Financial institutions must adhere strictly to anti-money laundering regulations. Receiving a Warning Letter for Violation of Bank Secrecy Act Policies signifies critical compliance failures that require immediate corrective action to avoid severe legal penalties. This guide outlines regulatory expectations, common pitfalls in internal controls, and essential remediation steps for management. To assist your compliance efforts, below are some ready to use template.

Image cover: Official Warning: Failure to Comply with Bank Secrecy Act and AML Compliance Standards

Letter Samples List

- Warning Letter for Failure to File Suspicious Activity Reports

- First Warning Letter Regarding Customer Identification Program Deficiencies

- Formal Warning Letter for Currency Transaction Report Oversight

- Official Warning Letter Concerning Anti-Money Laundering Training Noncompliance

- Final Warning Letter for Inadequate Know Your Customer Documentation

- Written Warning Letter for Unreported Large Cash Transactions

- Disciplinary Warning Letter for Neglecting Office of Foreign Assets Control Screening

- Compliance Warning Letter for Bank Secrecy Act Recordkeeping Violations

- Supervisory Warning Letter for Improper Enhanced Due Diligence Procedures

- Administrative Warning Letter Regarding Unauthorized Disclosure of Suspicious Activity

- Executive Warning Letter for Failure to Monitor High-Risk Accounts

- Internal Warning Letter for Negligence in Wire Transfer Auditing

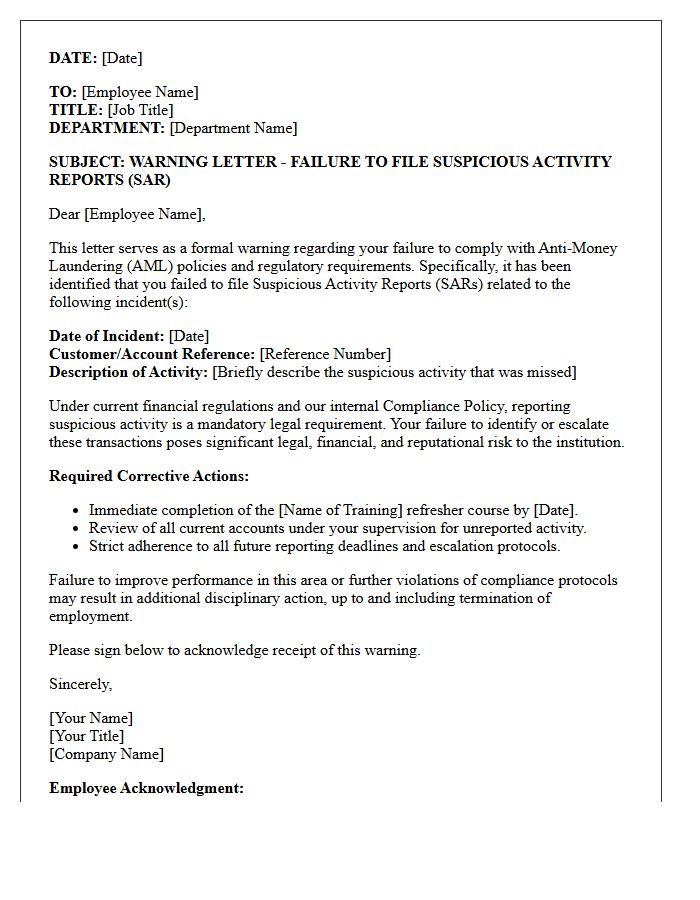

Warning Letter for Failure to File Suspicious Activity Reports

A financial institution receives a Warning Letter for Failure to File Suspicious Activity Reports (SARs) when regulatory bodies identify deficiencies in monitoring potentially illegal transactions. This formal notification highlights a breach of anti-money laundering (AML) compliance standards. Failure to rectify these issues promptly can lead to severe civil money penalties, increased oversight, or criminal prosecution. It is essential to implement robust transaction monitoring systems and ensure timely reporting to FinCEN to demonstrate regulatory adherence and mitigate further legal risks or reputational damage to the organization.

