A Community Reinvestment Act Evaluation Letter summarizes a bank's performance in meeting local credit needs. Issued by federal regulators, these documents assess lending, investment, and service tests to ensure fair housing and economic growth within diverse neighborhoods. Understanding these reports is essential for compliance officers and community advocates. To help you draft professional correspondence regarding these reviews, below are some ready to use template.

Image cover: Comprehensive Guide to Community Reinvestment Act Evaluation Templates and Sample Letters

Letter Samples List

- Community Reinvestment Act Outstanding Performance Evaluation Letter

- Banking Institution Public Comment Acknowledgment Letter

- Community Reinvestment Act Strategic Plan Approval Notification Letter

- Low-Income Neighborhood Investment Commitment Letter

- Community Development Loan Qualification Assessment Letter

- Community Reinvestment Act Examination Preliminary Findings Letter

- Branch Closure Public Notice and Justification Letter

- Moderate-Income Housing Grant Distribution Letter

- Annual Community Reinvestment Act Public File Update Confirmation Letter

- Regulatory Compliance Deficiencies Remediation Letter

- Community Reinvestment Act Needs Assessment Survey Letter

- Fair Lending Practices Joint Evaluation Letter

- Financial Institution Small Business Lending Review Letter

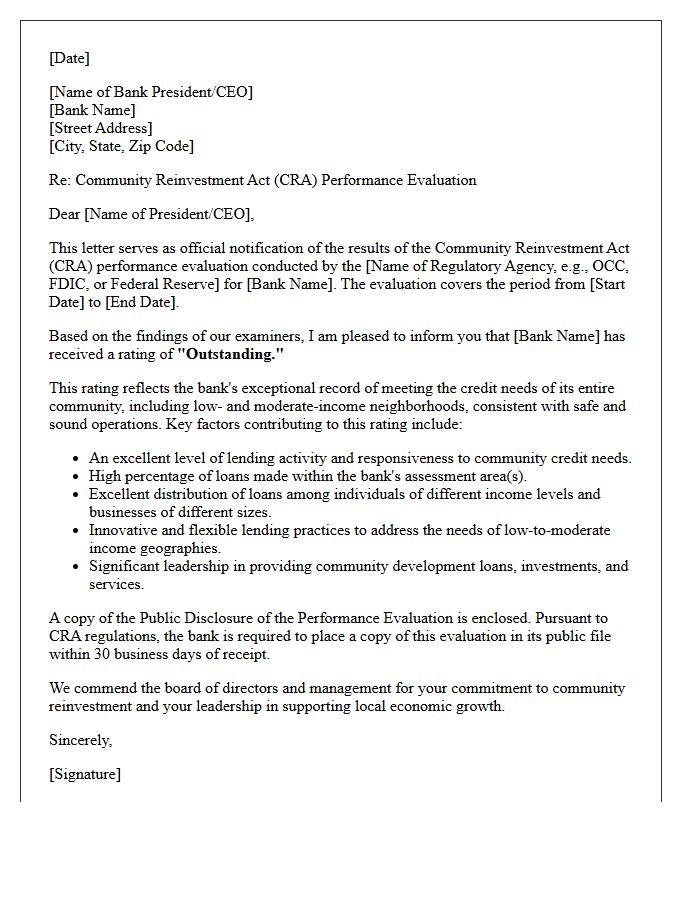

Community Reinvestment Act Outstanding Performance Evaluation Letter

A Community Reinvestment Act (CRA) Outstanding Performance Evaluation Letter is a formal document issued by federal regulators. It signifies that a financial institution has exceeded statutory requirements in meeting the credit needs of its entire community, including low-to-moderate-income neighborhoods. This highest possible rating reflects exceptional leadership in community development lending, innovative investment strategies, and accessible service delivery. Achieving this status enhances a bank's reputation and facilitates regulatory approval for future mergers and acquisitions, demonstrating a superior commitment to equitable economic growth and financial inclusion.

