Receiving a Warning Letter for Missed Mortgage Payment can be stressful, but it is a vital legal notice from your lender. This document outlines your overdue balance, potential late fees, and the risk of foreclosure if the debt remains unpaid. Taking immediate action can help protect your home and credit score. To assist you, below are some ready to use templates.

Image cover: Missed Mortgage Payment Warning Letter: Professional Templates and Samples

Letter Samples List

- First Notice of Missed Mortgage Payment Letter

- Friendly Reminder for Missed Mortgage Payment Letter

- Second Warning Letter for Missed Mortgage Payment

- Urgent Mortgage Account Delinquency Warning Letter

- Final Warning Letter for Mortgage Default

- Notice of Intent to Foreclose Letter

- Mortgage Payment Grace Period Expiration Letter

- Pre-Foreclosure Warning Letter for Missed Payment

- Breach of Mortgage Contract Notice Letter

- Mortgage Loan Acceleration Warning Letter

- Notice of Default and Right to Cure Letter

- Demand for Past Due Mortgage Payment Letter

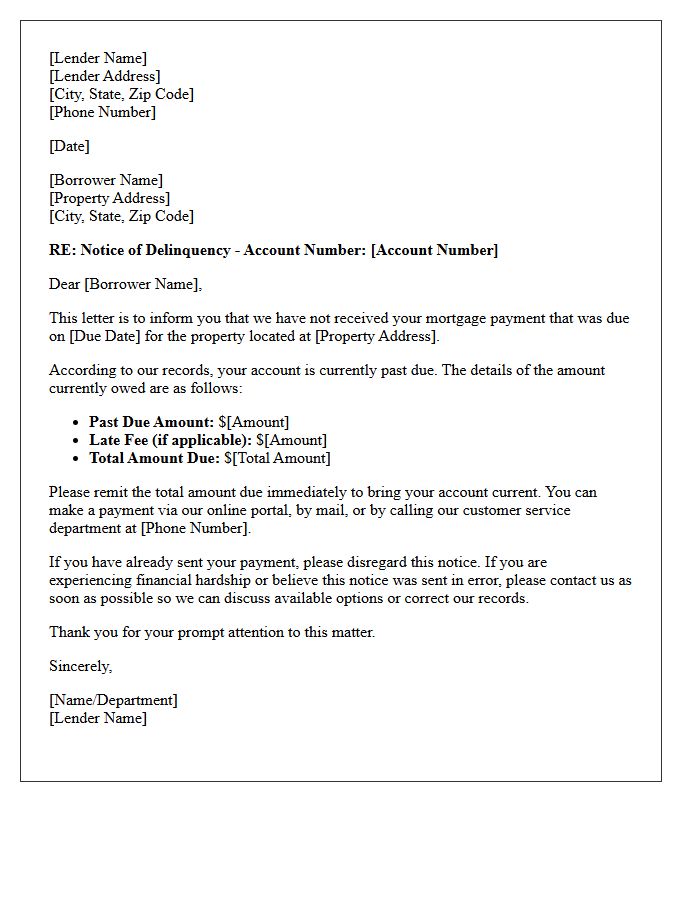

First Notice of Missed Mortgage Payment Letter

Receiving a First Notice of Missed Mortgage Payment is a critical warning that your account is delinquent. This formal letter serves as an official record of a late payment and typically outlines the amount owed, including any late fees. It is the first step in the loss mitigation process required by law before a lender can pursue foreclosure. To protect your home, you must contact your servicer immediately to discuss repayment plans or loan modifications. Prompt communication is essential to resolve the default and maintain your credit standing.