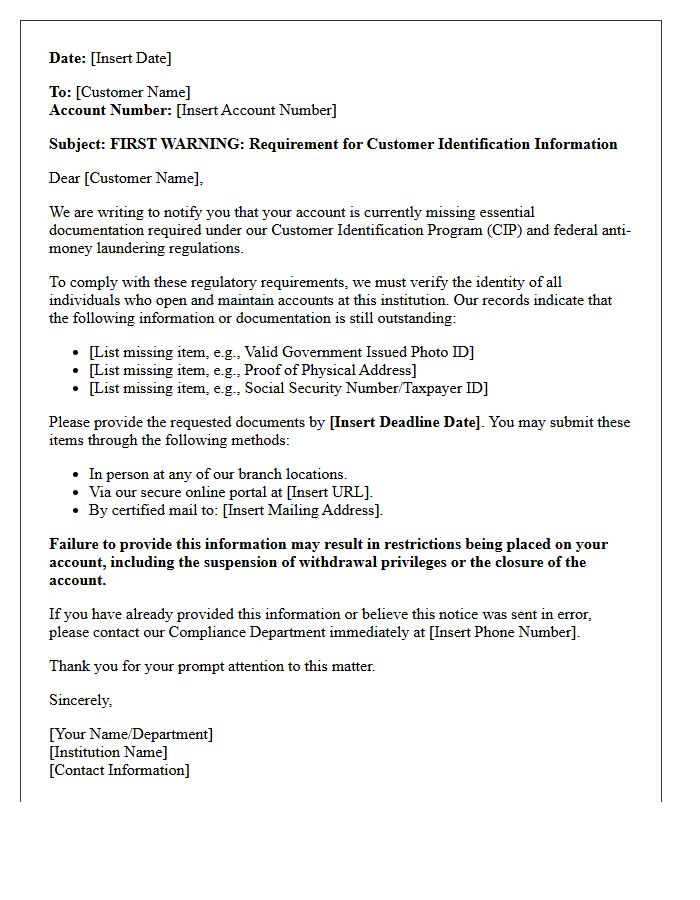

First Warning Letter Regarding Customer Identification Program Deficiencies

Receiving a first warning letter regarding Customer Identification Program (CIP) deficiencies indicates critical failures in verifying client identities. Financial institutions must comply with Anti-Money Laundering (AML) regulations to prevent identity theft and fraud. This formal notice demands immediate remediation of internal controls and record-keeping processes. Failure to address these gaps can lead to severe regulatory sanctions, heavy fines, or loss of operating licenses. Timely corrective action is essential to demonstrate compliance and protect the institution's integrity within the global financial system.

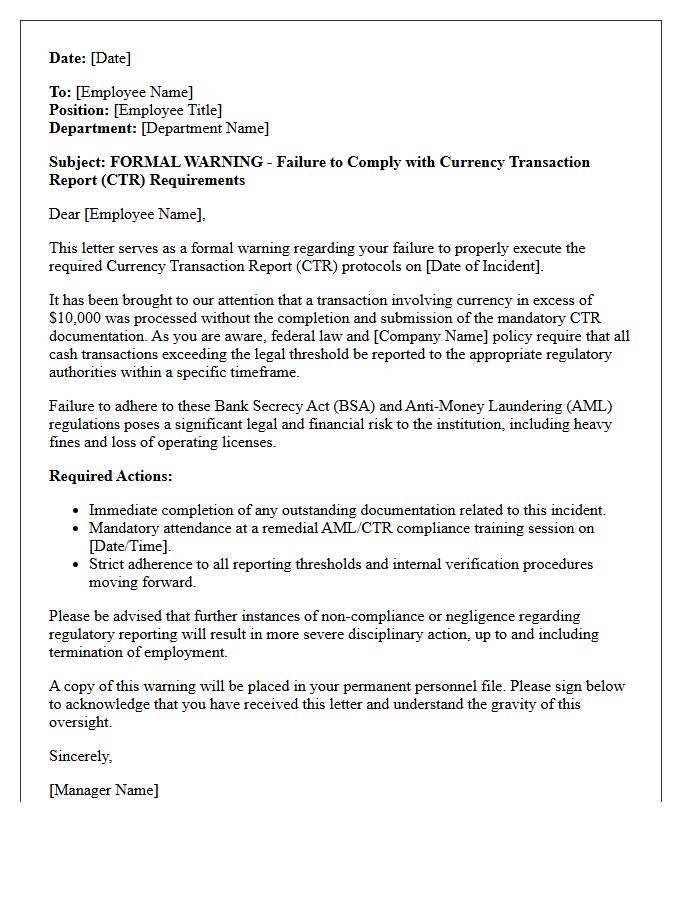

Formal Warning Letter for Currency Transaction Report Oversight

A formal warning letter regarding Currency Transaction Report (CTR) oversight is a critical regulatory notification. It indicates that a financial institution failed to document cash transactions exceeding $10,000 as required by the Bank Secrecy Act. This document serves as an official reprimand, highlighting systemic weaknesses in internal controls or compliance monitoring. To mitigate legal risks and potential fines, the organization must provide a documented response outlining immediate remedial actions, improved staff training, and enhanced auditing processes to ensure future reporting accuracy and regulatory adherence.

