Receiving an Overdraft Fee Assessment Notice can be stressful, as it indicates your bank account has a negative balance. This official notification details the specific charges applied when transactions exceed your available funds. Understanding these notices is essential for managing your finances and avoiding future penalties. To help you respond effectively, below are some ready to use template.

Image cover: Professional Templates for Overdraft Fee Assessment Notices

Letter Samples List

- Initial Overdraft Fee Assessment Notice Letter

- Standard Account Overdraft Fee Notification Letter

- Insufficient Funds and Overdraft Penalty Letter

- Continuous Negative Balance Overdraft Fee Letter

- Courtesy Pay Overdraft Assessment Warning Letter

- Extended Overdraft Fee Accrual Notice Letter

- Multiple Transaction Overdraft Fee Assessment Letter

- Commercial Account Overdraft Penalty Notice Letter

- Retail Banking Overdraft Fee Assessment Letter

- Tiered Overdraft Assessment and Balance Letter

- Daily Overdraft Charge Assessment Notice Letter

- Final Overdraft Fee Assessment and Closure Letter

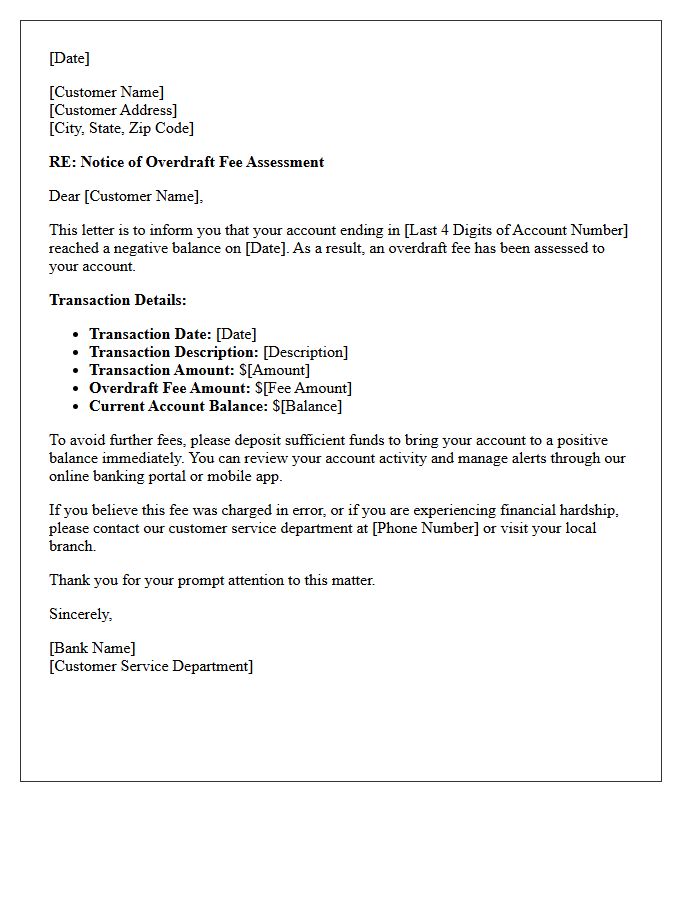

Initial Overdraft Fee Assessment Notice Letter

An Initial Overdraft Fee Assessment Notice Letter informs a customer that their account balance has dropped below zero. This formal communication details specific transaction amounts and the resulting penalties applied. It serves as a legal warning to rectify the deficit immediately to avoid further charges or account suspension. Understanding this notice is crucial for managing financial liquidity and maintaining a positive banking history. Review the document carefully to verify any potential errors and ensure you understand your bank's current overdraft protection policies and repayment timelines.

