Managing outstanding debts requires a professional approach that balances firmness with empathy. This guide explores how to draft an effective Past Due Notice With Payment Plan Offer Letter to recover funds while maintaining positive client relationships. Learn to structure clear terms and flexible repayment options to encourage immediate action. Below are some ready to use templates.

Image cover: Friendly Payment Arrangement: Past Due Notice Templates and Samples

Letter Samples List

- First Notice Past Due Payment Plan Offer Letter

- Second Notice Past Due Payment Plan Offer Letter

- Final Warning Past Due Payment Plan Offer Letter

- Friendly Reminder Past Due Payment Plan Offer Letter

- Urgent Account Past Due Payment Plan Offer Letter

- Delinquent Balance Past Due Payment Plan Offer Letter

- Pre-Collection Past Due Payment Plan Offer Letter

- Financial Hardship Past Due Payment Plan Offer Letter

- Installment Agreement Past Due Payment Plan Offer Letter

- Medical Debt Past Due Payment Plan Offer Letter

- Commercial Invoice Past Due Payment Plan Offer Letter

- Notice of Default Past Due Payment Plan Offer Letter

- Good Faith Past Due Payment Plan Offer Letter

- Account Suspension Past Due Payment Plan Offer Letter

- Consumer Credit Past Due Payment Plan Offer Letter

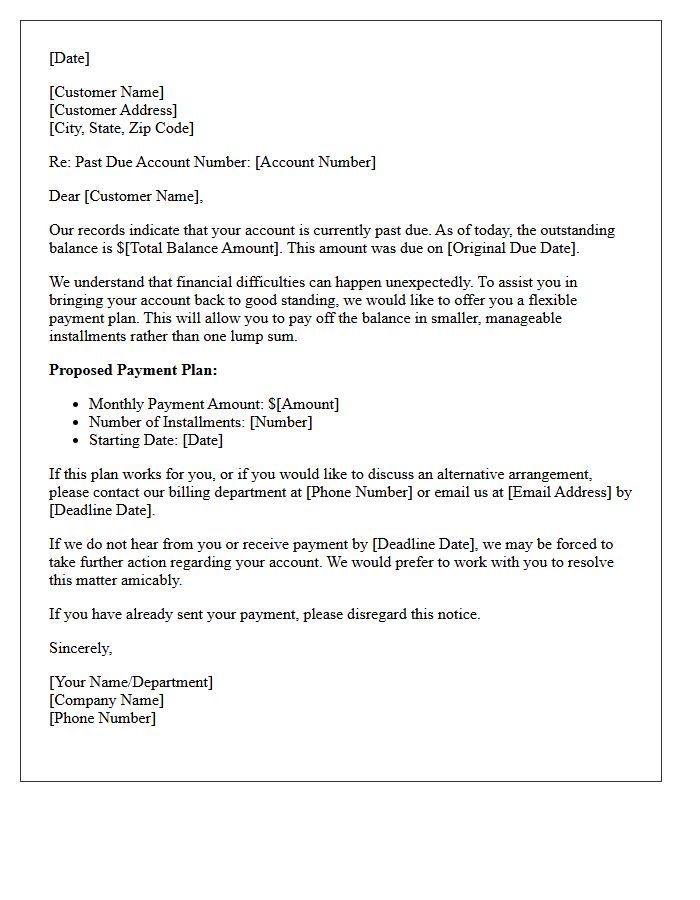

First Notice Past Due Payment Plan Offer Letter

A First Notice Past Due Payment Plan Offer Letter is a formal communication sent to debtors who have missed payments. Its primary goal is debt resolution by proposing a structured repayment schedule to settle outstanding balances. This document serves as a final opportunity to avoid aggressive collection actions or legal proceedings. Recipients should carefully review the terms and conditions, as accepting the offer creates a new, legally binding agreement that can help protect their credit score and restore financial standing with the creditor.

