Receiving a refinance application denial letter due to an underwater mortgage can be frustrating. This occurs when your home's market value is lower than your outstanding loan balance, creating negative equity. Understanding your options is the first step toward regaining financial stability and exploring alternative relief programs. To help you respond effectively to lenders, below are some ready to use templates.

Image cover: Winning Your Appeal: Underwater Mortgage Refinance Denial Letter Templates

Letter Samples List

- Negative Equity Refinance Denial Letter

- Underwater Mortgage Refinance Rejection Letter

- Insufficient Equity Refinance Adverse Action Letter

- Loan-to-Value Exceeded Refinance Denial Letter

- Property Appraisal Shortfall Refinance Decline Letter

- Home Value Deficit Refinance Application Denial Letter

- Adverse Action Letter for Underwater Mortgage Refinance

- Notice of Refinance Denial Due to Underwater Mortgage Letter

- Insufficient Collateral Refinance Rejection Letter

- Underwater Property Refinance Ineligibility Letter

- High Loan-to-Value Refinance Application Denial Letter

- Valuation Deficit Refinance Denial Letter

Negative Equity Refinance Denial Letter

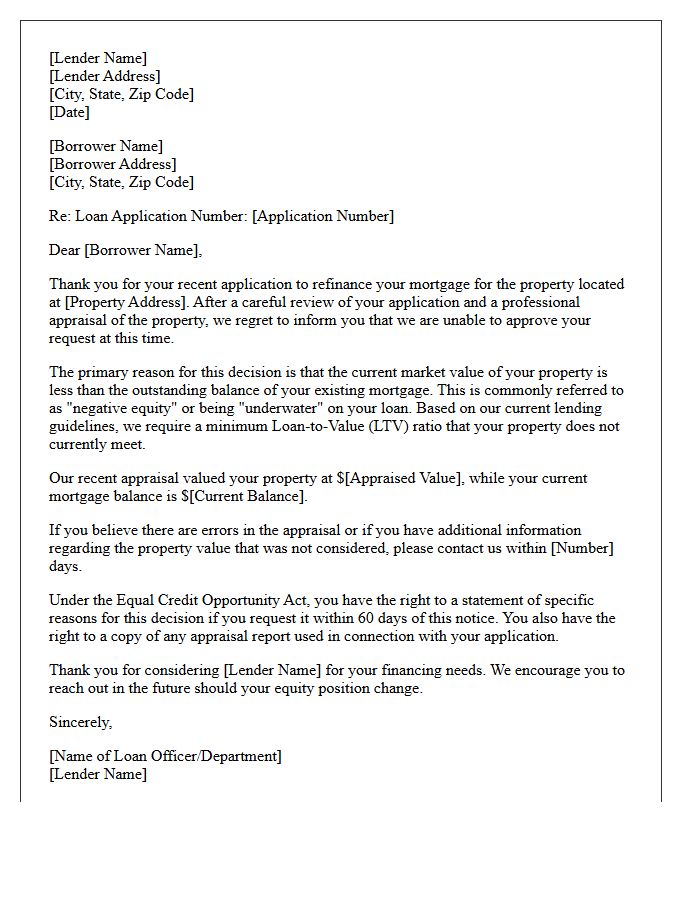

Receiving a Negative Equity Refinance Denial Letter indicates that your home's current market value is lower than your outstanding mortgage balance. Lenders typically reject applications when there is "underwater" collateral because it exceeds the maximum loan-to-value (LTV) ratio required for approval. This document formally outlines the appraisal shortfall and your creditworthiness status. To resolve this, homeowners should explore government-backed relief programs, consider a cash-in refinance, or appeal the valuation if comparable local sales support a higher price. Understanding these specific reasons is essential for financial recovery.

Underwater Mortgage Refinance Rejection Letter

Receiving an underwater mortgage refinance rejection letter indicates your home's market value is lower than your outstanding loan balance. Lenders typically deny applications when the loan-to-value (LTV) ratio exceeds traditional limits, creating excessive risk. To resolve this, review the specific denial reasons, such as credit score or debt-to-income issues. Explore government-backed alternatives like HIRO or specialized streamline programs designed for negative equity. Correcting errors on your appraisal or improving your financial profile can help you reapply successfully and secure a lower interest rate despite being underwater.