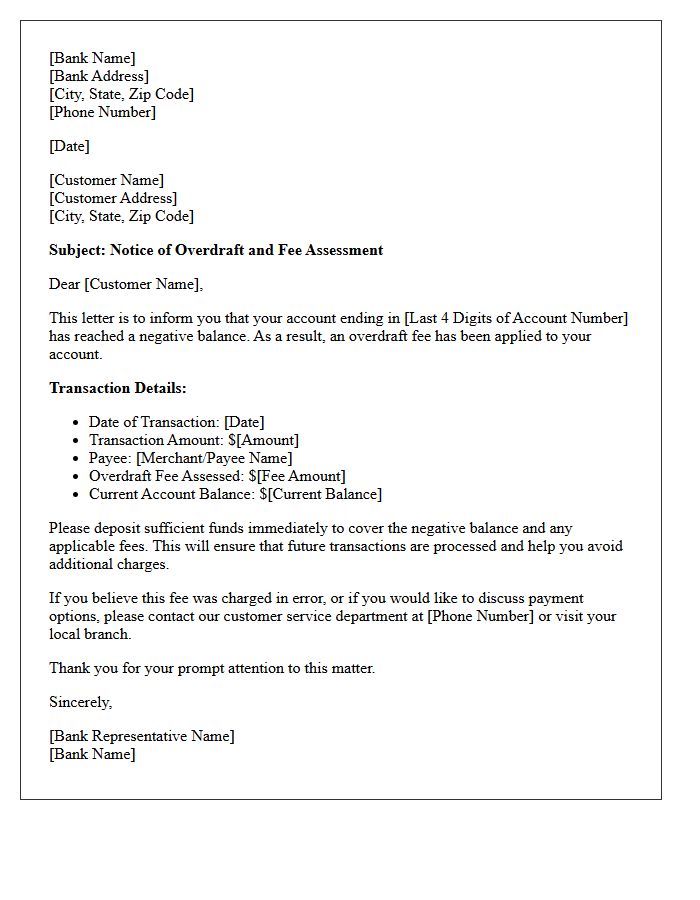

Standard Account Overdraft Fee Notification Letter

A Standard Account Overdraft Fee Notification Letter informs customers when their balance falls below zero. The most important term is the overdraft fee, which is the specific penalty charged per transaction. This letter details the transaction date, the exact overdraft amount, and any required repayment deadline to avoid further NSF fees. Understanding these notifications is crucial for financial management and preventing account suspension. Carefully review the document to ensure all banking charges are accurate and to maintain a positive balance promptly.

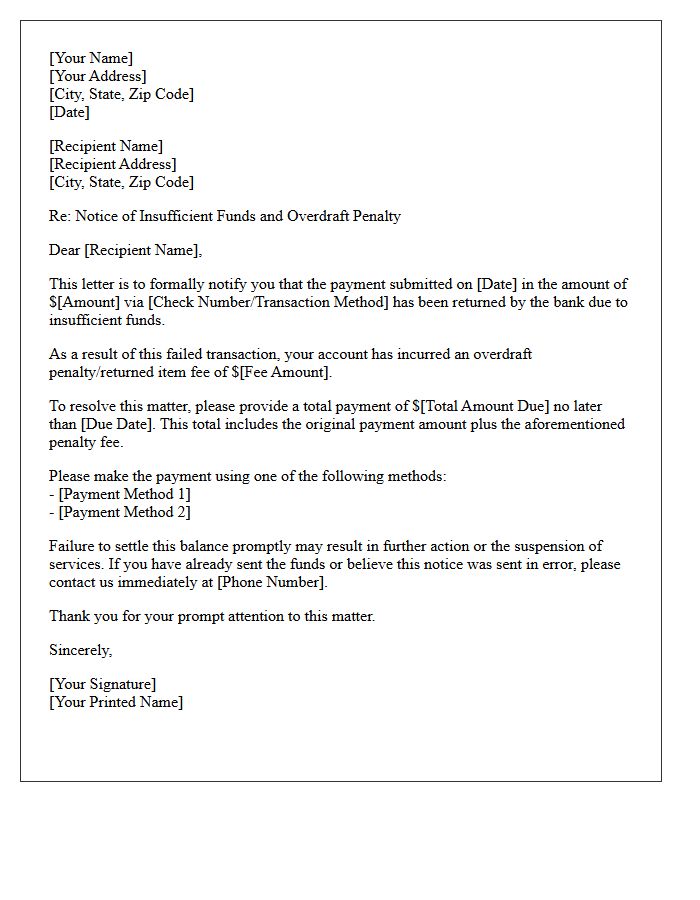

Insufficient Funds and Overdraft Penalty Letter

Receiving an overdraft penalty letter signifies your account balance dropped below zero, triggering high non-sufficient funds (NSF) fees. This notice typically demands immediate repayment of the negative balance plus penalties. To avoid further financial damage, contact your bank to negotiate a fee waiver and ensure all pending transactions are covered. Chronic insufficient funds can lead to account closure and negative reporting to ChexSystems, impacting your future banking eligibility. Always monitor your balance closely and consider linking a savings account for overdraft protection to prevent these costly automatic charges.