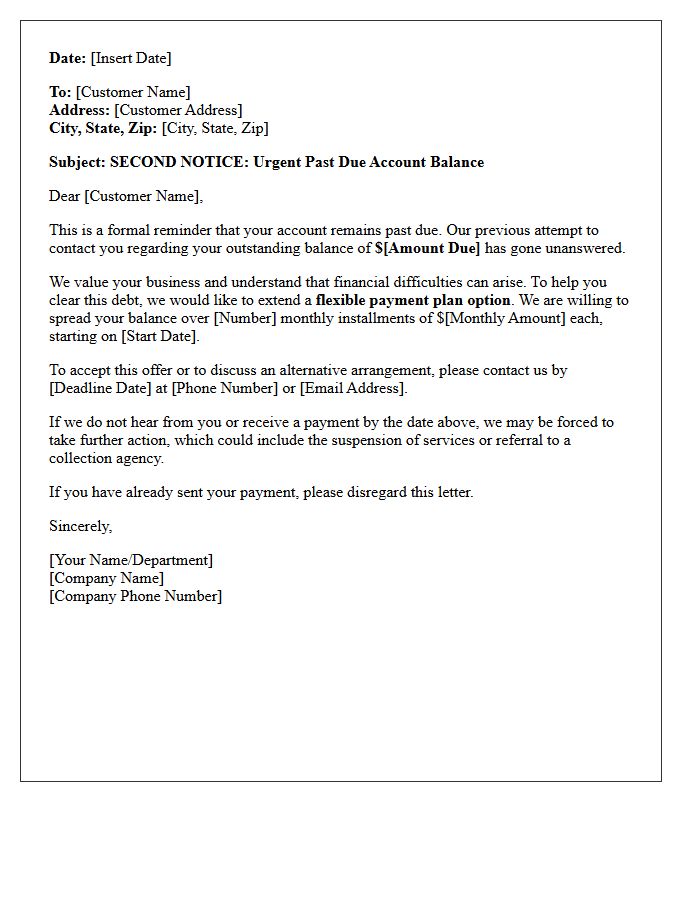

Second Notice Past Due Payment Plan Offer Letter

A Second Notice Past Due Payment Plan Offer Letter is a final formal attempt to resolve outstanding debt before escalating to collections. This urgent notification serves as a courtesy, providing structured options to settle balances through manageable installments. It is crucial to respond immediately to avoid credit score damage or legal action. By accepting the payment plan terms, you demonstrate a good-faith effort to meet your financial obligations while protecting your long-term fiscal reputation and maintaining a positive relationship with the creditor.

