Failing to address a missed payment can lead to severe financial consequences and credit score damage. A second reminder letter serves as a formal notification to resolve outstanding debt before escalating to collections. It is essential to maintain a professional yet firm tone to encourage immediate action. Below are some ready to use templates to help you communicate effectively with cardholders.

Image cover: Final Notice: Resolving Your Outstanding Credit Card Balance and Next Steps

Letter Samples List

- Initial Reminder Letter For Outstanding Credit Card Balances

- First Notice Letter For Delinquent Credit Card Accounts

- Second Reminder Letter For Overdue Credit Card Balances

- Third Warning Letter For Unpaid Credit Card Debt

- Final Demand Letter For Defaulted Credit Card Accounts

- Pre-Legal Action Letter For Outstanding Credit Card Balances

- Settlement Offer Letter For Delinquent Credit Card Debt

- Payment Plan Agreement Letter For Overdue Credit Card Balances

- Notice Of Default Letter For Unresolved Credit Card Debt

- Debt Validation Notice Letter For Credit Card Consumers

- Account Escalation Letter For Unpaid Credit Card Balances

- Intent To Sue Notification Letter For Defaulted Credit Card Accounts

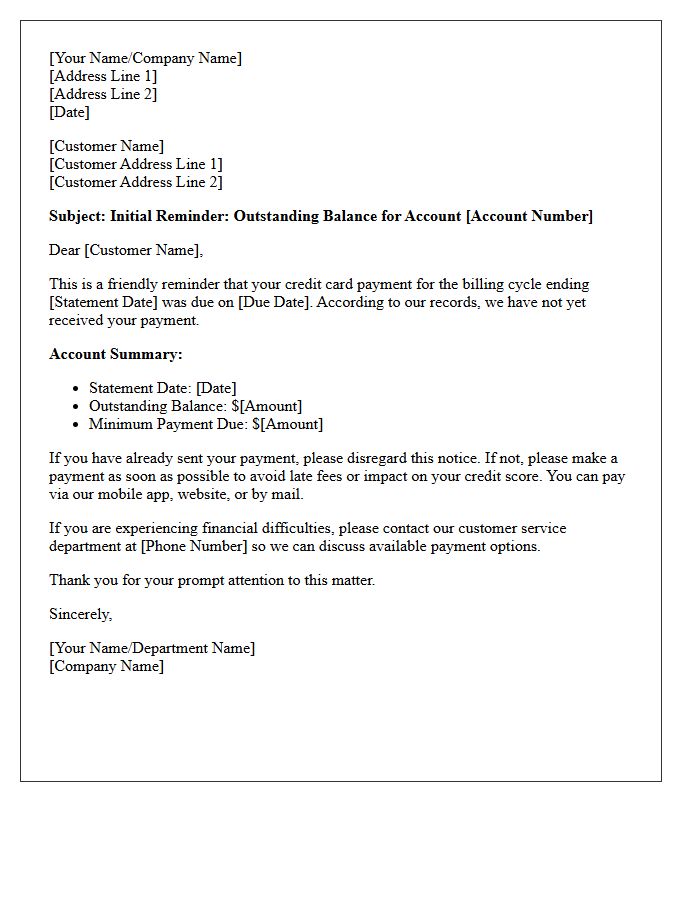

Initial Reminder Letter For Outstanding Credit Card Balances

An initial reminder letter serves as a formal notification that your credit card payment is overdue. Its primary purpose is to alert you to the outstanding balance before late fees or interest penalties escalate. Receiving this notice is a critical window to protect your credit score from negative reporting. You should immediately verify the statement details and contact your issuer to arrange a payment or discuss hardship options. Timely action prevents the account from moving into formal debt collection or triggering a default status on your financial record.

