Addressing transaction discrepancies requires a formal Automated Teller Machine Error Inquiry Response Letter to ensure regulatory compliance and customer satisfaction. This document acknowledges the reported issue, outlines the bank's investigation process, and provides a clear resolution regarding the disputed funds. Use a structured approach to communicate results professionally and maintain trust. To simplify your workflow, below are some ready to use templates.

Image cover: Official ATM Transaction Dispute and Error Investigation Response Templates

Letter Samples List

- Acknowledgment of Automated Teller Machine Error Inquiry Letter

- Automated Teller Machine Dispense Error Refund Letter

- Automated Teller Machine Error Claim Denial Letter

- Additional Information Request for Automated Teller Machine Dispute Letter

- Automated Teller Machine Cash Deposit Discrepancy Adjustment Letter

- Retained Card at Automated Teller Machine Incident Response Letter

- Automated Teller Machine Check Deposit Error Investigation Letter

- Automated Teller Machine Error Investigation Time Extension Letter

- Provisional Credit for Automated Teller Machine Error Letter

- Final Resolution for Automated Teller Machine Error Inquiry Letter

- Network Timeout During Automated Teller Machine Transaction Response Letter

- Provisional Credit Reversal for Automated Teller Machine Dispute Letter

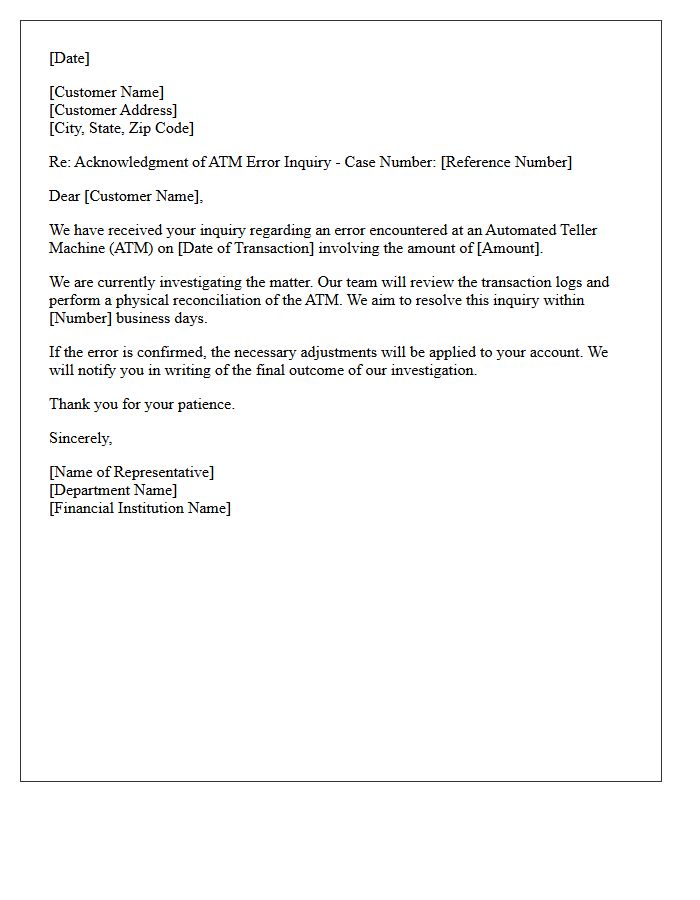

Acknowledgment of Automated Teller Machine Error Inquiry Letter

An Acknowledgment of Automated Teller Machine Error Inquiry Letter is a formal document issued by a bank to confirm receipt of a customer's reported transaction discrepancy. This notice provides legal protection under the Electronic Fund Transfer Act by establishing a timeline for the investigation. It serves as proof that your claim is being processed and typically outlines your rights regarding provisional credit while the bank verifies the ATM malfunction or unauthorized withdrawal. Always retain this correspondence as a reference for tracking the resolution of your disputed funds.

