Compliance with Know Your Customer legal information demand is essential for financial transparency and risk mitigation. Regulatory bodies require businesses to verify client identities to prevent fraud and money laundering. Understanding these mandates ensures your organization remains compliant while protecting sensitive data through standardized procedures. To simplify your documentation process, below are some ready to use template.

Image cover: Mastering KYC Legal Information Requests: Essential Samples and Templates

Letter Samples List

- Initial Know Your Customer Information Demand Letter

- Corporate Entity Legal Structure Declaration Letter

- Ultimate Beneficial Ownership Verification Letter

- Enhanced Due Diligence Information Demand Letter

- Source Of Wealth Legal Verification Letter

- Politically Exposed Person Compliance Letter

- Routine Know Your Customer Update Demand Letter

- Trust Legal Documentation Request Letter

- Cross Border Account Compliance Demand Letter

- High Risk Client Legal Information Demand Letter

- Missing Know Your Customer Document Warning Letter

- Final Notice Account Suspension Letter

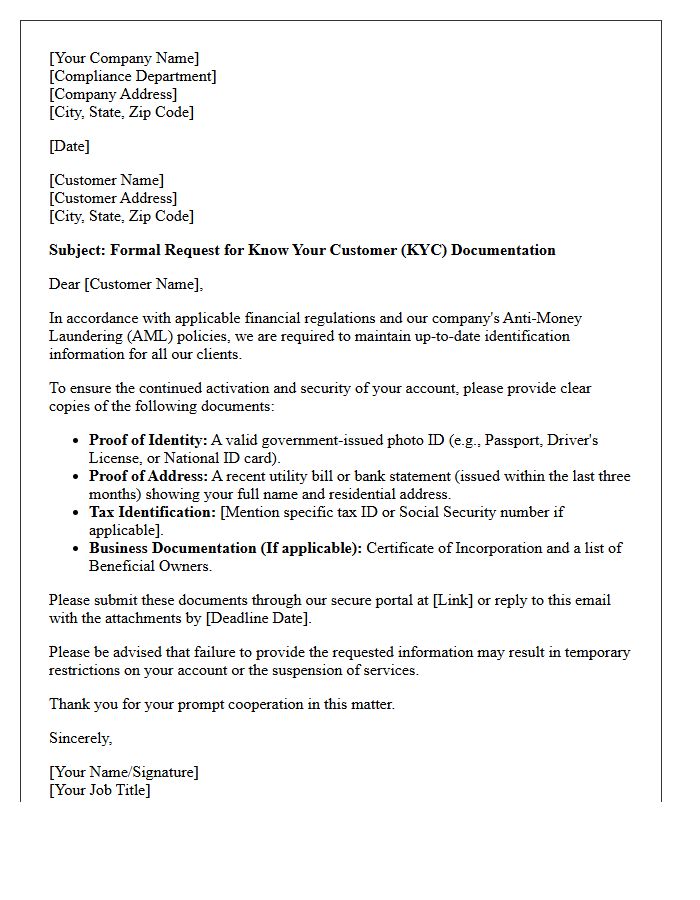

Initial Know Your Customer Information Demand Letter

An Initial Know Your Customer (KYC) Information Demand Letter is a formal request from financial institutions to verify a client's identity and assess potential risks. This document is essential for regulatory compliance against money laundering and fraud. Recipients must provide accurate personal data, such as identification and proof of address, within a specific timeframe. Failure to respond to this due diligence inquiry can lead to account restrictions or termination. Promptly submitting the required documentation ensures your financial activities remain transparent and legally compliant with international banking standards.