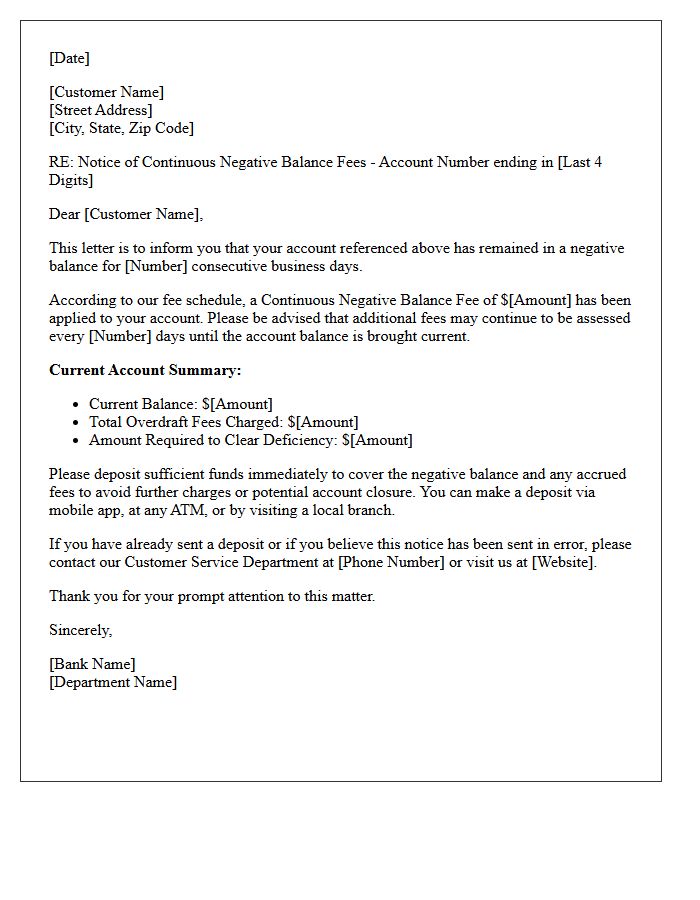

Continuous Negative Balance Overdraft Fee Letter

Receiving a Continuous Negative Balance Overdraft Fee Letter notifies you that your bank account has remained overdrawn beyond a specific grace period. Banks typically charge a recurring fee for every day or week the balance stays below zero. To stop these accumulating costs, you must deposit funds immediately to cover the overdrawn amount and any accrued penalties. Ignoring this notice can lead to account closure and negative reports to credit bureaus, significantly impacting your future financial standing and ability to open new banking accounts.

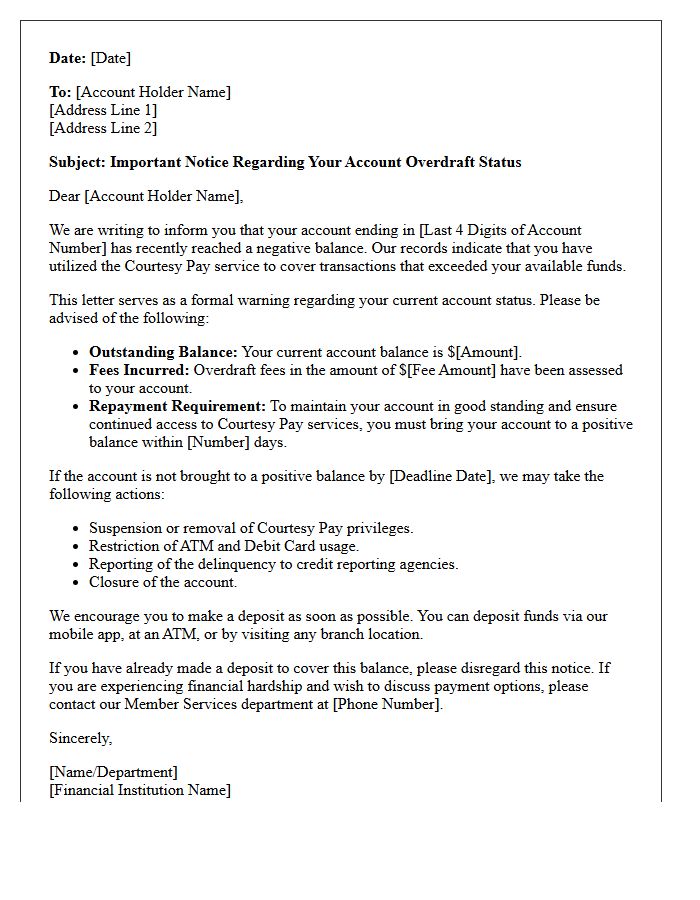

Courtesy Pay Overdraft Assessment Warning Letter

A Courtesy Pay Overdraft Assessment Warning Letter serves as a critical notice that your account has reached a negative balance. This document informs you that the financial institution covered a transaction exceeding your available funds, resulting in an overdraft fee. It is essential to deposit funds immediately to restore a positive balance and avoid further penalties. Receiving this letter is a signal to review your spending habits and account management to prevent future account restrictions or the eventual closure of your banking services due to unpaid balances.

