If your lender has failed to return surplus funds after a loan payoff or analysis, you must take formal action. A Grievance Letter for Delayed Mortgage Escrow Refund serves as an official notice to resolve withholding issues and ensure compliance with federal regulations. Protect your financial rights and demand your money back promptly. Below are some ready to use templates.

Image cover: Claim Your Late Mortgage Escrow Refund: Letter Samples and Professional Templates

Letter Samples List

- Initial Grievance Letter for Delayed Mortgage Escrow Refund

- Follow-Up Grievance Letter for Delayed Mortgage Escrow Refund

- Second Request Grievance Letter for Delayed Mortgage Escrow Refund

- Final Demand Grievance Letter for Delayed Mortgage Escrow Refund

- Notice of Error Letter for Delayed Mortgage Escrow Refund

- Executive Escalation Grievance Letter for Delayed Mortgage Escrow Refund

- Regulatory Complaint Letter for Delayed Mortgage Escrow Refund

- Post-Payoff Grievance Letter for Delayed Mortgage Escrow Refund

- Refinance Disbursement Grievance Letter for Delayed Mortgage Escrow Refund

- Legal Action Threat Letter for Delayed Mortgage Escrow Refund

- Ombudsman Escalation Grievance Letter for Delayed Mortgage Escrow Refund

- Account Closure Grievance Letter for Delayed Mortgage Escrow Refund

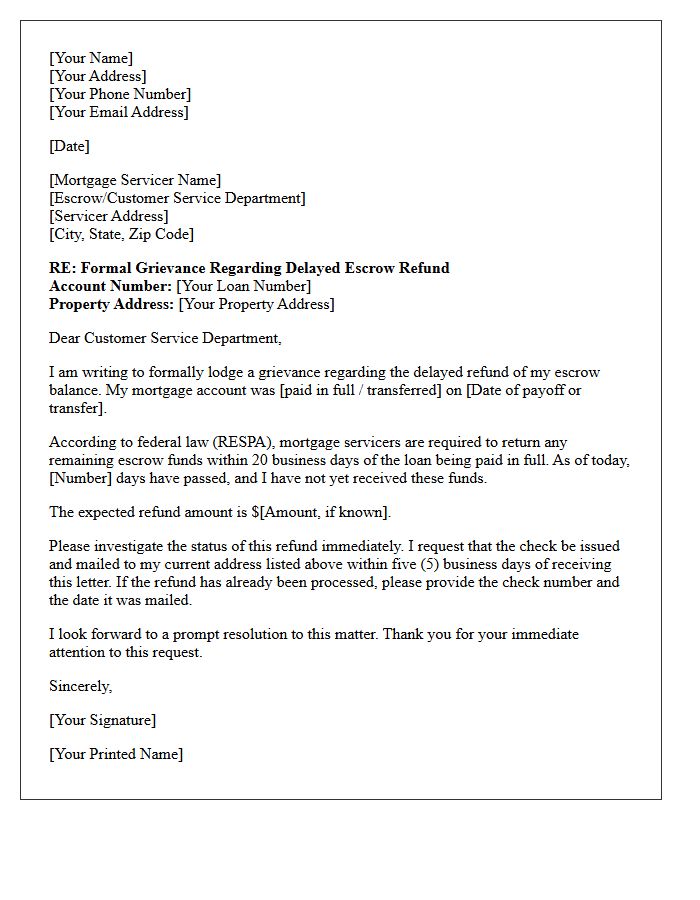

Initial Grievance Letter for Delayed Mortgage Escrow Refund

When drafting an Initial Grievance Letter for a delayed mortgage escrow refund, you must clearly state that your loan is paid in full. Federal law under RESPA requires servicers to return excess escrow funds within 20 days of account payoff. Explicitly include your loan number, the payoff date, and the exact refund amount expected. Send this formal notice via certified mail to create a legal paper trail. Formally requesting this refund ensures your consumer rights are protected against administrative processing delays by the mortgage servicer.