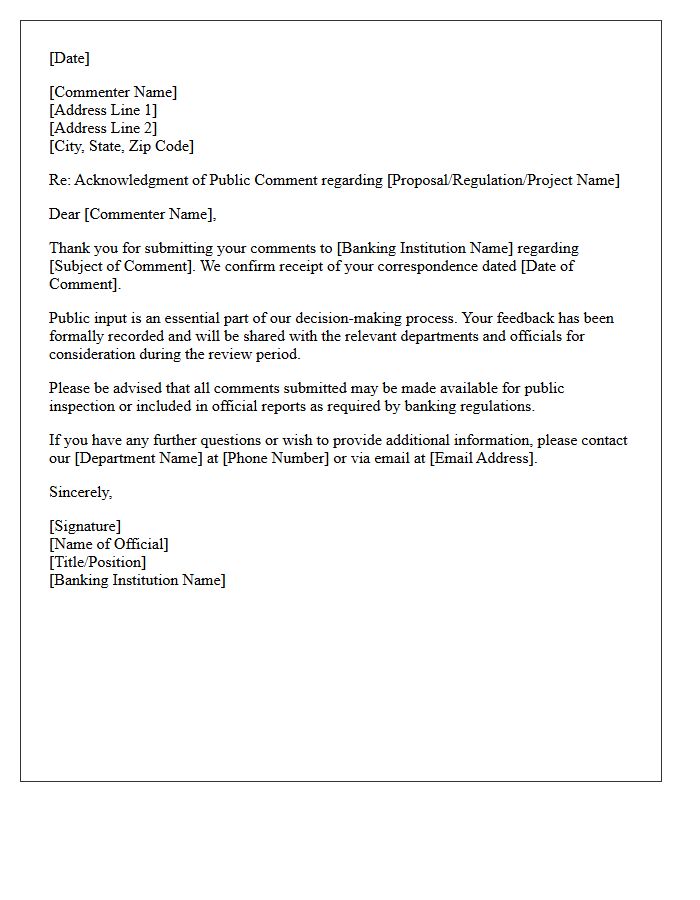

Banking Institution Public Comment Acknowledgment Letter

A Banking Institution Public Comment Acknowledgment Letter is a formal document issued by regulatory bodies or banks to confirm receipt of feedback regarding specific corporate applications. This letter ensures that stakeholder input-such as concerns about the Community Reinvestment Act or potential mergers-is officially recorded in the public file. It serves as a procedural guarantee that public sentiment will be considered during the administrative review process, maintaining transparency and regulatory accountability within the financial sector's decision-making framework.