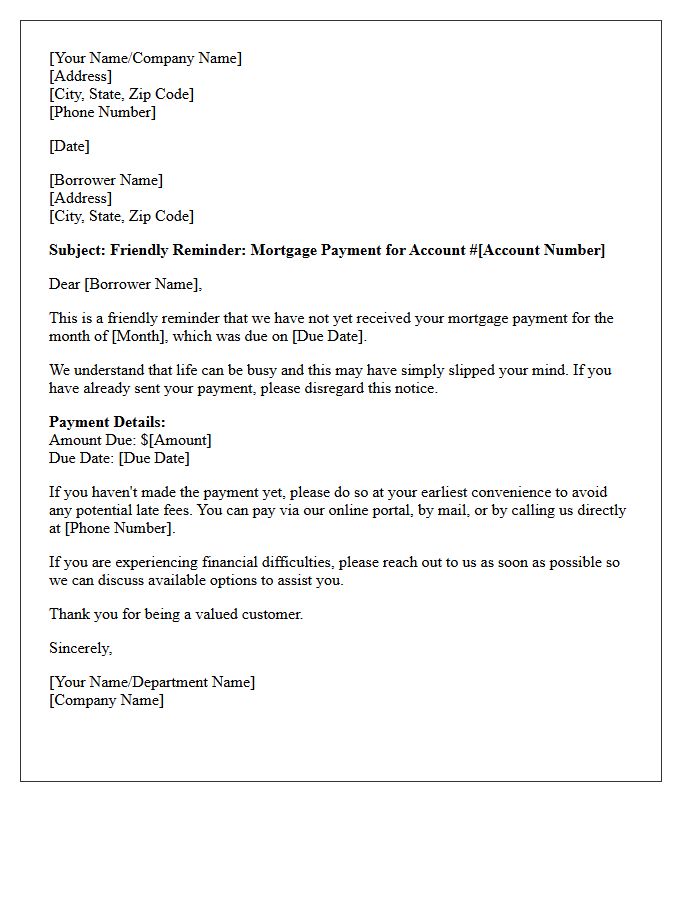

Friendly Reminder for Missed Mortgage Payment Letter

Receiving a friendly reminder for a missed mortgage payment is a critical notice designed to help you avoid late fees and credit score damage. Most lenders offer a brief grace period, typically fifteen days, before penalties apply. It is essential to communicate immediately with your loan servicer to discuss repayment options or loss mitigation if you are facing financial hardship. Promptly addressing this letter prevents the situation from escalating into default or foreclosure, ensuring your home ownership remains secure through proactive financial management and timely resolution.

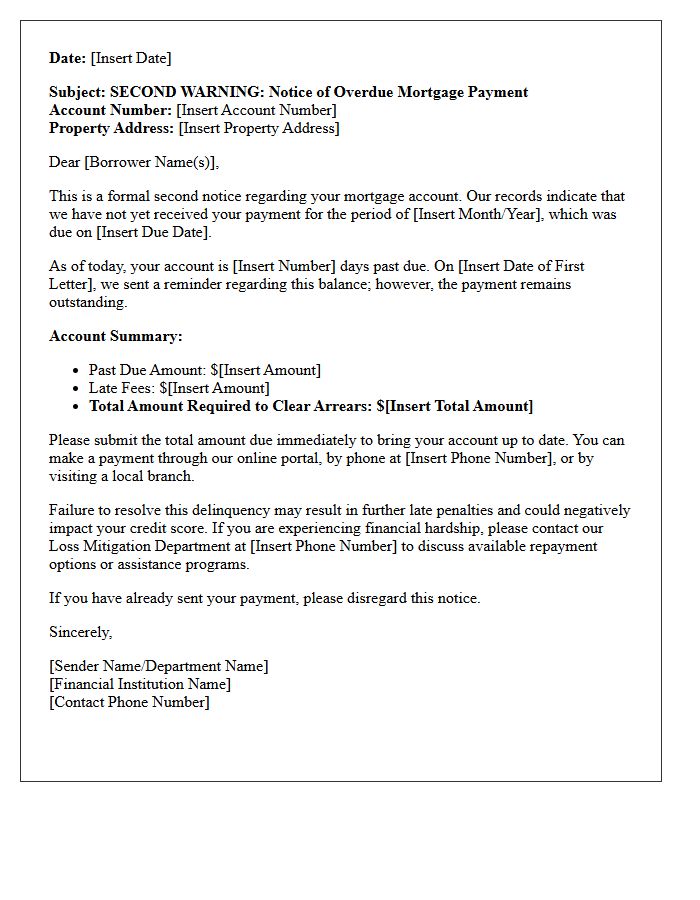

Second Warning Letter for Missed Mortgage Payment

A Second Warning Letter is a critical formal notice indicating that your mortgage account is in serious default. Receiving this document means previous attempts to resolve missed payments have failed, significantly increasing the risk of foreclosure. It typically outlines the total overdue balance, late fees, and a strict deadline for payment. To protect your home, you must immediately contact your lender to discuss loss mitigation options, such as loan modification or a repayment plan, before the legal process advances toward home forfeiture and severe credit damage.

