Receiving a Credit Card Missed Payment Initial Warning Letter is a formal notice from your lender regarding an overdue balance. This notification serves as a critical reminder to settle your debt before late fees or credit score damage occur. Addressing the issue promptly helps maintain your financial standing. To assist you, below are some ready to use template options.

Image cover: Late Payment Notice: Essential Credit Card Warning Letter Templates and Samples

Letter Samples List

- Initial Courtesy Reminder Credit Card Payment Letter

- First Notice of Missed Credit Card Payment Letter

- Account Past Due Initial Warning Letter

- Urgent Outstanding Credit Card Balance Letter

- Action Required Missed Credit Card Installment Letter

- Friendly Reminder Overdue Account Status Letter

- Pre-Collection Initial Credit Card Warning Letter

- Immediate Attention Past Due Account Letter

- First Stage Delinquency Notification Letter

- Credit Card Default Prevention Warning Letter

- Overdue Statement and Initial Warning Letter

- Unpaid Credit Card Balance Notification Letter

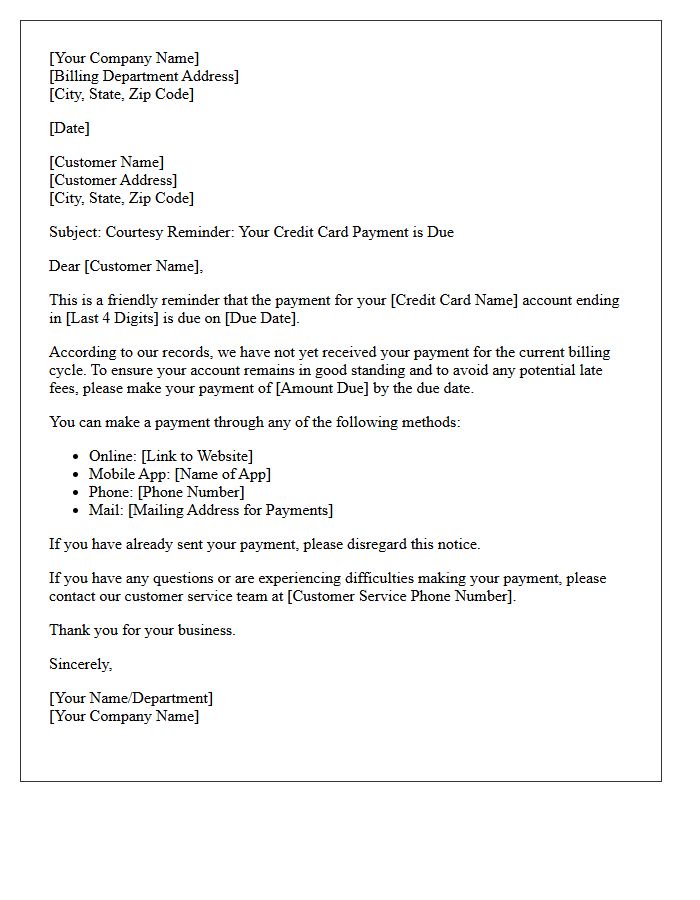

Initial Courtesy Reminder Credit Card Payment Letter

An Initial Courtesy Reminder is a proactive communication sent to cardholders shortly before or after a payment due date. This letter serves as a soft nudge to ensure customers maintain a positive credit standing. It typically outlines the total balance due, the minimum payment required, and the specific deadline. By emphasizing account security and financial health, this notice helps users avoid late fees and potential interest charges. It is an essential tool for maintaining transparent communication between the financial institution and the borrower while preventing inadvertent missed payments.