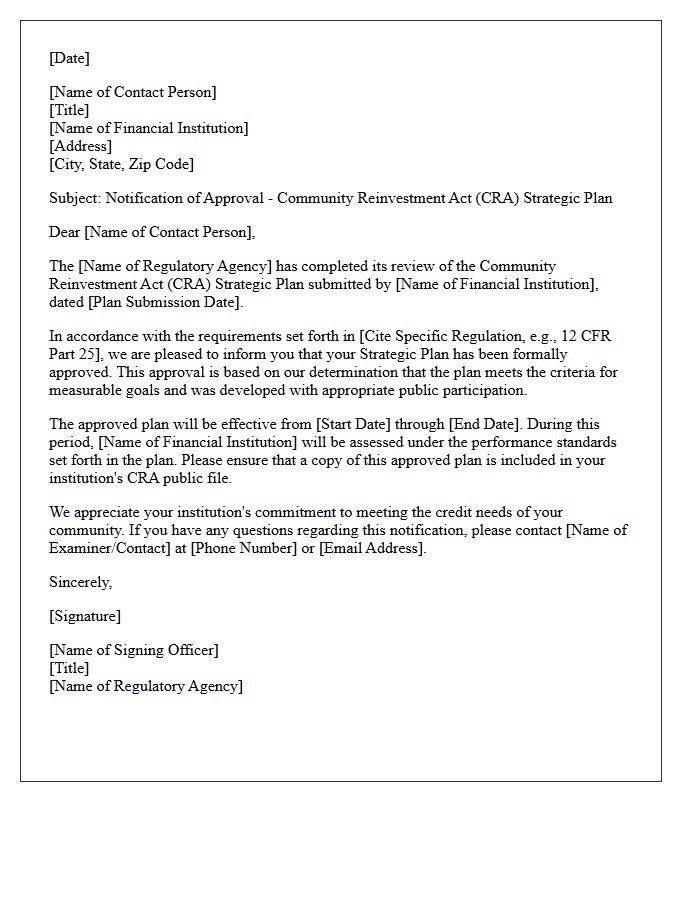

Community Reinvestment Act Strategic Plan Approval Notification Letter

The Community Reinvestment Act Strategic Plan Approval Notification Letter is a formal document issued by federal regulators confirming that a financial institution's custom performance goals have been authorized. This letter signifies that the bank's tailored compliance framework meets statutory requirements for serving its local community. Once received, the bank must operate under this approved plan for future evaluations. It is crucial for stakeholders to monitor these notifications, as they outline how the institution intends to fulfill its lending, investment, and service obligations to low-income and moderate-income neighborhoods.

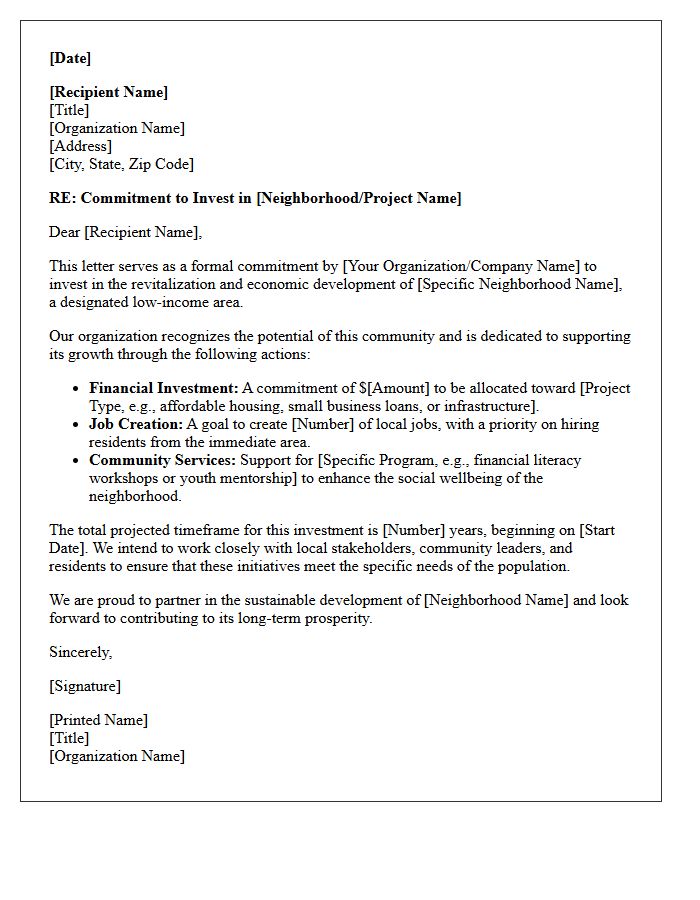

Low-Income Neighborhood Investment Commitment Letter

A Low-Income Neighborhood Investment Commitment Letter is a formal document where financial institutions pledge capital to support underprivileged communities. This agreement is vital for urban revitalization, ensuring funds are allocated for affordable housing, small business growth, and infrastructure. These letters often demonstrate compliance with the Community Reinvestment Act (CRA). By providing a roadmap for equitable development, they help bridge the wealth gap and foster economic stability. For developers and non-profits, this commitment serves as a guarantee that essential resources will be available to drive sustainable social and economic impact in high-need areas.