Official Warning Letter Concerning Anti-Money Laundering Training Noncompliance

Receiving an official warning letter regarding Anti-Money Laundering (AML) training noncompliance indicates a serious regulatory breach. Organizations must ensure all staff complete mandatory compliance education to prevent financial crimes. Failure to address this notice promptly can lead to severe legal penalties, heavy fines, and operational license revocation. It is essential to document all remedial training actions immediately to satisfy regulatory oversight and demonstrate a commitment to financial integrity and robust internal controls.

Final Warning Letter for Inadequate Know Your Customer Documentation

A final warning letter for inadequate KYC documentation is a formal notice issued by financial institutions before account restriction or closure. It signifies a critical failure to provide mandatory identity verification or source of funds details required by anti-money laundering regulations. To maintain your banking relationship, you must submit the requested records immediately. Ignoring this communication leads to permanent account termination and potential reporting to regulatory authorities. Ensure all documents are valid, certified, and up-to-date to resolve compliance gaps and prevent the loss of access to your financial services.

Written Warning Letter for Unreported Large Cash Transactions

A written warning letter for unreported large cash transactions is a formal disciplinary document addressing a compliance violation of anti-money laundering regulations. Under Bank Secrecy Act requirements, businesses must report cash payments exceeding $10,000 using Form 8300. Failure to document these financial thresholds exposes the company to severe legal penalties and audits. This letter serves as a final notice to the employee, emphasizing the legal obligation to maintain accurate records and ensure full transparency to prevent potential regulatory fines or criminal liability for the organization.

Disciplinary Warning Letter for Neglecting Office of Foreign Assets Control Screening

A disciplinary warning letter for neglecting OFAC screening serves as a formal notification of non-compliance with federal trade sanctions. Failing to vet clients against specially designated nationals lists exposes the organization to severe legal penalties and financial risks. This document emphasizes that adherence to Office of Foreign Assets Control regulations is a mandatory condition of employment. Employees must prioritize these mandatory background checks to ensure organizational security. Future violations regarding these regulatory mandates may result in further disciplinary action, including potential termination for compromising institutional integrity and legal standing.

Compliance Warning Letter for Bank Secrecy Act Recordkeeping Violations

A Compliance Warning Letter serves as a formal notification from regulators regarding specific Bank Secrecy Act (BSA) recordkeeping deficiencies. It signals that an institution failed to accurately document financial transactions, customer identification, or suspicious activity reports. While not a public enforcement action, it is a critical legal alert demanding immediate remediation. Failure to address these gaps can lead to severe civil money penalties and formal consent orders. Ensuring robust audit trails and data integrity is essential to maintaining regulatory standing and avoiding heightened oversight by federal examiners.

Supervisory Warning Letter for Improper Enhanced Due Diligence Procedures

A Supervisory Warning Letter is a formal regulatory notice issued to financial institutions for failing to maintain adequate Enhanced Due Diligence (EDD) protocols. This document signals critical deficiencies in identifying and monitoring high-risk customers, such as PEPs or entities in jurisdictions with weak anti-money laundering controls. Receiving this letter serves as a final directive to remediate compliance gaps before the regulator imposes severe penalties, cease-and-desist orders, or heavy fines. Organizations must immediately overhaul their risk assessment frameworks and documentation processes to satisfy supervisory expectations and ensure legal financial integrity.

Administrative Warning Letter Regarding Unauthorized Disclosure of Suspicious Activity

An Administrative Warning Letter is a formal notification issued to financial institutions for the unauthorized disclosure of suspicious activity. It serves as a serious reprimand when an employee or organization violates "tipping off" regulations by revealing the existence of a Suspicious Activity Report (SAR) to involved parties. Maintaining confidentiality is critical to protecting ongoing criminal investigations and national security. Failure to adhere to these non-disclosure requirements can lead to severe civil penalties, regulatory sanctions, or criminal charges under the Bank Secrecy Act.