Urgent Mortgage Account Delinquency Warning Letter

An Urgent Mortgage Account Delinquency Warning Letter is a formal notification from your lender indicating that your home loan is past due. This critical document outlines the total arrears, late fees, and a specific deadline for payment to avoid default. Ignoring this notice can trigger foreclosure proceedings, leading to the loss of your property. It is essential to contact your loan servicer immediately to discuss loss mitigation options, such as loan modification or a repayment plan, to protect your homeownership and credit score.

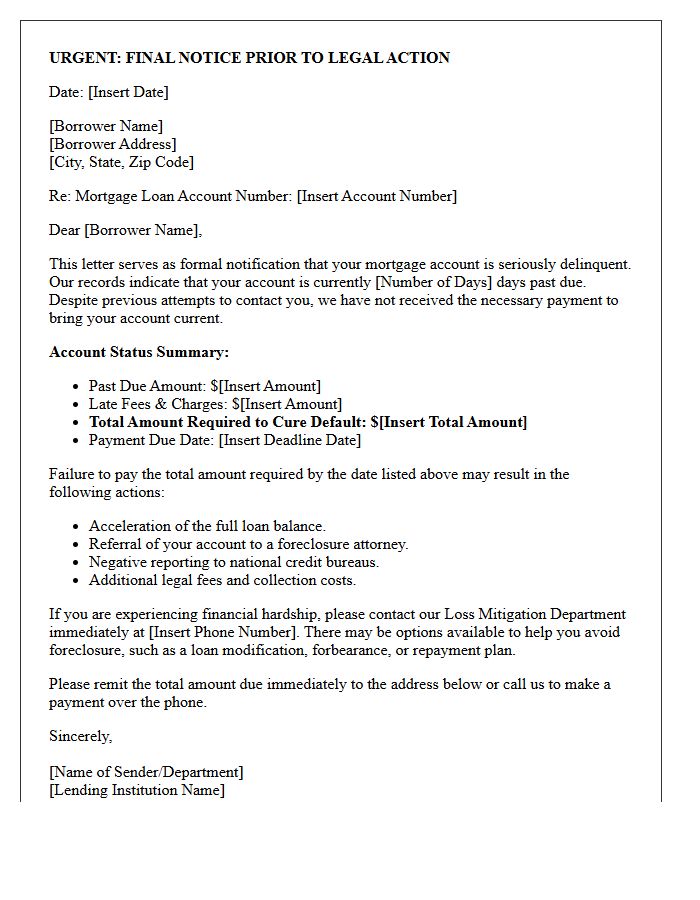

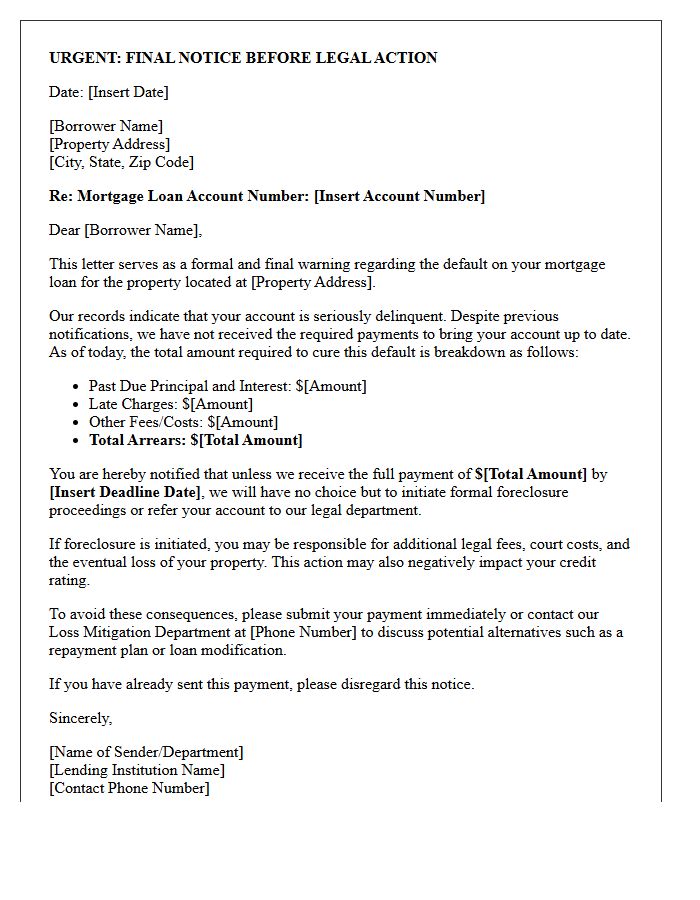

Final Warning Letter for Mortgage Default

A Final Warning Letter for mortgage default is a critical formal notice issued by lenders before initiating foreclosure proceedings. It serves as a legal notification that your loan is seriously delinquent and demands immediate payment to cure the default. Ignoring this document can lead to the loss of your property and severe credit damage. Homeowners should prioritize legal advice or contact their loan servicer immediately to discuss loss mitigation options, such as loan modification or repayment plans, to prevent the final acceleration of the debt.