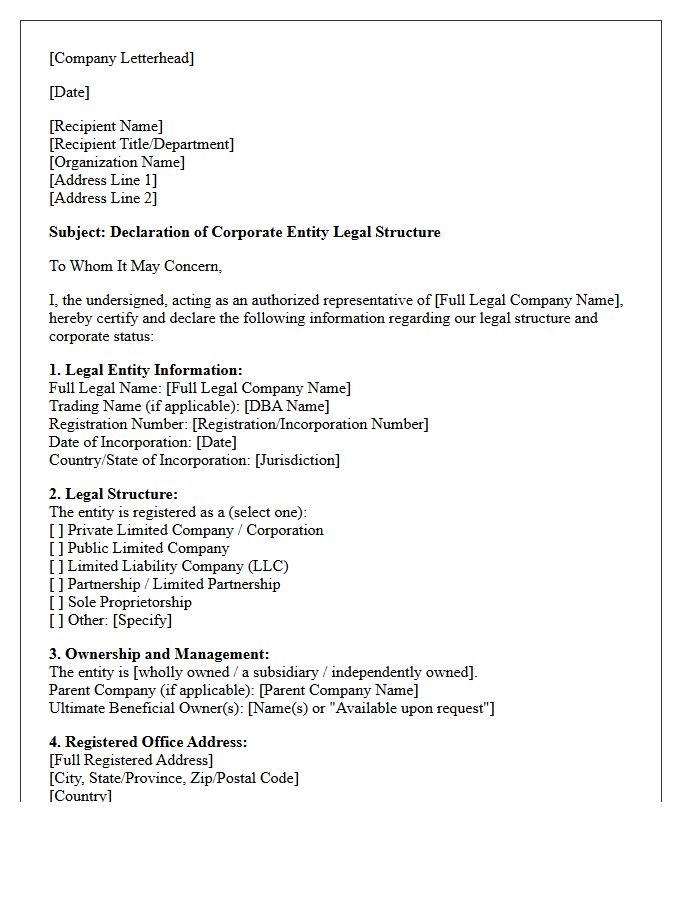

Corporate Entity Legal Structure Declaration Letter

A Corporate Entity Legal Structure Declaration Letter is a formal document used to verify a business's legal framework and ownership details. It provides authorities or financial institutions with essential information regarding regulatory compliance and operational status. This declaration confirms the entity's type, such as a corporation or LLC, ensuring transparency in legal and tax matters. It is a mandatory requirement for many KYC procedures, corporate account openings, and international trade agreements to prevent fraud and ensure accountability within the global market.

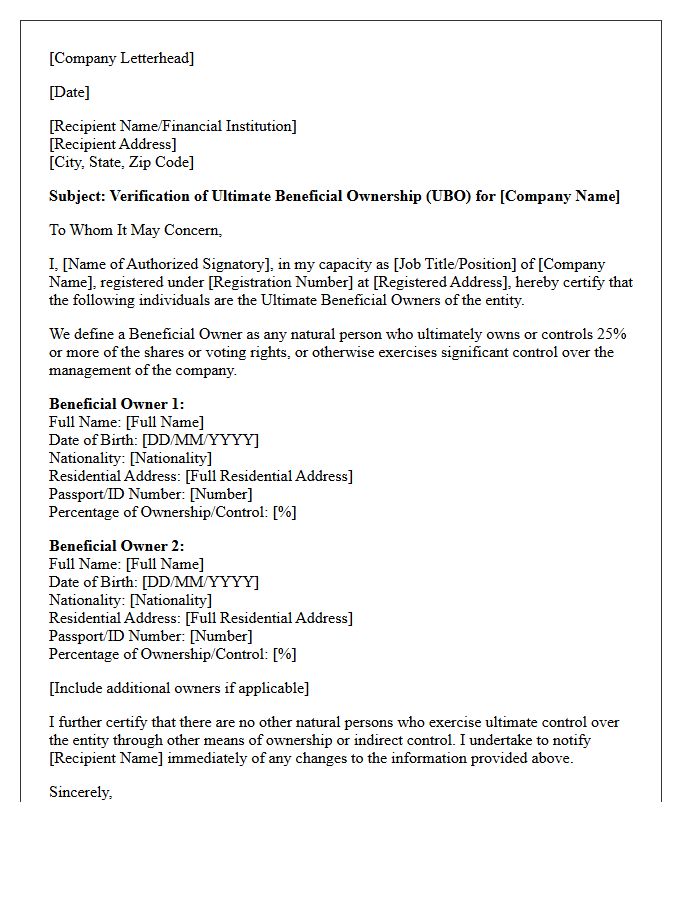

Ultimate Beneficial Ownership Verification Letter

An Ultimate Beneficial Ownership (UBO) Verification Letter is a legal document used to identify individuals who exercise significant control or own more than 25% of a legal entity. Financial institutions require this letter to ensure compliance with Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations. It prevents financial crimes by uncovering the true natural persons behind corporate structures. Providing accurate details, such as full names and tax IDs, is essential for maintaining transparent business relationships and meeting global regulatory standards during bank account openings or due diligence processes.