Insufficient Equity Refinance Adverse Action Letter

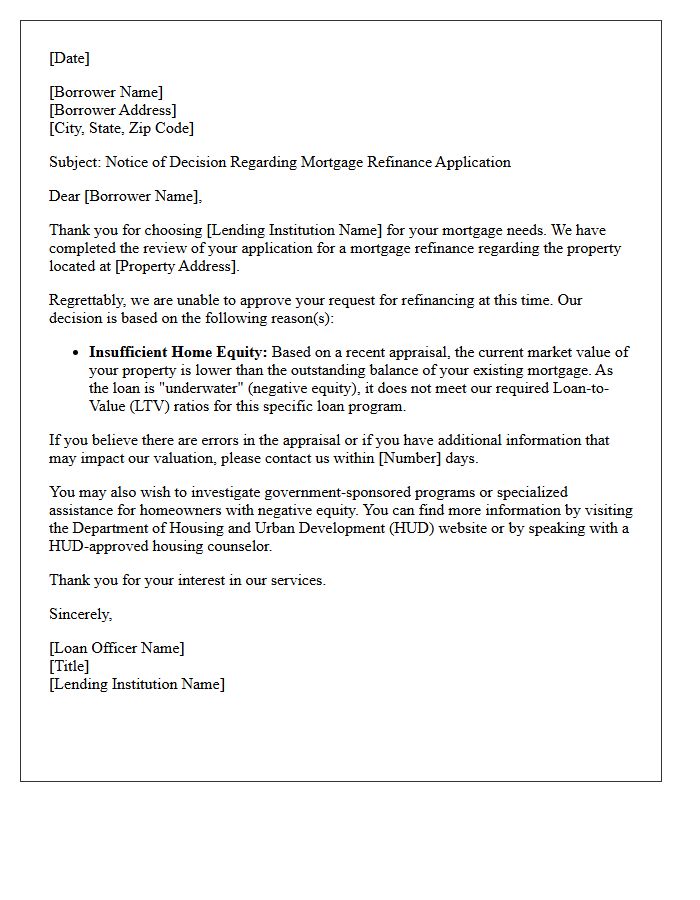

An Insufficient Equity Refinance Adverse Action Letter is a formal notice issued by lenders when a mortgage application is denied because the property's appraised value is too low relative to the requested loan amount. This document explains that the borrower lacks the required loan-to-value (LTV) ratio to qualify for the new terms. Under the Equal Credit Opportunity Act, lenders must provide specific reasons for the rejection, allowing borrowers to understand equity shortfalls or challenge potential appraisal inaccuracies before seeking alternative financing options.

Loan-to-Value Exceeded Refinance Denial Letter

A Loan-to-Value Exceeded Refinance Denial Letter is a formal notification sent by lenders when a property's current market value is too low compared to the requested loan amount. This occurs when the LTV ratio surpasses the lender's maximum threshold, often due to declining property values or insufficient equity. To resolve this, borrowers can appeal the appraisal, pay down the principal balance, or explore government-backed programs like the High LTV Refinance Option. Understanding this letter is essential for identifying financial gaps before reapplying for mortgage refinancing.

Property Appraisal Shortfall Refinance Decline Letter

Receiving a property appraisal shortfall refinance decline letter occurs when a home's market value is lower than the loan amount requested. This discrepancy increases the loan-to-value (LTV) ratio, often exceeding lender risk thresholds. To resolve this, homeowners can challenge the appraisal with comparable sales data, provide a larger cash contribution to reduce the debt, or seek a second opinion. Understanding these valuation gaps is essential for successfully restructuring your refinancing application and meeting lender equity requirements before reapplying for mortgage approval.

Home Value Deficit Refinance Application Denial Letter

Receiving a Home Value Deficit Refinance Application Denial Letter indicates your mortgage balance exceeds the property's current market worth, often called being underwater. This negative equity creates a high loan-to-value ratio, making traditional refinancing difficult. To resolve this, homeowners should review the appraisal report for errors or consider government assistance programs like HIRO or FMERR. Improving your credit score and paying down principal can also help bridge the gap. Understanding this letter is crucial for navigating alternative debt restructuring options to stabilize your financial future.

