A Notice of Dishonored Check Due to Closed Account is a formal legal demand issued when a payment fails because the sender's bank account no longer exists. This notice protects your rights to recover funds and seek statutory damages for bad checks. Managing these financial disputes requires clear, professional documentation to ensure successful debt collection. Below are some ready to use templates.

Image cover: Official Notice: Dishonored Check Due to a Closed Account

Letter Samples List

- First Notice Letter of Dishonored Check Due to Closed Account

- Final Demand Letter for Dishonored Check on Closed Account

- Formal Debt Collection Letter for Bounced Check from Closed Account

- Official Warning Letter Regarding Dishonored Check on Closed Account

- Legal Action Pending Letter for Closed Account Dishonored Check

- Urgent Payment Demand Letter for Dishonored Check Due to Closed Account

- Notice of Returned Check Letter for Closed Bank Account

- Debt Recovery Letter for Dishonored Check on Closed Account

- Pre-Litigation Notice Letter for Closed Account Dishonored Check

- Urgent Collection Letter for Dishonored Check on a Closed Account

- Statutory Notice Letter for Dishonored Check Due to Closed Account

- Default Resolution Letter for Dishonored Check from Closed Account

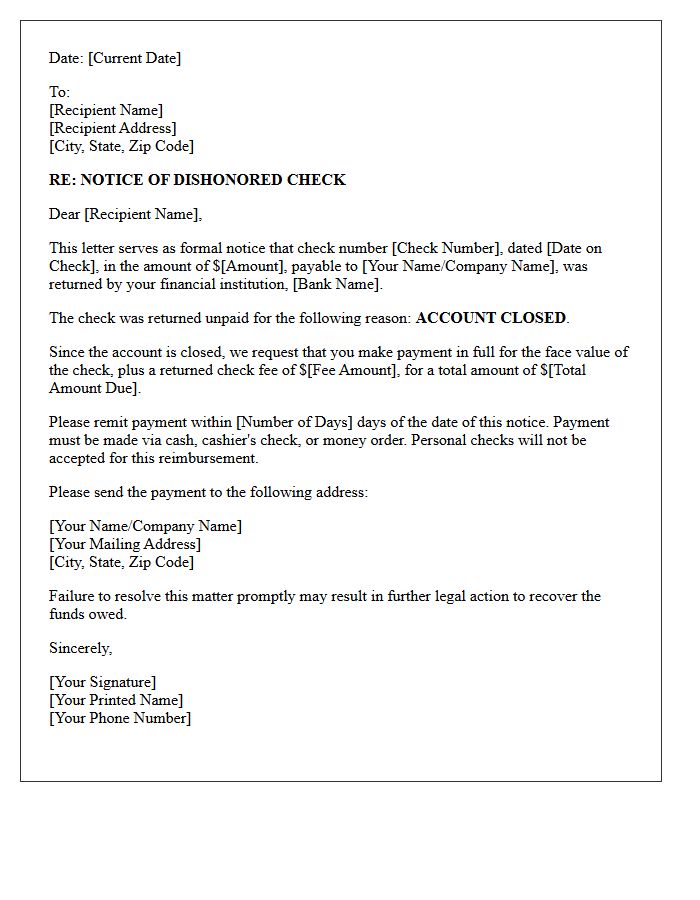

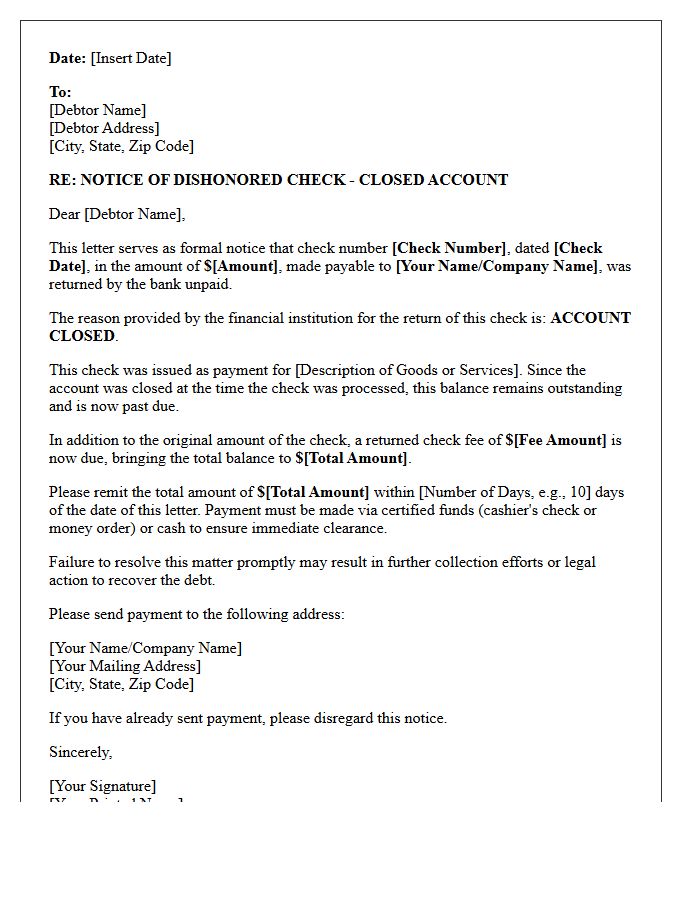

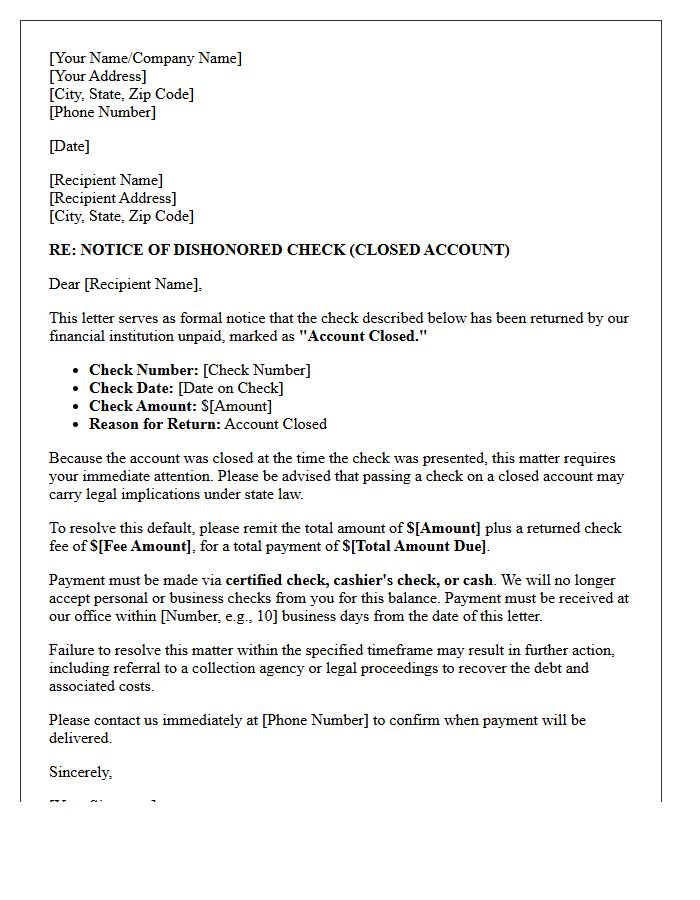

First Notice Letter of Dishonored Check Due to Closed Account

Receiving a First Notice Letter is a formal legal notification that a payment was rejected because the bank account is closed. This document serves as a mandatory demand for payment, typically requiring the recipient to provide restitution within a specific timeframe, such as ten days. It is crucial to settle the debt immediately via cash or certified funds to avoid potential civil lawsuits or criminal prosecution for fraud. Ignoring this notice can lead to additional penalties, legal fees, and severe damage to your credit standing and financial reputation.