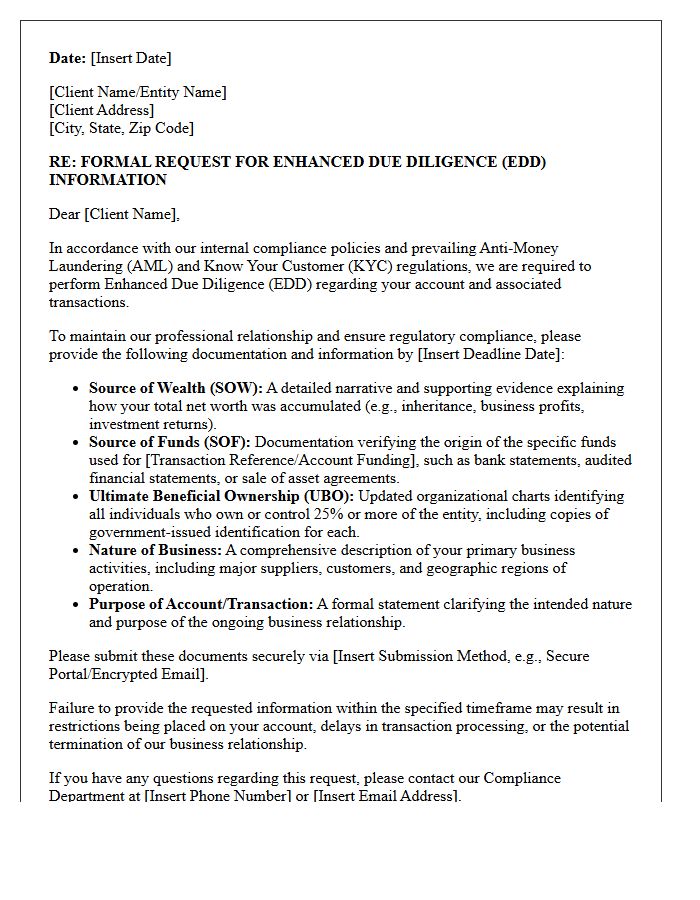

Enhanced Due Diligence Information Demand Letter

An Enhanced Due Diligence (EDD) Information Demand Letter is a formal request from financial institutions to high-risk clients. It mandates the disclosure of detailed source of wealth, transaction origins, and ultimate beneficial ownership. Failure to provide comprehensive documentation can lead to immediate account restrictions or termination. This process ensures compliance with global Anti-Money Laundering (AML) regulations by mitigating potential financial crimes. Recipients must respond accurately and promptly to satisfy rigorous regulatory scrutiny and maintain their banking relationship while demonstrating full transparency regarding their fiscal activities.