Adverse Action Letter for Underwater Mortgage Refinance

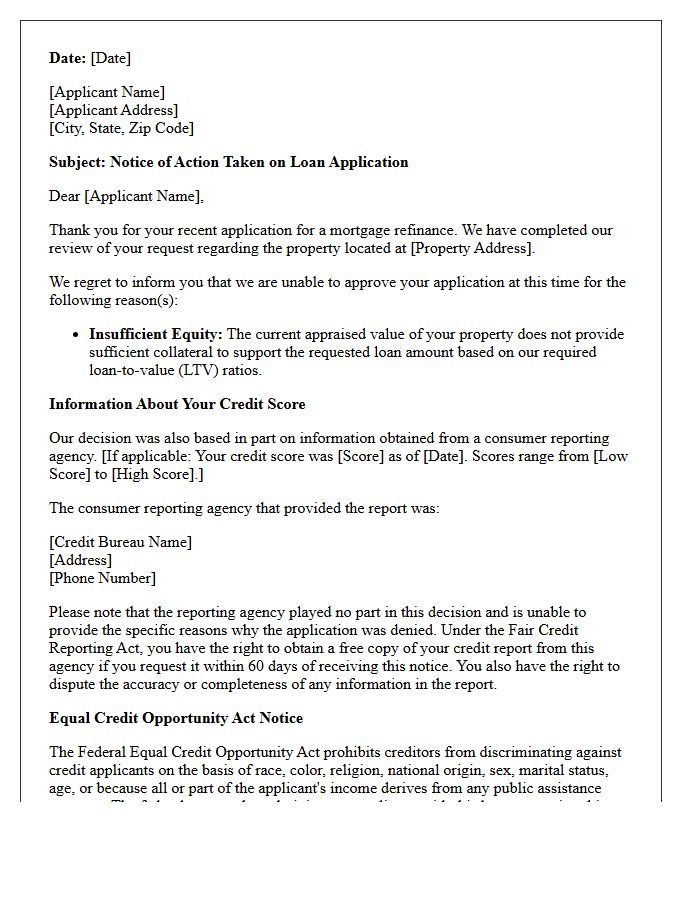

An Adverse Action Letter is a formal notice issued by lenders when denying an underwater mortgage refinance application. Under the Equal Credit Opportunity Act, this document must clearly state the specific reasons for rejection, such as a high loan-to-value ratio or insufficient creditworthiness. For homeowners with negative equity, receiving this letter is critical for consumer protection, as it identifies financial barriers and outlines your right to dispute inaccuracies in credit reports. Understanding these disclosures helps borrowers address valuation gaps before reapplying for government-backed relief programs.

Notice of Refinance Denial Due to Underwater Mortgage Letter

Receiving a notice of refinance denial due to an underwater mortgage indicates that your home's current market value is lower than your outstanding loan balance. Lenders typically require a specific loan-to-value ratio to approve new terms. This negative equity situation makes traditional refinancing difficult as the property serves as insufficient collateral. To address this, homeowners should explore government-backed programs like the High LTV Refinance Option or contact their servicer to discuss specialized loan modification alternatives designed for properties with declining values.

Insufficient Collateral Refinance Rejection Letter

An Insufficient Collateral Refinance Rejection Letter is a formal notification from a lender stating that your property's current appraised value is too low to secure the requested loan amount. This occurs when the Loan-to-Value (LTV) ratio exceeds the bank's risk threshold, meaning the asset does not provide enough security for the debt. To resolve this, borrowers can challenge the appraisal, provide a larger down payment to reduce the principal, or seek a loan with more flexible equity requirements. Understanding this document is vital for navigating mortgage restructuring hurdles.

Underwater Property Refinance Ineligibility Letter

Receiving an Underwater Property Refinance Ineligibility Letter indicates that your home's current market value is lower than your outstanding mortgage balance. This negative equity situation often leads to denial because traditional lenders require specific loan-to-value ratios to mitigate risk. To move forward, review the document for specific reasons, such as credit scores or debt-to-income limits. You may still qualify for relief through specialized government programs or private loan modifications designed specifically for negative equity homeowners seeking to lower their monthly payments despite current valuation gaps.