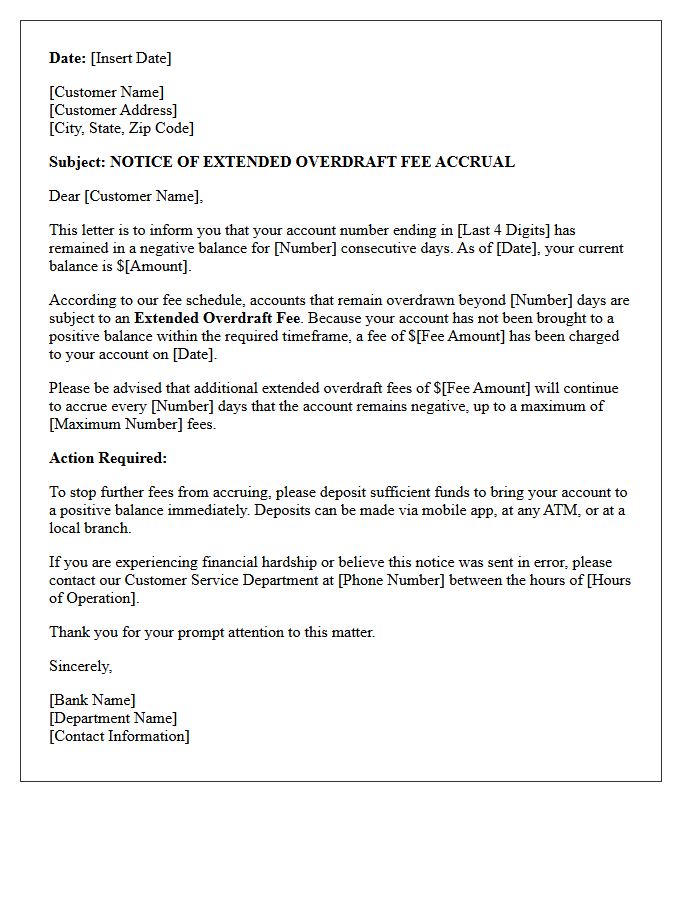

Extended Overdraft Fee Accrual Notice Letter

An Extended Overdraft Fee Accrual Notice Letter informs customers that their bank account has remained in a negative balance for several consecutive days. This document serves as a final warning before additional sustained overdraft fees are applied. To avoid these recurring charges, you must deposit sufficient funds to cover the deficit immediately. Reviewing this notice is critical for maintaining financial health and preventing further penalties. Understanding the specific grace period and repayment terms outlined in the letter can help you restore a positive balance and protect your credit standing.