Follow-Up Grievance Letter for Delayed Mortgage Escrow Refund

When your mortgage escrow refund remains unpaid beyond the legal thirty-day window, a follow-up grievance letter is essential. This formal notice should clearly state your original request date and include your account number to expedite processing. Explicitly mention RESPA violations to signal your awareness of federal consumer protection laws. Request an immediate status update and a specific disbursement timeline. Sending this correspondence via certified mail creates a vital paper trail for potential legal escalation or CFPB complaints, ensuring the lender prioritizes your outstanding balance and interest penalties.

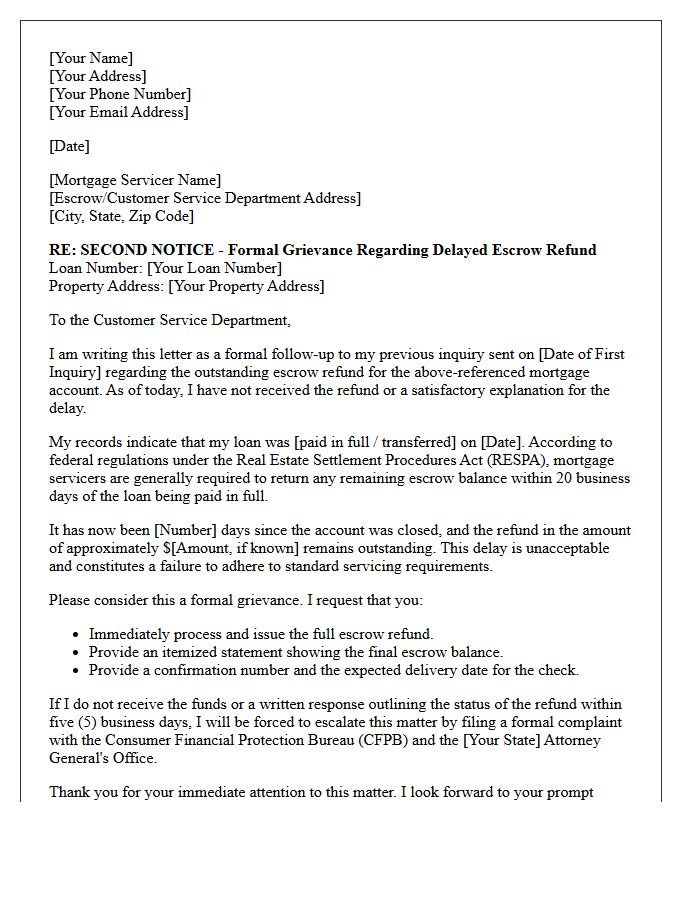

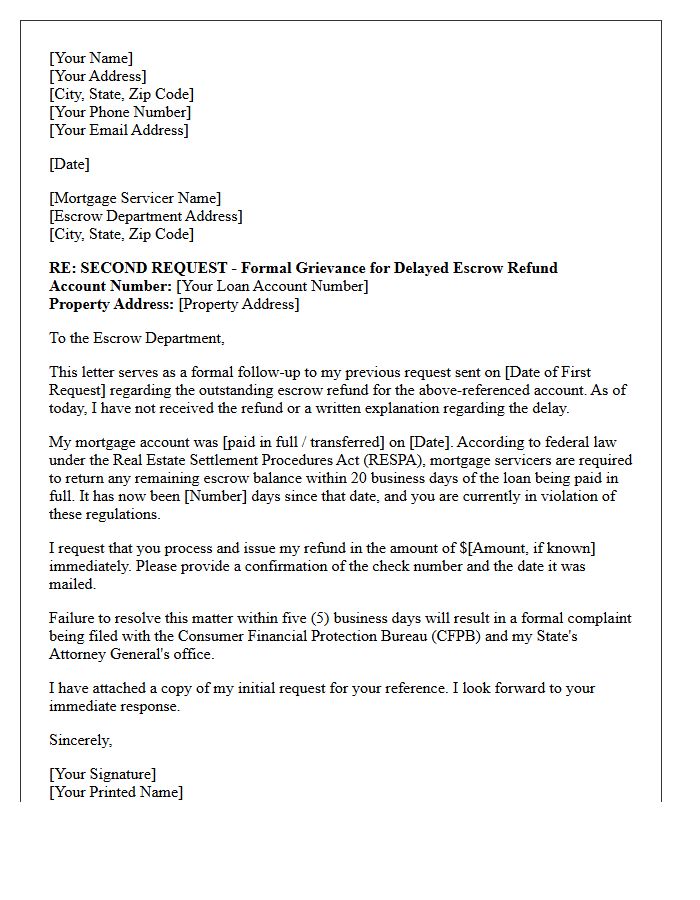

Second Request Grievance Letter for Delayed Mortgage Escrow Refund

When sending a Second Request Grievance Letter for a delayed mortgage escrow refund, you must cite RESPA guidelines. Federal law typically requires lenders to return surplus funds within 30 days of account payoff. Clearly state that your initial inquiry was ignored and include your loan number for tracking. Demand an immediate escrow reimbursement and threaten to escalate the dispute to the Consumer Financial Protection Bureau (CFPB) if the check is not issued. Sending this via certified mail ensures documented proof of your formal follow-up regarding the outstanding balance.

Final Demand Grievance Letter for Delayed Mortgage Escrow Refund

A Final Demand Grievance Letter is a formal legal notice issued when a lender fails to return surplus funds after a loan payoff. You must clearly cite the Real Estate Settlement Procedures Act (RESPA), which mandates refunds within 20 business days of account closure. Explicitly state the outstanding balance, the original deadline missed, and your intent to escalate the dispute to the Consumer Financial Protection Bureau (CFPB). This document serves as critical evidence of your attempt to resolve the mortgage escrow refund delay before pursuing legal action or regulatory intervention.

Notice of Error Letter for Delayed Mortgage Escrow Refund

