Protect your financial rights by effectively addressing an Improper Debt Assignment dispute notice. When creditors transfer accounts unlawfully, you must demand documented proof of ownership and legal standing to collect. Understanding the correct validation process ensures you aren't paying the wrong entity. Learn how to challenge these claims and safeguard your credit score. Below are some ready to use template.

Image cover: Mastering Your Response: Professional Templates for Improper Debt Assignment Disputes

Letter Samples List

- Acknowledgment Letter for Improper Debt Assignment Dispute Notice

- Validation Letter Verifying Proper Debt Assignment and Chain of Title

- Response Letter Rejecting Improper Debt Assignment Claims

- Verification Letter Enclosing Bill of Sale for Debt Assignment Dispute

- Inquiry Letter Requesting Clarification on Debt Assignment Dispute Notice

- Collection Resumption Letter Following Debt Assignment Dispute Review

- Notification Letter Redirecting Debt Assignment Dispute to Original Creditor

- Final Resolution Letter Regarding Improper Debt Assignment Dispute Notice

- Account Closure Letter Following Unverifiable Debt Assignment Dispute

- Response Letter Providing Original Creditor Affidavit for Assignment Dispute

- Clarification Letter Explaining Legal Standing in Debt Assignment Dispute

- Response Letter Addressing Frivolous Improper Debt Assignment Dispute Notice

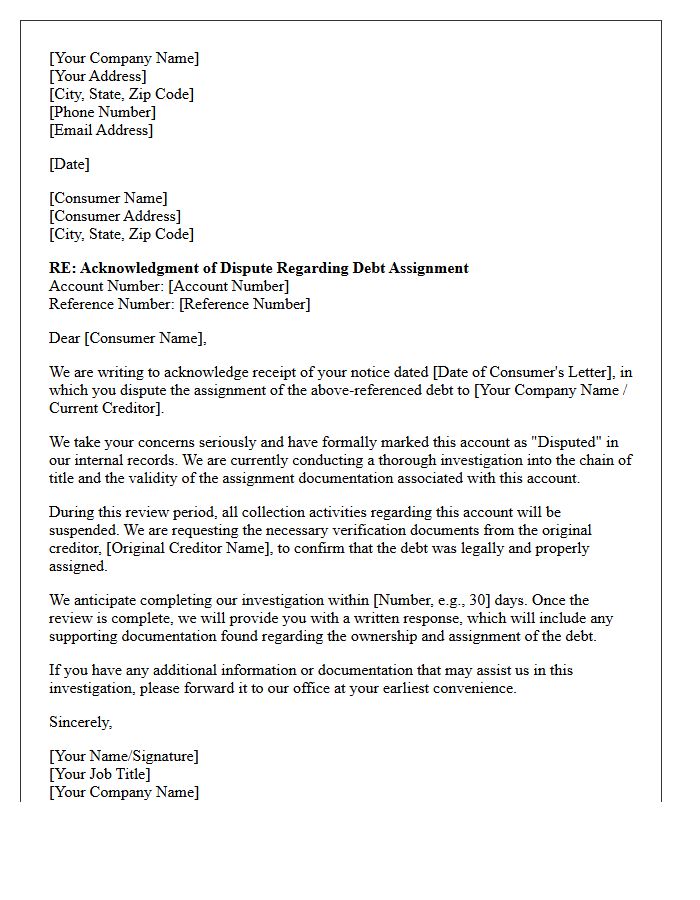

Acknowledgment Letter for Improper Debt Assignment Dispute Notice

An acknowledgment letter confirms a creditor or collection agency has received your dispute notice regarding an improper debt assignment. This document is essential for legal protection under fair debt collection laws. It serves as proof that the agency is aware the debt may be misassigned, undocumented, or legally unenforceable. Upon receipt, the collector must typically cease collection activities until they provide verification of the debt's ownership. Keep this letter as evidence to safeguard your credit report and prevent further harassment during the investigation process.