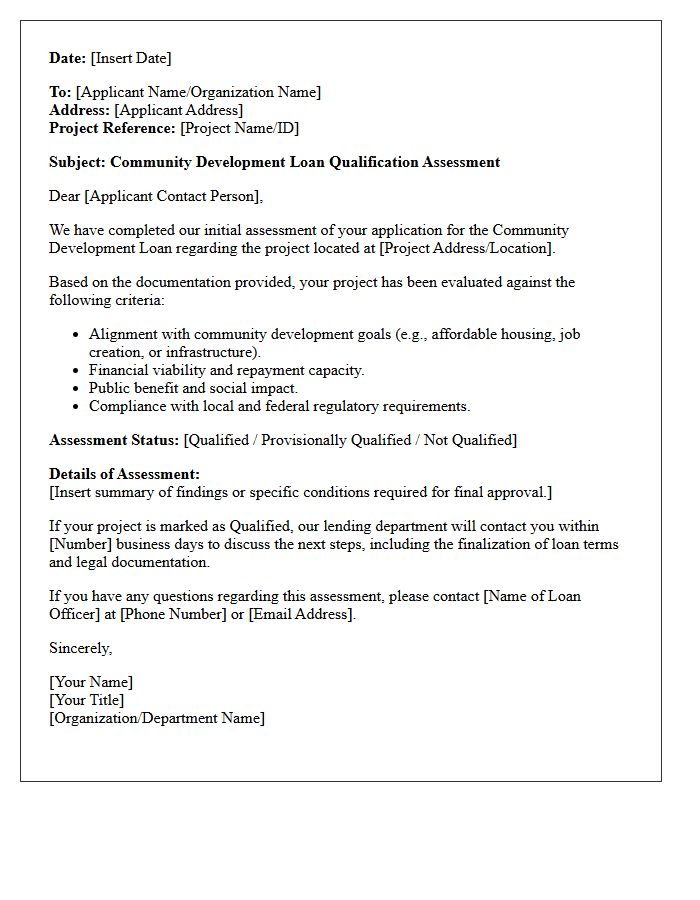

Community Development Loan Qualification Assessment Letter

A Community Development Loan Qualification Assessment Letter is a formal certification verifying that a specific financial project meets regulatory requirements for community reinvestment. It serves as documented evidence for lenders and investors, confirming that their funding supports low-to-moderate income areas or small business growth. This letter is essential for banks to receive CRA credit, ensuring their investments align with economic revitalization goals. Having this assessment simplifies the approval process, minimizes financial risk for the institution, and guarantees that capital effectively stimulates local development and sustainable community improvement.