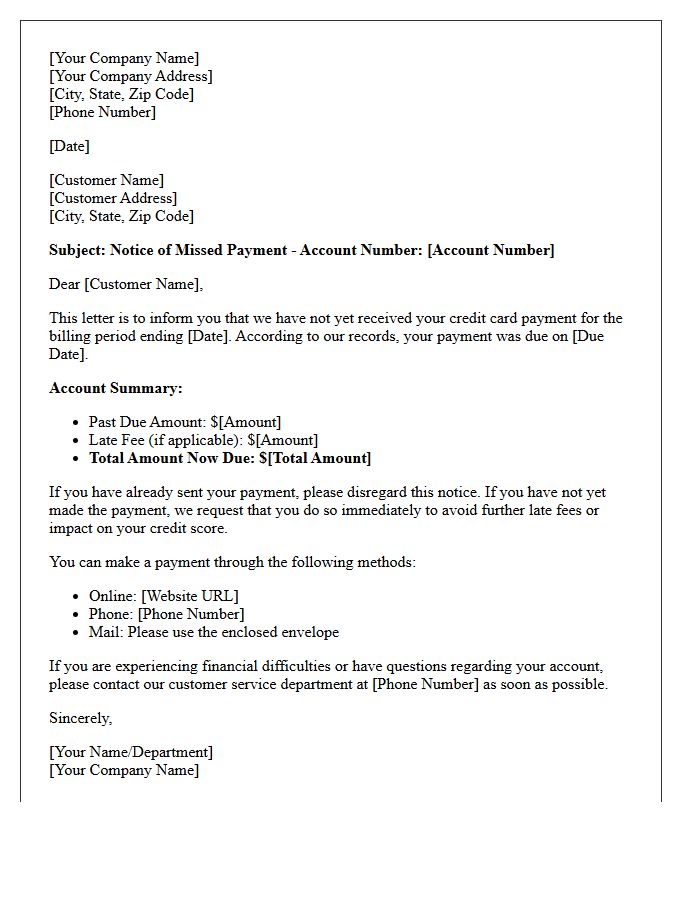

First Notice of Missed Credit Card Payment Letter

Receiving a First Notice of Missed Credit Card Payment is a critical warning that your account is past due. To protect your credit score, you must pay the minimum balance immediately before the delinquency reaches the thirty-day mark. Most lenders provide a short grace period where they may waive the initial late fee if you contact them promptly. Addressing this notice quickly prevents negative reporting to credit bureaus, avoids penalty interest rates, and ensures your account remains in good standing to maintain your financial reputation.

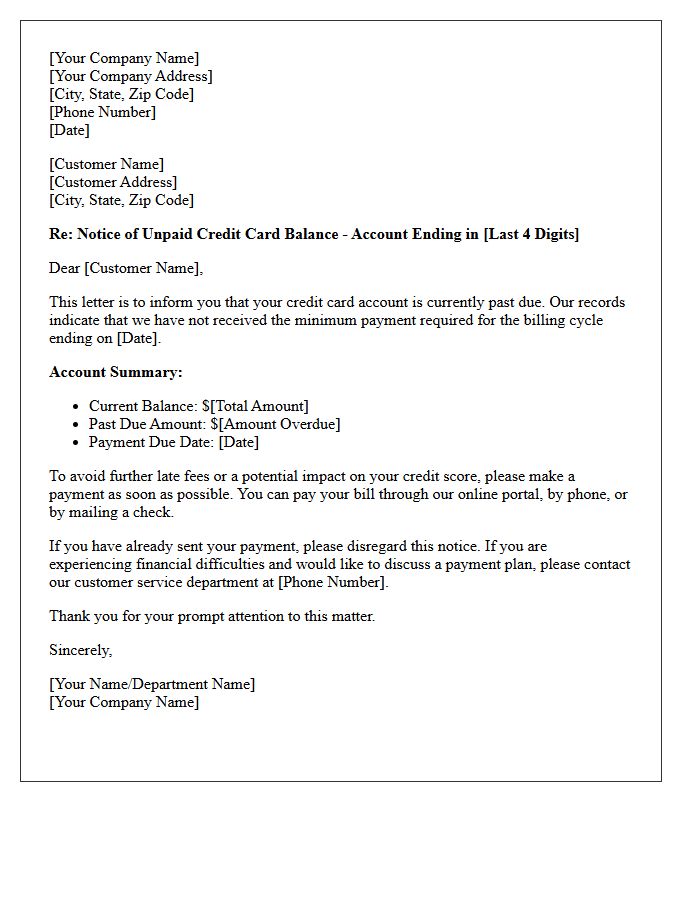

Account Past Due Initial Warning Letter

An Initial Warning Letter serves as a formal notification that an account is past due. This document acts as a professional reminder to settle an outstanding balance before late fees or credit penalties apply. It must clearly state the exact amount owed, the original due date, and available payment methods. Promptly addressing this notice is crucial to maintaining a positive business relationship and protecting your credit score. Treating this initial communication with urgency helps avoid escalated collection actions or service interruptions.