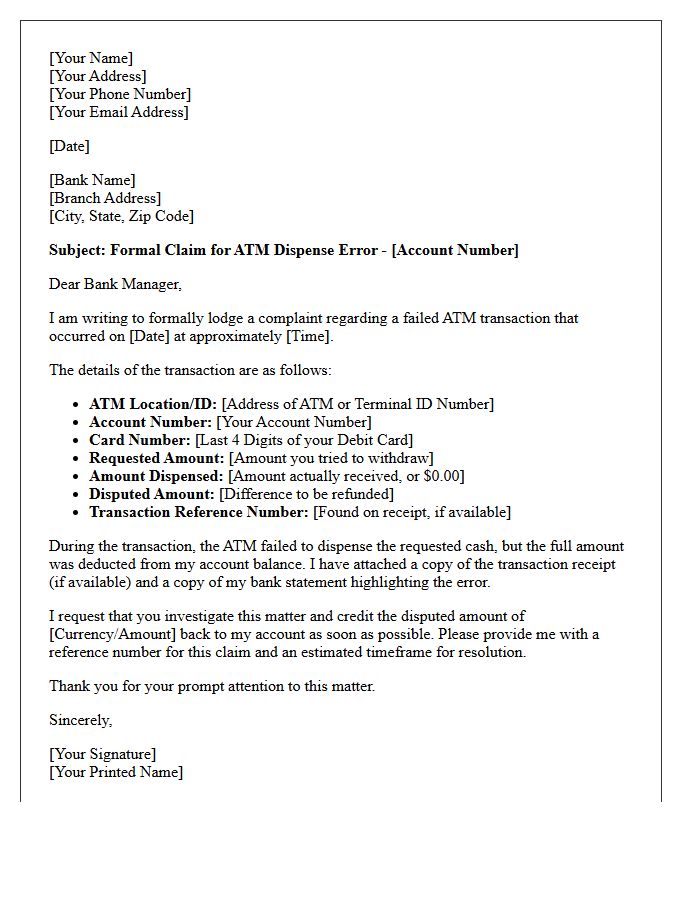

Automated Teller Machine Dispense Error Refund Letter

If an ATM fails to provide cash but debits your account, you must submit an Automated Teller Machine Dispense Error Refund Letter immediately. Clearly state the transaction date, location, and the exact amount missing. Formal written documentation serves as legal proof of your claim under banking regulations. Ensure you include the terminal ID and a copy of the failed transaction receipt. Banks are required to investigate these disputed transactions within a specific timeframe to restore your funds. Timely communication is essential for a successful reversal of charges.