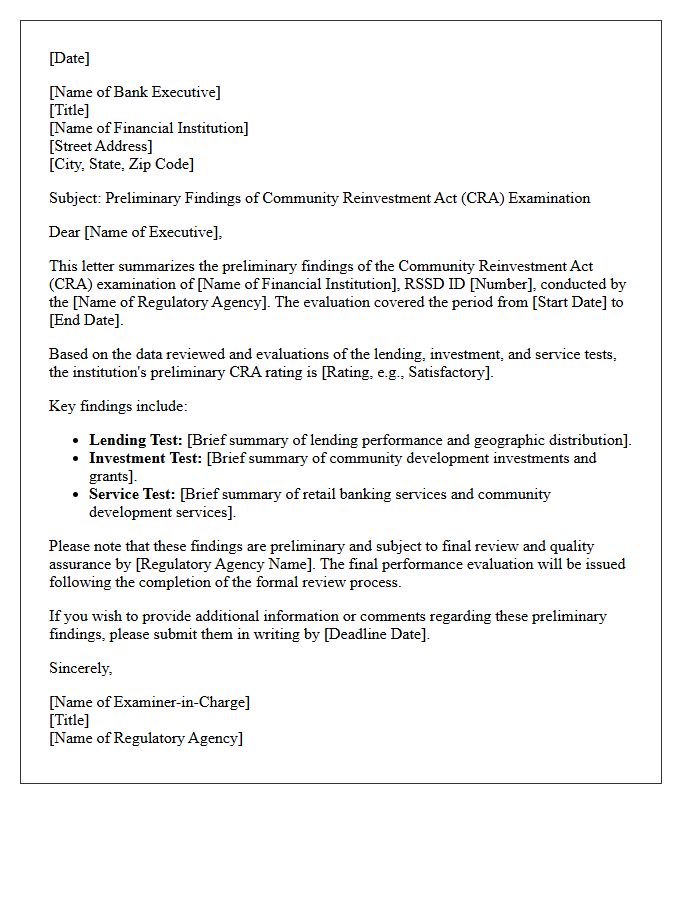

Community Reinvestment Act Examination Preliminary Findings Letter

A Community Reinvestment Act (CRA) Preliminary Findings Letter provides banks with early regulatory feedback regarding their lending, investment, and service performance. This document outlines preliminary ratings and identifies potential deficiencies before the final report is issued. It is a critical opportunity for institutions to review examiner conclusions, address compliance gaps, or provide additional data to clarify performance context. Timely analysis of these findings allows banks to proactively manage their community reinvestment obligations and ensure alignment with federal fair lending standards before official public disclosure.

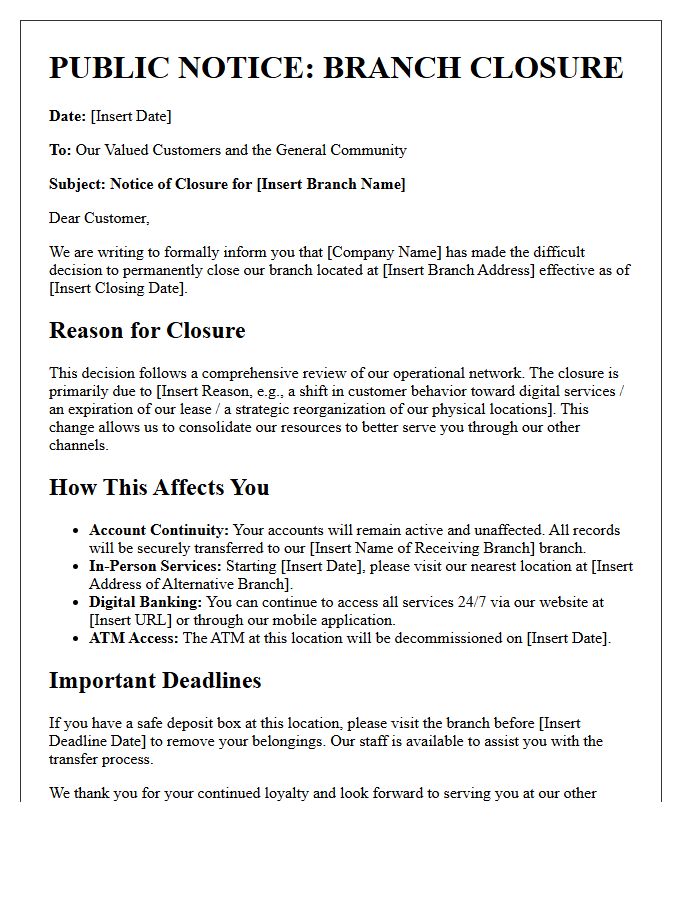

Branch Closure Public Notice and Justification Letter

A Branch Closure Public Notice and Justification Letter are regulatory requirements when a bank permanently shuts a location. This process ensures transparency for customers and stakeholders. The justification letter must provide the primary reasons for the closure, such as shifting market demographics or increased digital banking adoption. Additionally, banks must notify the relevant governing body and post a formal notice at the physical branch at least 90 days in advance. These documents are essential for maintaining regulatory compliance and ensuring customers have adequate time to transition their accounts to alternative service channels.

Moderate-Income Housing Grant Distribution Letter

A Moderate-Income Housing Grant Distribution Letter is a formal notification confirming the allocation of financial assistance to eligible recipients. This document specifies the grant amount, approved usage, and mandatory compliance terms for affordable housing initiatives. It serves as legal proof of funding, outlining disbursement schedules and reporting requirements to ensure transparency. Recipients must carefully review the eligibility criteria and deadlines mentioned to maintain their qualification status and ensure the successful completion of their housing projects under the designated government or organizational program.

