Accurate financial reconciliation is vital for credit unions and banks. This article outlines essential guidelines for managing a Memorandum on Teller Cash Drawer Discrepancy Procedures, ensuring staff accountability and regulatory compliance when handling overages or shortages. Learn how to document variances effectively to maintain operational integrity. To simplify your documentation process, below are some ready to use template.

Image cover: Official Memorandum Guide: Teller Cash Drawer Discrepancy Procedures and Templates

Letter Samples List

- Letter of Warning for Minor Cash Drawer Discrepancy

- Letter of Reprimand for Repeated Cash Shortage

- Letter of Commendation for Perfect Drawer Balancing

- Letter of Notification for Cash Discrepancy Investigation

- Letter of Explanation Regarding Teller Drawer Overage

- Letter of Authorization for Surprise Drawer Audit

- Letter of Suspension Pending Discrepancy Review

- Letter of Termination for Fraudulent Cash Handling

- Letter of Acknowledgment for Discrepancy Procedure Training

- Letter of Instruction for Resolving End-of-Day Shortages

- Letter of Appeal Regarding Disciplinary Action

- Letter of Clearance Following Cash Discrepancy Audit

- Letter of Record for Daily Drawer Balancing Variance

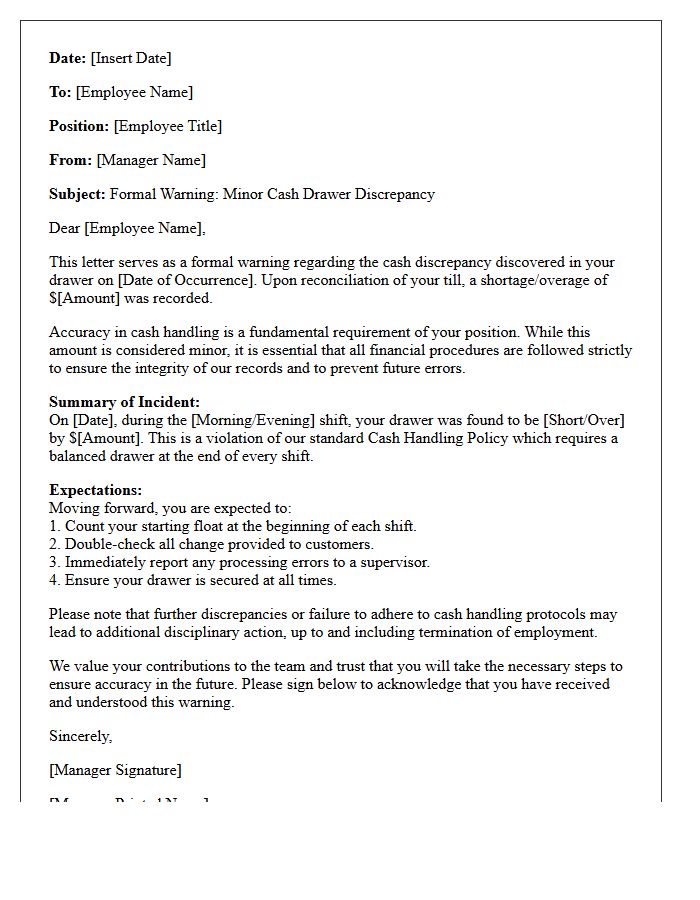

Letter of Warning for Minor Cash Drawer Discrepancy

A Letter of Warning serves as a formal disciplinary record addressing a cash drawer discrepancy. While the shortage or overage may be minor, it highlights a failure to follow established cash handling procedures. Employers use this document to emphasize the importance of accountability and financial accuracy. It typically outlines the specific incident, required corrective actions, and potential consequences for future reconcilement errors. Professionalism and strict adherence to protocol are essential to maintaining trust and ensuring operational integrity within the workplace.

