If you discover an unauthorized transaction or a billing discrepancy on your bank statement, you must act quickly. Filing a formal Electronic Funds Transfer Error Notice Letter is the essential legal step to protect your consumer rights and recover missing funds under federal law. Timely notification ensures your financial institution investigates the issue promptly. To simplify this process, below are some ready to use templates.

Image cover: Mastering Electronic Funds Transfer Error Resolution: Essential Letter Samples and Templates

Letter Samples List

- Unauthorized Electronic Funds Transfer Dispute Letter

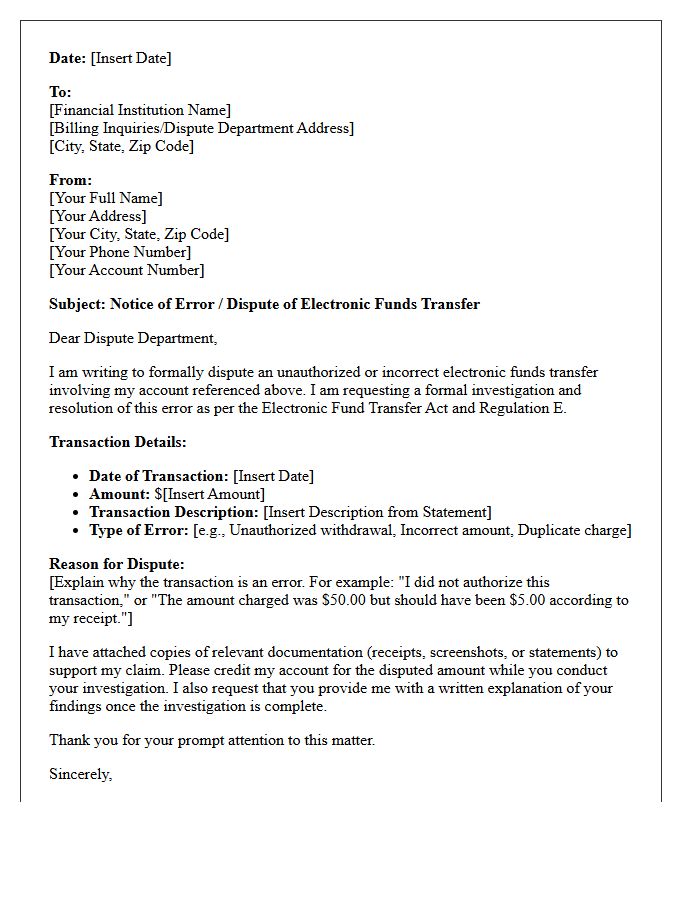

- Notice of Electronic Funds Transfer Error Letter

- Bank Investigation of Electronic Funds Transfer Error Letter

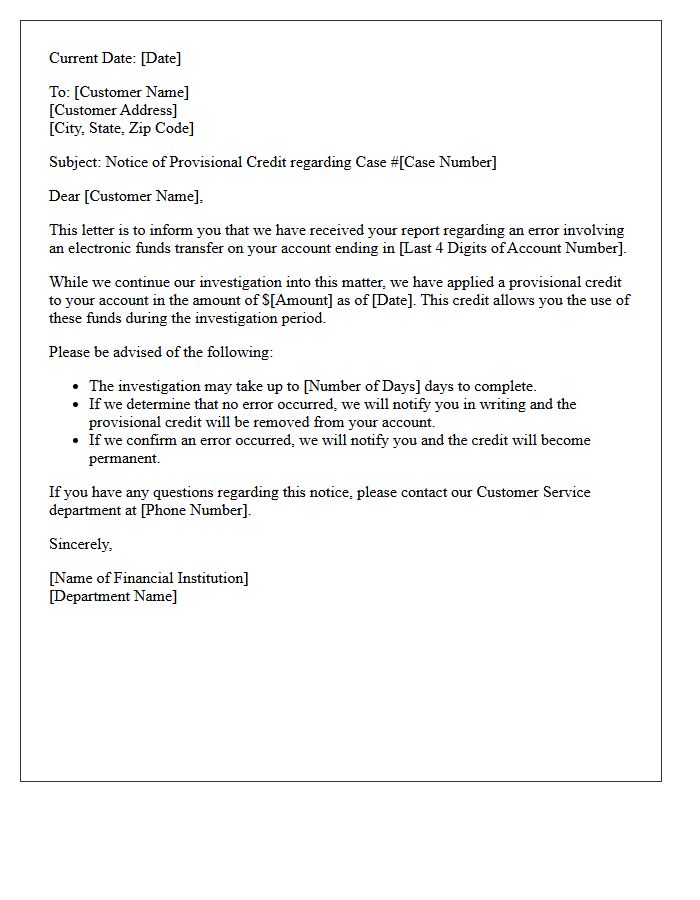

- Provisional Credit for Electronic Funds Transfer Error Letter

- Resolution of Electronic Funds Transfer Dispute Letter

- Denial of Electronic Funds Transfer Error Claim Letter