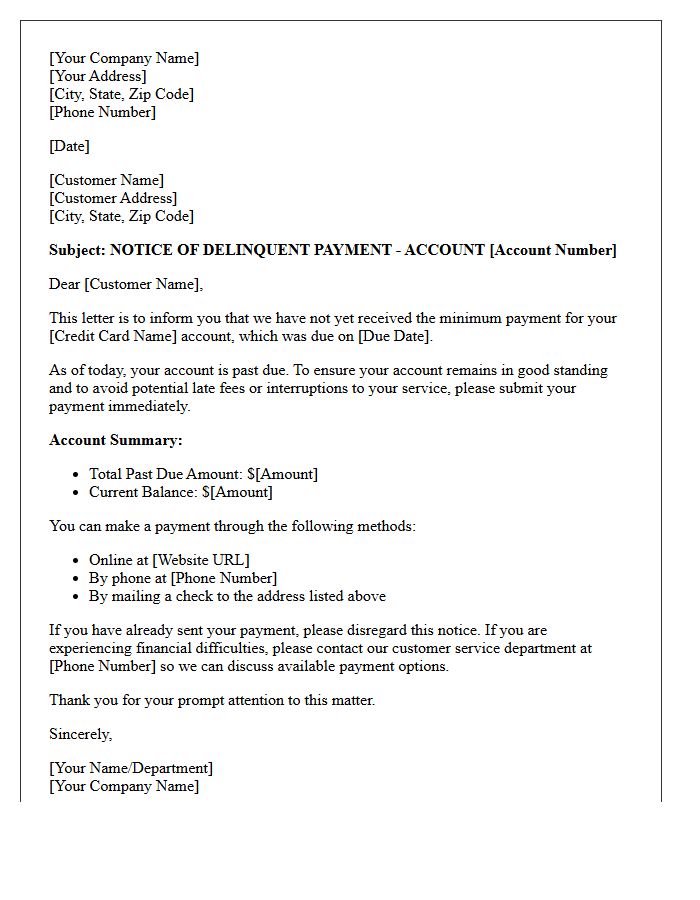

First Notice Letter For Delinquent Credit Card Accounts

A First Notice Letter serves as an official warning when a credit card payment is overdue. This document informs the cardholder of the delinquent status and specifies the outstanding balance, including any applicable late fees. It is the final opportunity to resolve the debt before the creditor reports the missed payment to credit bureaus, which can severely damage your credit score. Promptly addressing this notice helps avoid escalated collection actions, increased interest rates, or account suspension. Timely communication with the issuer is essential to maintain financial health and prevent long-term credit penalties.

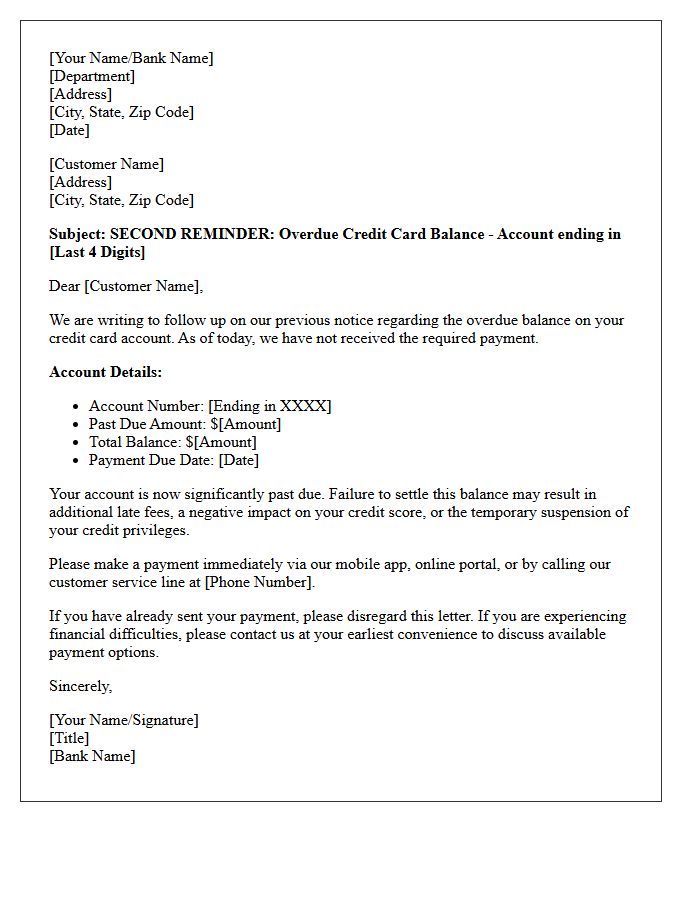

Second Reminder Letter For Overdue Credit Card Balances

A second reminder letter signifies a serious escalation regarding your overdue credit card balance. At this stage, the issuer may impose late fees, increase interest rates, and report the delinquency to credit bureaus, negatively impacting your credit score. It is crucial to contact the bank immediately to discuss repayment plans or hardship options. Ignoring this notice often leads to account suspension or debt collection. Acting now prevents further financial penalties and protects your long-term financial stability from aggressive legal recovery actions.