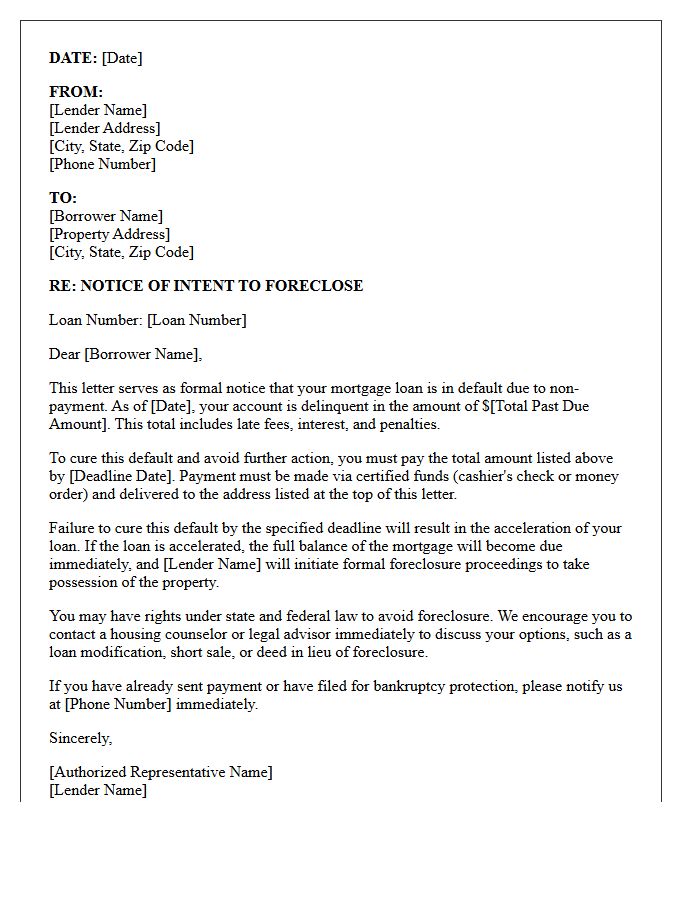

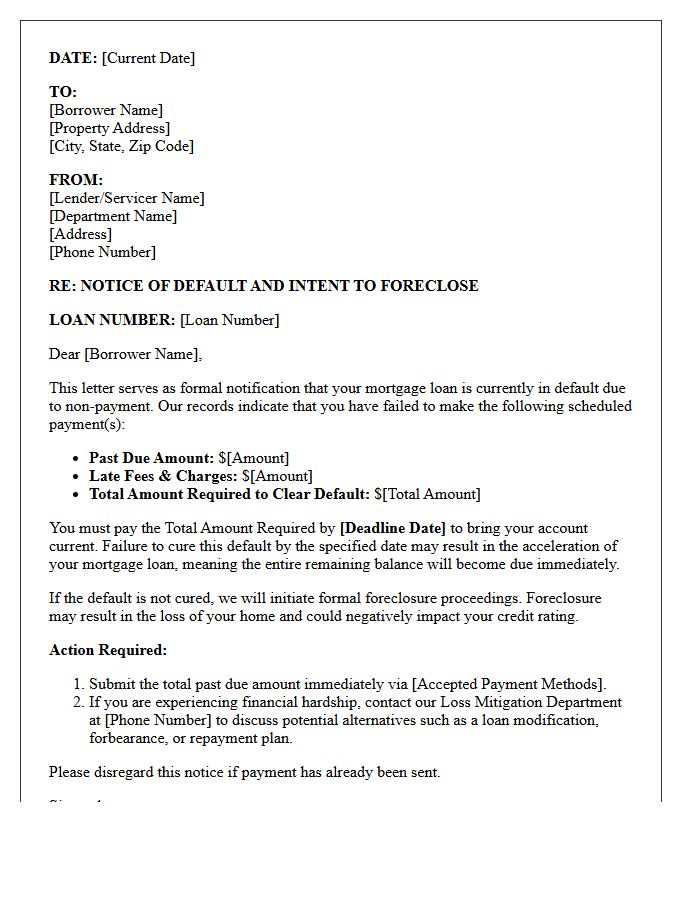

Notice of Intent to Foreclose Letter

A Notice of Intent to Foreclose is a formal legal warning sent by a mortgage lender to a borrower who has fallen behind on payments. This document serves as the final alert before a foreclosure action officially begins in court. It outlines the specific amount needed to cure the default, provides a deadline for payment, and explains your rights to loss mitigation. Receiving this letter is critical because it represents the last opportunity to resolve the debt through a loan modification or repayment plan to save your home.

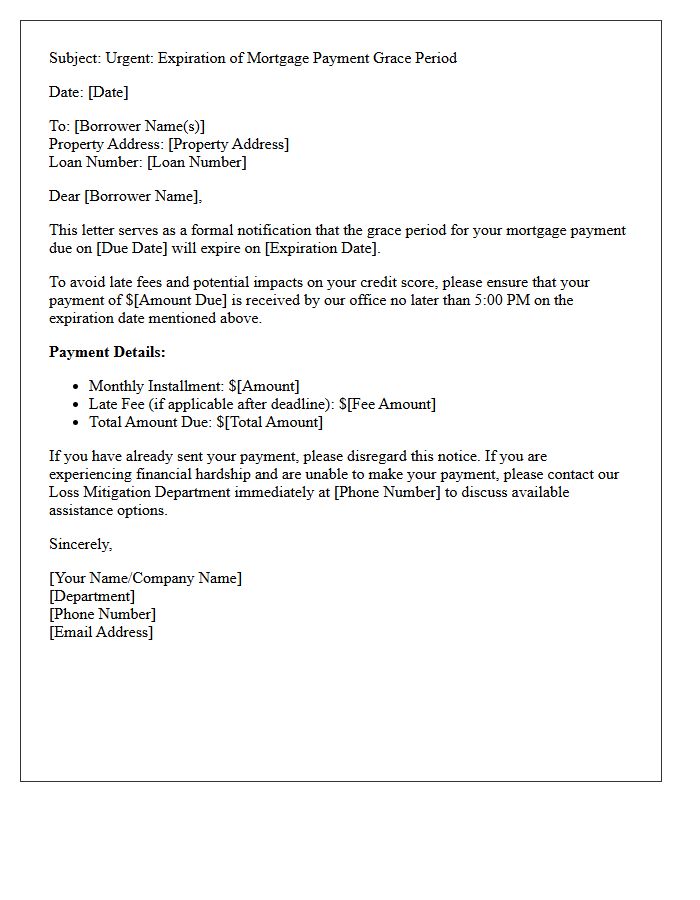

Mortgage Payment Grace Period Expiration Letter

Receiving a Mortgage Payment Grace Period Expiration Letter is a critical notification that your late payment window has closed. This document confirms that your lender will now assess late fees and potentially report the delinquency to credit bureaus. It serves as a formal warning that your account is entering default status. To protect your credit score and avoid foreclosure proceedings, you must submit the outstanding balance immediately. Contacting your loan servicer promptly to discuss repayment options or loss mitigation can prevent further financial penalties and legal action against your property.