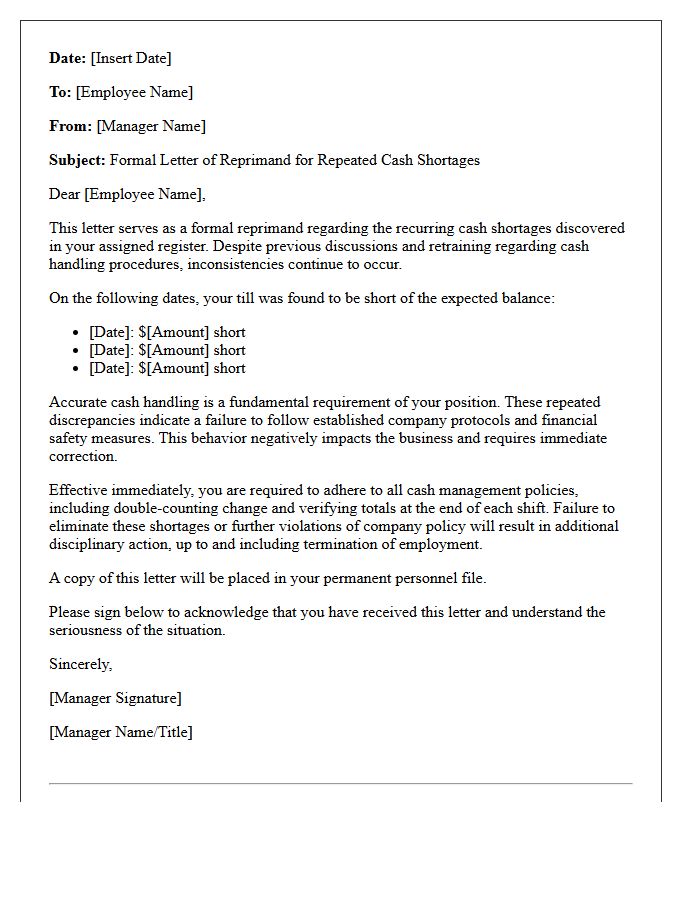

Letter of Reprimand for Repeated Cash Shortage

A Letter of Reprimand for repeated cash shortages serves as a formal disciplinary record documenting a persistent failure to maintain accurate financial accountability. This document outlines specific dates of discrepancies, violates company policy, and establishes clear expectations for future performance. It acts as a final warning, indicating that continued procedural errors or till imbalances may lead to severe consequences, including termination of employment. Employees should treat this notice as a critical opportunity to improve cash handling accuracy and comply with internal auditing standards immediately.