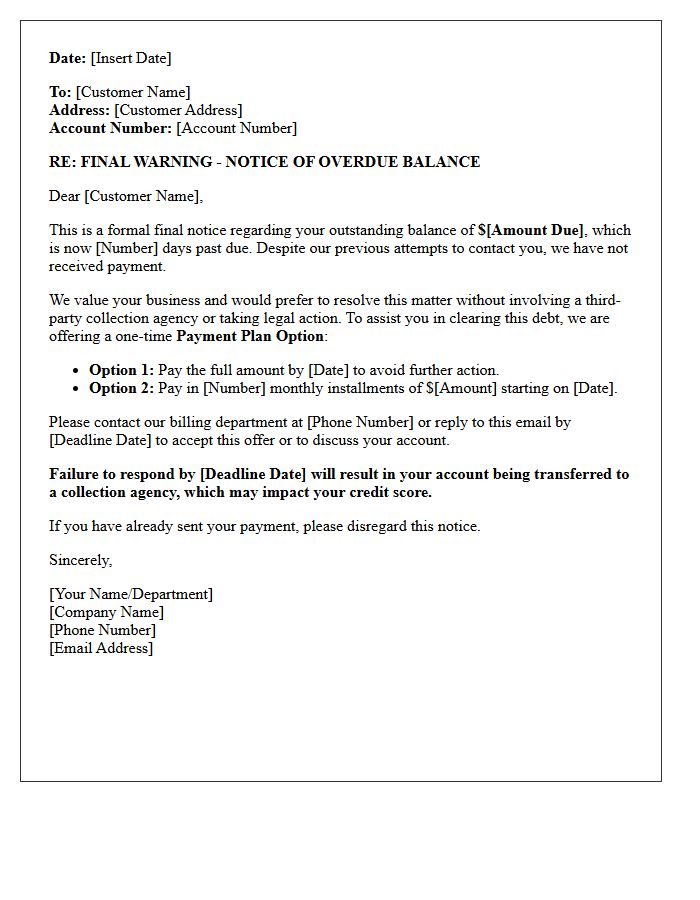

Final Warning Past Due Payment Plan Offer Letter

A Final Warning Past Due Payment Plan Offer Letter is a critical legal notice issued before debt escalation or legal action. It serves as a final opportunity to resolve outstanding balances through a structured settlement. This document outlines the total amount owed, strict deadlines, and potential consequences of non-payment. Ignoring this formal demand can lead to credit score damage or collection agency involvement. To protect your financial standing, you must either accept the offer or negotiate new terms immediately to prevent further litigation or service disconnection.

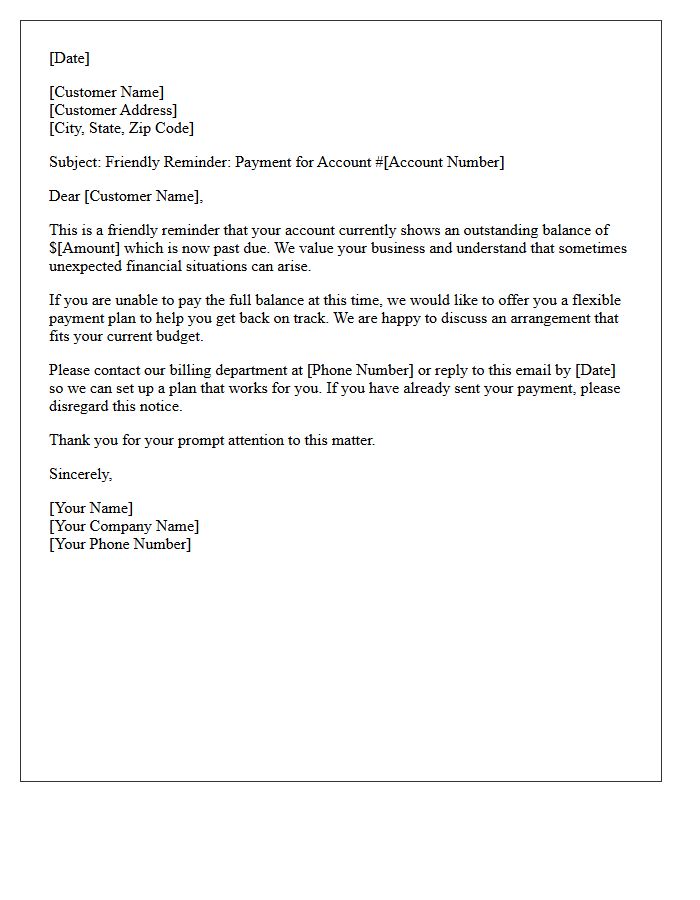

Friendly Reminder Past Due Payment Plan Offer Letter

This Friendly Reminder serves as a proactive notification regarding your past due balance. We understand that financial challenges occur, which is why we are offering a flexible Payment Plan to help you regain good standing. By accepting this offer, you can settle your debt through manageable installments while avoiding late fees or service interruptions. Please review the enclosed terms and contact us immediately to activate your plan. Resolving your account now ensures continued credit stability and prevents further collection actions on your outstanding outstanding debt.