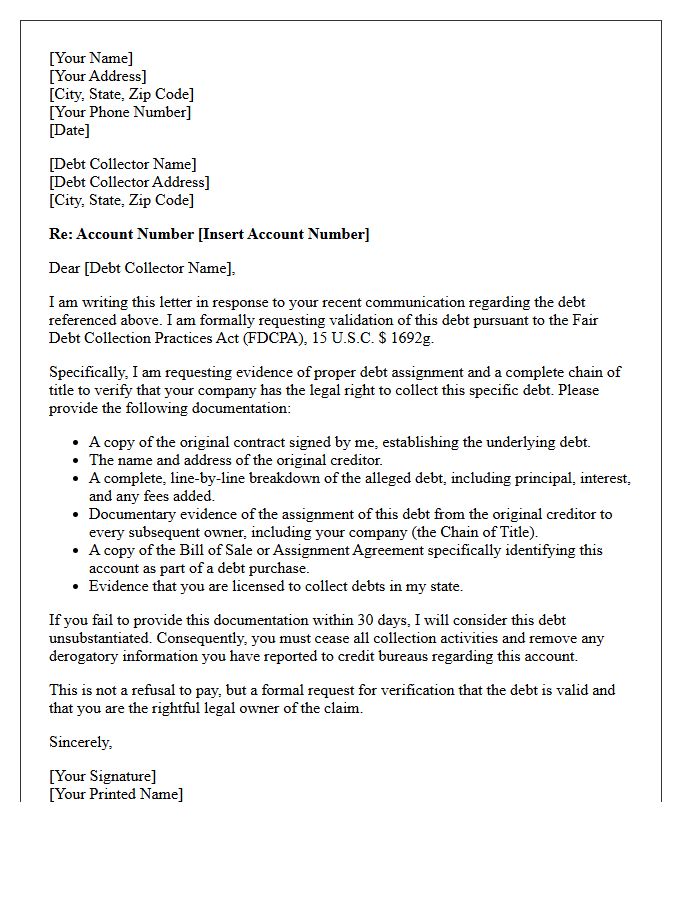

Validation Letter Verifying Proper Debt Assignment and Chain of Title

A debt validation letter is crucial for ensuring a collector has the legal right to pursue payment. It must verify the chain of title, providing documented proof of how the debt was transferred from the original creditor to the current owner. Without a proper debt assignment, the collector may lack the legal standing to sue or report to credit bureaus. Always demand a complete, unbroken paper trail to confirm the collector's authority and the accuracy of the balance before making any payments or acknowledging the debt.

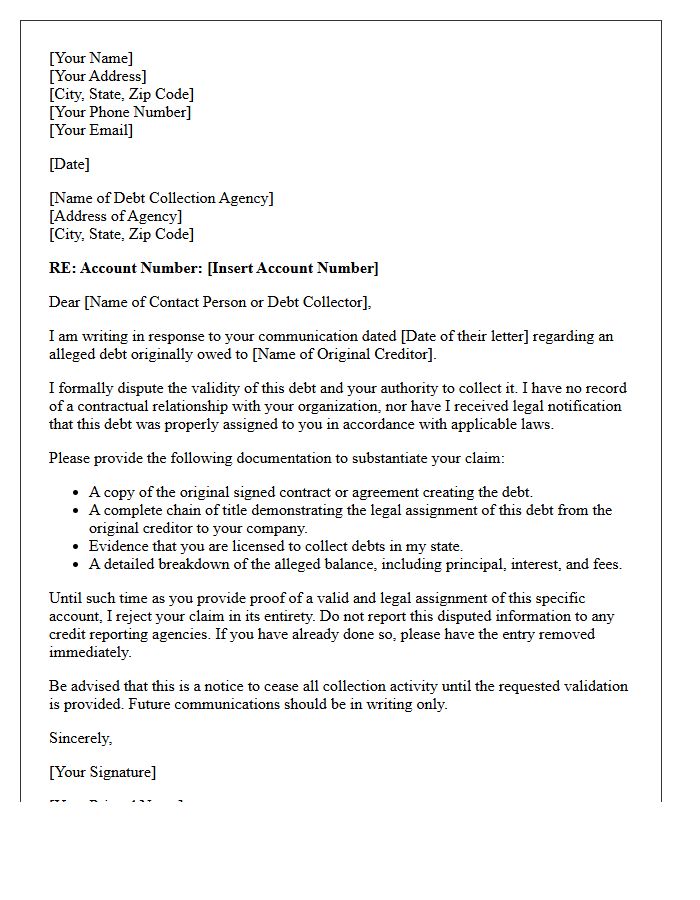

Response Letter Rejecting Improper Debt Assignment Claims

A formal response letter rejecting improper debt assignment claims must clearly state that the assignment of debt is legally invalid. You should demand validated proof of the transfer, such as the original agreement and a complete chain of title. Explicitly notify the collector that their claim lacks documentation, rendering it unenforceable under consumer protection laws. If the collector fails to provide verified evidence, they must cease all collection activities. Documenting this rejection protects your credit score and legal rights against unverified third-party claims and potential harassment.

