Persistent delays in closing a bank or service account can lead to unwanted fees and security risks. If your formal requests have been ignored, a professional Grievance Letter for Delayed Account Closure is necessary to escalate the issue and demand immediate action. This guide explains how to protect your rights and finalize the process. Below are some ready to use templates.

Image cover: Formal Grievance Letter Templates for Delayed Bank Account Closure

Letter Samples List

- Grievance Letter for Delayed Savings Account Closure

- Formal Complaint Letter Regarding Incomplete Bank Account Closure

- Escalation Letter for Pending Account Closure Request

- Follow-Up Grievance Letter on Unresolved Account Closure

- Notice Letter Demanding Immediate Bank Account Termination

- Grievance Letter Addressing Unauthorized Fees After Closure Request

- Final Warning Letter Prior to Banking Ombudsman Escalation

- Grievance Letter Concerning Ignored Account Closure Application

- Dispute Letter for Unlawful Charges During Account Closure Delay

- Official Grievance Letter to Branch Manager for Delayed Closure

- Appeal Letter for Waiving Penalties Due to Delayed Account Closure

- Legal Notice Letter Regarding Delayed Business Account Closure

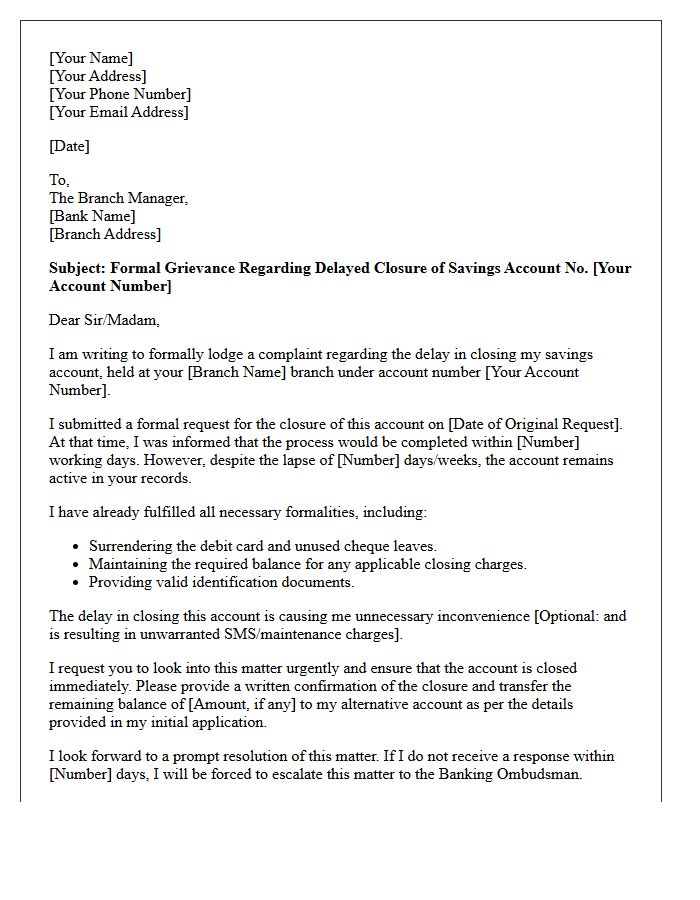

Grievance Letter for Delayed Savings Account Closure

A formal grievance letter is essential when a bank fails to close your savings account within the regulated timeframe. Clearly state your account details and the date of your initial request. Emphasize that the delay causes financial inconvenience and potential unauthorized charges. Demand an immediate resolution and a written confirmation of closure. If the bank remains unresponsive, this document serves as vital evidence for escalating your complaint to the Banking Ombudsman or relevant regulatory authority to protect your consumer rights.

