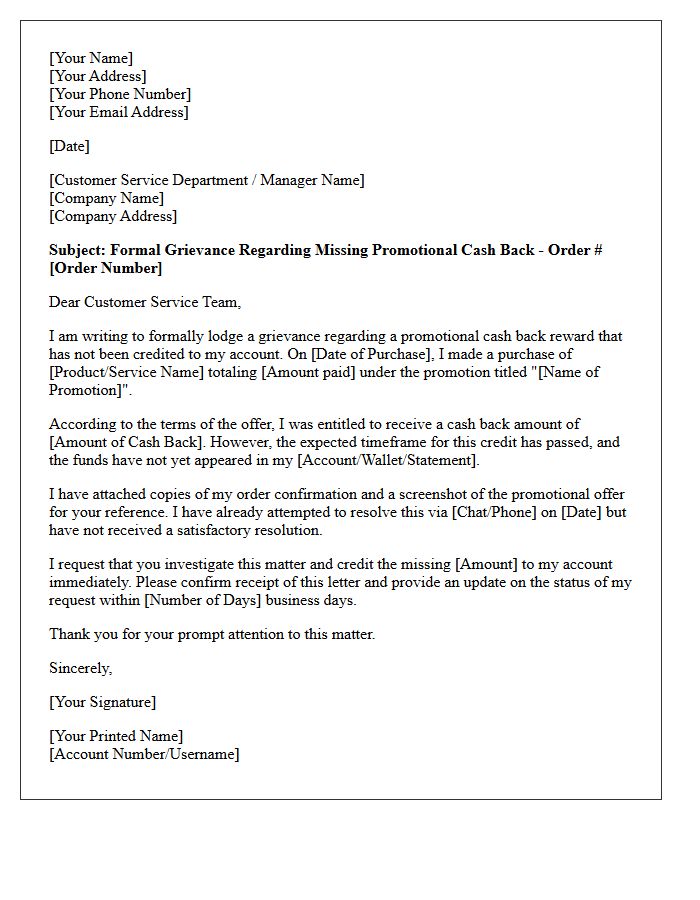

Grievance Letter for Unapplied Promotional Cash Back

A grievance letter for unapplied promotional cash back serves as a formal dispute to claim missing rewards. You must clearly state the offer details, transaction dates, and the specific promotional code used. Attaching evidence like receipts or promotional screenshots strengthens your case. Clearly outline the expected resolution to ensure the company corrects the balance. Maintaining a professional tone while citing the terms and conditions increases the likelihood of a successful credit adjustment to your account.

What should I include in a grievance letter for a credit card billing discrepancy?

Your letter should include your full name, account number, a clear description of the disputed transaction (date, amount, and merchant name), the specific reason for the dispute, and copies of any supporting documentation like receipts or statements.

What is the timeframe for filing a formal credit card billing dispute?

Under the Fair Credit Billing Act (FCBA), you must mail your written grievance letter so that it reaches the creditor within 60 days after the first bill containing the error was mailed to you.

Where should I send my credit card billing grievance letter?

The letter must be sent to the specific address designated for "billing inquiries" or "disputes," which is typically listed on the back of your monthly statement, rather than the address where you send your payments.

Do I have to pay the disputed amount while the investigation is pending?

You are legally permitted to withhold payment for the specific disputed amount and related finance charges while the issuer investigates; however, you must continue to pay the undisputed portion of your credit card balance to avoid late fees.

How long does the bank have to respond to my billing discrepancy letter?

The creditor must acknowledge receipt of your written grievance within 30 days and must resolve the dispute within two complete billing cycles (but no later than 90 days) after receiving your letter.

Comments