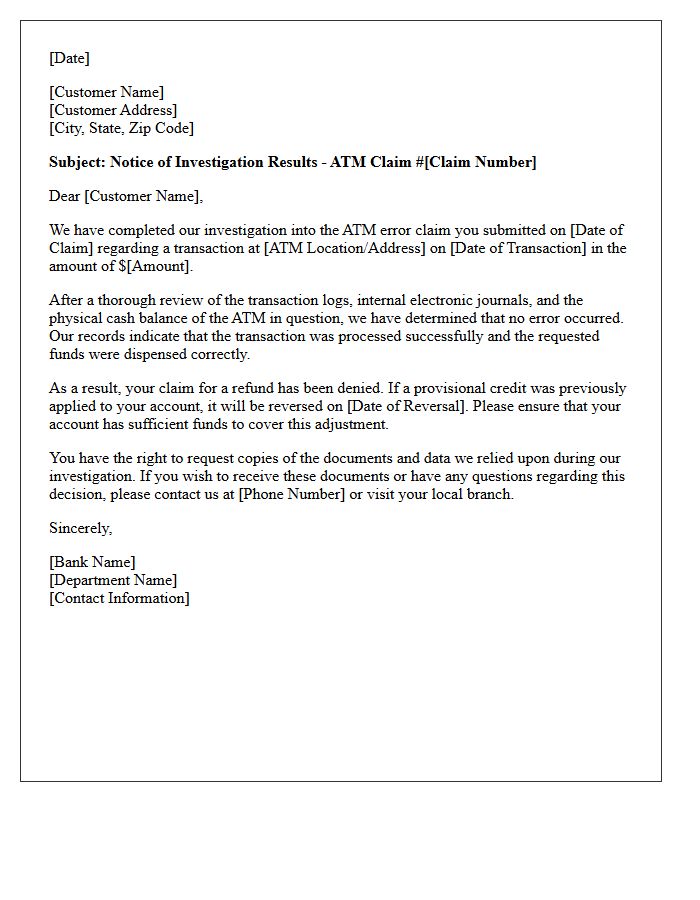

Automated Teller Machine Error Claim Denial Letter

Receiving an ATM error claim denial letter means your bank rejected a dispute regarding a failed transaction or incorrect dispense. The most critical step is to immediately request the evidence used for the decision, as required by Regulation E. Banks must provide the transaction logs, camera footage, or audit reports they relied upon. If you find discrepancies, file a formal appeal or contact the Consumer Financial Protection Bureau (CFPB). Act quickly, as strict federal timelines apply to your right to challenge these findings and recover your missing funds.

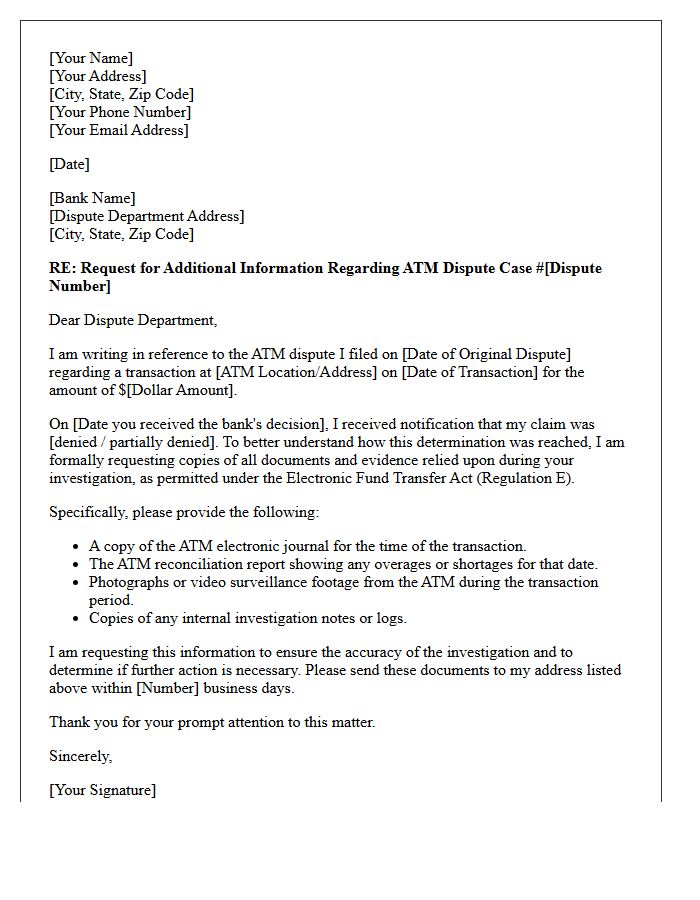

Additional Information Request for Automated Teller Machine Dispute Letter

When responding to an Additional Information Request for an ATM dispute, precision is vital. Clearly state the transaction date, exact location, and the specific amount missing. You must highlight the transaction receipt or provide a digital bank statement as primary evidence. Describe the error clearly, noting if the machine failed to dispense cash or provided an incorrect sum. Timely cooperation ensures the bank can complete its regulatory investigation under Electronic Fund Transfer laws, maximizing your chances of a successful chargeback and fund recovery.