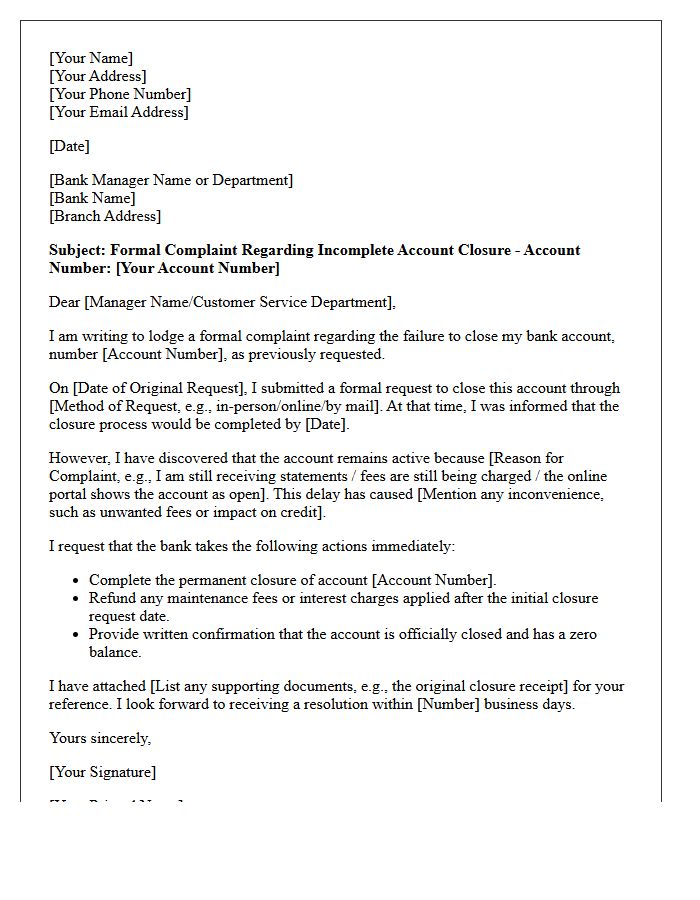

Formal Complaint Letter Regarding Incomplete Bank Account Closure

When drafting a formal complaint letter for an incomplete bank account closure, you must clearly state your account details and the date of your original request. Highlight the specific failure, such as unauthorized fees or an active balance, that proves the account remains open. Request an immediate resolution and a written confirmation of the closure. Mentioning your intent to escalate the issue to a financial ombudsman or regulatory body often encourages the bank to resolve the administrative error promptly and protect your credit score.

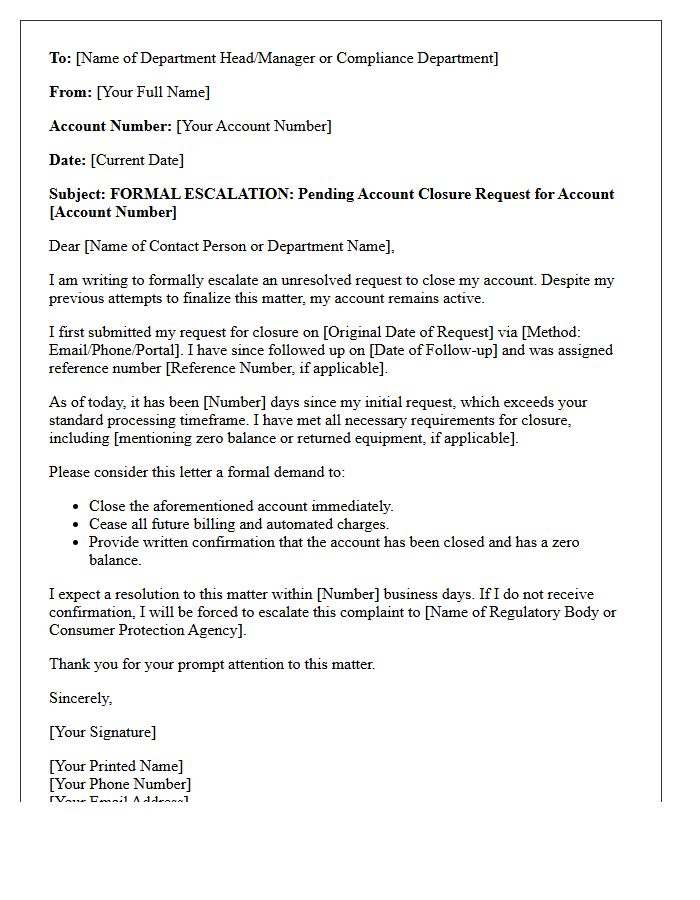

Escalation Letter for Pending Account Closure Request

An Escalation Letter is a formal document sent to senior management when a Pending Account Closure Request remains unresolved despite previous attempts. It effectively highlights service failures, specifies the original case reference number, and demands immediate action to finalize the termination. Clearly stating the legal and financial implications of continued delays helps prioritize your request. Use a professional tone to ensure the institution understands your commitment to closing the account, preventing further unauthorized fees or data retention issues while creating a formal paper trail for regulatory compliance.