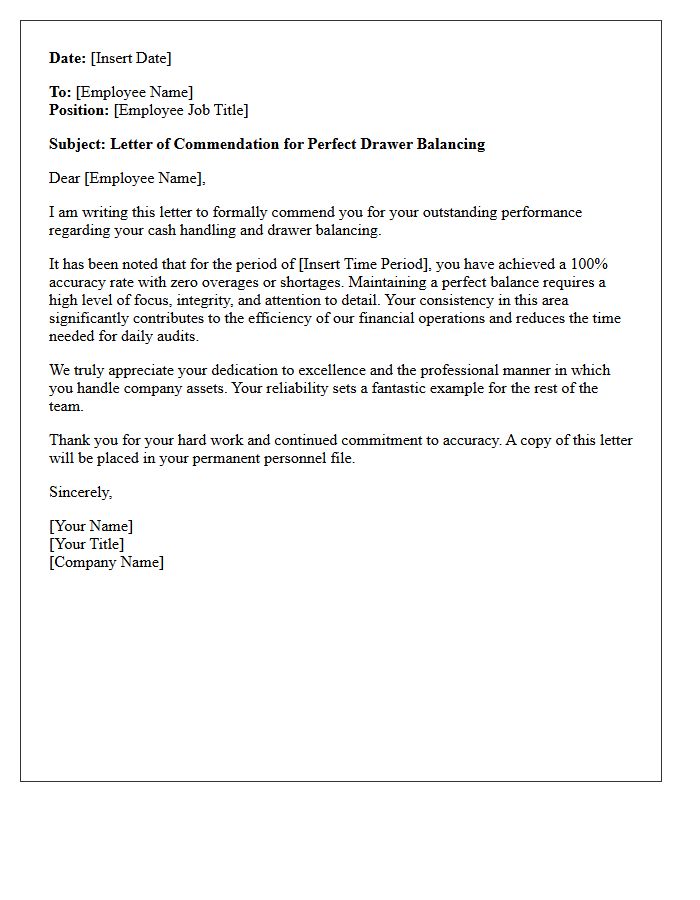

Letter of Commendation for Perfect Drawer Balancing

A Letter of Commendation for Perfect Drawer Balancing is a formal recognition awarded to employees who demonstrate exceptional accuracy in financial reconciliations. Achieving a consistent zero-variance balance reflects high integrity, attention to detail, and proficiency in cash handling procedures. This document serves as a valuable addition to a professional portfolio, highlighting accountability and reliability in high-stakes environments. Such recognition often influences performance reviews and career advancement by validating an individual's commitment to operational excellence and fiscal responsibility within the organization.

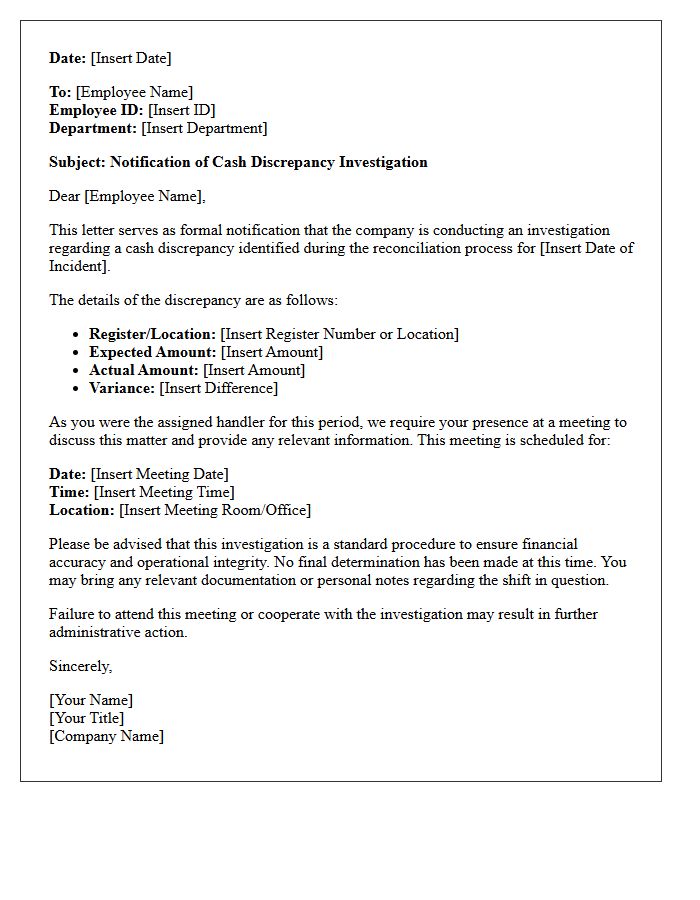

Letter of Notification for Cash Discrepancy Investigation

A Letter of Notification for Cash Discrepancy Investigation is a formal document issued when recorded balances do not match physical currency. It informs the responsible employee or department of an audit or internal review to identify the root cause, such as clerical errors, theft, or procedural failures. This notice ensures accountability and transparency throughout the financial inquiry. Receivers must provide documentation or explanations to assist in reconciliation. Understanding this process is vital for maintaining organizational integrity and ensuring that all financial discrepancies are legally and systematically resolved.