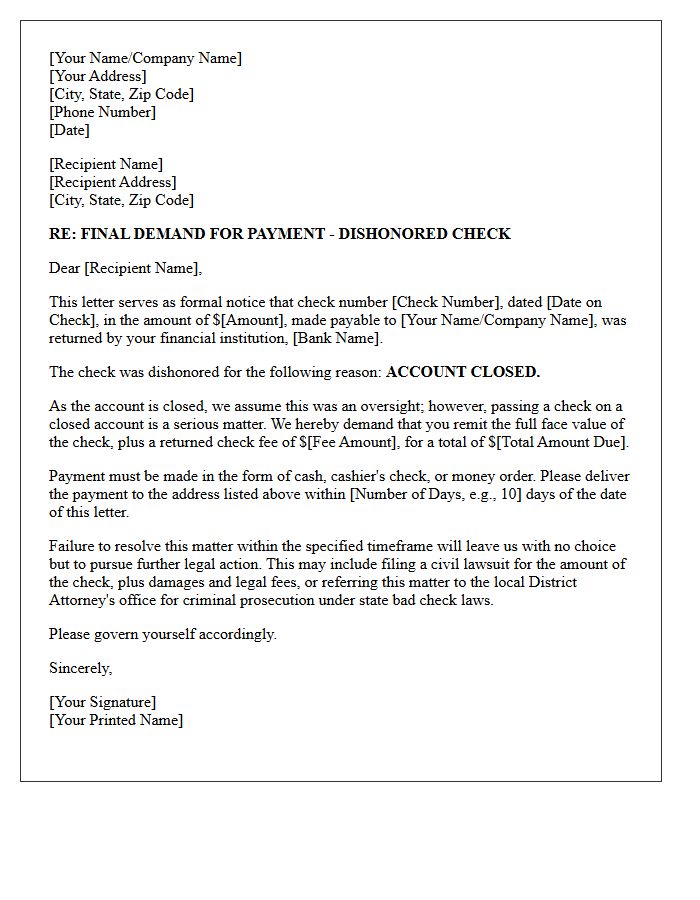

Final Demand Letter for Dishonored Check on Closed Account

A final demand letter for a dishonored check is a legal notice sent when a payment is rejected due to a closed account. It serves as a formal ultimatum, requiring the debtor to pay the full amount plus applicable statutory fees within a specific timeframe, often thirty days. Sending this notice is a mandatory prerequisite for pursuing civil litigation or criminal charges in many jurisdictions. To protect your rights, ensure the letter is sent via certified mail with a return receipt to provide proof of delivery for potential court proceedings.

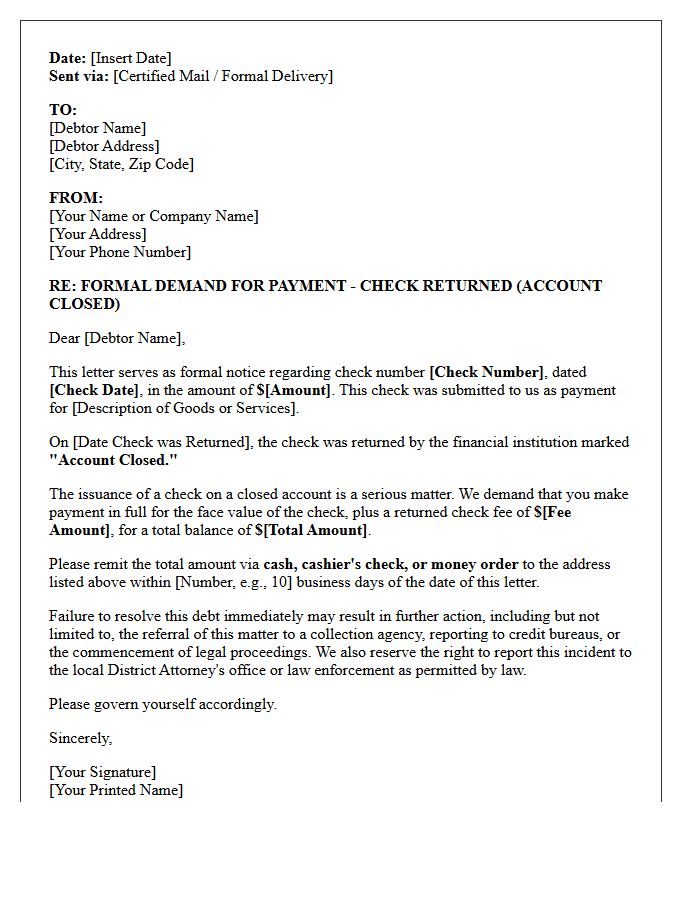

Formal Debt Collection Letter for Bounced Check from Closed Account

Receiving a formal debt collection letter for a check written from a closed account is a serious legal matter. This document serves as an official demand for payment, often citing state-specific bad check laws. It is essential to verify the debt's validity immediately to avoid potential civil penalties or criminal charges for fraud. You must respond within the specified timeframe to negotiate a settlement or provide proof of error. Timely action prevents further litigation and protects your credit score from the long-term impact of an unresolved financial judgment.