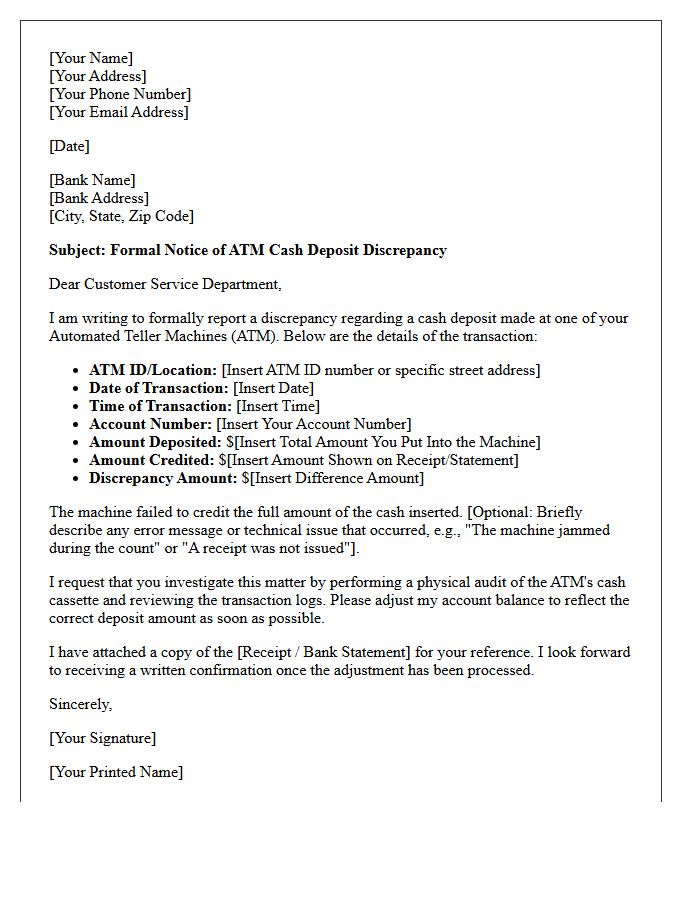

Automated Teller Machine Cash Deposit Discrepancy Adjustment Letter

If your ATM cash deposit reflects an incorrect balance, you must submit a formal discrepancy adjustment letter to your bank immediately. This document serves as an official request to rectify the error after a machine malfunction or counting mistake. Clearly state the transaction date, location, machine ID, and the exact amount missing. Providing a copy of the transaction receipt strengthens your claim. Banks typically initiate an internal audit of the ATM's physical cash log to verify and resolve the financial discrepancy within a specific regulatory timeframe.

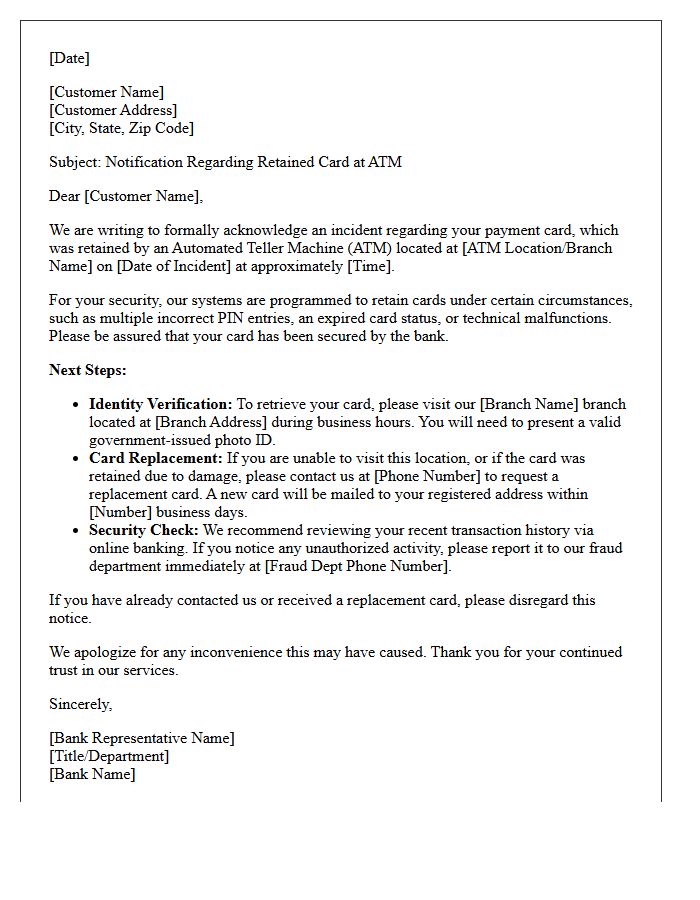

Retained Card at Automated Teller Machine Incident Response Letter

A Retained Card Incident Response Letter is a formal notification sent to customers when an ATM withholds their bank card. This document explains the security reasons for the retention, such as multiple incorrect PIN entries or hardware malfunctions. It provides clear instructions on how to retrieve the card or request a replacement. Including contact details for fraud prevention departments ensures the account remains secure while minimizing customer anxiety. Timely communication is essential for maintaining trust and resolving the transaction disruption efficiently.