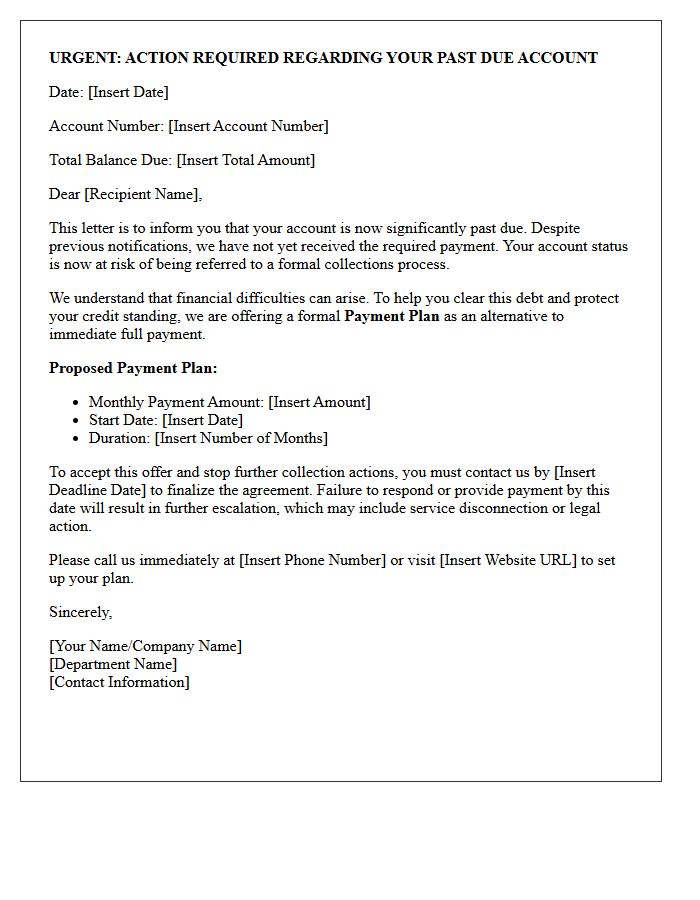

Urgent Account Past Due Payment Plan Offer Letter

An Urgent Account Past Due Payment Plan Offer Letter is a formal notice sent to customers with delinquent balances. This communication outlines a structured repayment schedule designed to resolve outstanding debt while avoiding severe consequences like service disconnection or legal action. It typically highlights a limited-time settlement offer or installment options to encourage immediate action. Reviewing these terms carefully is essential to maintaining your credit standing and securing a mutually beneficial repayment agreement before the account transitions to a collection agency.