Official Warning Letter Regarding Dishonored Check on Closed Account

Receiving an official warning letter for a dishonored check on a closed account is a serious legal matter. This notification indicates that a payment was rejected because the underlying bank account no longer exists. Under many jurisdictions, issuing checks from closed accounts can be classified as fraud or criminal intent. To avoid potential litigation or criminal charges, the recipient must immediately provide restitution, typically including the original amount plus administrative fees, within the specified legal timeframe to resolve the debt and prevent further prosecution.

Legal Action Pending Letter for Closed Account Dishonored Check

Receiving a legal action pending letter for a closed account indicates that a dishonored check has triggered potential litigation. This formal notice warns that the creditor may pursue a civil lawsuit to recover the debt plus statutory damages. To avoid court costs and negative credit reporting, you must respond immediately to verify the claim and settle the balance. Ignoring this document often leads to a default judgment or wage garnishment. It is crucial to document all communication and seek legal counsel if you dispute the validity of the underlying transaction.

Urgent Payment Demand Letter for Dishonored Check Due to Closed Account

Receiving or sending an Urgent Payment Demand Letter is the critical first step after a check is returned for a closed account. This formal notice serves as legal evidence that the payer was informed of the dishonored instrument. To avoid potential civil penalties or criminal bad check charges, the issuer must typically provide full restitution within a specific statutory timeframe. Promptly addressing this demand is essential to resolve the financial liability and prevent further litigation or additional collection fees associated with the unpaid debt.

Notice of Returned Check Letter for Closed Bank Account

A Notice of Returned Check Letter informs a recipient that their payment failed because it was drawn on a closed bank account. This formal document serves as legal notification, demanding immediate repayment of the original balance plus applicable NSF fees. It is crucial to address this notice promptly to avoid potential civil litigation or criminal prosecution for fraud. Most jurisdictions require a specific cure period, typically ten days, for the debtor to provide certified funds before further legal action is taken to recover the outstanding debt.

Debt Recovery Letter for Dishonored Check on Closed Account

Receiving a debt recovery letter for a dishonored check on a closed account requires immediate action. This notice signifies that a payment failed because the bank account was inactive, potentially leading to civil penalties or criminal charges under state bad check laws. It is essential to verify the debt's legitimacy and respond within the specified timeframe to prevent legal escalation. Resolving the balance promptly helps protect your credit score and avoids additional collection fees or litigation initiated by the payee or a third-party recovery agency.