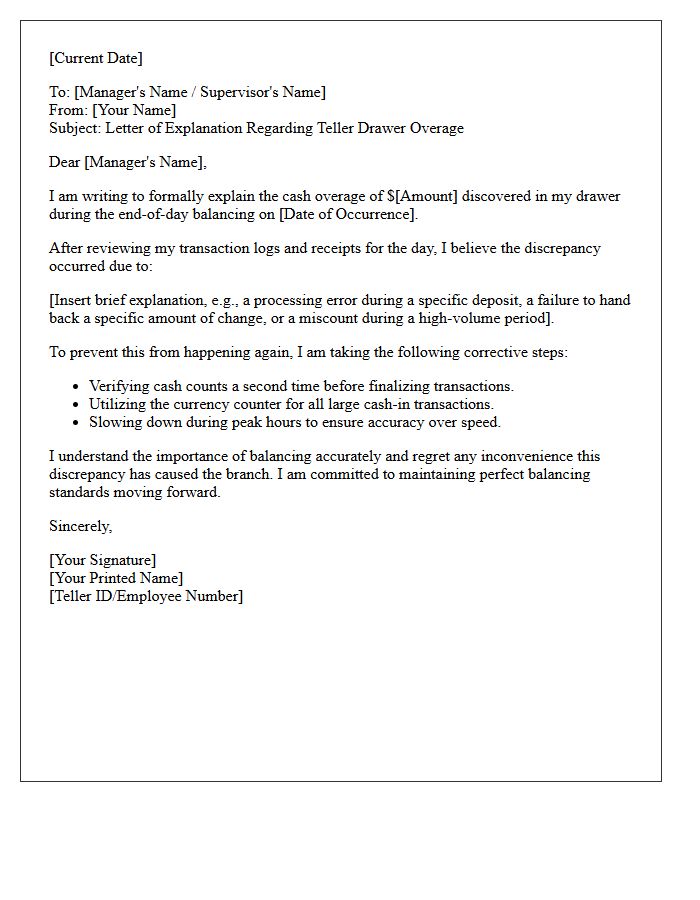

Letter of Explanation Regarding Teller Drawer Overage

A Letter of Explanation regarding a teller drawer overage is a formal document used to justify discrepancies in cash balancing. It must clearly outline the transactional error, such as a processing mistake or miscounted currency, that led to the surplus. Providing a precise audit trail and specific date helps management maintain financial integrity. Ensuring accuracy in this report is vital for internal controls and professional accountability within the banking sector.