Executive Warning Letter for Failure to Monitor High-Risk Accounts

An Executive Warning Letter for failure to monitor high-risk accounts serves as a formal disciplinary notice regarding severe compliance lapses. It highlights a critical breach of fiduciary duty and failure to implement mandated Anti-Money Laundering (AML) protocols. Such letters emphasize that neglecting oversight on volatile accounts poses significant legal, financial, and reputational threats to the organization. Executives must respond by implementing immediate corrective actions and enhanced auditing procedures to mitigate risks. Persistent failure to address these systemic vulnerabilities often leads to regulatory penalties, professional sanctions, or termination of employment.

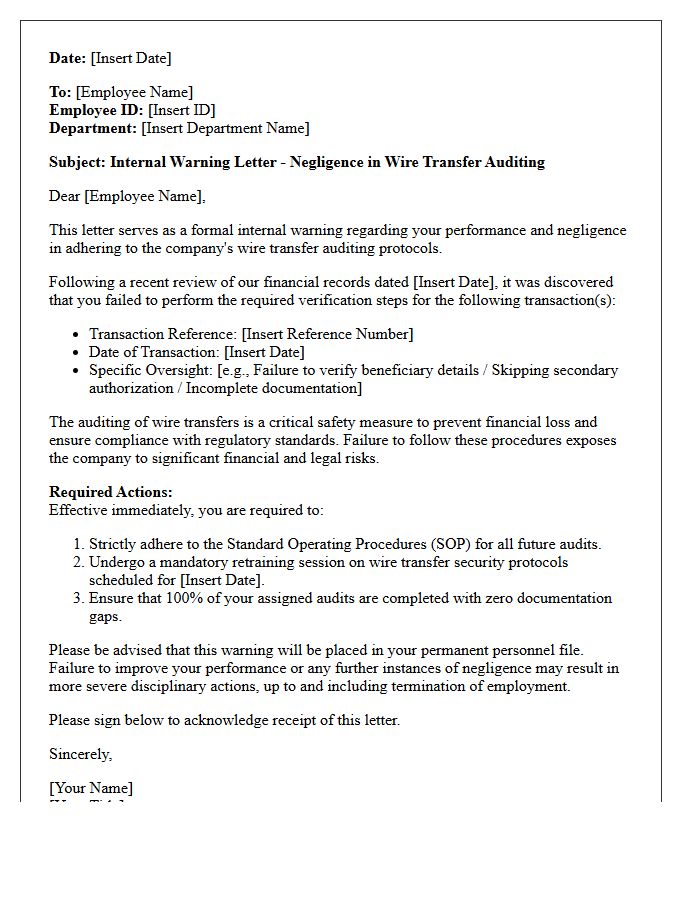

Internal Warning Letter for Negligence in Wire Transfer Auditing

An internal warning letter for negligence in wire transfer auditing serves as a formal disciplinary record. It highlights a failure to follow compliance protocols and verification procedures essential for preventing financial fraud. This document emphasizes the employee's responsibility to maintain accuracy and vigilance during high-risk transactions. It outlines the specific audit lapses identified and mandates corrective actions to ensure future regulatory adherence. Failure to improve performance after receiving this notice can lead to severe administrative consequences or termination, as securing financial integrity remains a critical operational priority for the organization.

What is a Warning Letter for Violation of Bank Secrecy Act (BSA) Policies?

A warning letter for BSA policy violations is a formal disciplinary document issued to an employee or department for failing to comply with federal anti-money laundering (AML) regulations and internal bank protocols designed to prevent financial crimes.

What are common reasons for receiving a BSA violation warning?

Common triggers include failure to file Suspicious Activity Reports (SARs) or Currency Transaction Reports (CTRs) on time, neglecting Customer Due Diligence (CDD) procedures, or failing to properly verify a client's identity during the onboarding process.

What are the legal implications of ignoring BSA policy warnings?

Ignoring BSA warnings can lead to severe consequences, including termination of employment, personal civil money penalties, and potential criminal charges if the negligence is found to have facilitated money laundering or terrorist financing.

How should an employee respond to a BSA violation warning letter?

An employee should provide a written acknowledgment that addresses the specific deficiency, outlines the corrective actions they will take, and details any additional training required to ensure future compliance with the Bank Secrecy Act.

How do financial institutions track repeated BSA policy infractions?

Banks maintain internal compliance logs and personnel files to track infractions; repeated violations typically trigger an escalated "Matter Requiring Attention" (MRA) from federal regulators or immediate termination under the institution's progressive discipline policy.

Comments