Pre-Foreclosure Warning Letter for Missed Payment

Receiving a pre-foreclosure warning letter is a critical legal notice indicating that your mortgage is officially delinquent. This document serves as a formal notice of default, outlining the total amount overdue, including late fees and interest. It provides a specific timeframe to cure the debt before the lender initiates formal foreclosure proceedings. To protect your home, you must prioritize communication with your loan servicer to discuss mitigation options like loan modification or repayment plans. Acting immediately is essential to prevent the loss of your property and severe damage to your credit score.

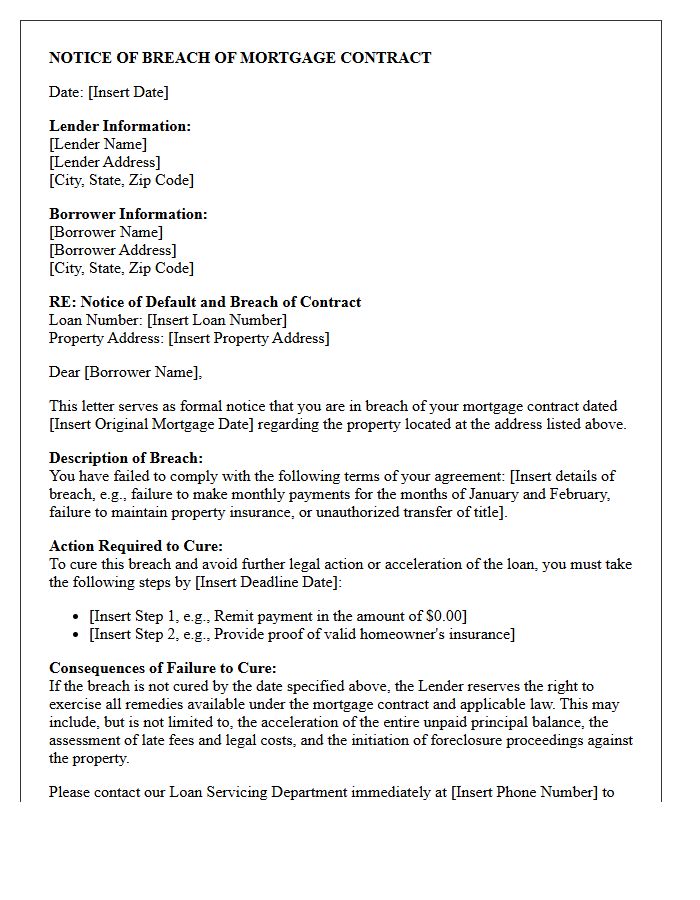

Breach of Mortgage Contract Notice Letter

A Breach of Mortgage Contract Notice Letter is a formal legal warning issued by a lender when a borrower violates loan terms, most commonly through delinquent payments. This document serves as a mandatory step before initiating foreclosure, detailing the specific default, the required cure amount, and a strict deadline for resolution. Understanding this notice is critical, as it outlines your rights to reinstate the loan and the legal consequences of inaction. Prompt communication with your servicer after receiving this letter is essential to exploring loss mitigation options and protecting your home equity.