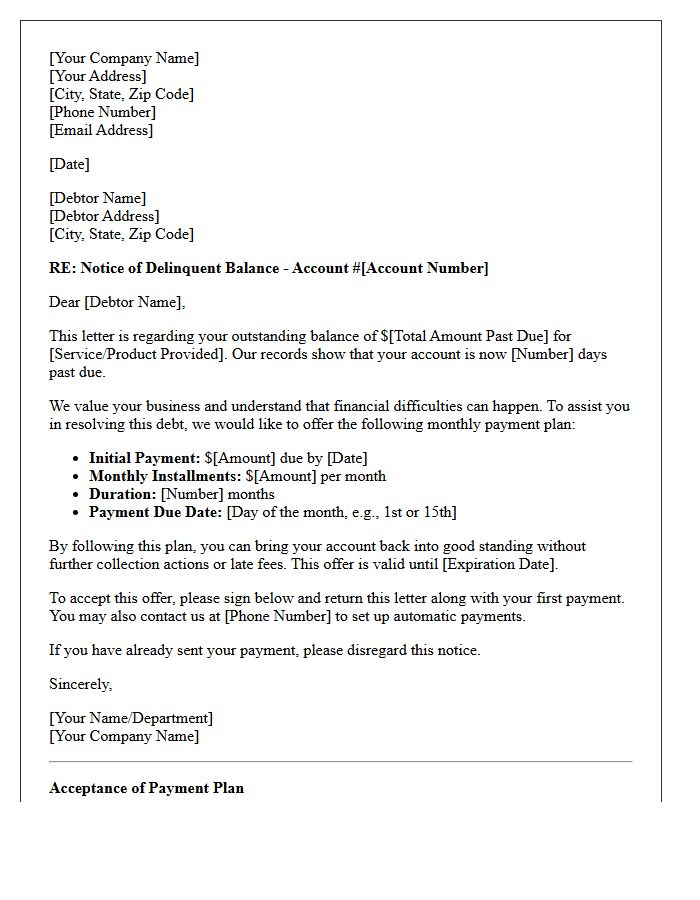

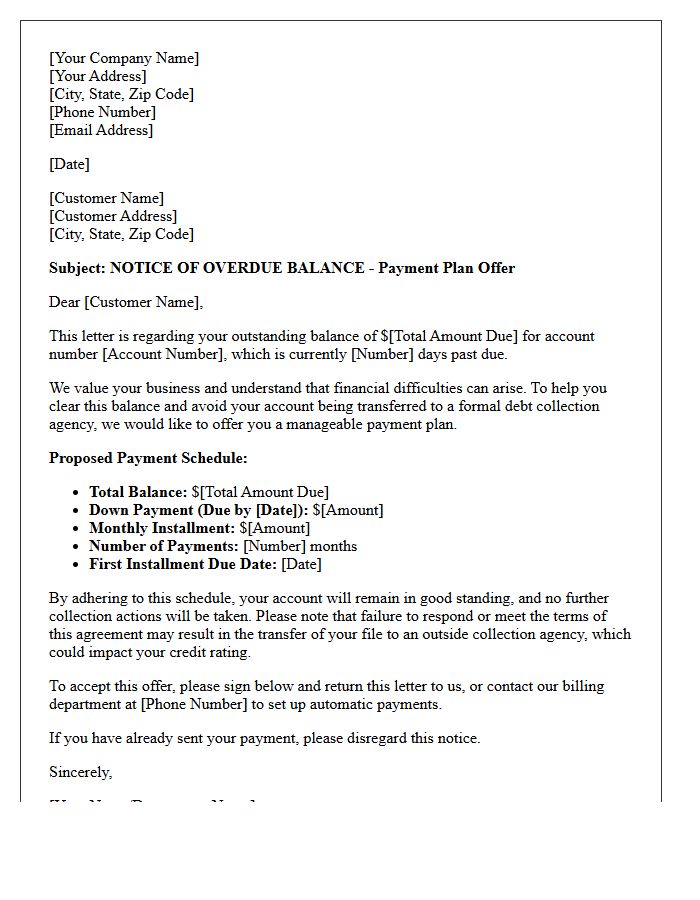

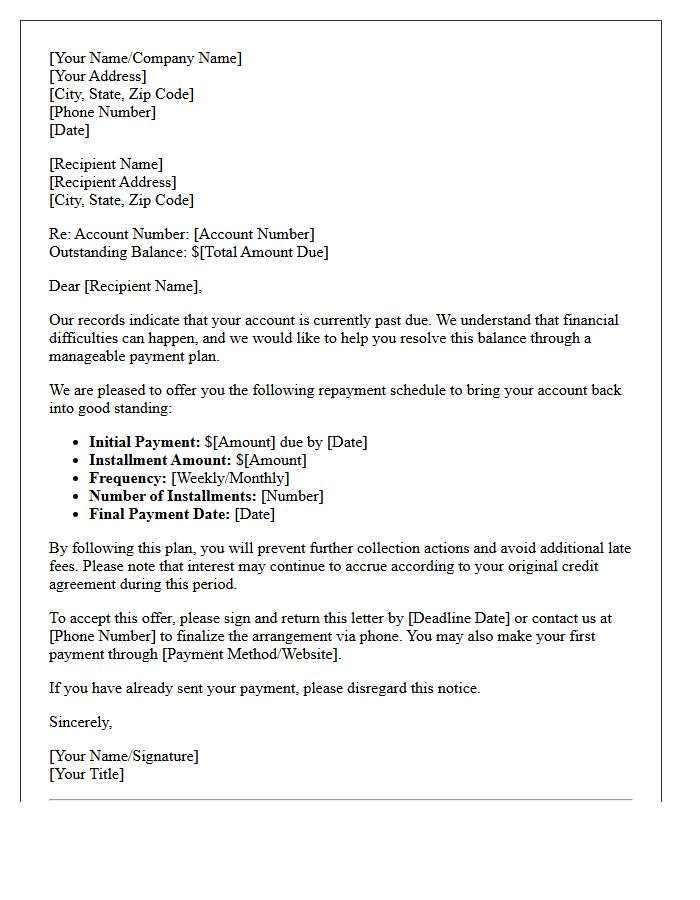

Delinquent Balance Past Due Payment Plan Offer Letter

A delinquent balance past due payment plan offer letter is a formal proposal to settle outstanding debt through structured installments. The most important goal is to prevent legal action or credit reporting damage by demonstrating a good-faith effort to pay. These letters typically outline specific payment amounts, negotiated deadlines, and potential interest waivers. Understanding the terms is crucial, as signing constitutes a binding agreement that can restore your standing with creditors while managing your financial liquidity effectively. Always verify the remaining balance before committing to a long-term repayment schedule.