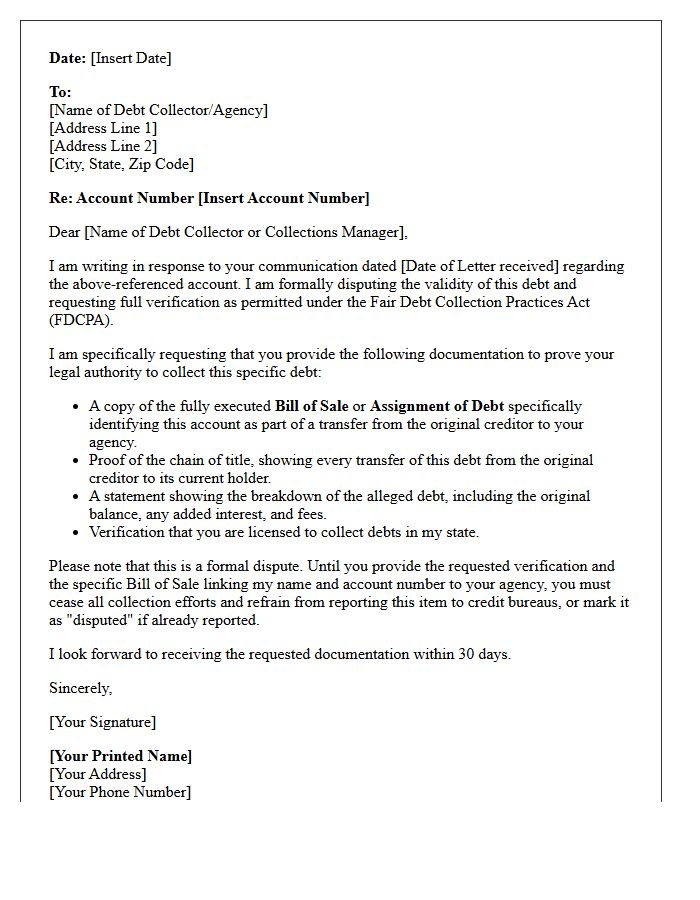

Verification Letter Enclosing Bill of Sale for Debt Assignment Dispute

When disputing a debt assignment, a Verification Letter is essential to demand proof of ownership. You must request a Bill of Sale to confirm the legal transfer of the debt from the original creditor to the collection agency. This document serves as vital evidence that the collector has the legal right to pursue the balance. Without a valid assignment trail, the debt may be unenforceable. Always send this request via certified mail to maintain a paper trail for your records and potential legal protection under consumer rights acts.

Inquiry Letter Requesting Clarification on Debt Assignment Dispute Notice

An Inquiry Letter is essential when you receive a debt assignment notice that seems inaccurate. You must formally request clarification to verify the legal transfer of ownership and the total amount claimed. This written dispute forces the new creditor to provide debt validation documents, ensuring they have the legal right to collect. Clearly state your intent to contest the balance and ask for a detailed payment history. Sending this letter via certified mail protects your consumer rights and prevents unauthorized collection activities while the dispute is being investigated.

Collection Resumption Letter Following Debt Assignment Dispute Review

A Collection Resumption Letter confirms that a debt collector is restarting recovery efforts after a dispute review. Following the assignment of debt, the agency must investigate any contested claims regarding balance accuracy or liability. Once they provide debt validation and verify the legal right to collect, the suspension period ends. This formal notice serves as legal notification that the account is active again. Consumers should carefully review the provided evidence to ensure all dispute resolutions align with their records before arranging payments or further challenging the debt's validity under consumer protection laws.