Urgent Outstanding Credit Card Balance Letter

An Urgent Outstanding Credit Card Balance Letter is a formal notice demanding immediate payment to resolve overdue debt. This legal communication warns of serious consequences, including credit score damage, penalty fees, and potential account suspension. It is essential to contact the issuer promptly to discuss repayment plans or settlements to avoid debt collection agencies. Ignoring this final notice can lead to long-term financial instability. Always verify the total balance and due date mentioned in the letter to ensure accuracy and protect your consumer rights under fair debt collection laws.

Action Required Missed Credit Card Installment Letter

Receiving an Action Required Missed Credit Card Installment Letter demands immediate attention to avoid severe financial consequences. This formal notice indicates a late payment that could trigger penalty fees, increased interest rates, and negative reporting to credit bureaus. To protect your credit score, you must quickly settle the outstanding balance or contact your bank to discuss a repayment plan. Ignoring this communication may lead to account suspension or debt collection efforts. Timely resolution is essential to maintain your financial standing and prevent long-term damage to your borrowing capacity.

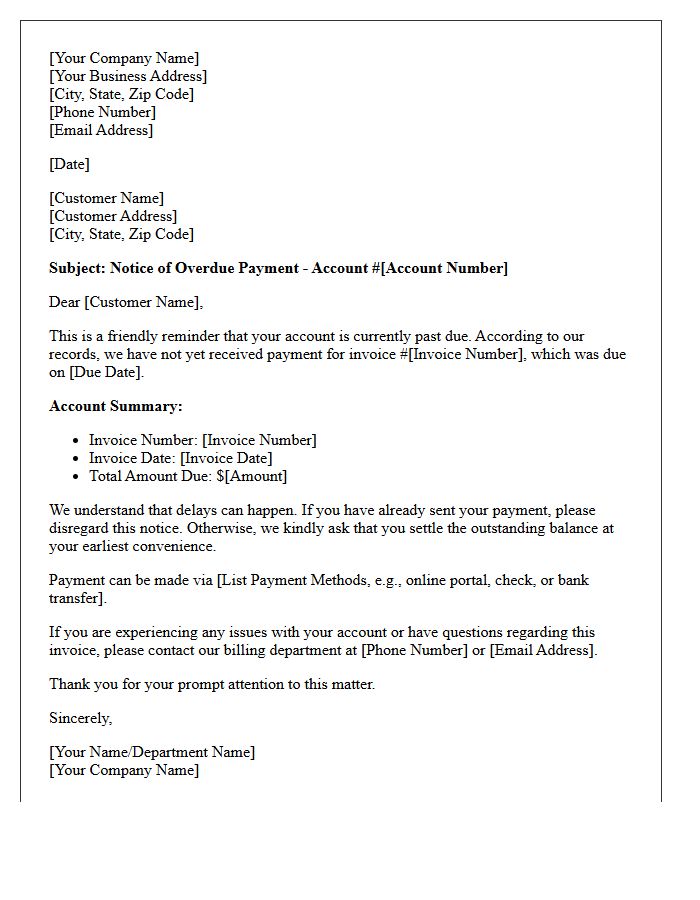

Friendly Reminder Overdue Account Status Letter

A Friendly Reminder Overdue Account Status Letter serves as a professional nudge to resolve unpaid invoices while maintaining a positive client relationship. It is essential to include the specific outstanding balance, original due date, and clear payment instructions. Use a polite yet firm tone to encourage immediate action without causing offense. Mentioning available support or payment plans can help overcome financial hurdles. Prompt communication ensures cash flow stability and prevents the account from escalating to formal collection stages or incurring late fees.