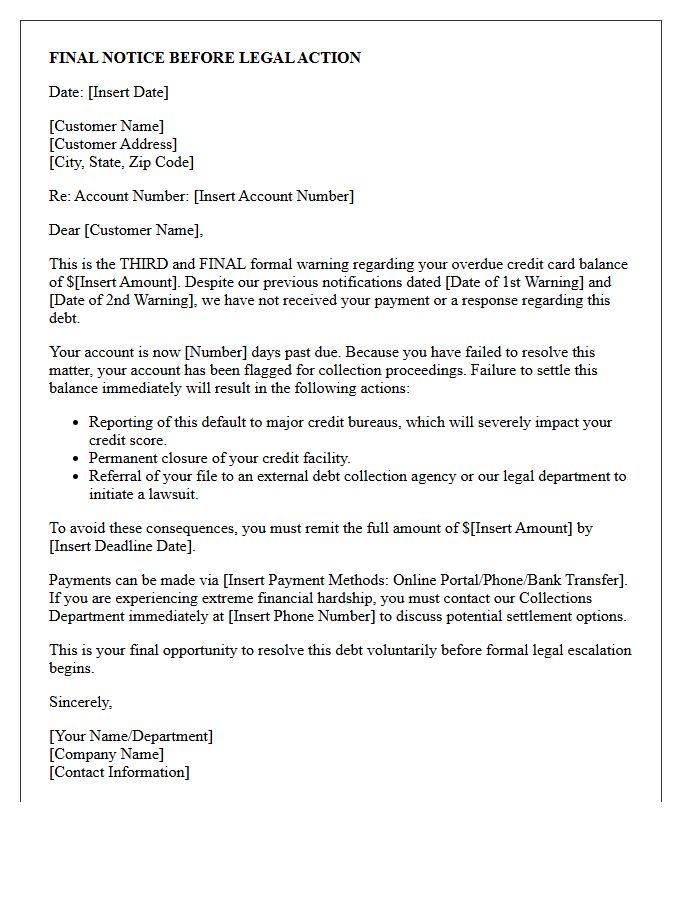

Third Warning Letter For Unpaid Credit Card Debt

Receiving a third warning letter for unpaid credit card debt indicates an urgent escalation in the collection process. This final notice serves as a pre-legal notification, signaling that your account is approaching a permanent charge-off status. At this stage, the creditor may transfer the balance to a third-party agency or initiate a lawsuit to secure a judgment. To avoid severe damage to your credit score or potential wage garnishment, you must prioritize communication. Contacting the issuer immediately to negotiate a settlement or repayment plan is essential to prevent further litigation.