Pre-Collection Past Due Payment Plan Offer Letter

A Pre-Collection Past Due Payment Plan Offer Letter is a formal notice sent before an account is assigned to a collection agency. It serves as a final opportunity for debtors to resolve outstanding balances through flexible repayment terms. By accepting this offer, individuals can avoid negative impacts on their credit scores and prevent legal action. These letters typically outline specific installment amounts and deadlines, aiming to facilitate a mutually beneficial settlement. Responding promptly to these offers helps maintain financial stability and preserves the professional relationship between the creditor and the consumer.

Financial Hardship Past Due Payment Plan Offer Letter

A financial hardship past due payment plan offer letter is a formal proposal sent to creditors to resolve delinquent debt. It explains your current financial limitations while demonstrating a proactive commitment to repayment. This document typically requests a temporary reduction in monthly installments or a settled lump-sum payment. To ensure effectiveness, include specific details regarding your income, essential expenses, and a realistic timeframe for the proposed schedule. Clearly outlining these terms helps prevent legal action or further credit damage by establishing a mutually beneficial agreement during difficult economic periods.

Installment Agreement Past Due Payment Plan Offer Letter

An Installment Agreement is a formal IRS arrangement allowing taxpayers to settle tax debt through monthly payments. If you receive a past due payment plan offer letter, it indicates you are eligible to resolve delinquent balances before aggressive collection actions begin. Review the proposed terms, including monthly amounts and interest rates, to ensure affordability. Timely acceptance prevents levies or liens. Always verify the letter's authenticity to avoid scams and confirm that all tax compliance requirements, such as current filings, are met before finalizing the agreement.

Medical Debt Past Due Payment Plan Offer Letter

A medical debt past due payment plan offer letter is a formal proposal to settle outstanding balances through manageable installments. It is crucial to verify the debt accuracy before signing any agreement. Ensure the letter clearly outlines the monthly payment amount, the total repayment period, and a guarantee that no further interest will accrue. Always request written confirmation that consistent payments will prevent the account from being referred to third-party collections or negatively impacting your credit score. Reviewing these terms protects your financial health while resolving healthcare liabilities.

Commercial Invoice Past Due Payment Plan Offer Letter

A Commercial Invoice Past Due Payment Plan Offer Letter is a professional proposal sent to creditors to resolve delinquent balances. It outlines a structured repayment schedule, demonstrating a good-faith commitment to settle debts while preserving business relationships. This formal document should specify the total amount owed, proposed installment amounts, and specific payment dates. By proactively offering a settlement strategy, businesses can avoid legal escalation, minimize late fees, and maintain a positive credit standing during temporary cash flow challenges.