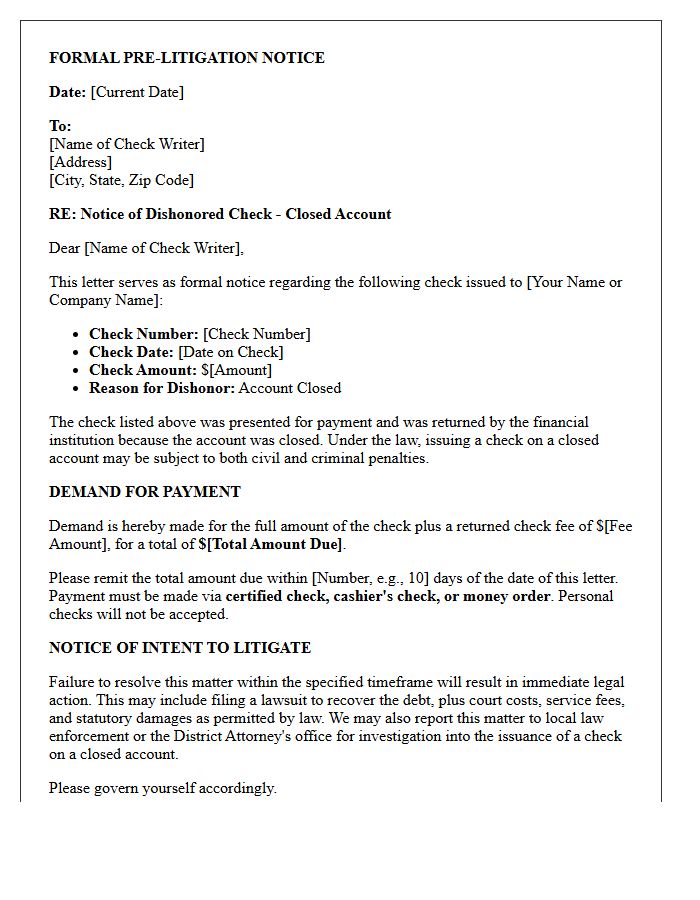

Pre-Litigation Notice Letter for Closed Account Dishonored Check

A pre-litigation notice letter for a dishonored check on a closed account serves as a formal legal demand for payment. It notifies the issuer that their payment failed due to account closure, which often carries stricter legal implications than simple insufficient funds. This document provides a final opportunity to settle the debt plus applicable fees before legal action or criminal charges are initiated. Recipients must respond within the statutory timeframe, typically 10 to 30 days, to avoid potential litigation and significant financial penalties under state commercial codes.

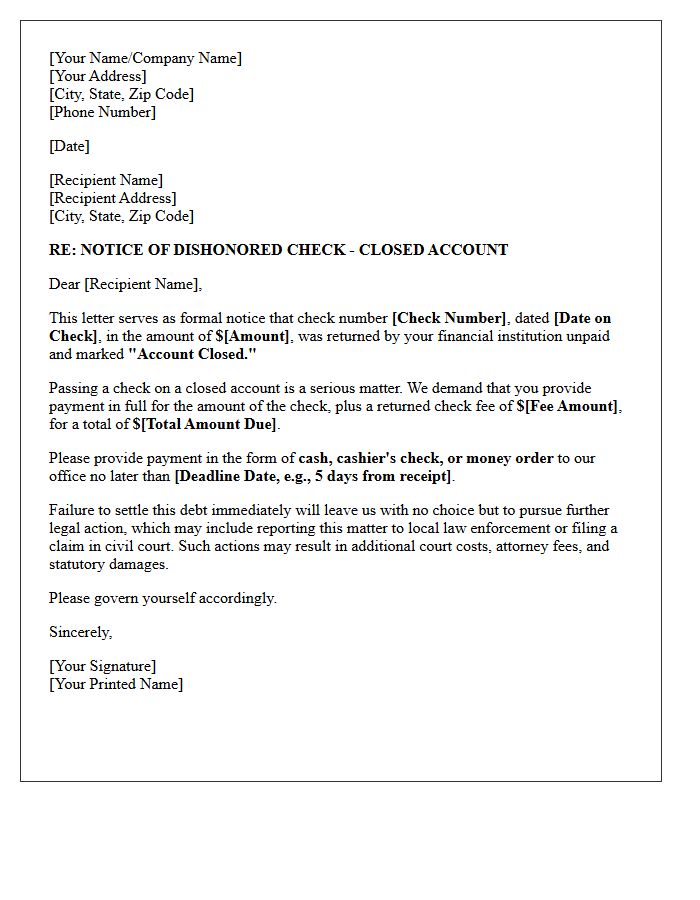

Urgent Collection Letter for Dishonored Check on a Closed Account

An Urgent Collection Letter serves as a formal demand for payment after a check is returned due to a closed account. This situation is legally significant, as issuing a check on a terminated account often suggests premeditated intent rather than a simple accounting error. The notice typically provides a strict deadline, often ten days, to settle the debt plus applicable fees before the matter escalates to legal action or criminal prosecution. Promptly addressing this notice is essential to avoid severe damage to your credit rating and potential statutory penalties.