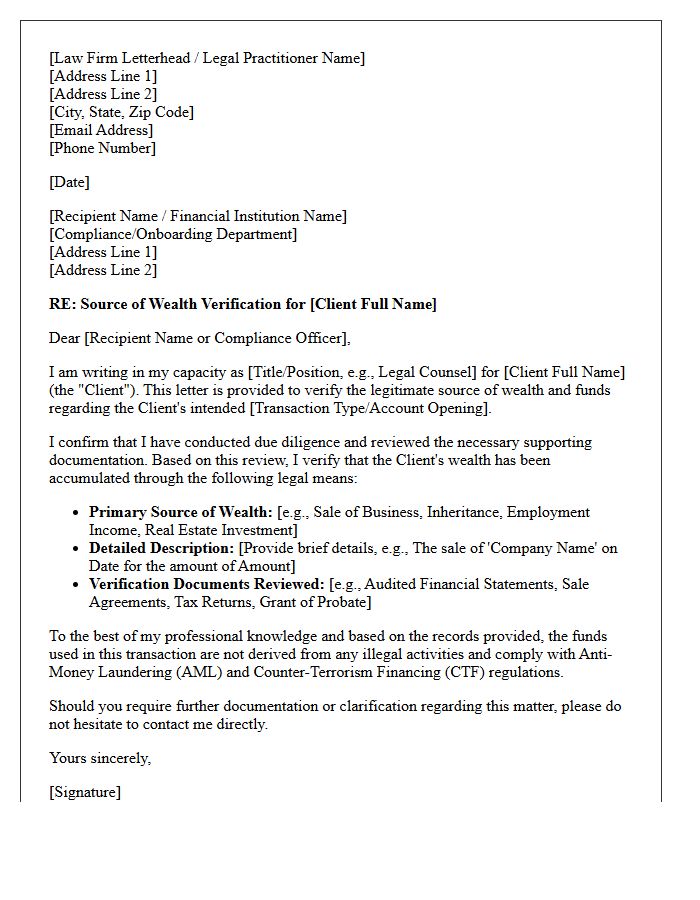

Source Of Wealth Legal Verification Letter

A Source of Wealth (SoW) Legal Verification Letter is a formal document used to confirm the legitimacy of an individual's total net worth. Typically issued by a lawyer or licensed accountant, it provides compliance evidence for anti-money laundering (AML) regulations. Financial institutions require this letter to verify that accumulated assets originate from lawful activities like inheritance, business profits, or investments. Ensuring transparency during high-value transactions, this verification protects both the client and the bank by validating the historical origin of funds through professional legal attestation.

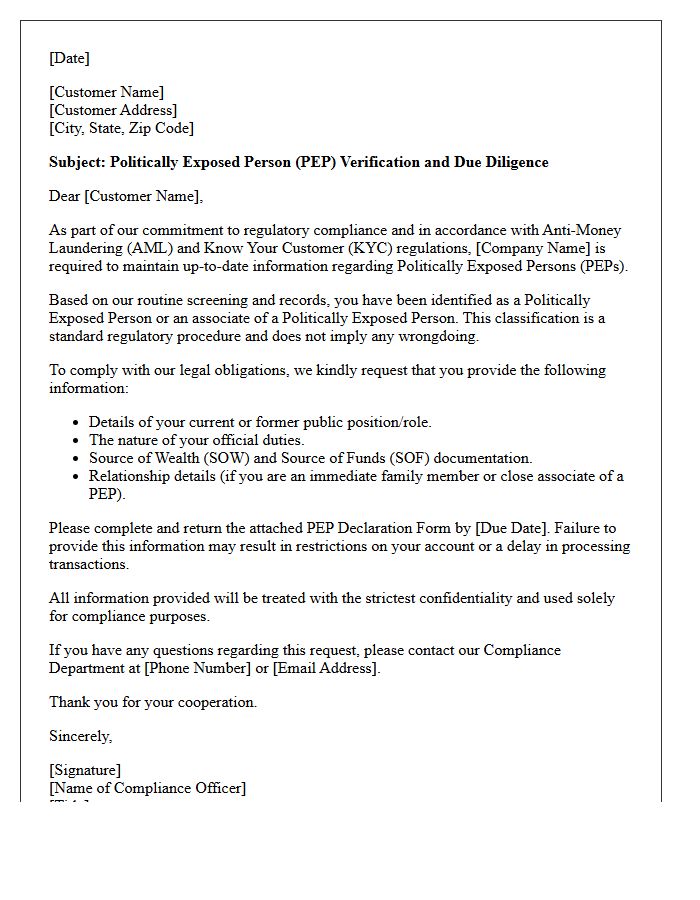

Politically Exposed Person Compliance Letter

A Politically Exposed Person (PEP) Compliance Letter is a formal document used by financial institutions to verify the identity and risk level of individuals in prominent public positions. This due diligence process is essential for meeting Anti-Money Laundering (AML) regulations. The letter confirms whether a client, or their close associates, holds political influence that could increase exposure to bribery or corruption. Providing accurate information ensures legal compliance and prevents potential financial crimes, protecting both the institution and the individual from regulatory penalties during the onboarding or monitoring stages.