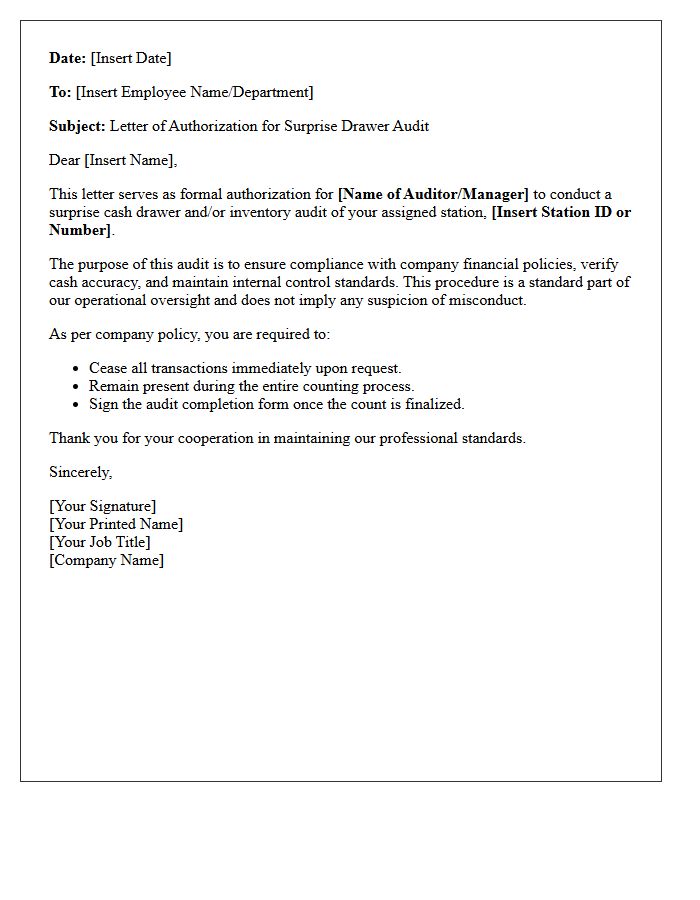

Letter of Authorization for Surprise Drawer Audit

A Letter of Authorization for a Surprise Drawer Audit is a formal document granting specific personnel the legal right to inspect cash registers without prior notice. This internal control protocol ensures financial accountability, deters employee theft, and verifies transaction accuracy. By establishing clear compliance standards, the letter protects both the business assets and the integrity of the accounting process. It must clearly state the authorized auditor's name, the scope of the inspection, and the effective date to maintain transparency and operational security within the retail or banking environment.

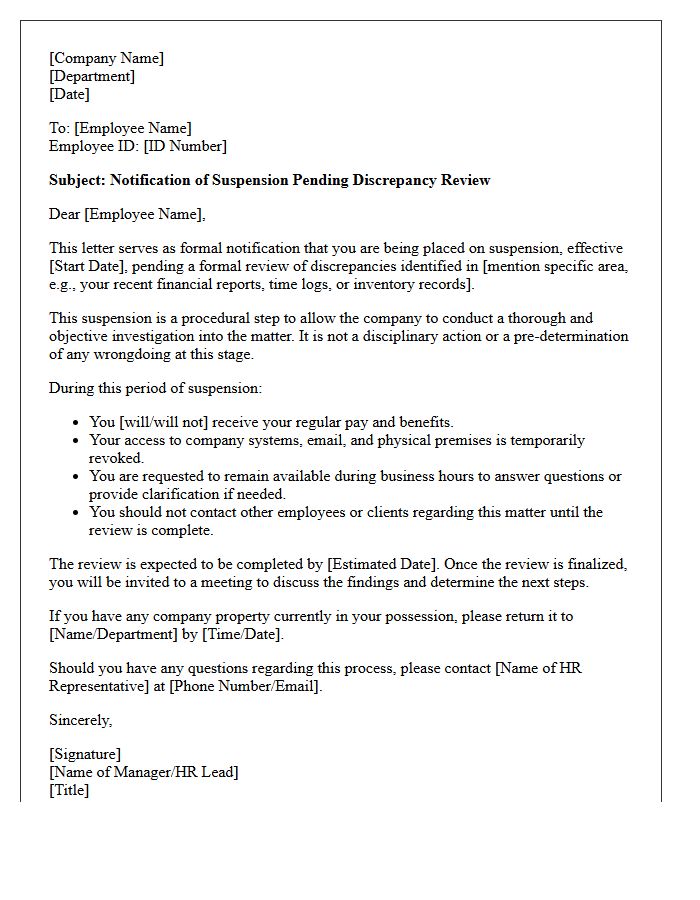

Letter of Suspension Pending Discrepancy Review

A Letter of Suspension Pending Discrepancy Review is a formal notice informing an employee of their temporary removal from duties. This action occurs when an employer identifies conflicting information or potential misconduct that requires a formal investigation. The primary purpose is to maintain workplace integrity while verifying facts. Being placed on suspension is often a procedural step rather than a final disciplinary decision. During this period, the employee should review their contract, gather evidence, and prepare for a follow-up adjudication meeting to resolve the identified inconsistencies.

Letter of Termination for Fraudulent Cash Handling

A letter of termination for fraudulent cash handling is a formal document used to permanently end employment due to financial dishonesty. It must clearly state the specific misconduct discovered, such as theft or embezzlement, following a thorough investigation. To ensure legal protection, include evidence of policy violations and the effective date of dismissal. Providing a detailed explanation helps justify the decision during potential legal disputes or unemployment claims. This document serves as a critical record of the employee's breach of fiduciary duty and the company's adherence to disciplinary protocols.

