Facing unexpected bank charges can be frustrating and financially draining. If your bank has unfairly charged you, submitting a formal Grievance Letter for Unjustified Overdraft Fee Deduction is the most effective way to demand a refund and protect your consumer rights. Clear documentation and professional communication are essential for a successful resolution. To help you get started, below are some ready to use template.

Image cover: Effective Samples for Challenging Unfair Overdraft Fee Deductions

Letter Samples List

- Grievance Letter for Unjustified Overdraft Fee Deduction

- Letter of Grievance Regarding Erroneous Overdraft Charges

- Formal Dispute Letter for Unauthorized Overdraft Fee Deduction

- Customer Grievance Letter for Unwarranted Account Overdraft Penalties

- Letter of Complaint for Incorrect Overdraft Fee Assessment

- Appeal Letter for Reversal of Unjustified Overdraft Deduction

- Grievance Letter Concerning System Error Overdraft Deduction

- Letter Requesting Refund for Unfair Overdraft Fee Deduction

- Bank Grievance Letter for Disputed Overdraft Charges

- Letter of Escalation for Unresolved Overdraft Fee Deduction

- Client Grievance Letter for Unnotified Overdraft Penalty Deduction

- Letter of Dispute for Inaccurate Overdraft Deduction

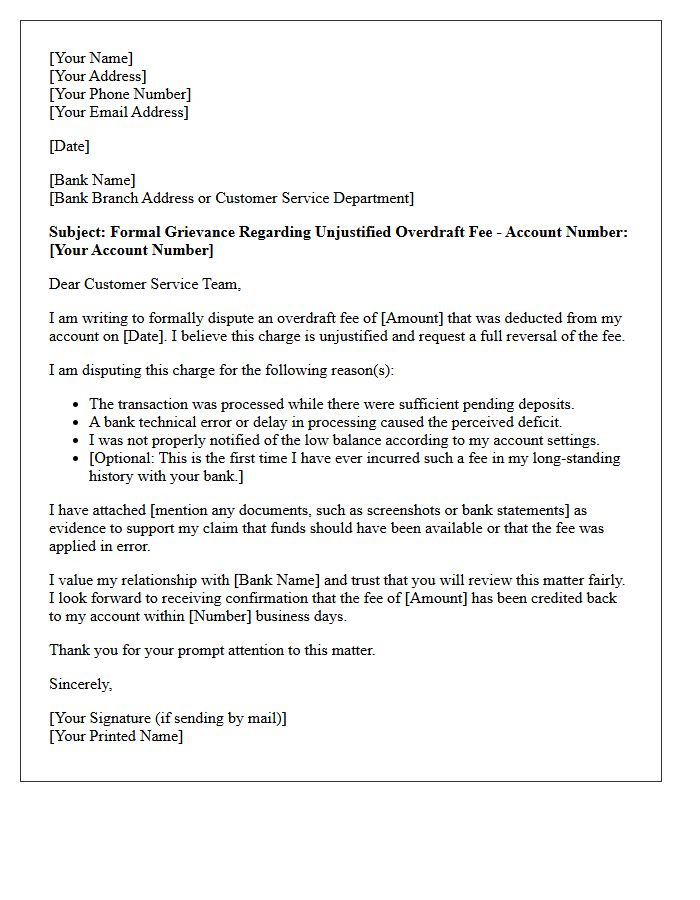