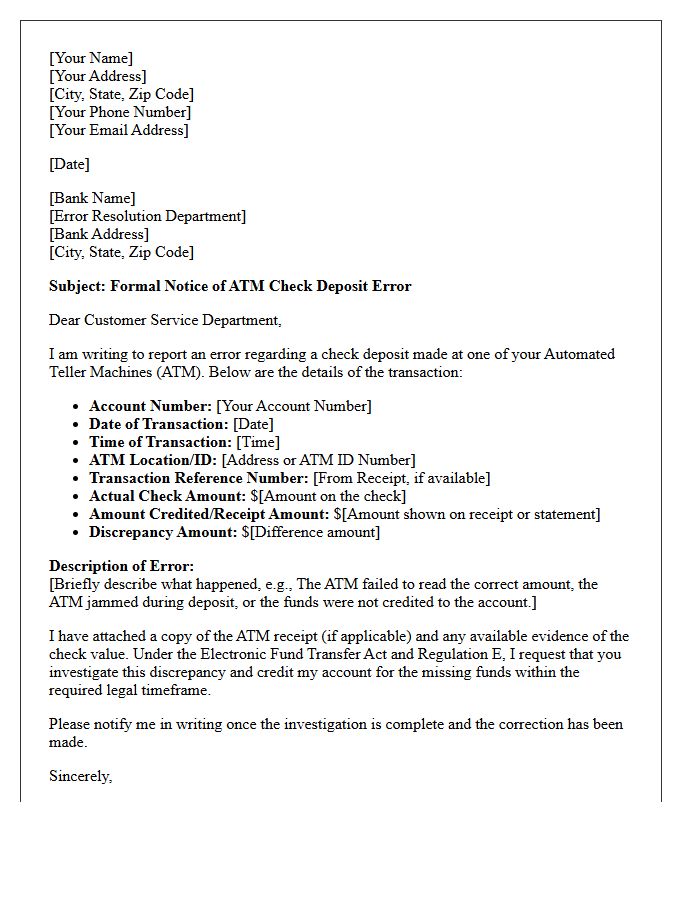

Automated Teller Machine Check Deposit Error Investigation Letter

When an ATM fails to credit your account, you must submit an Automated Teller Machine Check Deposit Error Investigation Letter immediately. Under federal law, specifically Regulation E, consumers are protected against banking malfunctions. Your formal notice should include the transaction date, machine location, and the exact missing amount. Financial institutions are legally obligated to investigate the discrepancy and provide a written resolution. Retaining your original ATM receipt is critical evidence to ensure the bank corrects the ledger balance and restores your funds promptly without unnecessary financial loss.

Automated Teller Machine Error Investigation Time Extension Letter

An Automated Teller Machine Error Investigation Time Extension Letter is a formal notice sent by banks when they require more than the standard ten business days to resolve a transaction dispute. Under Regulation E, this document informs the consumer that the investigation period is being extended, often up to forty-five or ninety days. Importantly, the bank must provide a provisional credit to your account for the disputed amount during this additional time, ensuring you have access to funds while they conduct a thorough review of the electronic error.

Provisional Credit for Automated Teller Machine Error Letter

A Provisional Credit letter is a formal notice from your bank regarding a reported ATM error. When you dispute a transaction, federal law requires banks to temporarily restore the missing funds while they investigate. This credit ensures you have access to your money during the dispute process. However, this credit is temporary; if the bank's final investigation finds no error occurred, they will legally reverse the credit and remove the funds from your account. Always keep this letter as a legal record of your reported claim.

Final Resolution for Automated Teller Machine Error Inquiry Letter

A Final Resolution letter formalizes the bank's decision regarding an ATM transaction dispute. This document confirms whether the investigated error, such as a dispensing failure or incorrect balance, was validated or denied. It serves as legal proof of the outcome under Regulation E. If the claim is successful, any provisional credit becomes permanent. If denied, the letter must explain the findings and provide instructions for requesting the documentation used during the inquiry. Always retain this letter for your financial records to ensure account accuracy and protection against future discrepancies.