Annual Community Reinvestment Act Public File Update Confirmation Letter

The Annual Community Reinvestment Act Public File Update Confirmation Letter serves as vital documentation for financial institutions. It formally verifies that the bank has reviewed and updated its CRA public file in compliance with federal regulations. This file must contain current data on branch locations, services, and geographic coverage. Maintaining an accurate record is essential for demonstrating a commitment to meeting community credit needs. Regulatory agencies examine this confirmation during examinations to ensure transparency and regulatory compliance with the Community Reinvestment Act standards.

Regulatory Compliance Deficiencies Remediation Letter

A Regulatory Compliance Deficiencies Remediation Letter is a formal document addressing compliance failures identified during an audit. Its primary purpose is to outline a structured corrective action plan to resolve legal or operational gaps. This letter must detail specific timelines, responsible parties, and evidence of improvement to satisfy regulatory bodies. Failing to provide a robust response can lead to severe penalties, fines, or loss of licensure. Clear communication and transparency are vital to demonstrating a commitment to industry standards and ensuring long-term regulatory adherence.

Community Reinvestment Act Needs Assessment Survey Letter

A Community Reinvestment Act (CRA) Needs Assessment Survey Letter is a formal request from a bank to local stakeholders to identify community credit needs. This document helps financial institutions fulfill federal requirements by gathering data on affordable housing, small business support, and essential infrastructure gaps. Participating in this survey is crucial because your feedback directly influences how banks allocate community development loans and investments. Responding ensures that local voices shape the reinvestment strategies meant to revitalize low-to-moderate income neighborhoods and promote equitable economic growth within your specific region.

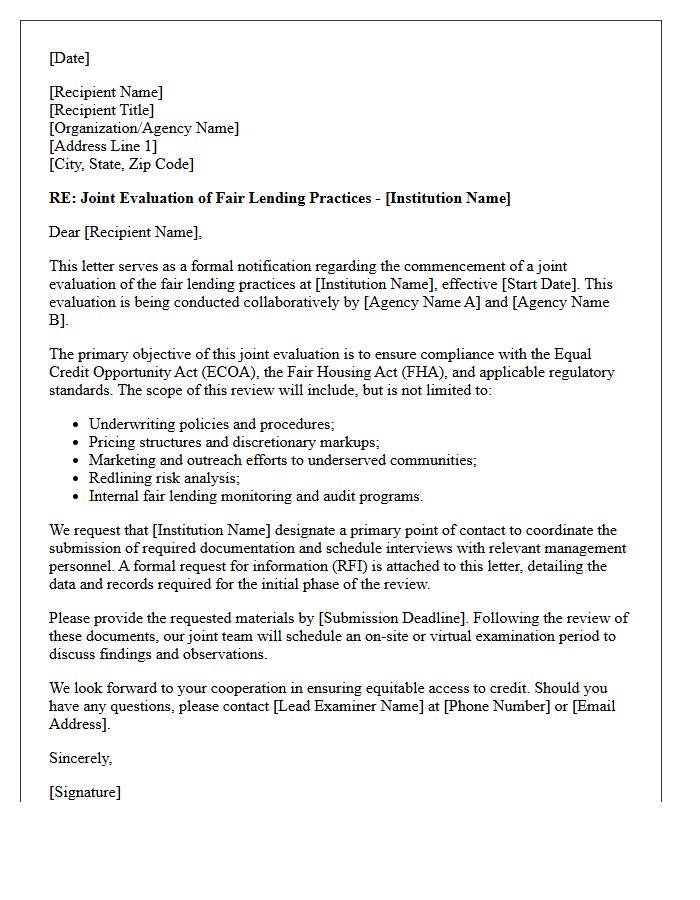

Fair Lending Practices Joint Evaluation Letter

The Fair Lending Practices Joint Evaluation Letter is a formal regulatory communication issued by federal agencies to assess a financial institution's compliance with anti-discrimination laws. It evaluates adherence to the Equal Credit Opportunity Act and the Fair Housing Act to ensure equitable access to credit. This letter identifies potential risks, such as redlining or underwriting disparities, and mandates corrective actions for identified weaknesses. Understanding this document is essential for maintaining regulatory compliance, avoiding legal penalties, and promoting inclusive financial services within the marketplace.