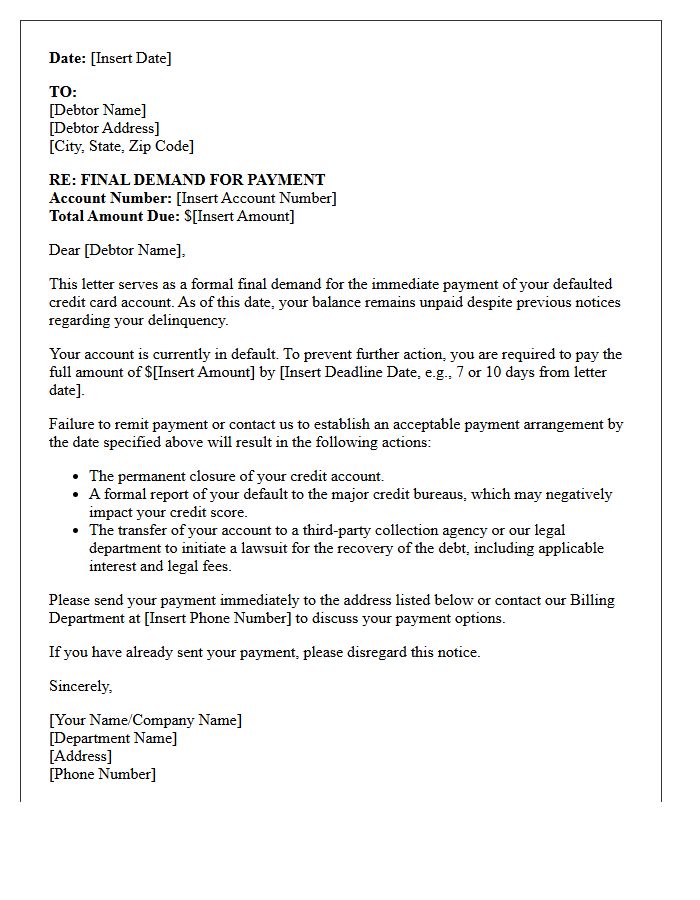

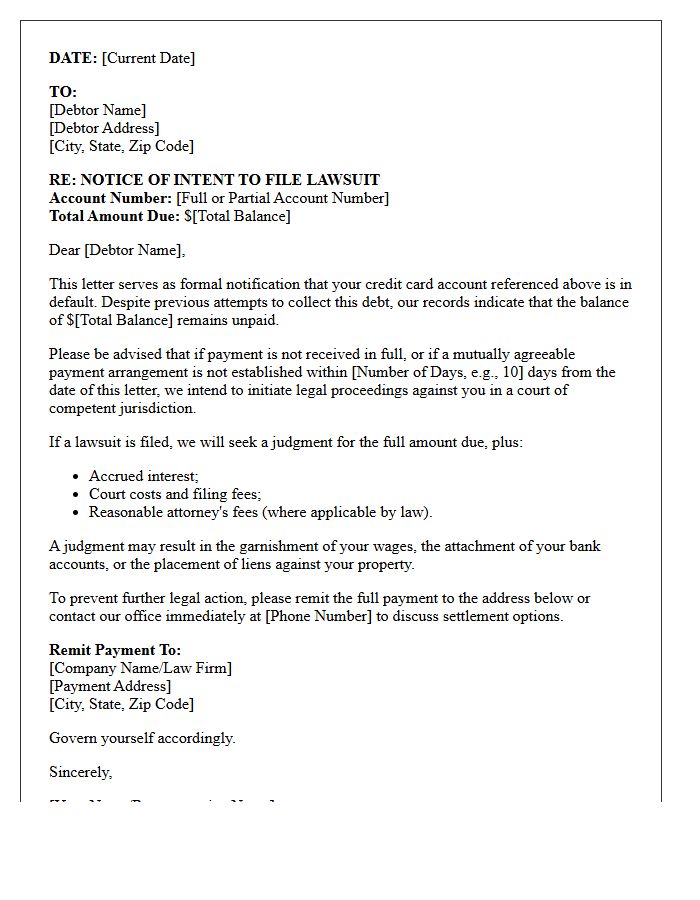

Final Demand Letter For Defaulted Credit Card Accounts

A Final Demand Letter is the last formal notification sent by creditors before initiating legal action or transferring debt to a collection agency. This document signifies that your credit card account is in default, demanding immediate payment of the total outstanding balance. Ignoring this notice can lead to lawsuits, wage garnishment, or severe long-term damage to your credit score. It is critical to respond promptly by negotiating a settlement or repayment plan to avoid further litigation and additional legal fees associated with debt recovery efforts.