Letter of Acknowledgment for Discrepancy Procedure Training

The Letter of Acknowledgment confirms an employee's participation in discrepancy procedure training. This document serves as formal evidence that staff members understand how to identify, report, and resolve operational inconsistencies or inventory errors. By signing, employees commit to following established protocols, ensuring regulatory compliance and organizational accountability. It is a critical record for quality management systems and internal audits, verifying that the workforce is equipped to maintain data integrity and minimize risks associated with procedural deviations in the workplace.

Letter of Instruction for Resolving End-of-Day Shortages

A Letter of Instruction is a formal document used to authorize specific financial actions for resolving end-of-day shortages. It directs a bank or institution to move funds from a secondary account to cover deficits, ensuring all transactions settle. This process is vital for maintaining liquidity management and preventing overdraft fees. By providing clear standing orders, businesses automate cash positioning and maintain financial stability without manual intervention during daily closing procedures. Proper documentation ensures regulatory compliance and accurate record-keeping for all automated fund transfers.

Letter of Appeal Regarding Disciplinary Action

A Letter of Appeal Regarding Disciplinary Action is a formal document used to challenge an employer's decision. It must clearly outline the grounds for appeal, such as new evidence, procedural errors, or an unfairly harsh penalty. Ensure the tone remains professional and provide specific facts to support your case. Submitting this written request within the company's specified deadline is crucial for protecting your employment rights and ensuring a fair review of the disciplinary process. Clearly state the desired outcome to resolve the matter effectively.

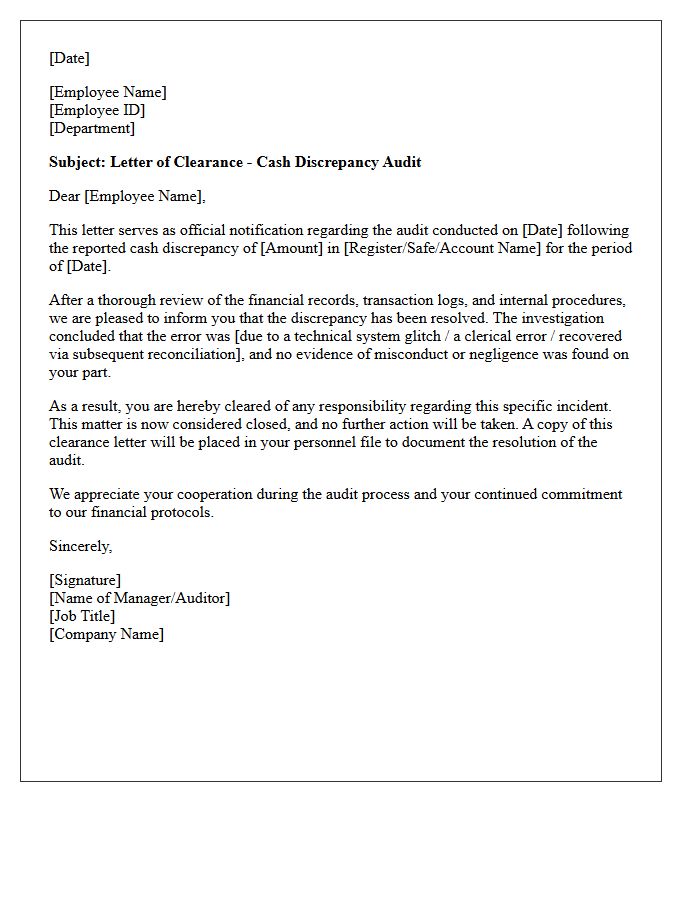

Letter of Clearance Following Cash Discrepancy Audit

A Letter of Clearance is a formal document issued after a cash discrepancy audit to confirm that all financial inconsistencies have been resolved. It serves as official proof that an employee or department is no longer under investigation for missing funds. This letter is essential for professional exoneration, protecting your reputation and future employability. It verifies that the audit trail is complete and that you are cleared of any liability or suspicion regarding the previously identified shortages, ensuring full accountability and closure within the organization.