Follow-Up Grievance Letter on Unresolved Account Closure

When sending a Follow-Up Grievance Letter, you must reference your initial complaint reference number and the date it was filed. Clearly state that the account closure remains unresolved and emphasize the financial impact or lack of communication received. Demand a final response or a deadlock letter to escalate the matter to an ombudsman or regulatory body. Maintain a professional tone, provide any new supporting evidence, and set a specific deadline for a resolution to ensure your consumer rights are protected during this formal dispute process.

Notice Letter Demanding Immediate Bank Account Termination

A notice demanding immediate bank account termination is a formal legal directive, often triggered by suspicious activity, regulatory non-compliance, or a breach of terms. Receiving this letter means your financial access will be revoked, freezing your ability to process transactions or withdrawals. It is imperative to review the specific closure date and instructions for transferring remaining balances. Failure to respond or rectify underlying issues can lead to permanent blacklisting or negative reporting to agencies. Always seek immediate legal or financial counsel to protect your liquidity and maintain banking continuity.

Grievance Letter Addressing Unauthorized Fees After Closure Request

When sending a grievance letter regarding unauthorized fees charged after a closure request, focus on documentary evidence. Clearly state the date of your original termination notice and demand an immediate refund of all erroneous debits. Explicitly mention that any further collection attempts violate consumer protection standards. This formal record serves as critical proof if you need to escalate the dispute to a financial ombudsman or regulatory body. Always request a written confirmation that the account is fully closed and the balance is zero to ensure future financial protection.

Final Warning Letter Prior to Banking Ombudsman Escalation

A final warning letter is a critical formal notice sent to a financial institution before escalating a dispute. It serves as the Final Response, clearly stating that their previous resolution was unsatisfactory. To ensure legal weight, explicitly mention your intent to refer the case to the Banking Ombudsman if a settlement is not reached within a specific timeframe. This document is essential for the Ombudsman process, proving you have exhausted the bank's internal grievance redressal mechanisms before seeking independent mediation or legal intervention.