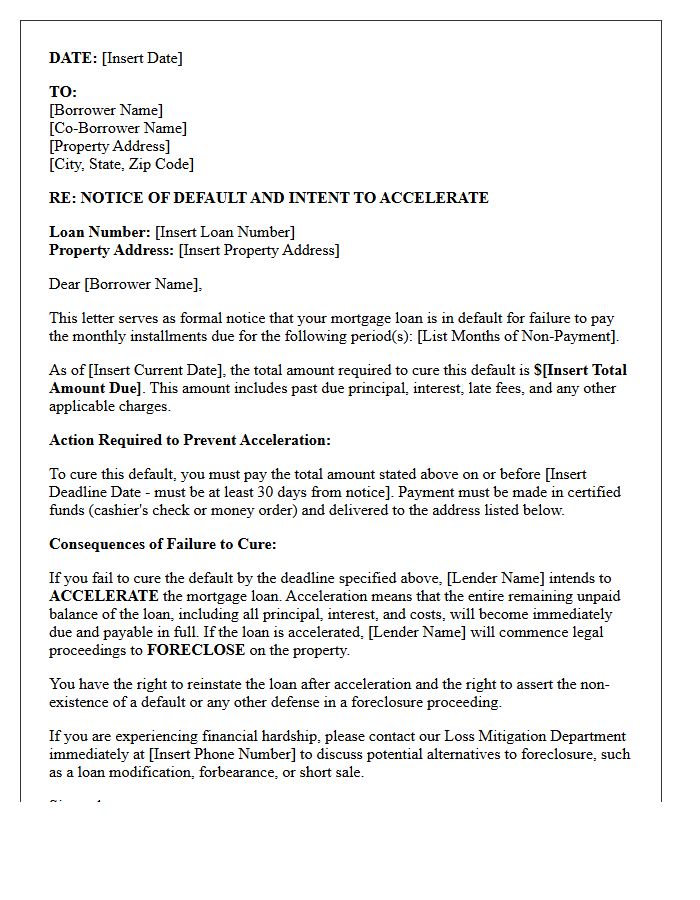

Mortgage Loan Acceleration Warning Letter

A Mortgage Loan Acceleration Warning Letter is a formal notice from a lender indicating that a default has occurred, typically due to missed payments. This critical document serves as a final demand for the borrower to cure the delinquency within a specific timeframe. Failure to pay the requested amount triggers the acceleration clause, making the entire loan balance due immediately. This is the final step before the lender initiates foreclosure proceedings. Borrowers must act quickly to negotiate a repayment plan or loan modification to protect their property ownership.

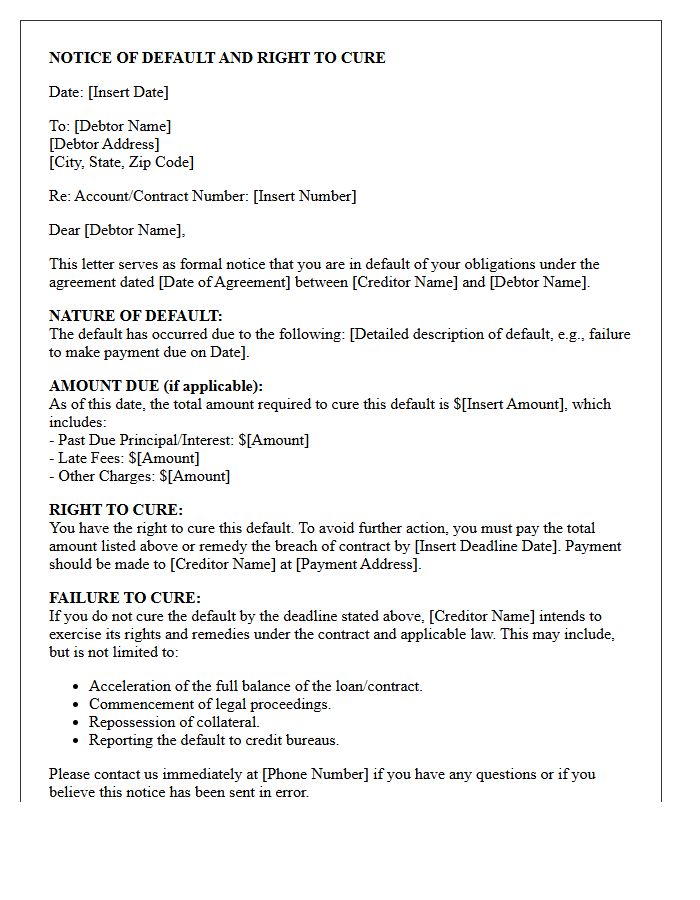

Notice of Default and Right to Cure Letter

A Notice of Default and Right to Cure is a formal legal warning issued by a lender when a borrower breaches a contract, typically through missed payments. This document is a critical step in the foreclosure or repossession process, identifying the specific default occurred. It grants the borrower a mandatory grace period to pay the outstanding balance and late fees to reinstate the loan. Failing to "cure" the debt within this timeframe allows the creditor to accelerate the loan and pursue foreclosure or legal action to reclaim the collateral.