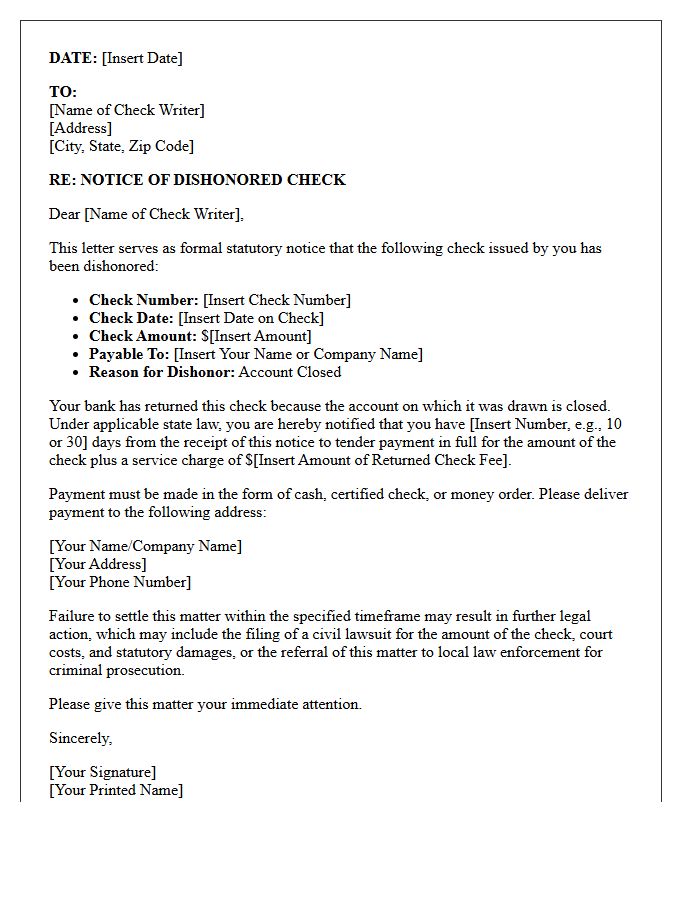

Statutory Notice Letter for Dishonored Check Due to Closed Account

A statutory notice letter is a formal legal demand sent to a drawer whose check was returned for a closed account. This document serves as an essential pre-suit requirement, providing the recipient a specific timeframe to settle the debt plus applicable fees. Failure to comply after receiving this notice can escalate the matter to criminal prosecution or civil litigation, often resulting in triple damages under state law. It acts as critical evidence of intent, proving the sender attempted to resolve the dishonored payment before pursuing further legal action.

Default Resolution Letter for Dishonored Check from Closed Account

A Default Resolution Letter is a formal notice sent when a check is returned for a closed account. This document serves as a legal demand for the original amount plus applicable bank fees. It is a critical step in debt collection, providing the issuer a final opportunity to settle the balance before the matter escalates to legal action or criminal prosecution for fraud. To protect your rights, ensure the letter includes the check number, date, and a specific deadline for repayment via guaranteed funds like a money order or cashier's check.

What is a Notice of Dishonored Check Due to Closed Account?

A Notice of Dishonored Check Due to Closed Account is a formal legal notification sent by a payee to a drawer after a bank refuses to honor a check because the associated bank account has been permanently closed. This notice serves as a demand for payment and is a required step before pursuing further legal action or criminal charges.

How long do I have to pay after receiving a notice for a closed account check?

In most jurisdictions, you typically have between 10 to 30 days from the date the notice was mailed or delivered to provide full payment. Failure to resolve the balance within this specified grace period may result in the assessment of additional collection fees, civil penalties, or the filing of criminal charges for issuing a bad check.

What are the legal consequences of writing a check on a closed account?

Writing a check on a closed account is often considered more serious than a simple "insufficient funds" error because it suggests intent to defraud. Legal consequences can include civil lawsuits for triple the amount of the check, mandatory administrative fees, and potential criminal prosecution for a misdemeanor or felony, depending on the check amount and local state laws.

What information must be included in a formal Notice of Dishonored Check?

A formal notice must include the date the check was issued, the check number, the exact dollar amount, the name of the bank that dishonored the check, and the reason for dishonor (closed account). It must also state a clear deadline for payment and provide instructions on how to remit the funds, usually via cash, certified check, or money order.

Can I be charged with a crime if I didn't know the account was closed?

While "intent" is a factor in criminal law, the act of writing a check on a closed account often creates a legal presumption of intent to defraud. To avoid criminal liability, the drawer must immediately pay the full amount plus any applicable fees upon receiving the Notice of Dishonored Check to demonstrate a good-faith effort to rectify the error.

Comments