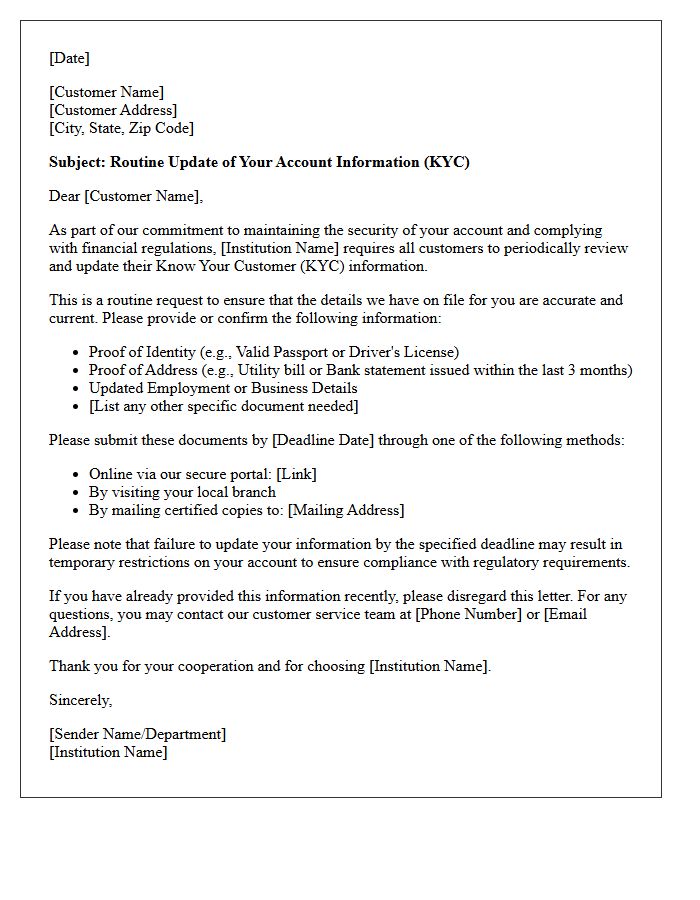

Routine Know Your Customer Update Demand Letter

A Routine Know Your Customer Update Demand Letter is a formal request from a financial institution to verify your identity and financial profile. This mandatory compliance procedure ensures your account remains active and prevents unauthorized access. It is crucial to provide updated identification documents and proof of address before the specified deadline. Failure to respond to this regulatory requirement may result in temporary account restrictions or full closure. Always verify the sender's authenticity to protect against phishing while ensuring your legal information remains current for continued banking services.

Trust Legal Documentation Request Letter

A Trust Legal Documentation Request Letter is a formal written demand sent by a beneficiary to a trustee to obtain essential information. This document is vital for transparency and ensures the trustee fulfills their fiduciary duties. It typically requests copies of the trust agreement, accounting reports, and asset lists to verify proper administration. Under most jurisdictions, beneficiaries have a legal right to this information to protect their interests. Using a formal request creates a legal record, which is necessary if disputes arise or if court intervention is required to enforce disclosure.

Cross Border Account Compliance Demand Letter

A Cross Border Account Compliance Demand Letter is a formal legal notification issued by financial institutions to resolve regulatory discrepancies in international banking. It typically mandates that account holders provide updated tax documentation, such as FATCA or CRS certifications, to confirm their residency status. Failure to respond promptly can lead to account freezing, mandatory tax withholding, or permanent closure. Ensuring total transparency and meeting the specified deadlines is essential to maintaining global financial standing and avoiding severe legal penalties or investigations by international tax authorities.

High Risk Client Legal Information Demand Letter

A High Risk Client Legal Information Demand Letter is a formal notice used to mitigate exposure when dealing with volatile or non-compliant parties. This document serves as a pre-litigation strategy to secure vital evidence, clarify contractual breaches, and establish a clear timeline for response. By formalizing demands for documentation or payment, you create an essential paper trail for potential court proceedings. It is crucial to ensure all claims are legally substantiated to prevent defamation or harassment allegations while protecting your professional interests against high-risk behavior.