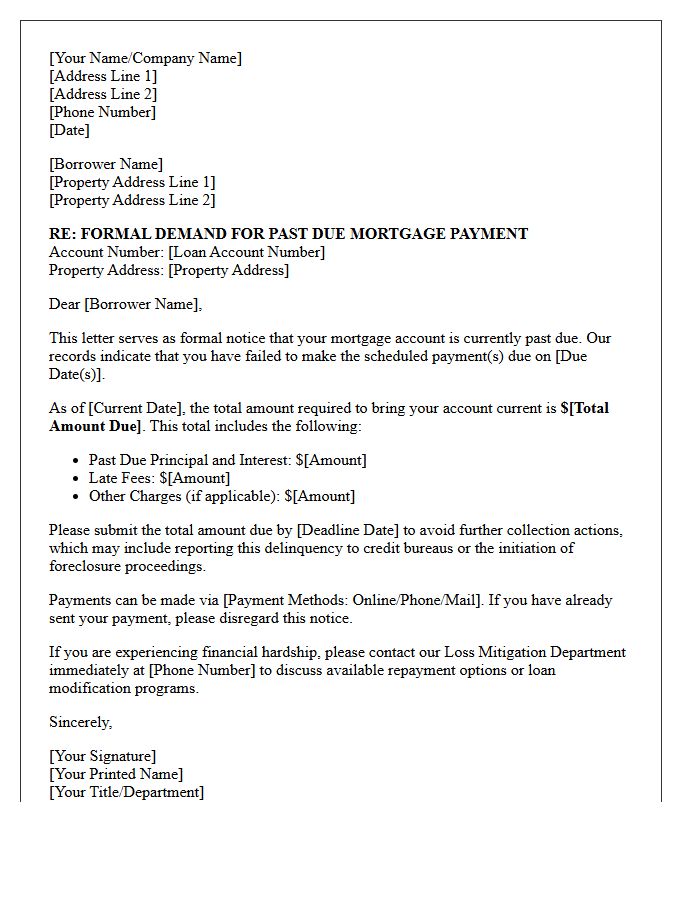

Demand for Past Due Mortgage Payment Letter

A Demand for Past Due Mortgage Payment Letter is a formal notice sent by lenders to borrowers who have missed scheduled payments. This critical document serves as a legal warning that the loan is in default. It outlines the total amount owed, including late fees, and provides a specific deadline for payment to avoid further action. Receiving this letter is a vital signal to initiate communication with your servicer. Addressing the delinquency immediately is the best way to prevent foreclosure proceedings and protect your long-term property ownership rights.

What is a warning letter for a missed mortgage payment?

A warning letter, also known as a notice of delinquency, is a formal document sent by a mortgage lender to inform a borrower that they have missed a scheduled payment. It serves as an official record and provides details on the overdue amount, late fees, and the deadline to rectify the default before further legal action or foreclosure begins.

What should I do immediately after receiving a mortgage missed payment notice?

Upon receiving the letter, you should immediately contact your loan servicer to discuss your financial situation. Review the letter for accuracy regarding the payment amount and due date, then attempt to make the payment or request a formal payment plan to prevent the account from moving into further stages of delinquency.

Will a single mortgage warning letter affect my credit score?

Yes, a single missed payment can significantly impact your credit score if the payment is more than 30 days past due. Lenders typically report delinquencies to credit bureaus at the 30-day mark, which can lower your score and remain on your credit report for up to seven years.

Can I lose my home after receiving one warning letter for a missed payment?

While one letter is the first step in the legal process, foreclosure typically does not occur immediately. Federal law generally requires a borrower to be more than 120 days delinquent before a lender can officially start the foreclosure process, providing a window of time to seek loss mitigation options.

What options are available to resolve a mortgage delinquency warning?

Borrowers can resolve a delinquency through several options including reinstatement (paying the total owed), a repayment plan, loan modification, or forbearance. If you cannot afford the mortgage long-term, options like a short sale or a deed-in-lieu of foreclosure may be discussed with the lender to avoid a formal foreclosure on your record.

Comments