- Missing Electronic Funds Transfer Deposit Notice Letter

- Duplicate Electronic Funds Transfer Charge Dispute Letter

- Incorrect Electronic Funds Transfer Amount Notice Letter

- Confirmation of Electronic Funds Transfer Error Correction Letter

- Request for Additional Information on Electronic Funds Transfer Error Letter

- Final Decision on Electronic Funds Transfer Error Letter

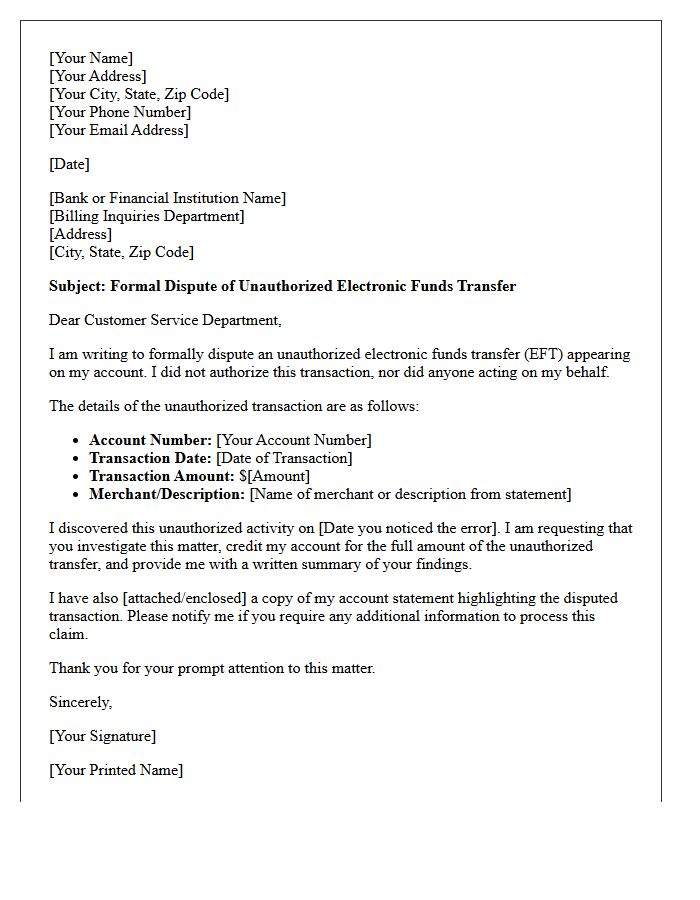

Unauthorized Electronic Funds Transfer Dispute Letter

An Unauthorized Electronic Funds Transfer Dispute Letter is a formal notice sent to your bank to report fraudulent transactions. To protect your rights under the Electronic Fund Transfer Act (Regulation E), you must submit this written claim within 60 days of the statement date. Clearly list the disputed amount, date, and merchant details. Providing this written documentation ensures the financial institution investigates the error and potentially issues a provisional credit while the case is reviewed, helping you recover stolen funds and secure your account.

