An escrow account shortage occurs when your property taxes or insurance premiums increase beyond your current balance. This notification informs homeowners that their monthly mortgage payments must adjust to cover the deficit and maintain a required minimum cushion. Understanding these adjustments is essential for managing your home finances effectively. To simplify your communication, below are some ready to use template.

Image cover: Managing Escrow Account Shortages: Official Notification Templates and Samples

Letter Samples List

- Initial Notification of Escrow Account Shortage Letter

- Annual Escrow Analysis Shortage Notification Letter

- Property Tax Escrow Shortage Warning Letter

- Homeowners Insurance Escrow Deficiency Notice Letter

- Escrow Shortage Payment Option Election Letter

- Final Notice of Escrow Account Shortage Letter

- Escrow Account Negative Balance Alert Letter

- Mortgage Escrow Shortage Explanation Letter

- Adjusted Monthly Payment Escrow Shortage Letter

- Lump Sum Escrow Shortage Payment Request Letter

- Post-Disbursement Escrow Account Shortage Letter

- Delinquent Escrow Shortage Action Required Letter

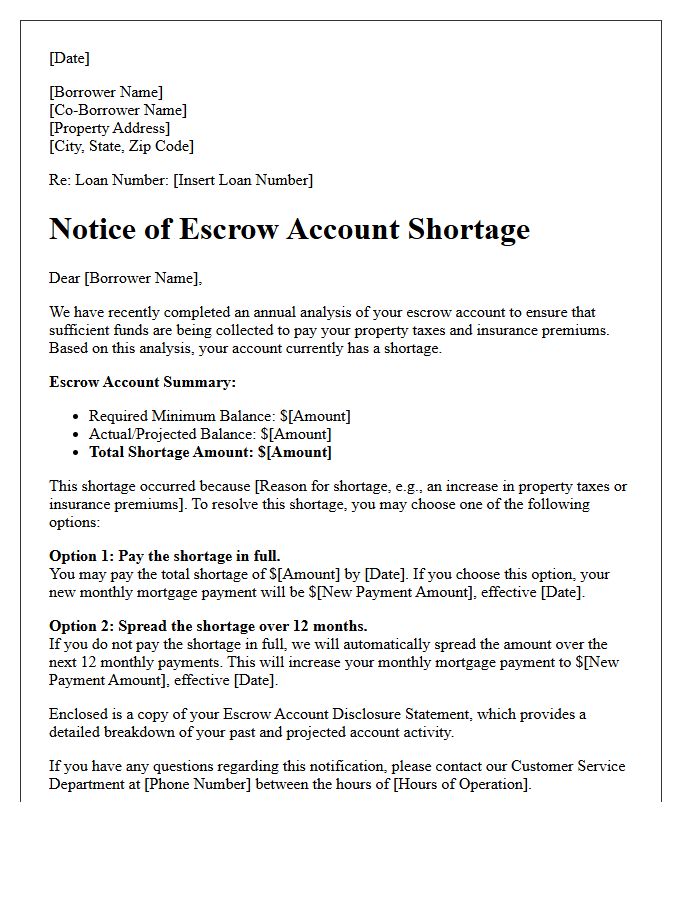

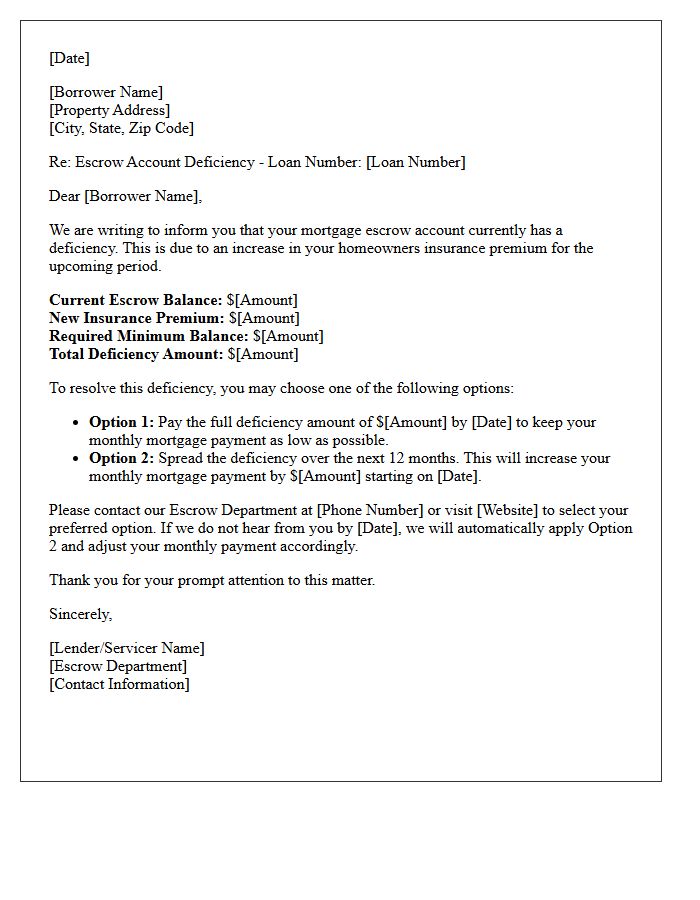

Initial Notification of Escrow Account Shortage Letter