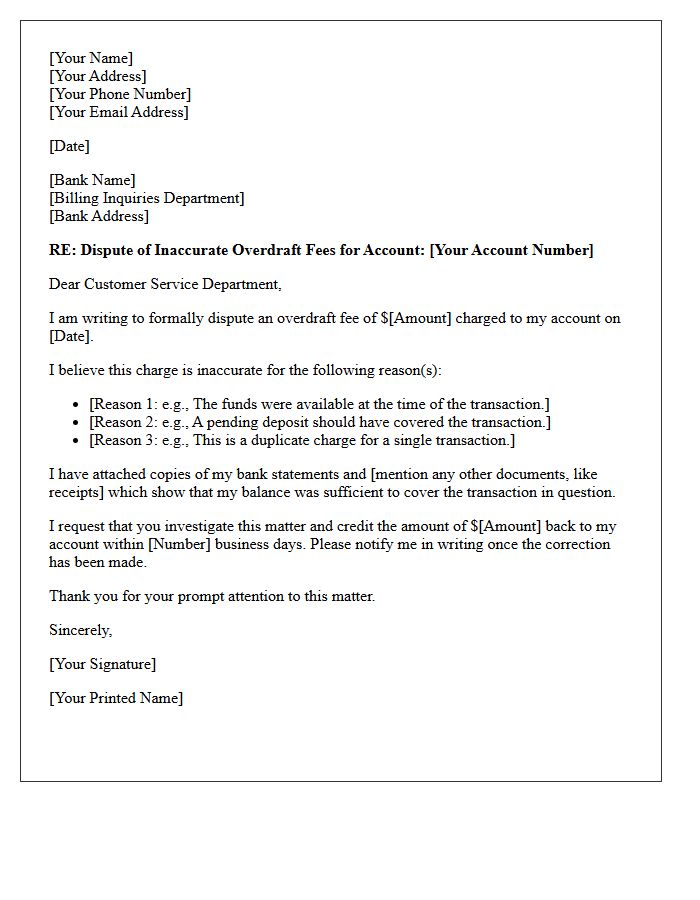

Grievance Letter for Unjustified Overdraft Fee Deduction

When drafting a grievance letter for an unjustified overdraft fee, focus on clear evidence. State the specific transaction date and amount, then explain why the charge is erroneous, such as a bank processing delay or a merchant error. Formally request a full refund while citing your history as a loyal customer. Using professional language increases your chances of a successful fee reversal. Ensure you include your account details and a clear deadline for a response to resolve the financial dispute efficiently.

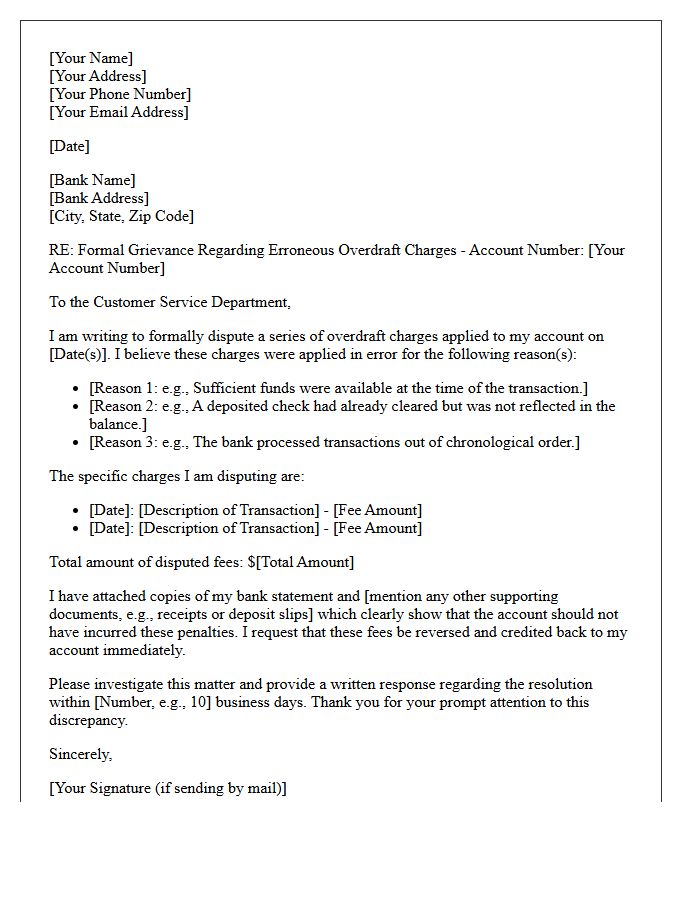

Letter of Grievance Regarding Erroneous Overdraft Charges

A Letter of Grievance is a formal document used to dispute erroneous overdraft charges with your financial institution. It is essential to clearly state the specific transaction dates, amounts, and the reason the fees are unjustified, such as bank processing errors or missing deposits. Submitting this written complaint creates a necessary paper trail for consumer protection rights. Timely communication is critical to ensure a refund and to protect your account's standing. Always request a formal response and keep copies of all correspondence to resolve the billing dispute effectively.