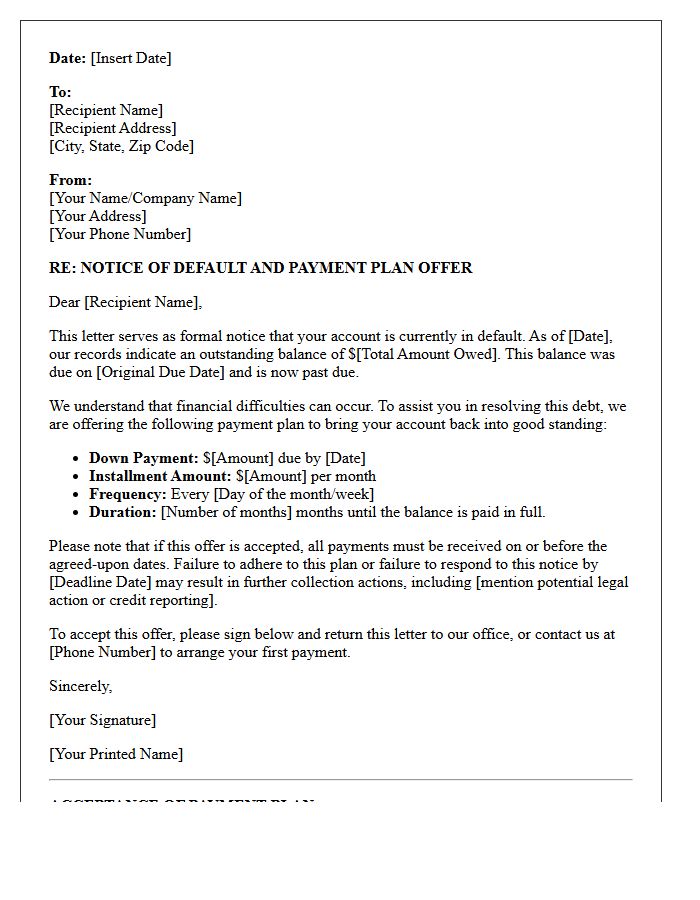

Notice of Default Past Due Payment Plan Offer Letter

A Notice of Default confirms your loan is officially delinquent, but a Past Due Payment Plan Offer provides a critical opportunity to avoid foreclosure. This legal document outlines a repayment schedule designed to resolve arrears over a specific period. It is essential to review the terms immediately, as missing deadlines can lead to permanent property loss. By formalizing a reinstatement agreement, you can stabilize your finances and protect your credit score. Always verify the lender's requirements and ensure all signatures are submitted before the foreclosure process escalates further.

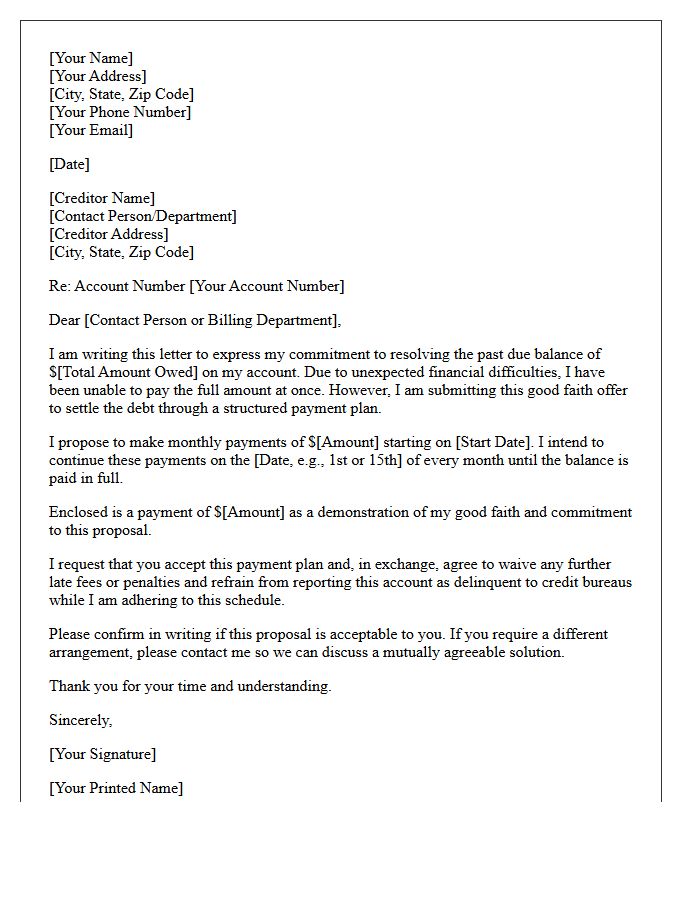

Good Faith Past Due Payment Plan Offer Letter

A Good Faith Past Due Payment Plan Offer Letter is a formal proposal sent by a debtor to a creditor to resolve outstanding debt. This document demonstrates your sincere intention to pay while acknowledging financial hardships. By offering a voluntary partial payment immediately, you build trust and show reliability. Clearly outline a specific repayment schedule and request a temporary halt on late fees or legal actions. Using this proactive approach can prevent credit damage and help you negotiate more favorable settlement terms while maintaining a positive professional relationship with your lender.