An Escrow Account Shortage Letter is a formal notice informing homeowners that their property tax or insurance payments exceeded the funds available. This shortage occurs when escrow disbursements rise, leaving a deficit in the account balance. To resolve this, lenders typically offer options: paying the total amount upfront or spreading the cost across future monthly mortgage payments. Reviewing your annual escrow analysis is essential to understand these fluctuations and adjust your budget accordingly to maintain financial stability and avoid unexpected payment increases.

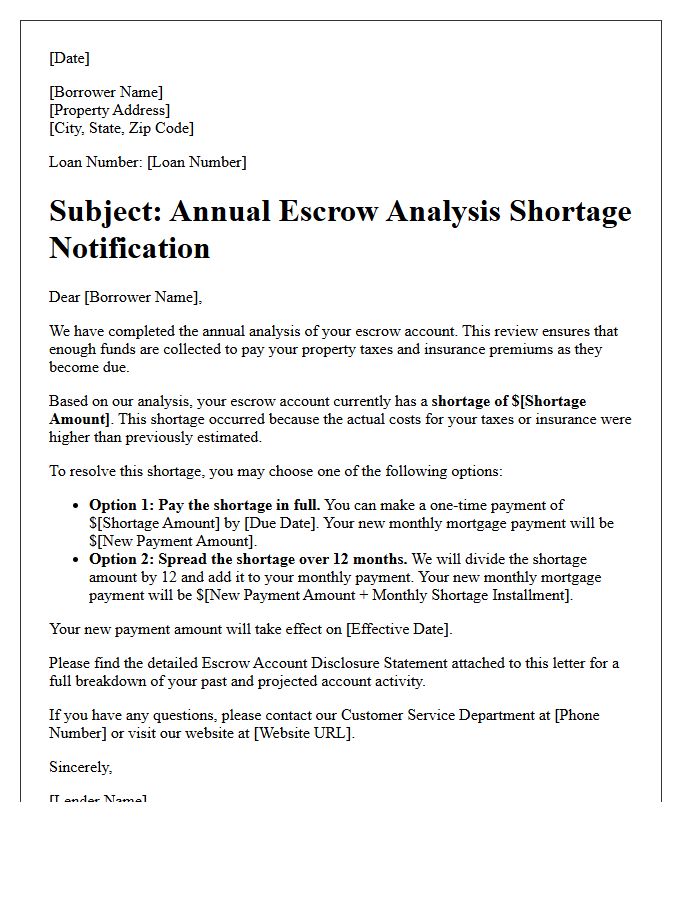

Annual Escrow Analysis Shortage Notification Letter

An Annual Escrow Analysis Shortage Notification Letter informs homeowners that their current escrow balance is insufficient to cover projected property taxes and insurance premiums. This occurs when actual expenses exceed the previous year's estimates. Your monthly mortgage payment will likely increase to cover the deficit and rebuild the required reserve. You can usually resolve a shortage through a one-time lump sum payment or by spreading the cost across twelve months. Reviewing this statement ensures your impound account remains adequately funded to prevent future payment shocks or coverage lapses.