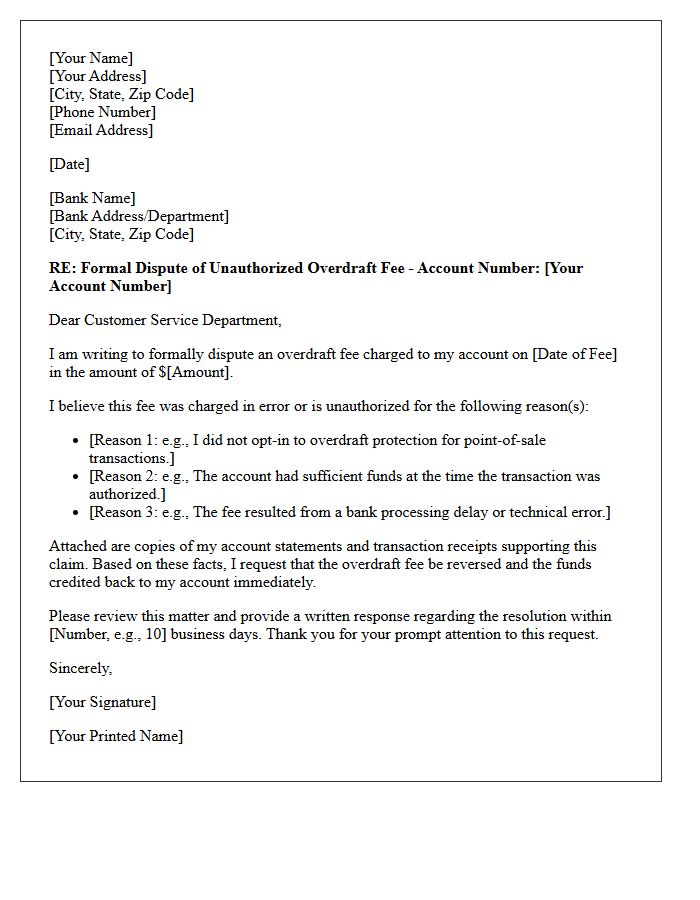

Formal Dispute Letter for Unauthorized Overdraft Fee Deduction

A formal dispute letter is essential for reclaiming an unauthorized overdraft fee. Clearly state your account details, the specific transaction date, and the exact amount deducted. Explicitly mention that you did not authorize the charge or that it violates the bank's terms of service. Request a full reversal and a formal written response within a set timeframe. Sending this document via certified mail provides a legal paper trail, ensuring your consumer rights are protected under banking regulations while forcing the institution to investigate the billing error officially.

Customer Grievance Letter for Unwarranted Account Overdraft Penalties

When drafting a customer grievance letter for unwarranted account overdraft penalties, you must clearly state the specific transaction dates and disputed amounts. Emphasize that the charges resulted from bank errors or systemic delays rather than insufficient funds. Formally request a full refund and a corrected statement to protect your credit standing. Providing supporting evidence, such as dated receipts or balance snapshots, strengthens your claim. Use professional language to demand an immediate internal review, ensuring the reversal of all unfair fees to restore your financial balance promptly.

Letter of Complaint for Incorrect Overdraft Fee Assessment

When drafting a letter of complaint for an incorrect overdraft fee assessment, you must clearly state the specific transaction date and the exact amount charged. Explicitly reference your account statement as evidence that your balance was sufficient to cover the payment. Request an immediate reversal of the fee and any associated interest charges. Asserting your consumer rights under banking regulations ensures the financial institution addresses the error promptly. Professional communication helps maintain a positive banking relationship while protecting your financial interests from unauthorized penalties and systemic banking errors.

Appeal Letter for Reversal of Unjustified Overdraft Deduction

When drafting an Appeal Letter for Reversal of Unjustified Overdraft Deduction, clearly state your account details and the specific transaction date. Formally request a refund by explaining why the fee was erroneous, such as a bank processing delay or a proven technical error. Attach supporting documentation like bank statements or deposit receipts to substantiate your claim. Emphasize your history as a loyal customer to encourage a goodwill adjustment. Sending this formal written request promptly ensures a documented paper trail, significantly increasing your chances of recovering the unfairly deducted funds efficiently.