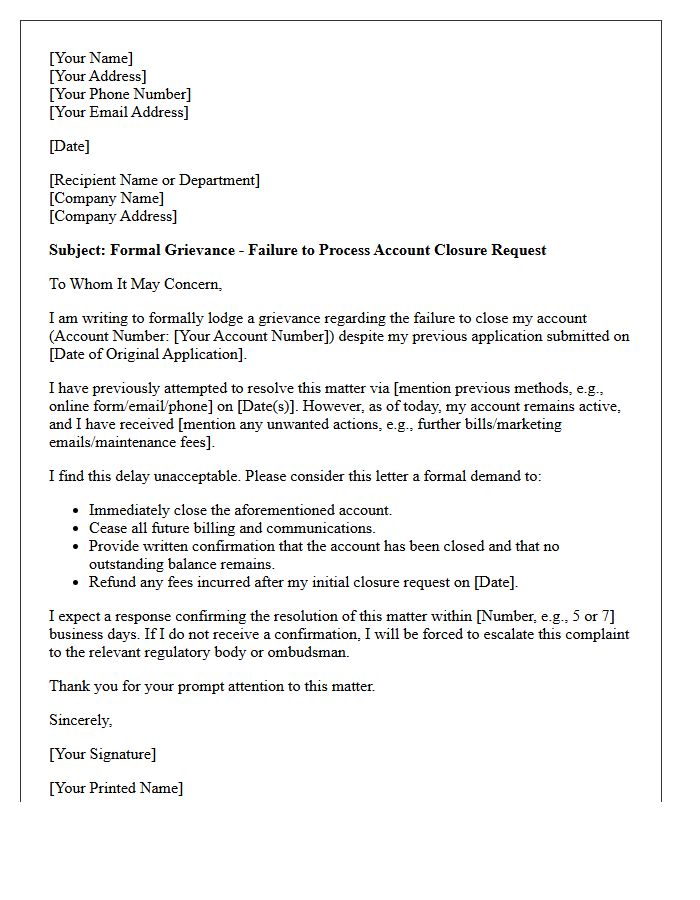

Grievance Letter Concerning Ignored Account Closure Application

If a bank or service provider fails to process your termination request, a formal grievance letter is essential. This document serves as legal evidence that you attempted to end the contract. Clearly state your original request date and demand an immediate account closure to prevent further unauthorized charges. Mention that ignored applications violate consumer rights and express your intent to escalate the matter to an ombudsman if unresolved. Always include your account details and attach previous correspondence to ensure a swift resolution and protect your financial standing.

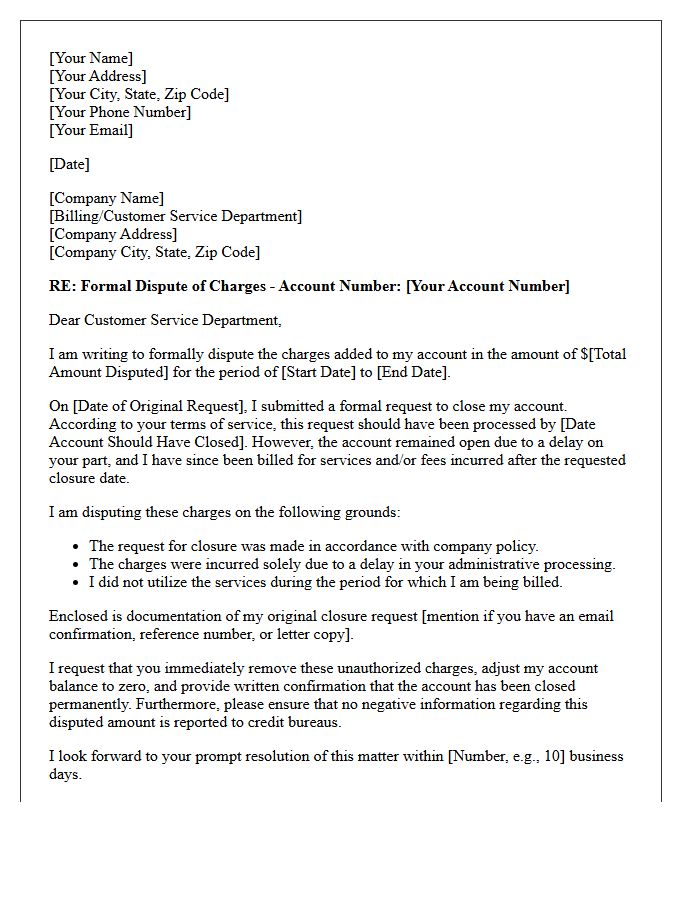

Dispute Letter for Unlawful Charges During Account Closure Delay

When a financial institution delays closing your account, resulting in unlawful charges or maintenance fees, you must submit a formal dispute letter immediately. This document serves as legal proof that you requested closure and provides a clear timeline of events. Explicitly state that any fees accrued after your initial request are unauthorized under banking regulations. Demand a full refund of these predatory charges and confirmation of a zero balance. Sending this via certified mail ensures a paper trail, protecting your credit score from potential negative reporting caused by institutional negligence.