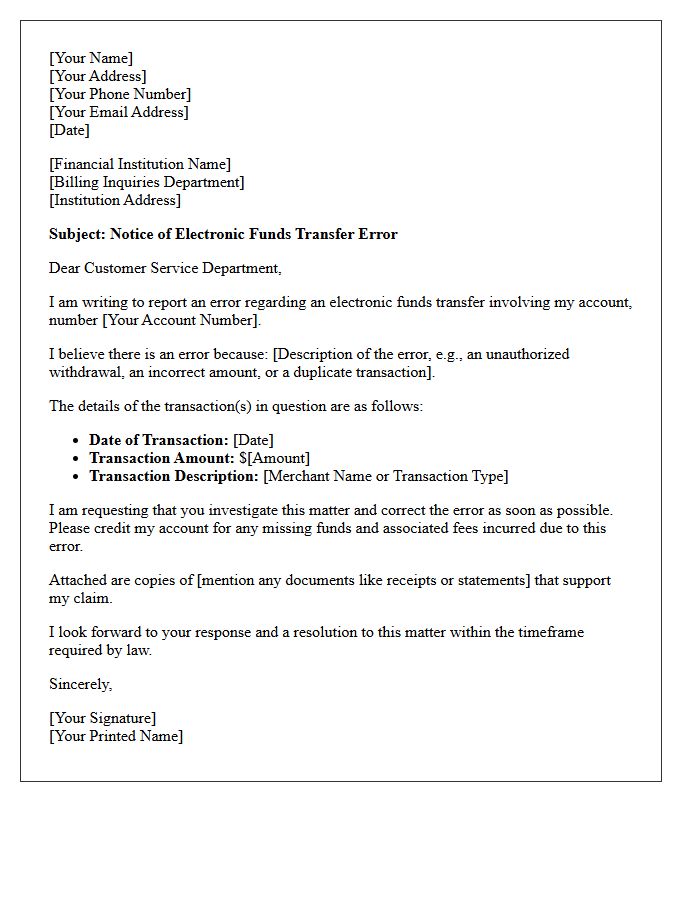

Notice of Electronic Funds Transfer Error Letter

A Notice of Electronic Funds Transfer Error Letter is a critical legal tool used to dispute unauthorized transactions or banking mistakes under the Electronic Fund Transfer Act. To protect your rights, you must notify your financial institution within 60 days of the statement date containing the error. This formal written notice should include your account details, the specific transaction date, and the disputed amount. Promptly submitting this letter mandates that the bank investigates the discrepancy and potentially provides a provisional credit while resolving the issue.