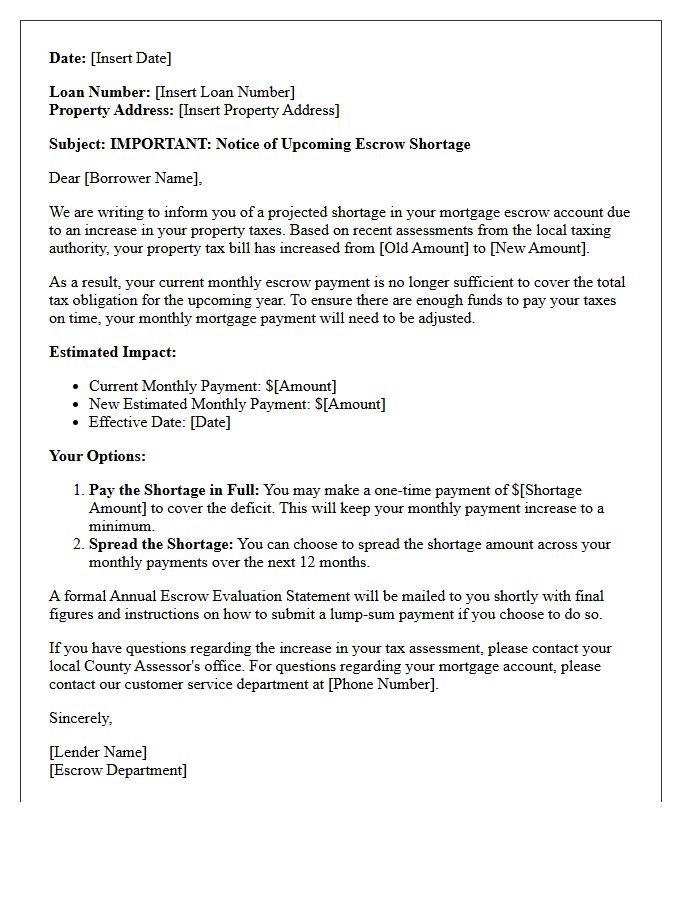

Property Tax Escrow Shortage Warning Letter

Receiving a Property Tax Escrow Shortage Warning Letter means your monthly payments were insufficient to cover rising property taxes or insurance premiums. This escrow deficiency occurs when your lender pays more out of your account than projected. You typically have two options: pay the full shortage amount as a lump sum or spread the balance across your future monthly mortgage payments. Ignoring this notice will lead to a mandatory increase in your monthly housing costs to ensure your tax obligations remain fully funded and current.

Homeowners Insurance Escrow Deficiency Notice Letter

A homeowners insurance escrow deficiency notice occurs when your escrow account lacks sufficient funds to cover rising insurance premiums. This shortfall often results from annual rate increases or updated property assessments. When you receive this letter, your mortgage servicer typically provides two options: pay the shortage in a single lump sum or spread the cost over twelve months through higher monthly mortgage payments. Promptly addressing this notice is essential to avoid financial penalties or unexpected spikes in your monthly housing costs while ensuring your property remains fully protected.

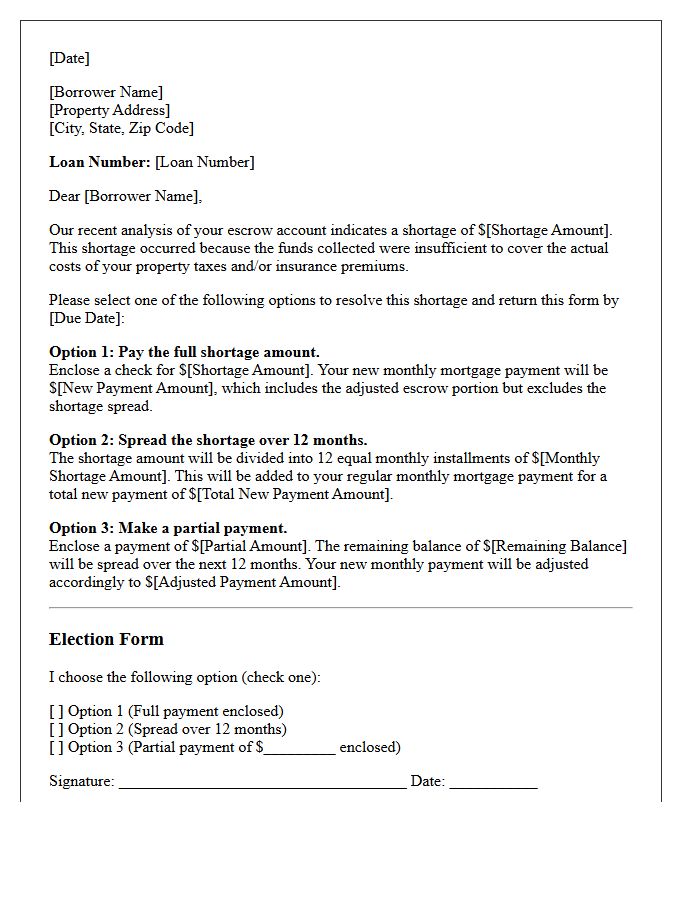

Escrow Shortage Payment Option Election Letter

An Escrow Shortage Payment Option Election Letter informs homeowners that their escrow account lacks sufficient funds to cover upcoming property taxes or insurance premiums. This document outlines specific repayment options to resolve the deficit. You can typically choose to pay the shortage amount in a single lump sum to keep monthly payments stable or spread the balance over the next twelve months, which will increase your monthly mortgage payment. Promptly returning this election form ensures your lender applies your preferred method for balancing the account and maintaining necessary coverage.