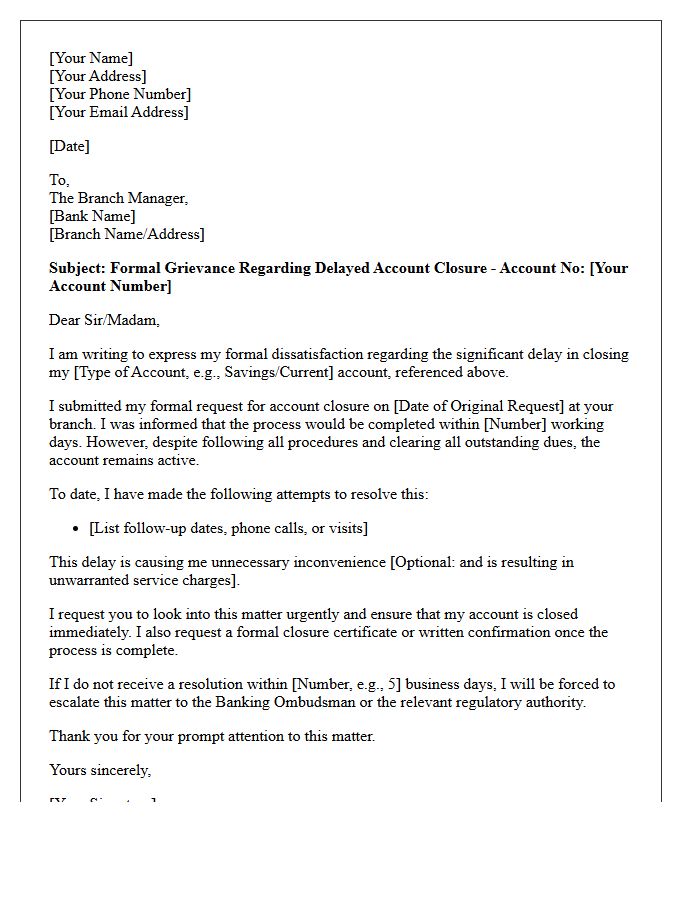

Official Grievance Letter to Branch Manager for Delayed Closure

When drafting an Official Grievance Letter to Branch Manager, clearly state your account details and the specific duration of the unresolved delay. Formally request an immediate account closure and demand a written explanation for the non-compliance with standard banking timelines. Mentioning potential escalation to the Banking Ombudsman often accelerates the process. Ensure you attach copies of previous requests as evidence to strengthen your claim and ensure regulatory compliance. A professional tone is essential for a formal resolution of your complaint regarding delayed services.

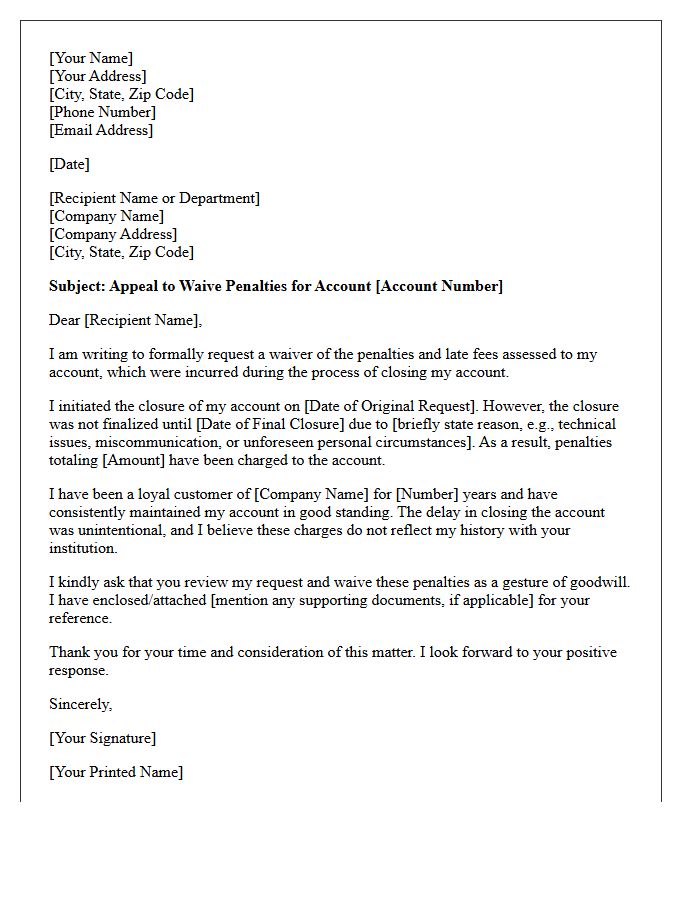

Appeal Letter for Waiving Penalties Due to Delayed Account Closure

When drafting an appeal letter for waiving penalties, focus on demonstrating reasonable cause for the delayed account closure. Clearly state the account details, the specific penalties incurred, and the extenuating circumstances, such as medical emergencies or administrative errors. Providing supporting documentation strengthens your case significantly. Emphasize your history of compliance and request a one-time courtesy waiver. A professional, concise tone helps expedite the review process and increases the likelihood of a favorable resolution from the financial institution or authority.