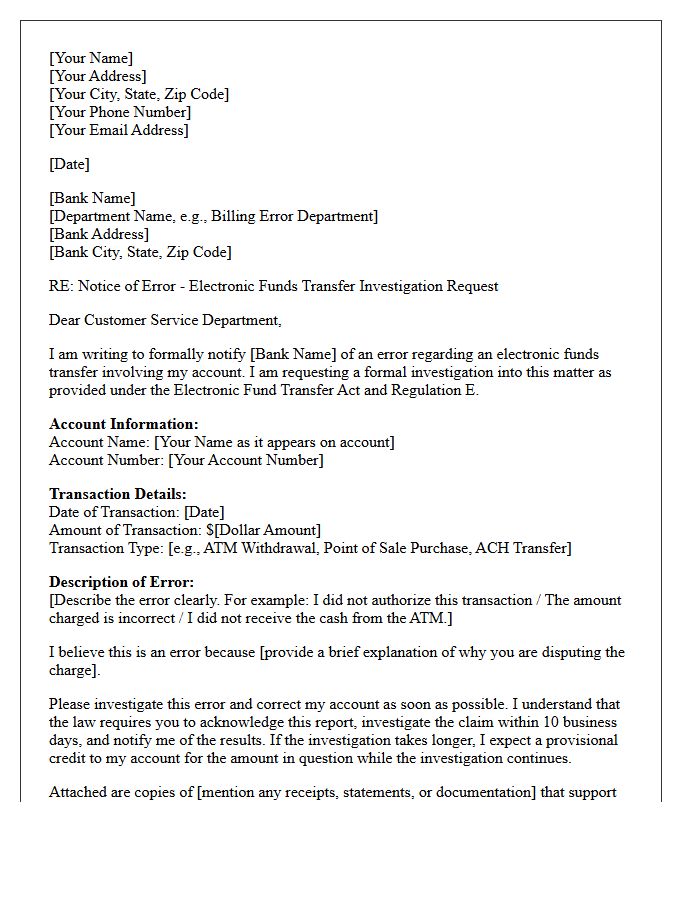

Bank Investigation of Electronic Funds Transfer Error Letter

A Bank Investigation of Electronic Funds Transfer Error Letter is a formal notice sent by a consumer to report unauthorized transactions or billing mistakes. Under Regulation E of the Electronic Fund Transfer Act, you must notify your financial institution within 60 days to protect your consumer rights and limit liability. The letter should include your account details, the specific error date, and the disputed amount. Providing clear documentation helps ensure the bank conducts a timely investigation and provides a provisional credit while resolving the claim.

Provisional Credit for Electronic Funds Transfer Error Letter

A Provisional Credit is a temporary refund issued by your bank while they investigate a reported Electronic Funds Transfer (EFT) error. Under Regulation E, if a financial institution takes longer than ten business days to resolve a dispute, they must credit the disputed amount to your account. To protect your rights, you should submit a formal written notice or error letter within 60 days. While the credit allows you full access to the funds immediately, the bank can reverse it if their investigation determines no error occurred.

Resolution of Electronic Funds Transfer Dispute Letter

When drafting a Resolution of Electronic Funds Transfer Dispute Letter, you must notify your financial institution within 60 days of the statement date. Clearly document the unauthorized transaction, providing dates, amounts, and reasons for the challenge. Under the Electronic Fund Transfer Act, banks must investigate and typically provide provisional credit if the inquiry takes longer than ten business days. Send the letter via certified mail to maintain a formal paper trail, ensuring your legal rights are protected during the billing error resolution process.