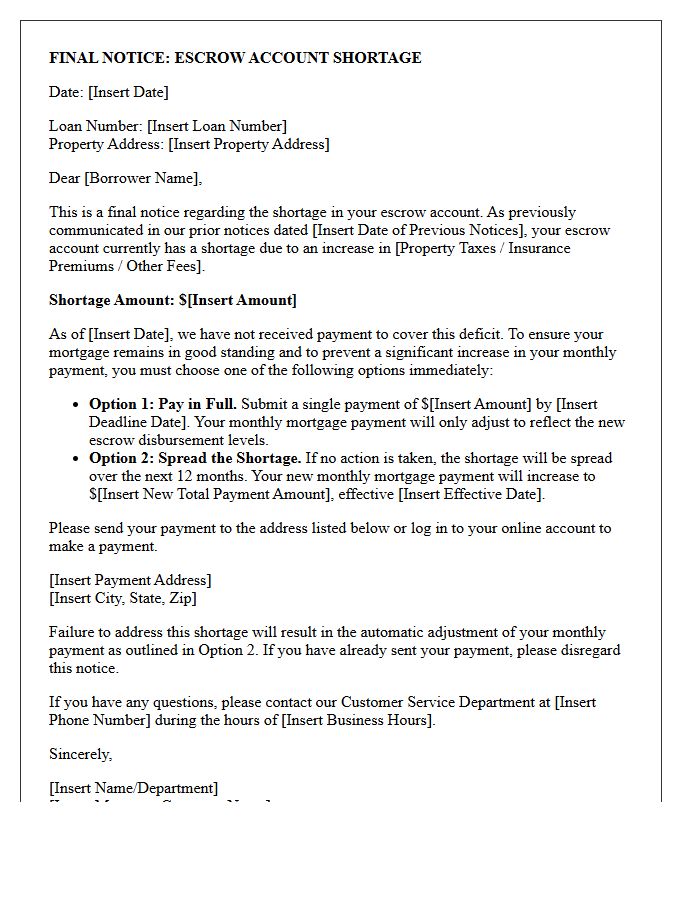

Final Notice of Escrow Account Shortage Letter

A Final Notice of Escrow Account Shortage Letter is a critical notification from your mortgage servicer indicating that your escrow balance is insufficient to cover projected property taxes and insurance premiums. This occurs due to tax hikes or rising insurance costs. To resolve the escrow deficiency, homeowners must typically choose between paying a one-time lump sum or increasing their monthly mortgage payment. Promptly addressing this notice is essential to avoid significant payment fluctuations and ensure your financial obligations are met to maintain continuous property coverage and tax compliance.