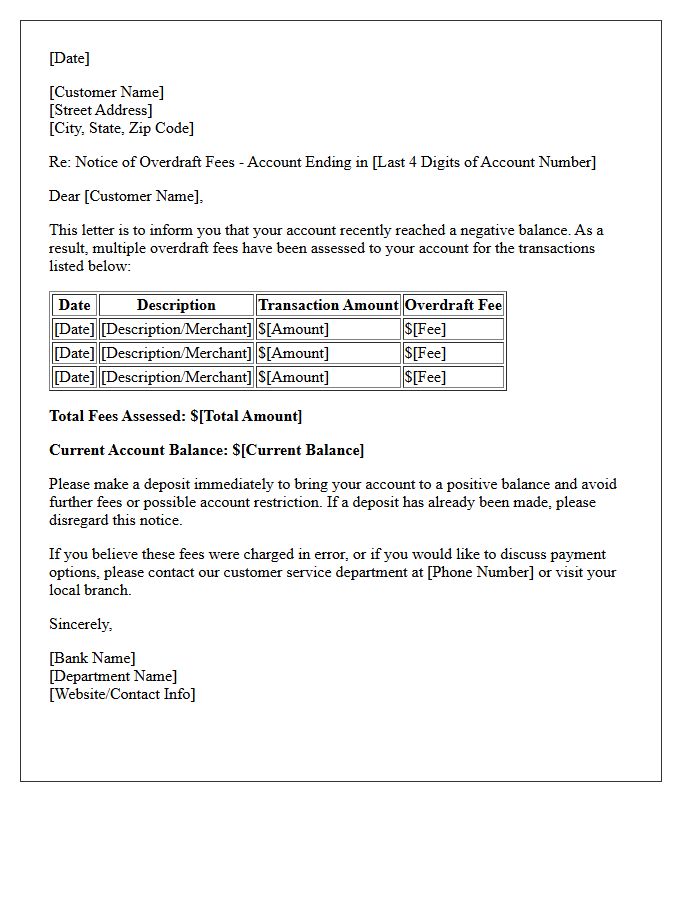

Multiple Transaction Overdraft Fee Assessment Letter

A Multiple Transaction Overdraft Fee Assessment Letter notifies account holders when consecutive overdraft charges occur due to insufficient funds. This document details the specific transactions, dates, and total fees incurred during a billing cycle. It is crucial to review these letters to identify repayment obligations and prevent further financial penalties. Understanding this notice helps consumers monitor automated clearing house activity and manage their balance effectively to avoid recurring service fees. Prompt action after receiving this letter can often lead to account stabilization and potential fee waivers through bank mediation.

Commercial Account Overdraft Penalty Notice Letter

A Commercial Account Overdraft Penalty Notice Letter is a formal notification issued by a bank when a business account carries a negative balance. This document outlines specific overdraft fees, the total amount owed, and the deadline for repayment to avoid further penalties. To maintain financial stability, it is crucial to reconcile the account immediately to prevent account suspension or negative reporting to credit agencies. Understanding these notices helps businesses manage cash flow effectively and ensures continued access to essential banking services and lines of credit.

Retail Banking Overdraft Fee Assessment Letter

A Retail Banking Overdraft Fee Assessment Letter is a formal notification sent when your account balance falls below zero. This document details the specific charges applied for covering a transaction without sufficient funds. It is crucial to review the Effective Date and the exact amount deducted to avoid further financial penalties. Under federal regulations, banks must provide these notices to ensure transparency. Understanding this letter helps you manage your available balance effectively and allows you to dispute any unauthorized fees or opt out of future overdraft protection services promptly.

Tiered Overdraft Assessment and Balance Letter

A Tiered Overdraft Assessment is a formal notification sent by banks when an account balance falls below zero. This letter details specific fees applied based on the severity and frequency of the overdraft. Understanding this document is crucial because it outlines the tiered pricing structure, where costs often increase with consecutive occurrences. Reviewing your Balance Letter helps you track the total deficit and identify required deposits to avoid further penalties. Monitoring these alerts is the most effective way to manage liquidity risks and maintain a healthy financial standing with your institution.

Daily Overdraft Charge Assessment Notice Letter

A Daily Overdraft Charge Assessment Notice Letter serves as a formal notification that your bank account has a negative balance. This document informs you that recurring fees are being applied for each day the account remains overdrawn. It is critical to deposit funds immediately to stop these accumulating costs. Reviewing this notice helps you monitor your financial health, understand specific penalty structures, and avoid further banking penalties or potential account closure. Always contact your financial institution promptly to discuss fee waivers or repayment options.

Final Overdraft Fee Assessment and Closure Letter

A Final Overdraft Fee Assessment and Closure Letter serves as formal notice that your bank is terminating your account relationship due to persistent negative balances. This document outlines the total outstanding debt, including accumulated overdraft fees, and provides a strict deadline for repayment. It is crucial to settle this balance immediately, as failure to comply often leads to your information being reported to ChexSystems. This can severely damage your banking history and prevent you from opening new accounts at other financial institutions in the future.

What is an Overdraft Fee Assessment Notice?

An Overdraft Fee Assessment Notice is an official notification sent by a financial institution to inform an account holder that a transaction has exceeded their available balance, resulting in a formal service charge or penalty fee.

Why did I receive an Overdraft Fee Assessment Notice?

You received this notice because a payment, withdrawal, or electronic transfer was processed against your account when funds were insufficient, triggering the bank's automated overdraft protection or standard fee policy.

How much is the typical charge listed on an Overdraft Fee Assessment Notice?

While costs vary by bank, the average fee listed on a notice typically ranges between $25 and $35 per transaction. The notice will detail the specific amount deducted from your balance for the identified incident.

Can I dispute an Overdraft Fee Assessment Notice?

Yes, you can dispute a fee by contacting your bank's customer service department. Banks may offer a one-time courtesy waiver or reverse the fee if the assessment resulted from a bank error or a delayed deposit.

How can I prevent receiving Overdraft Fee Assessment Notices in the future?

To avoid future notices, you can opt out of overdraft coverage, set up low-balance mobile alerts, link a savings account for backup transfers, or maintain a larger financial buffer in your primary checking account.

Comments