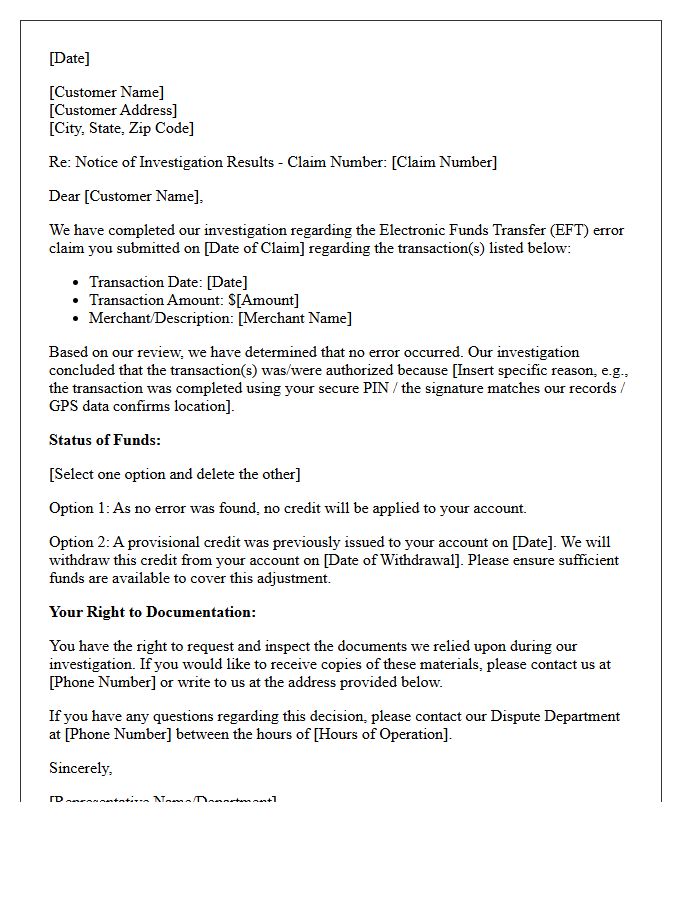

Denial of Electronic Funds Transfer Error Claim Letter

If you receive a Denial of Electronic Funds Transfer Error Claim Letter, you must act quickly. This document explains why a bank refused to reverse a disputed transaction under Regulation E. To challenge the decision, you have the legal right to request all evidence and documents the institution used during their investigation. Carefully review the specific reason for denial and prepare a written appeal within the required timeframe to protect your consumer rights and recover lost funds. Staying informed about your liability limits is essential for a successful resolution.

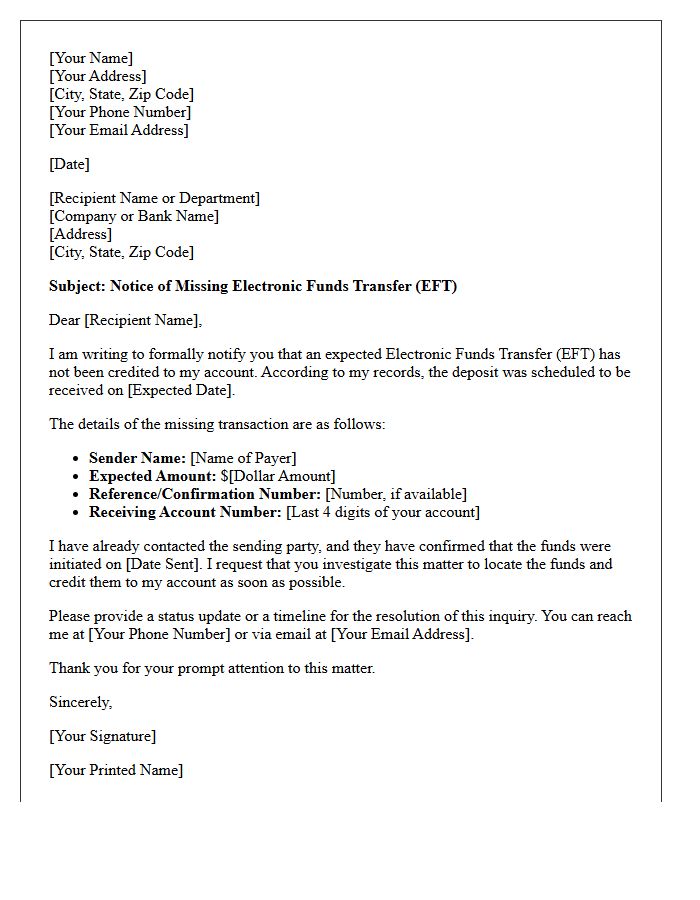

Missing Electronic Funds Transfer Deposit Notice Letter

A Missing Electronic Funds Transfer Deposit Notice Letter is a formal notification sent when a scheduled ACH payment or wire transfer fails to appear in a bank account. This document serves as an official inquiry to initiate a trace and resolve discrepancies between the sender and receiver. It is essential to include the transaction reference number, expected date, and exact amount to expedite the reconciliation process. Promptly issuing this letter helps identify technical errors, incorrect banking details, or processing delays within the financial network.