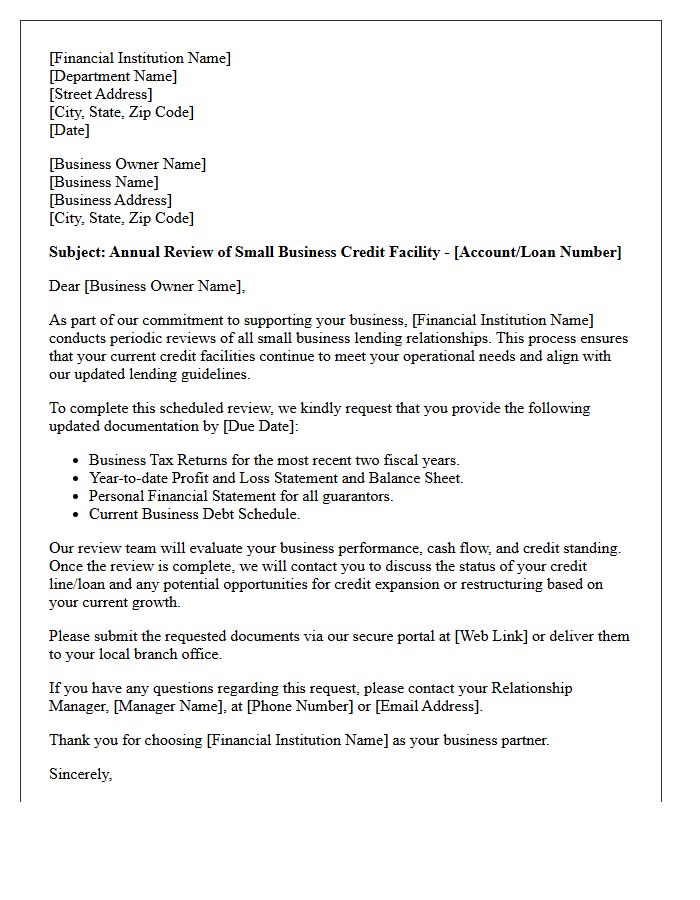

Financial Institution Small Business Lending Review Letter

A Financial Institution Small Business Lending Review Letter is a formal notification issued by regulators or internal auditors after assessing a bank's lending practices. It evaluates compliance with the Small Business Lending Rule, focusing on data accuracy, fair lending risks, and credit underwriting standards. This document highlights deficiencies in internal controls or reporting processes that require immediate corrective action. Understanding these findings is essential for maintaining regulatory standing, ensuring equitable access to capital, and avoiding potential enforcement penalties related to commercial credit distribution and data integrity.

What is a Community Reinvestment Act (CRA) Evaluation Letter?

A Community Reinvestment Act (CRA) evaluation letter, also known as a Performance Evaluation (PE), is a public document issued by federal banking regulators that assesses a financial institution's record of meeting the credit needs of its entire community, including low- and moderate-income neighborhoods.

Who issues the CRA Performance Evaluation for banks?

The evaluation letter is issued by one of three federal regulatory agencies: the Office of the Comptroller of the Currency (OCC), the Federal Deposit Insurance Corporation (FDIC), or the Federal Reserve Board, depending on the bank's charter type and regulatory oversight.

What are the different CRA ratings found in an evaluation letter?

Financial institutions are assigned one of four statutory ratings in their evaluation letter: Outstanding, Satisfactory, Needs to Improve, or Substantial Noncompliance. These ratings reflect the bank's effectiveness in lending, investment, and service within its assessment areas.

How can the public access a bank's CRA evaluation letter?

Under federal law, banks must maintain a "public file" that includes their most recent CRA evaluation letter. These documents are also available online through the searchable databases of the FFIEC (Federal Financial Institutions Examination Council) and the specific regulator's official website.

What criteria are used to determine a CRA evaluation grade?

Regulators grade institutions based on several performance tests, including the Lending Test (mortgage, small business, and consumer loans), the Investment Test (community development grants and initiatives), and the Service Test (availability of branches and community service activities).

Comments