Pre-Collection Initial Credit Card Warning Letter

A Pre-Collection Initial Credit Card Warning Letter is a formal notice sent by creditors before escalating debt to a third-party agency. This document serves as a final opportunity for cardholders to settle outstanding balances or negotiate a payment plan. It details the total amount owed, late fees, and a specific deadline for action. Receiving this letter is critical because it marks the last stage to protect your credit score from the severe negative impact of a formal collection entry on your financial record.

Immediate Attention Past Due Account Letter

An Immediate Attention Past Due Account Letter serves as a final formal notice to resolve an outstanding debt. This communication emphasizes the urgency of the situation to prevent further escalation, such as service suspension or legal action. It clearly states the total balance, the original due date, and available payment methods. Receiving this letter indicates that previous reminders were ignored, making it the last opportunity to settle the balance or arrange a payment plan before the account is transferred to a collections agency or impacts your credit score.

First Stage Delinquency Notification Letter

A First Stage Delinquency Notification Letter is a formal notice sent to a debtor when a payment becomes past due. Its primary purpose is to inform the recipient of the outstanding balance and request immediate payment to avoid further collection actions. This document serves as a critical legal record of the initial attempt to recover funds. Timely communication is essential, as it allows parties to resolve payment discrepancies or establish a repayment plan before the account escalates to more severe collection stages or impacts credit scores.

Credit Card Default Prevention Warning Letter

A credit card default prevention warning letter is a critical notice sent by lenders to alert borrowers of imminent delinquency. Receiving this document signifies that your account is at risk of being charged off, which can severely damage your credit score. It typically outlines the outstanding balance, required repayment actions, and potential legal consequences. To protect your financial standing, you must contact your bank immediately to discuss hardship programs or settlement options. Proactive communication is the most effective way to resolve debt before it escalates to a formal default status.

Overdue Statement and Initial Warning Letter

An overdue statement serves as a formal reminder that an account has unpaid balances past their maturity date. It provides a clear summary of outstanding invoices to encourage prompt settlement. If payment remains ignored, an initial warning letter is issued as the first step in the debt collection process. This document notifies the debtor of potential late fees or legal escalations while maintaining a professional tone. Monitoring these notices is crucial for maintaining healthy cash flow and preserving positive business relationships before credit scores are negatively impacted.

Unpaid Credit Card Balance Notification Letter

An Unpaid Credit Card Balance Notification Letter is a formal notice sent by issuers when a cardholder misses payments. It serves as a legal record of the outstanding debt and details late fees, penalty interest rates, and the required minimum payment. Receiving this letter indicates that the account is at risk of delinquency. To avoid severe credit score damage or internal collections, you must respond immediately by making a payment or arranging a settlement plan to restore your account status and prevent further financial penalties.

What is a credit card missed payment initial warning letter?

A credit card missed payment initial warning letter is a formal notice sent by a financial institution to inform a cardholder that a scheduled payment was not received by the due date. This letter serves as a reminder to settle the overdue balance immediately to avoid late fees, interest hikes, or negative impacts on credit scores.

Will a single missed payment warning letter affect my credit score?

Typically, an initial warning letter does not impact your credit score if you pay the balance within 30 days of the original due date. Most lenders only report delinquencies to credit bureaus (like Equifax or Experian) once the payment is 30 days or more overdue.

What should I do immediately after receiving a payment warning notice?

Upon receiving the notice, you should immediately pay the minimum amount due or the full statement balance via your online banking portal or mobile app. If you cannot afford the payment, contact your bank's customer service department right away to discuss a payment plan or hardship program.

Are there penalties associated with an initial missed payment warning?

Yes, most credit card issuers will charge a late payment fee (often ranging from $25 to $40) and may revoke any introductory 0% APR offers. Additionally, your account may begin accruing interest at a higher "penalty rate" if the balance remains unpaid for an extended period.

Can I have a late fee waived after receiving a warning letter?

Many credit card issuers are willing to waive a first-time late fee as a gesture of goodwill if you have a history of on-time payments. You should call the number on the back of your card, explain the situation, and ask the representative if they can remove the charge once the payment is settled.

Comments