Grievance Letter Concerning System Error Overdraft Deduction

When drafting a grievance letter regarding a system error overdraft deduction, it is vital to provide clear evidence of the technical glitch. Clearly state the specific transaction date, the exact amount deducted, and why the charge was unjustified. Request an immediate reversal of fees and a correction of your account balance. Emphasize that the error originated from the bank's internal processing rather than a lack of funds. Formally documenting this dispute protects your consumer rights and ensures a paper trail for potential escalations if the institution fails to rectify the mistake promptly.

Letter Requesting Refund for Unfair Overdraft Fee Deduction

When drafting a letter to your bank, clearly state that you are requesting a refund for an unfair overdraft fee. Briefly explain why the charge was unjust, such as a technical error or lack of prior notification. Include your account details and the specific transaction date to ensure quick processing. Emphasize your history as a loyal customer to encourage a courtesy reversal of the penalty. Professional communication is key to successfully disputing these costs and protecting your financial balance from unnecessary deductions.

Bank Grievance Letter for Disputed Overdraft Charges

When drafting a Bank Grievance Letter, clearly identify specific disputed overdraft charges by date and amount. Briefly explain the extenuating circumstances or technical errors that caused the deficit. Formally request a full refund or reversal of fees based on your account history or consumer rights. Attach supporting documentation, such as bank statements or receipts, to substantiate your claim. Send the correspondence via certified mail to ensure a tracking record, as this establishes a formal paper trail necessary for potential escalation to a financial ombudsman or regulatory body.

Letter of Escalation for Unresolved Overdraft Fee Deduction

A Letter of Escalation is a formal document sent to senior bank management when standard customer service fails to resolve an unresolved overdraft fee. This correspondence should clearly outline the history of the dispute, include account evidence, and cite specific reasons why the charges are unjust or erroneous. It serves as a final administrative attempt to reclaim funds before seeking external intervention from regulatory bodies like the Consumer Financial Protection Bureau. Clearly stating your demanded resolution and intent to escalate further often incentivizes banks to reverse predatory or accidental fees quickly.

Client Grievance Letter for Unnotified Overdraft Penalty Deduction

A formal grievance letter is essential when a bank fails to provide prior notification before deducting overdraft penalties. Clearly state that the unauthorized charge violates consumer protection standards and your account agreement. Demand an immediate refund of the fees, citing the lack of transparency and communication. Explicitly mention the specific transaction dates and amounts to ensure accuracy. Sending this written complaint creates a necessary paper trail for potential regulatory escalation if the financial institution refuses to rectify the error promptly and fairly.

Letter of Dispute for Inaccurate Overdraft Deduction

A Letter of Dispute is a formal legal tool used to challenge an inaccurate overdraft deduction with your bank. To protect your rights under the Electronic Fund Transfer Act, you must submit this written notice within 60 days of the statement date. Clearly document the specific transaction error and request an immediate investigation. Using certified mail ensures proof of delivery, forcing the financial institution to rectify the mistake or provide a valid explanation. Prompt action is essential to recover missing funds and maintain a healthy banking history.

What should I include in a grievance letter for an unjustified overdraft fee?

Your letter should include your full name, account number, the specific date and amount of the fee, a clear explanation of why the charge is unjustified (such as a bank error or delayed deposit), and a formal request for a full refund.

How do I prove an overdraft fee was charged in error?

To prove the fee was unjustified, attach supporting documentation such as bank statements showing available funds at the time of the transaction, proof of deposit receipts, or screenshots of technical glitches that prevented timely transfers.

What is the legal timeframe for a bank to respond to a fee dispute?

Under the Electronic Fund Transfer Act (Regulation E), banks generally have 10 to 45 business days to investigate a disputed transaction, though many institutions resolve internal grievance letters regarding overdraft fees within 5 to 7 business days.

Can I request a refund for an overdraft fee if it was my first mistake?

Yes, many banks offer a "one-time courtesy waiver" for long-standing customers. In your grievance letter, emphasize your history of responsible account management and request that the fee be waived as a gesture of goodwill.

What are the most common reasons for an unjustified overdraft fee?

Common reasons include the bank processing debits before credits (reordering transactions), delays in posting verified deposits, merchant processing errors, or fees triggered by "extended coverage" services that the account holder never opted into.

Comments