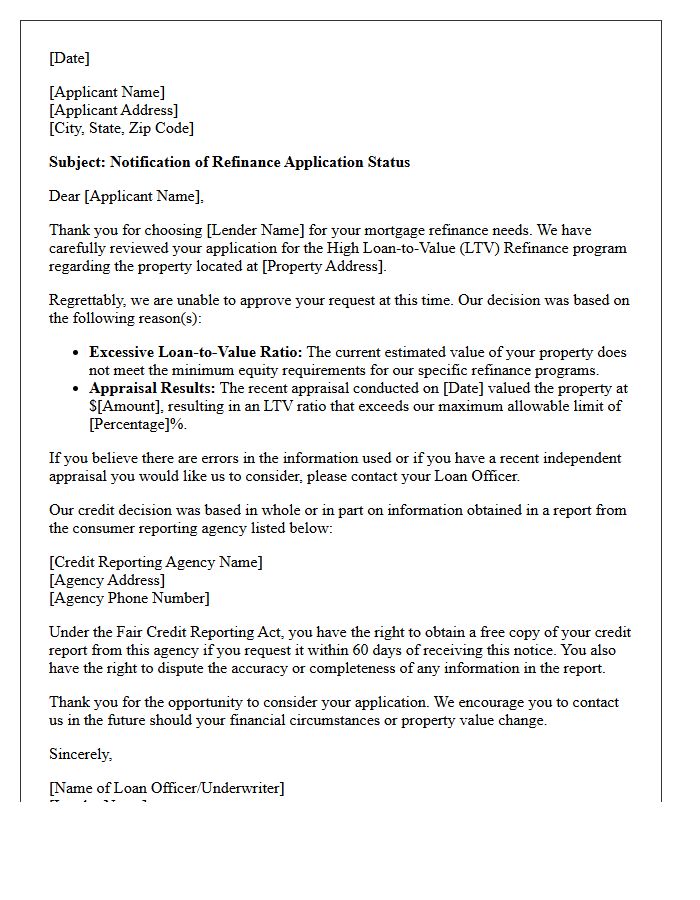

High Loan-to-Value Refinance Application Denial Letter

A High Loan-to-Value Refinance Application Denial Letter is a formal notice sent by lenders when a homeowner's mortgage balance exceeds the property's current market worth. This negative equity situation often prevents traditional refinancing. The letter must legally outline specific reasons for the rejection, such as credit score issues or insufficient income. Understanding these factors is crucial for exploring alternative government programs like HIRO or Fannie Mae RefiNow, which are designed to assist borrowers with limited equity in securing lower interest rates despite high LTV ratios.

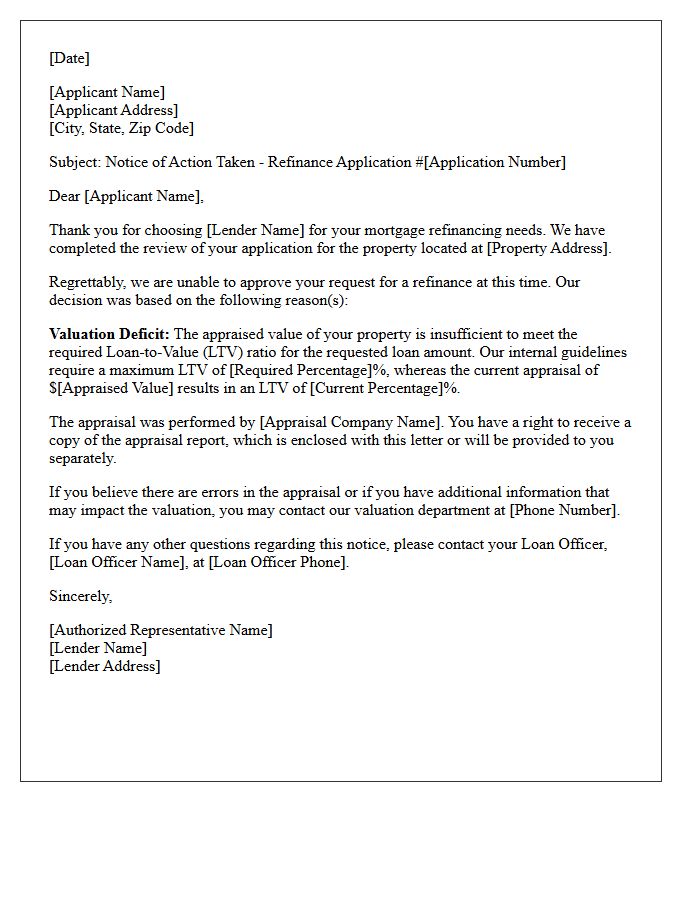

Valuation Deficit Refinance Denial Letter

A Valuation Deficit Refinance Denial Letter informs a borrower that their application was rejected because the appraised property value is lower than the amount required to secure the loan. This valuation gap typically occurs when the current market data does not support the expected equity levels. Receving this notice means the loan-to-value ratio exceeds lender limits, making the risk unacceptable. To move forward, homeowners must either appeal the appraisal, pay down the principal balance with cash, or wait for market conditions to improve before reapplying for refinancing.

Why was my refinance application denied due to being underwater on my mortgage?

Lenders typically deny refinance applications when the loan-to-value (LTV) ratio exceeds 100%, meaning you owe more than the home is currently worth. Most conventional loans require a minimum amount of equity to qualify for new financing terms.

What should I do if I receive a denial letter for an underwater mortgage refinance?

Review the "Statement of Credit Denial" or "Adverse Action Notice" to identify the specific appraised value and LTV requirements. You should then explore specialized government-backed programs like the High LTV Refinance Option (HIRO) or the Freddie Mac Enhanced Relief Refinance (FMERR) designed for negative equity situations.

Can I still refinance if my home value is lower than my loan balance?

Yes, though standard refinancing is difficult, you may qualify for relief programs if your loan is owned by Fannie Mae or Freddie Mac. These programs allow homeowners to refinance even with little to no equity, provided they have a history of on-time payments.

Does a refinance denial for negative equity hurt my credit score?

The denial itself does not impact your credit score. However, the hard credit inquiry performed during the application process may cause a temporary, minor dip in your score, typically lasting for one year.

What are the alternatives to refinancing if I am underwater and facing denial?

If you are denied due to being underwater, alternatives include a loan modification to lower interest rates, applying for a mortgage assistance program, or waiting for local property values to increase to improve your loan-to-value ratio.

Comments