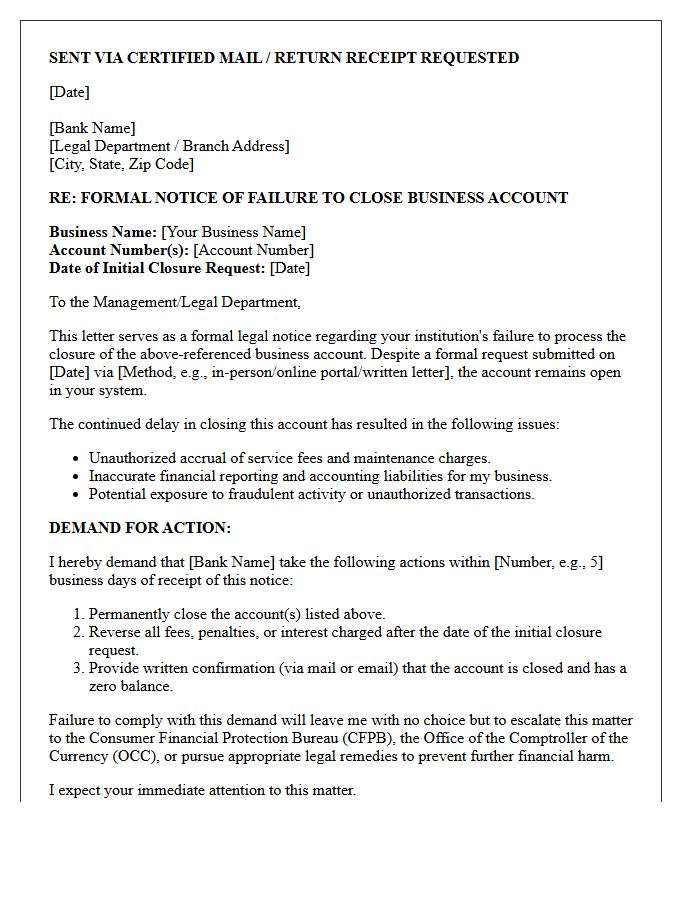

Legal Notice Letter Regarding Delayed Business Account Closure

A legal notice letter for a delayed business account closure serves as formal documentation of your request to terminate banking services. It is essential to include your account number, the initial closure date, and a clear demand for the immediate release of remaining funds. This letter protects your business by establishing a paper trail, mitigating potential unauthorized fees, and setting a firm deadline for compliance. Explicitly stating your intent to pursue legal action or regulatory complaints often accelerates the resolution of administrative bottlenecks or bank negligence.

What should be included in a grievance letter for a delayed account closure?

A formal grievance letter should include your full name, account number, the date of the original closure request, a summary of previous follow-ups, and a demand for immediate closure along with a final balance confirmation.

How long does a bank or institution legally have to close an account?

While timelines vary by jurisdiction and institution, most banks are expected to process a closure request within 3 to 7 business days. If the delay exceeds 30 days without valid justification, it is typically grounds for a formal complaint.

Can I claim compensation for a delay in closing my account?

Yes, if the delay resulted in financial loss, such as additional maintenance fees, interest charges, or negative impacts on your credit score, you can request a refund of those fees and monetary compensation in your grievance letter.

What is the next step if my grievance letter about account closure is ignored?

If the institution fails to resolve the issue within the timeframe specified in their complaints policy (usually 8 weeks), you should escalate the matter to the Financial Ombudsman Service or a relevant regulatory authority.

Should I continue paying fees while my account closure is being disputed?

To protect your credit rating, it is often advised to pay disputed fees "under protest" while explicitly stating in your grievance letter that you expect a full refund once the delayed closure is rectified.

Comments