Network Timeout During Automated Teller Machine Transaction Response Letter

Receiving a Network Timeout letter confirms a technical interruption occurred before the ATM could finalize your request. The most important action is to perform a Transaction Reconciliation to verify if funds were erroneously debited. If your account shows a discrepancy despite the hardware failure, you must file a Formal Dispute within the timeframe specified in the letter. Banks use these notices to document system errors, protecting your consumer rights under electronic fund transfer regulations while they investigate the connectivity lapse and restore your balance.

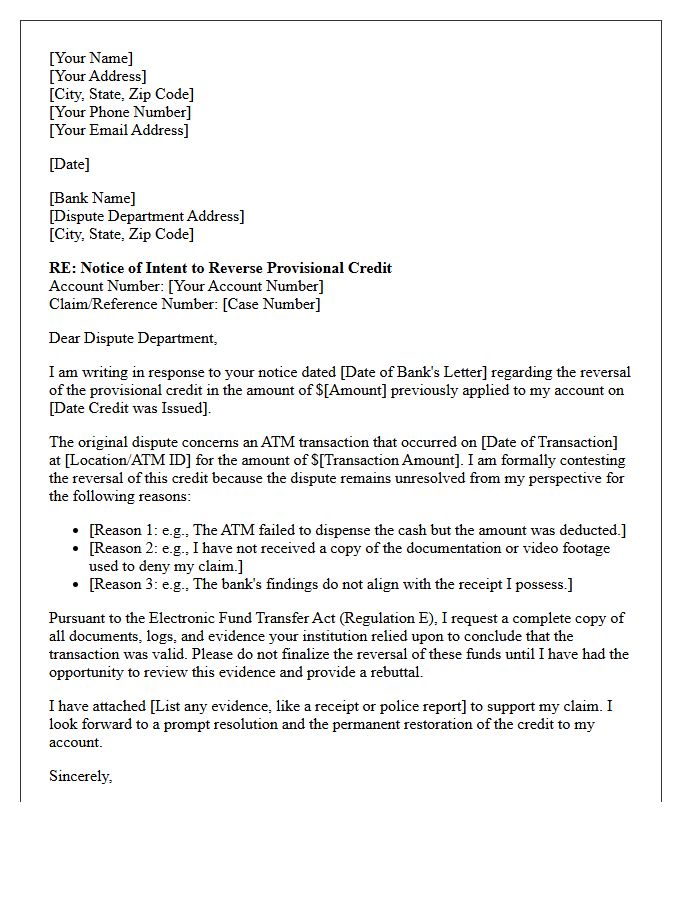

Provisional Credit Reversal for Automated Teller Machine Dispute Letter

A Provisional Credit Reversal occurs when a financial institution determines an ATM dispute is invalid after an investigation. This letter notifies the account holder that the temporary funds previously credited will be debited from their balance. It is crucial to review the bank's findings and provide additional evidence if you wish to appeal. Ensure your account maintains a sufficient balance to cover the reversal and avoid potential overdraft fees. Act quickly to challenge discrepancies, as the letter specifies a deadline for submitting further documentation regarding the disputed transaction.

How do I respond to an ATM error inquiry letter?

You should respond by clearly stating whether the error was confirmed or denied, providing the specific transaction details (date, amount, and location), and outlining the findings of the financial institution's investigation.

What information must be included in an ATM transaction dispute response?

The response letter must include the cardholder's name, the account number, the disputed transaction date, the specific ATM terminal ID, and a clear explanation of why the credit was issued or why the claim was denied based on the machine's electronic logs.

How long does a bank have to resolve an ATM error inquiry?

Under Regulation E, financial institutions generally have 10 business days to investigate an ATM error. If more time is needed, they may take up to 45 days, provided they issue a provisional credit to the customer's account during the investigation period.

What are the common reasons for denying an ATM error claim?

Common reasons for denial include the ATM's internal journal tape matching the dispensed amount, the "over/short" balance of the machine being zero at the end of the day, or security footage showing a successful cash withdrawal by the authorized user.

What are my rights if my ATM error inquiry is denied?

If the inquiry is denied, the financial institution is legally required to provide a written explanation of their findings and notify you that you have the right to request the documents and logs they used in their investigation.

Comments