Missing Know Your Customer Document Warning Letter

A Missing Know Your Customer (KYC) Document Warning Letter is a formal notice from a financial institution requesting essential identity verification documents. This compliance requirement is mandatory under anti-money laundering regulations. Failure to provide the requested information, such as proof of address or government ID, may lead to temporary account restrictions or total suspension. It is crucial to respond promptly to these alerts to ensure uninterrupted access to banking services and maintain legal regulatory standards. Always verify the request through official channels to protect against potential phishing attempts.

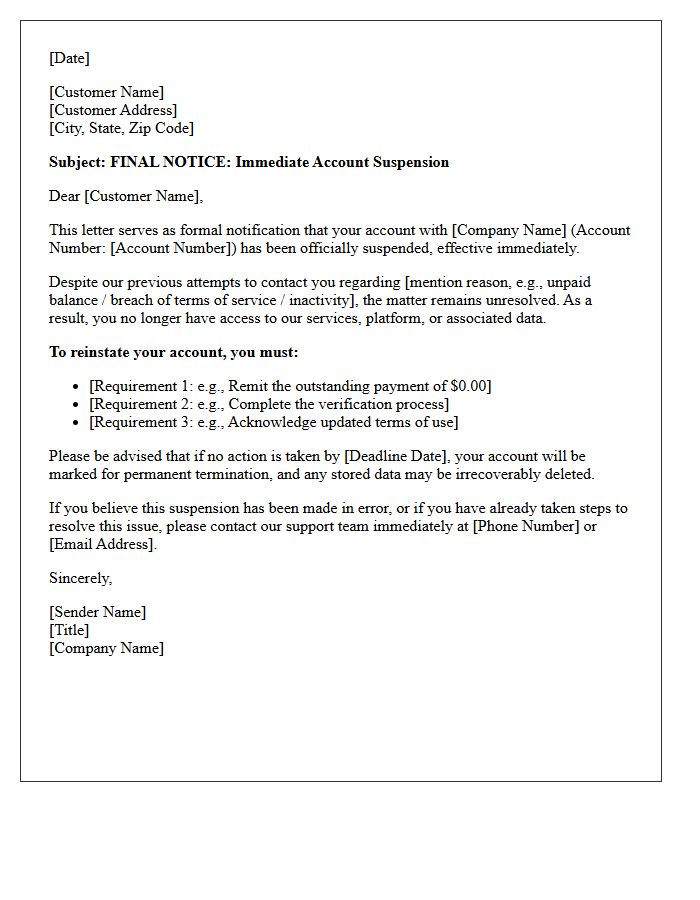

Final Notice Account Suspension Letter

A Final Notice Account Suspension Letter is a critical legal notification informing a user that their access to a service is being permanently revoked. This document typically outlines specific policy violations or non-compliance issues that led to the decision. It serves as the last stage of communication before account termination. Recipients should immediately review the provided justification and follow any listed appeal procedures if they believe the action was taken in error. Ignoring this notice usually results in total loss of data and service access without further warning.

What is a Know Your Customer (KYC) legal information demand?

A KYC legal information demand is a mandatory regulatory requirement where financial institutions collect and verify identity documents, corporate structures, and beneficial ownership details to prevent money laundering and financial crimes.

Which laws mandate the collection of KYC information?

KYC demands are primarily driven by the Anti-Money Laundering (AML) and Counter-Terrorist Financing (CTF) regulations, such as the Bank Secrecy Act in the US, the EU Anti-Money Laundering Directives, and local financial authority guidelines.

What specific documents are required for a KYC legal check?

Individuals typically must provide government-issued photo ID and proof of address. Entities must provide certificates of incorporation, articles of association, and a register of ultimate beneficial owners (UBOs) holding more than 25% interest.

Why do existing clients receive new KYC information demands?

Financial institutions are legally obligated to perform "Ongoing Monitoring." This requires periodic updates of client information to ensure records remain accurate and to assess changes in the risk profile of the business relationship.

What are the legal consequences of failing to provide KYC information?

Failure to comply with a KYC demand typically results in the restriction of account functionalities, freezing of assets, or the termination of the business relationship to ensure the institution remains compliant with international banking laws.

Comments