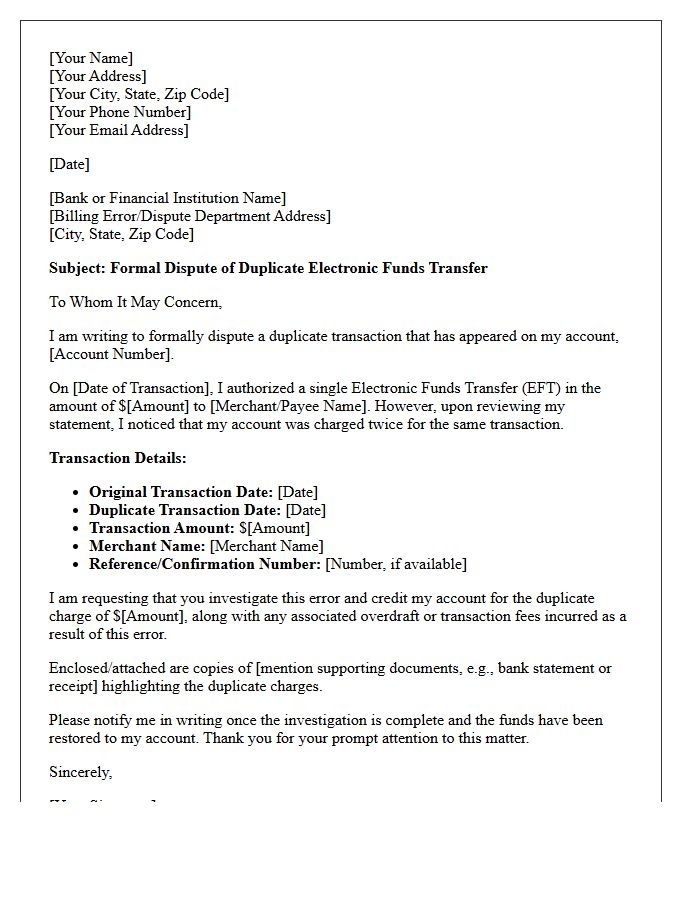

Duplicate Electronic Funds Transfer Charge Dispute Letter

When filing a Duplicate Electronic Funds Transfer Charge Dispute Letter, you must clearly identify the repeated transaction on your statement. Use Regulation E protections to ensure your bank investigates the billing error within legal timeframes. Explicitly state the exact date, amount, and merchant name for both the original and the duplicate charge. Attaching a copy of your bank statement with the errors highlighted will expedite the reversal of funds. Promptly submitting this formal written notice is essential to protecting your consumer rights and recovering your balance quickly.