A Notice of Error is a formal legal tool used to resolve a delayed mortgage escrow refund. Under federal law, servicers must return surplus funds within twenty days of account payoff. If your refund is overdue, sending this written notice forces the lender to investigate and respond within specific timelines. Clearly state that the escrow surplus has not been received to trigger consumer protections under Regulation X. This document creates a vital paper trail, ensuring the servicer rectifies the accounting mistake and issues your reimbursement promptly to satisfy legal requirements.

Executive Escalation Grievance Letter for Delayed Mortgage Escrow Refund

An Executive Escalation Grievance Letter is a formal demand sent to a lender's senior leadership to resolve a delayed mortgage escrow refund. After a loan payoff or sale, federal law under RESPA requires lenders to return surplus funds within 20 business days. If standard customer service fails, this letter serves as a critical legal notice to trigger internal compliance reviews. Clearly state the account details, the specific overage amount, and the duration of the delay to ensure immediate restitution and avoid further financial disputes or regulatory complaints.

Regulatory Complaint Letter for Delayed Mortgage Escrow Refund

When drafting a regulatory complaint letter for a delayed mortgage escrow refund, you must cite specific RESPA guidelines. Federal law typically requires servicers to return surplus funds within 20 days of account payoff. Clearly state your loan details, the exact refund amount owed, and the duration of the delay. Directing your formal grievance to the Consumer Financial Protection Bureau (CFPB) or state regulators creates an official paper trail, often compelling lenders to expedite the payment to avoid statutory penalties and legal scrutiny.

Post-Payoff Grievance Letter for Delayed Mortgage Escrow Refund

A post-payoff grievance letter is a formal notice sent to a mortgage servicer demanding a delayed escrow refund. Federal law under RESPA requires lenders to return remaining escrow funds within 20 days of account payoff. If your servicer exceeds this timeline, this document serves as a qualified written request (QWR) to resolve the delinquency. Clearly state your loan number, payoff date, and demand immediate reimbursement. Sending this letter via certified mail creates a legal paper trail, ensuring the lender complies with Consumer Financial Protection Bureau regulations and avoids further withholding of your money.