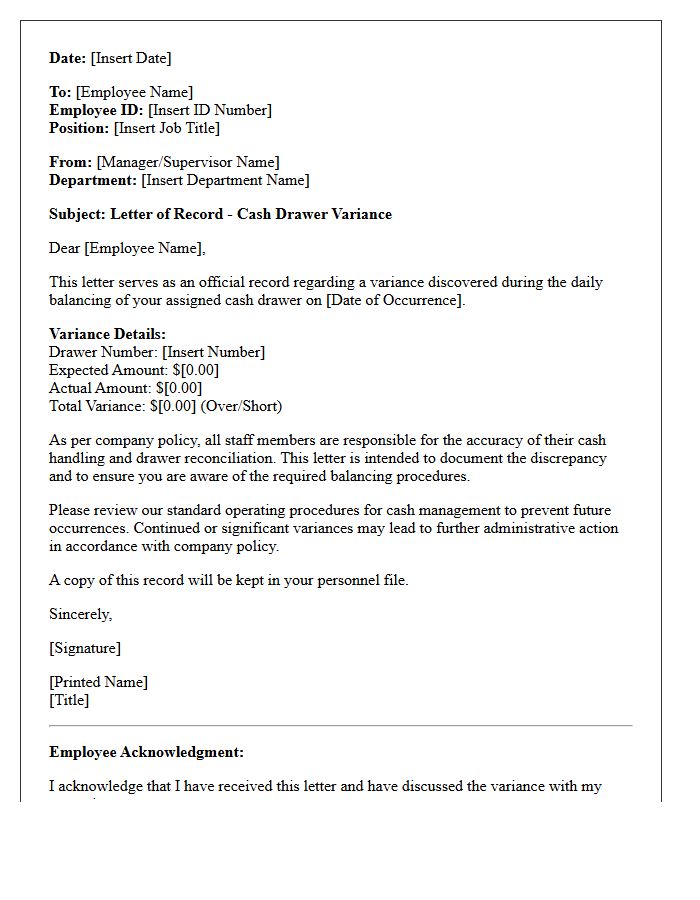

Letter of Record for Daily Drawer Balancing Variance

A Letter of Record for daily drawer balancing variance serves as a formal internal document used to track discrepancies between physical cash and sales reports. It is crucial for maintaining financial accountability and identifying patterns of loss or administrative error. When a variance occurs, this record provides a clear audit trail, ensuring transparency in retail operations. Consistent reconciliation helps managers implement corrective training and prevents internal theft. Maintaining these records is an essential practice for effective cash management and long-term loss prevention strategies within any business handling physical currency.

What is the purpose of the Memorandum on Teller Cash Drawer Discrepancy Procedures?

The memorandum establishes standardized protocols for identifying, reporting, and resolving cash variances to ensure financial accuracy and teller accountability.

When must a teller report a cash drawer discrepancy?

Any cash overage or shortage must be reported immediately to the supervisor or head teller as soon as the discrepancy is identified during balancing.

What are the mandatory steps for investigating a cash imbalance?

Tellers must perform a second count of the physical cash, verify all transaction receipts against the journal, and review processed checks or vouchers for entry errors.

What documentation is required for an unresolved cash variance?

Unresolved discrepancies require a formal Cash Variance Report, which must be signed by both the teller and the branch manager and filed for internal audit review.

What are the disciplinary consequences for frequent cash discrepancies?

Repeated variances exceeding established thresholds may result in mandatory retraining, loss of signing authority, or further disciplinary action as outlined in the human resources policy.

Comments