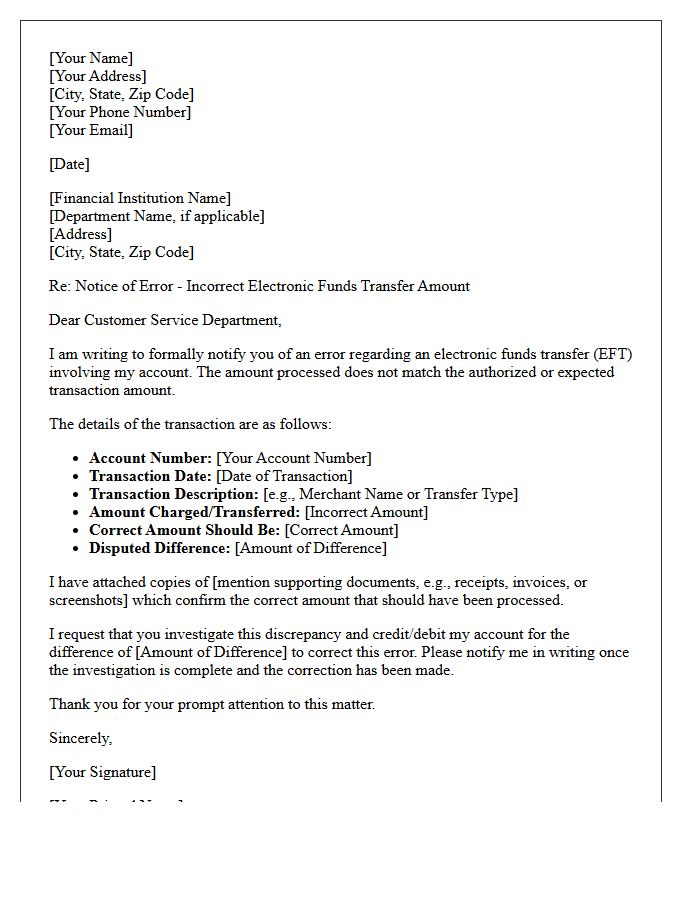

Incorrect Electronic Funds Transfer Amount Notice Letter

An Incorrect Electronic Funds Transfer Amount Notice Letter is a formal legal document used to dispute a transaction error under Regulation E. You must notify your financial institution within 60 days of the statement date to preserve your consumer protection rights. The letter should clearly detail the specific discrepancy, transaction date, and account information. Providing written notice ensures the bank initiates a timely investigation and provides potential provisional credit while resolving the billing error or unauthorized overcharge on your account.

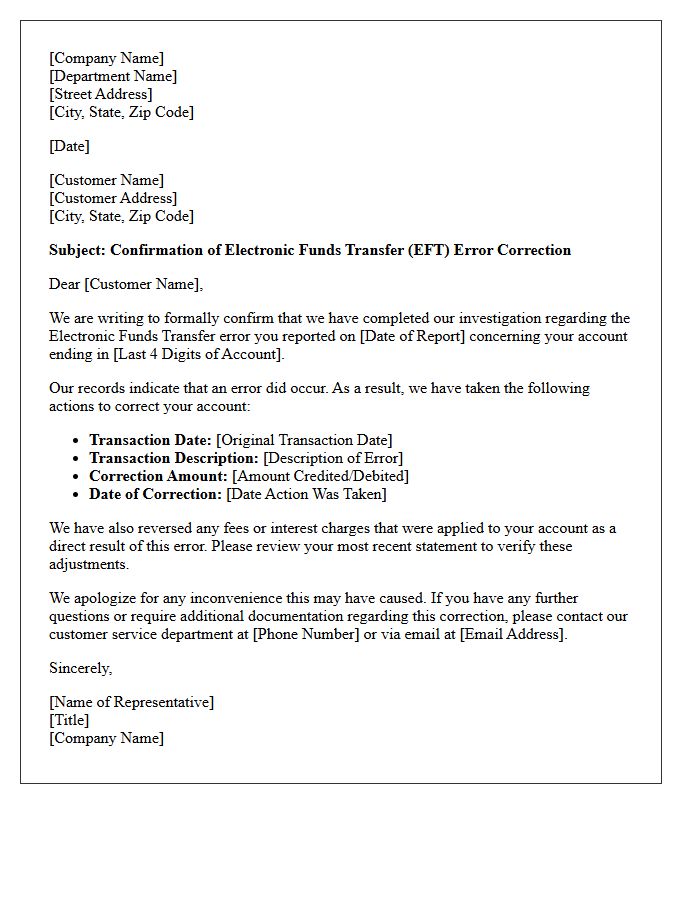

Confirmation of Electronic Funds Transfer Error Correction Letter

A Confirmation of Electronic Funds Transfer Error Correction Letter is a formal document sent by a financial institution to verify that a reported transaction discrepancy has been resolved. This letter serves as legal proof of rectification, ensuring that funds are correctly restored to your account. It typically outlines the specific error investigated, the correction date, and any adjusted interest. Always review this confirmation against your bank statement to ensure total accuracy and protect your consumer rights under banking regulations.