Refinance Disbursement Grievance Letter for Delayed Mortgage Escrow Refund

A Refinance Disbursement Grievance Letter is a formal complaint sent to a lender when a mortgage escrow refund is delayed beyond the legal timeframe. Under RESPA guidelines, lenders must typically return surplus funds within twenty days of loan payoff. This document serves as a "Notice of Error," requiring the servicer to investigate and respond. Clearly state your account details, the payoff date, and demand the immediate release of your escrow balance to resolve the financial delinquency and avoid further escalation or regulatory reporting.

Legal Action Threat Letter for Delayed Mortgage Escrow Refund

A legal action threat letter is a formal notice sent to a mortgage servicer demanding an immediate escrow refund. Federal law, specifically RESPA, requires lenders to return surplus funds within 20 days of account payoff. If your refund is delayed, this document serves as a final warning before pursuing litigation or filing complaints with the CFPB. It must clearly outline the outstanding balance, the statutory deadline exceeded, and your intent to seek damages and legal fees if the servicer fails to comply promptly.

Ombudsman Escalation Grievance Letter for Delayed Mortgage Escrow Refund

When drafting an Ombudsman Escalation Grievance Letter for a delayed mortgage escrow refund, you must clearly outline the unresolved dispute after exhausting the lender's internal complaints process. Explicitly state the refund amount, the duration of the delay, and provide a detailed chronology of previous communication. Mentioning specific violations of RESPA guidelines (Real Estate Settlement Procedures Act) strengthens your case. This formal escalation serves as a final legal notice to compel the financial institution to release your surplus funds and rectify administrative negligence under regulatory oversight.

Account Closure Grievance Letter for Delayed Mortgage Escrow Refund

If your lender fails to return surplus funds after a loan payoff, an Account Closure Grievance Letter is essential to demand your mortgage escrow refund. Federal law under RESPA requires services to issue these checks within 20 business days of account closure. Formally documenting the delay creates a legal paper trail for consumer protection agencies. Ensure your letter includes the final payoff date, specific escrow balance, and a clear deadline for reimbursement to resolve the financial discrepancy and avoid further administrative delays or potential interest loss.

How do I write a grievance letter for a delayed mortgage escrow refund?

To write an effective grievance letter, include your loan account number, the date your mortgage was paid off or closed, and the exact amount of the expected escrow refund. Clearly state that the federal 20-day refund deadline has passed and request immediate disbursement of the funds to avoid further escalation.

What is the legal time limit for a mortgage lender to refund escrow funds?

Under the Real Estate Settlement Procedures Act (RESPA), mortgage servicers are legally required to return any remaining funds in an escrow account within 20 business days of the loan being paid in full. If this window has passed, you have the right to file a formal written grievance with the lender's compliance department.

Where should I send a formal complaint about a late escrow refund?

You should send your grievance letter to the "Qualified Written Request" (QWR) or "Notice of Error" address specified on your monthly mortgage statement. Sending the letter via certified mail with a return receipt is recommended to ensure you have proof of delivery for regulatory bodies like the CFPB.

Can I claim interest on a delayed mortgage escrow refund?

While federal law (RESPA) does not mandate interest payments on delayed refunds, some state laws require lenders to pay interest on escrow accounts. In your grievance letter, you should demand the immediate release of principal and check your specific state statutes to see if you are entitled to additional interest penalties for the delay.

What should I do if a lender ignores my escrow refund grievance letter?

If the lender does not resolve the issue after receiving your grievance letter, you should file a formal complaint with the Consumer Financial Protection Bureau (CFPB) and your state's Attorney General. Provide these agencies with a copy of your letter and the certified mail receipt as evidence of your attempt to resolve the dispute directly.

Comments