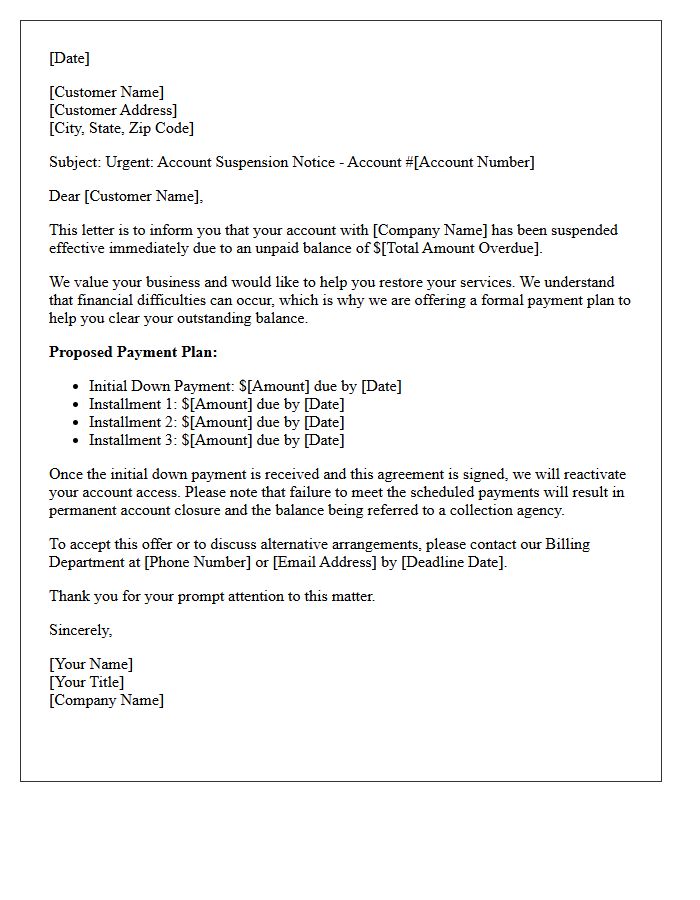

Account Suspension Past Due Payment Plan Offer Letter

Receiving an Account Suspension Past Due Payment Plan Offer Letter is a final opportunity to prevent service disconnection. This formal notice outlines a structured repayment schedule designed to resolve your outstanding balance over time. It is crucial to accept the terms by the specified deadline to maintain account standing. Failing to adhere to the agreed installment plan will result in immediate suspension and potential collection actions. Always verify the repayment dates and total amounts to ensure your services remain active while you settle your debt.

Consumer Credit Past Due Payment Plan Offer Letter

A Consumer Credit Past Due Payment Plan Offer Letter is a formal proposal sent by a creditor or collection agency to settle outstanding debt. The most important goal is to establish a repayment agreement that prevents further legal action or credit score damage. The letter outlines specific terms, including the reduced balance, installment frequency, and deadlines. It is crucial to get all terms in writing before making payments. This document serves as legal evidence of your commitment to resolve the delinquency while providing a structured path toward financial recovery and debt clearance.

What is a Past Due Notice with a Payment Plan Offer?

A Past Due Notice with a Payment Plan Offer is a formal communication sent to a debtor notifying them of an overdue balance while simultaneously providing a structured proposal to repay the debt through smaller, manageable installments over time.

How do I request a payment plan after receiving a past due notice?

To request a payment plan, you should immediately contact the creditor using the information provided in the letter. Most notices include a proposed schedule; you can accept this offer by signing the agreement or propose an alternative monthly amount that fits your current financial situation.

What should be included in a formal payment plan offer letter?

A professionally structured letter should include the total outstanding balance, the specific account number, the proposed monthly payment amount, the start date of the first payment, the frequency of installments, and a statement regarding the suspension of further collection actions once the plan is active.

Can a payment plan prevent my account from going to collections?

Yes, successfully establishing and adhering to a payment plan typically stops the account from being referred to a third-party collection agency and helps protect your credit score from the negative impact of a default or "charge-off" status.

Are there additional fees or interest when using a payment plan for past due debt?

Depending on the original terms of service or the specific offer, creditors may continue to accrue interest on the remaining balance or charge a one-time administrative fee to set up the installment agreement. It is important to review the terms of the offer letter to confirm if the interest rate is frozen or if late fees will be waived.

Comments