Notification Letter Redirecting Debt Assignment Dispute to Original Creditor

A notification letter regarding a debt assignment dispute informs the debtor that their dispute must be addressed directly with the original creditor. When a debt is transferred or assigned, the new assignee may redirect legal or factual challenges back to the source of the account. This redirection ensures that the party with the original documentation verifies the debt's validity. It is a critical step in the debt validation process, confirming that all records are accurate before further collection efforts proceed under the new ownership.

Final Resolution Letter Regarding Improper Debt Assignment Dispute Notice

A Final Resolution Letter regarding an improper debt assignment dispute is a critical document confirming that a collection agency has permanently ceased recovery efforts. It serves as formal evidence that the debt ownership transfer was legally flawed or invalid. This letter protects consumers by ensuring the disputed balance is removed from internal records and credit reports. Retaining this notice is essential for preventing future re-trafficking of the voided debt to other collectors, providing a definitive legal shield against repeated collection attempts for the same invalidated claim.

Account Closure Letter Following Unverifiable Debt Assignment Dispute

An Account Closure Letter serves as formal confirmation that a financial institution has ceased collection activities due to an unverifiable debt assignment. When a creditor cannot provide proof of legal ownership or original contract documentation, they must stop reporting the debt. This letter is crucial for your records, as it prevents future collection attempts and provides the necessary evidence to remove inaccurate entries from your credit report. Ensuring you have this written verification protects your consumer rights and prevents the debt from being resold to another agency.

Response Letter Providing Original Creditor Affidavit for Assignment Dispute

When disputing an account assignment, a response letter must include a notarized affidavit from the original creditor to prove the legal transfer of debt. This document establishes the chain of title, confirming that the debt buyer has the actual authority to collect. Without this sworn statement, the collector may lack the legal standing to pursue the claim. Ensure the affidavit explicitly identifies your specific account and balance to successfully resolve the ownership dispute and protect your consumer rights under fair debt collection practices.

Clarification Letter Explaining Legal Standing in Debt Assignment Dispute

A clarification letter regarding legal standing is essential in a debt assignment dispute to challenge a creditor's right to collect. This document demands proof of ownership through a complete chain of title, ensuring the claimant has a valid legal interest. By addressing standing to sue, a debtor can contest whether the current collector possesses the necessary documentation to enforce the debt legally. Providing clear evidence or questioning the validity of assignment can effectively halt unauthorized collection efforts or serve as a critical defense in potential litigation scenarios.

Response Letter Addressing Frivolous Improper Debt Assignment Dispute Notice

A response letter addressing a frivolous debt assignment dispute must provide clear evidence of a valid legal transfer. It is essential to include the Notice of Assignment, which proves the creditor's right to collect. The response should specifically refute claims of improper documentation by attaching the original contract and a detailed chain of title. Using a professional tone ensures compliance with Fair Debt Collection Practices Act (FDCPA) guidelines. Promptly delivering this verification of debt protects the agency's legal standing and prevents further meritless disputes regarding the ownership of the outstanding balance.

What is a response to an improper debt assignment dispute notice?

This response is a formal communication from a creditor or debt buyer addressing a consumer's claim that a debt was transferred or assigned without proper legal documentation or authorization. It serves to either validate the assignment with proof or acknowledge a correction in the account records.

What evidence is required to prove a legal debt assignment?

To prove a valid assignment, the responder must typically provide a "Bill of Sale" or an "Assignment and Assumption Agreement." These documents must clearly show the specific account was included in the transfer from the original creditor to the current holder, maintaining an unbroken chain of title.

How should a company respond if a debt assignment error is identified?

If the dispute reveals that the debt was assigned improperly, the company should immediately cease collection efforts, notify credit reporting agencies to remove any related derogatory marks, and provide the consumer with written confirmation that the account is being closed or returned to the prior owner.

What is the timeframe for responding to an improper debt assignment dispute?

Under the Fair Debt Collection Practices Act (FDCPA), debt collectors must provide verification of the debt if disputed within the initial 30-day validation period. While there is no universal deadline for subsequent disputes, a timely response within 30 days is industry standard to avoid regulatory scrutiny.

Can a debt collector continue reporting to credit bureaus during an assignment dispute?

Once a consumer disputes the validity of a debt assignment, the collector must mark the account as "disputed" on credit reports. If the collector cannot provide evidence of a legal assignment, they must stop reporting the debt entirely until the ownership chain is verified.

Comments