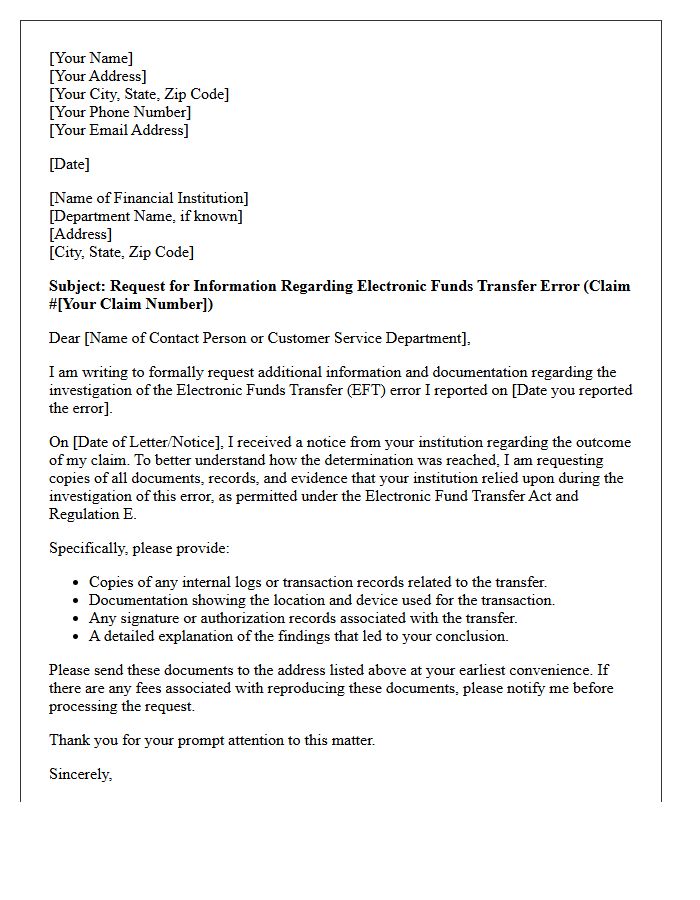

Request for Additional Information on Electronic Funds Transfer Error Letter

When responding to a Request for Additional Information on Electronic Funds Transfer Error Letter, accuracy is vital. You must provide specific transaction details, including the date, exact dollar amount, and the unique confirmation number. Clearly explain why the EFT error occurred to help the financial institution investigate the discrepancy. Ensure your documentation is submitted within the legal timeframe specified in the notice to protect your consumer rights under Regulation E. Providing comprehensive evidence promptly ensures a faster resolution and helps recover your missing funds efficiently.

Final Decision on Electronic Funds Transfer Error Letter

A Final Decision on Electronic Funds Transfer Error Letter is a formal notification from a financial institution regarding a disputed transaction. This document confirms the bank's conclusion after investigating potential unauthorized charges or processing mistakes. If the error is confirmed, the bank must provide a permanent credit to your account. However, if the claim is denied, the letter explains the reasoning and details how any provisional credit will be reversed. Reviewing this decision is essential for protecting your consumer rights under Regulation E and ensuring your account balance remains accurate.

What is an Electronic Funds Transfer (EFT) Error Notice Letter?

An Electronic Funds Transfer Error Notice Letter is a formal written notification sent by a consumer to their financial institution to report a discrepancy, unauthorized transaction, or mistake involving an electronic transfer of funds.

When should I send a notice of error for an electronic transfer?

Under Regulation E of the Electronic Fund Transfer Act, you should send the notice as soon as you identify a discrepancy, but no later than 60 days after the financial institution transmitted the first periodic statement on which the error appeared.

What information must be included in an EFT Error Notice Letter?

The letter should include your name and account number, the specific date and dollar amount of the suspected error, and a clear explanation of why you believe an error occurred or why you need more information.

How long does a bank have to investigate an EFT error after receiving my letter?

Generally, the bank has 10 business days to investigate. If they need more time (up to 45 or 90 days), they must typically provide a provisional credit to your account for the amount in question while they complete the investigation.

What types of transactions are covered by an EFT Error Notice?

EFT error notices apply to transactions such as unauthorized ATM withdrawals, point-of-sale debit card purchases, direct deposit errors, automated clearing house (ACH) transfers, and incorrect computer-initiated payments.

Comments