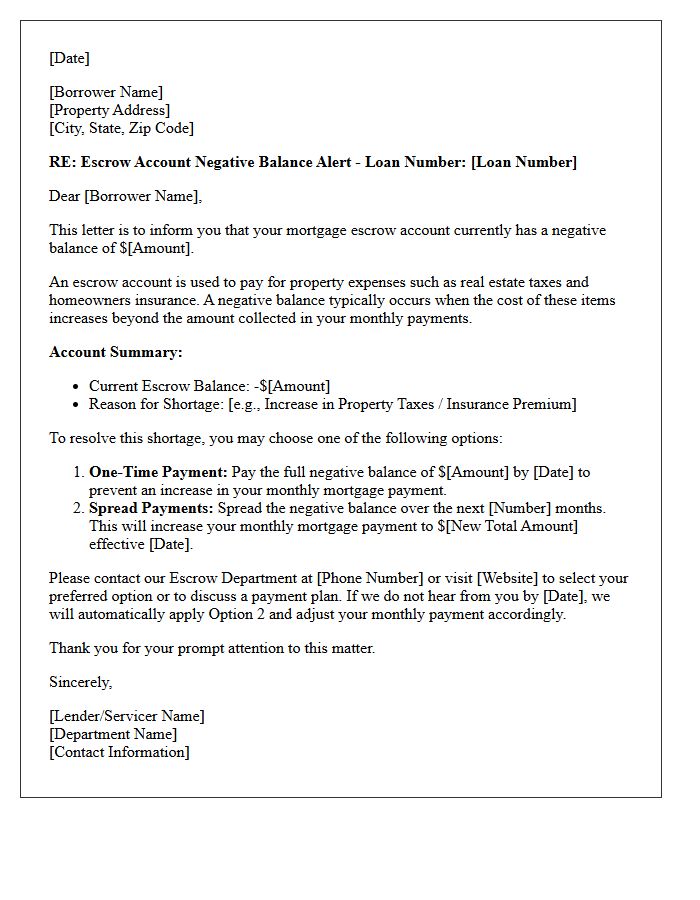

Escrow Account Negative Balance Alert Letter

An Escrow Account Negative Balance Alert Letter notifies homeowners of a shortage in their mortgage impound account. This typically occurs when property taxes or insurance premiums increase beyond previous estimates. The notice explains your payment options, such as providing a one-time lump sum to cover the deficit or spreading the cost across future monthly installments. It is crucial to address this alert promptly to avoid significant mortgage payment hikes or potential coverage lapses. Reviewing your annual escrow analysis helps verify that all disbursements are accurate and reflect current tax assessments.

Mortgage Escrow Shortage Explanation Letter

A mortgage escrow shortage explanation letter notifies homeowners when their escrow account contains insufficient funds to cover rising property taxes or insurance premiums. This shortage typically occurs due to annual tax assessments or increased insurance rates. The letter details your new monthly payment and offers options, such as paying the deficiency in a single lump sum or spreading the balance over the next twelve months. Reviewing this document is essential to understanding why your mortgage payment increased and ensuring your future tax and insurance obligations are fully funded.

Adjusted Monthly Payment Escrow Shortage Letter

An Escrow Shortage Letter notifies homeowners that their property taxes or insurance premiums increased beyond previous estimates. This document outlines your new Adjusted Monthly Payment, calculated to cover the deficit and maintain a required minimum balance. To resolve the gap, lenders typically offer options: pay the shortage amount in a single lump sum or spread the cost across your future monthly installments. Reviewing this annual analysis is essential to understand why your mortgage costs rose and to ensure your escrow account remains adequately funded for upcoming bills.

Lump Sum Escrow Shortage Payment Request Letter

A Lump Sum Escrow Shortage Payment Request Letter is a formal notice sent to a mortgage lender to resolve an underfunded escrow account. This document specifies your intent to pay the full deficit amount in a single installment rather than increasing monthly mortgage payments. Providing this written request ensures your escrow balance remains stable and helps stabilize your monthly budget by avoiding future payment spikes. Always include your loan number and attach the payment to guarantee accurate processing and proper account reconciliation.

Post-Disbursement Escrow Account Shortage Letter

A Post-Disbursement Escrow Account Shortage Letter notifies homeowners that their escrow balance is insufficient to cover future property taxes or insurance premiums. This usually occurs after an annual escrow analysis reveals increased costs. The letter outlines repayment options, such as a one-time lump sum payment or spreading the deficit over monthly mortgage installments. Understanding this notice is essential for budgeting, as it directly impacts your total monthly housing expense and ensures your required obligations remain fully funded throughout the year.

Delinquent Escrow Shortage Action Required Letter

A Delinquent Escrow Shortage Action Required Letter is a formal notice from your mortgage servicer indicating that your escrow account has a negative balance. This occurs when property taxes or insurance premiums increase beyond previous estimates. To resolve this, you must take immediate action by choosing to pay the deficiency in a lump sum or through increased monthly mortgage payments. Failure to address this shortage can lead to payment delinquency or unintended changes to your loan terms. Promptly reviewing the breakdown ensures your account remains in good standing.

What is an escrow account shortage?

An escrow account shortage occurs when the balance in your escrow account falls below the minimum required amount to cover your property taxes and homeowners insurance premiums. This usually happens if your tax assessments or insurance rates increase unexpectedly during the year.

Why did I receive a notification of escrow account shortage?

You received this notification because your annual escrow analysis revealed that your current monthly payments are insufficient to cover upcoming tax and insurance bills. Lenders are required to notify you when your account balance does not meet the minimum reserve requirements mandated by federal law.

How can I pay my escrow shortage?

You generally have two options: you can pay the full shortage amount as a one-time lump sum to keep your monthly mortgage payment lower, or you can spread the shortage amount over 12 months, which will be added to your regular monthly mortgage payment.

Will my monthly mortgage payment increase after an escrow shortage?

Yes, your monthly payment will likely increase. Even if you pay the shortage in full, your monthly payment may rise to cover the higher projected costs of taxes and insurance for the upcoming year to prevent a future shortage.

How is a shortage different from an escrow deficiency?

A shortage means your account balance is positive but below the required minimum reserve level. A deficiency occurs when your escrow account has a negative balance because the lender had to advance their own funds to pay your tax or insurance bills.

Comments