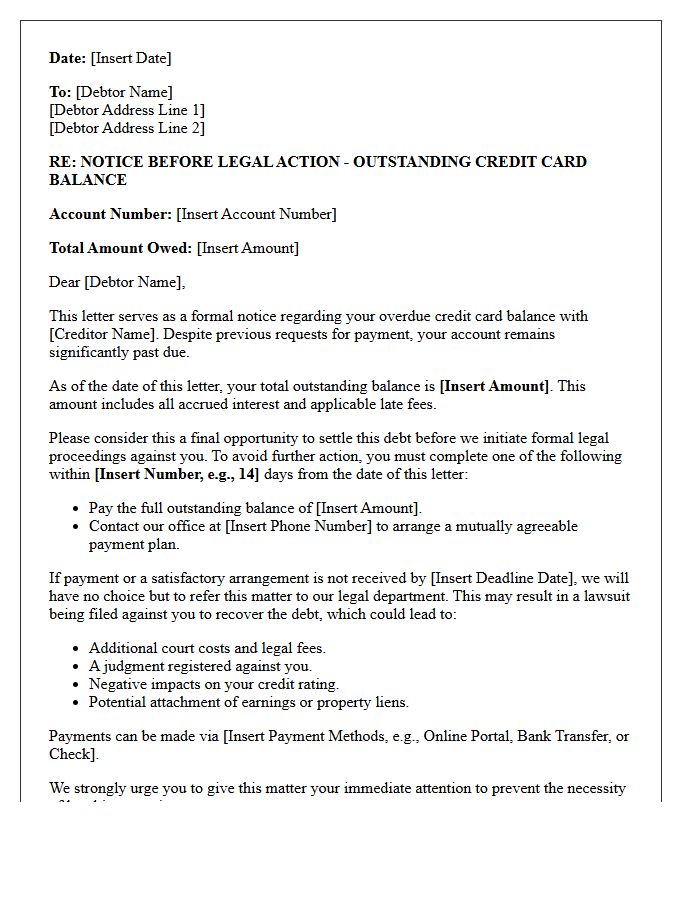

Pre-Legal Action Letter For Outstanding Credit Card Balances

A Pre-Legal Action Letter is a formal notice sent to cardholders with significant outstanding credit card balances before a lawsuit is filed. It serves as a final opportunity to resolve the debt through a repayment plan or settlement. Receiving this letter indicates that the creditor intends to pursue litigation to secure a court judgment, which could lead to wage garnishment or asset liens. Responding promptly is critical to avoid additional legal fees and further damage to your credit score. Always verify the debt's accuracy before making payments.

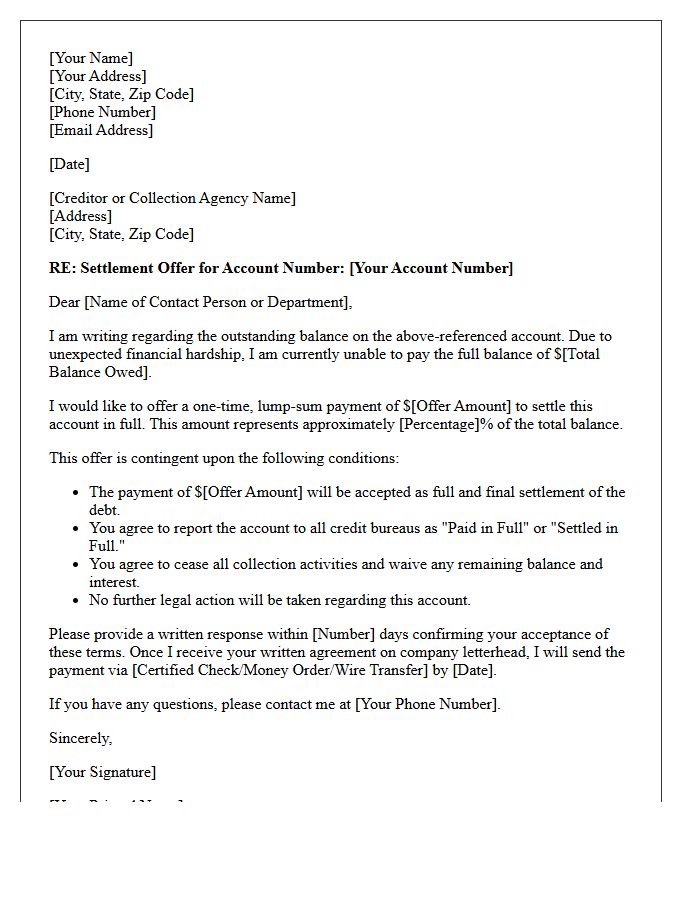

Settlement Offer Letter For Delinquent Credit Card Debt

A settlement offer letter is a formal proposal to resolve delinquent credit card debt for less than the full balance. It is a critical tool for debt negotiation that can stop collection calls and prevent legal action. When drafting, ensure you specify a lump-sum payment amount and request a "paid in full" status on your credit report. Always obtain a written agreement before sending funds to ensure the settlement is legally binding and protects your financial recovery. This process helps avoid bankruptcy while managing overwhelming financial obligations effectively.

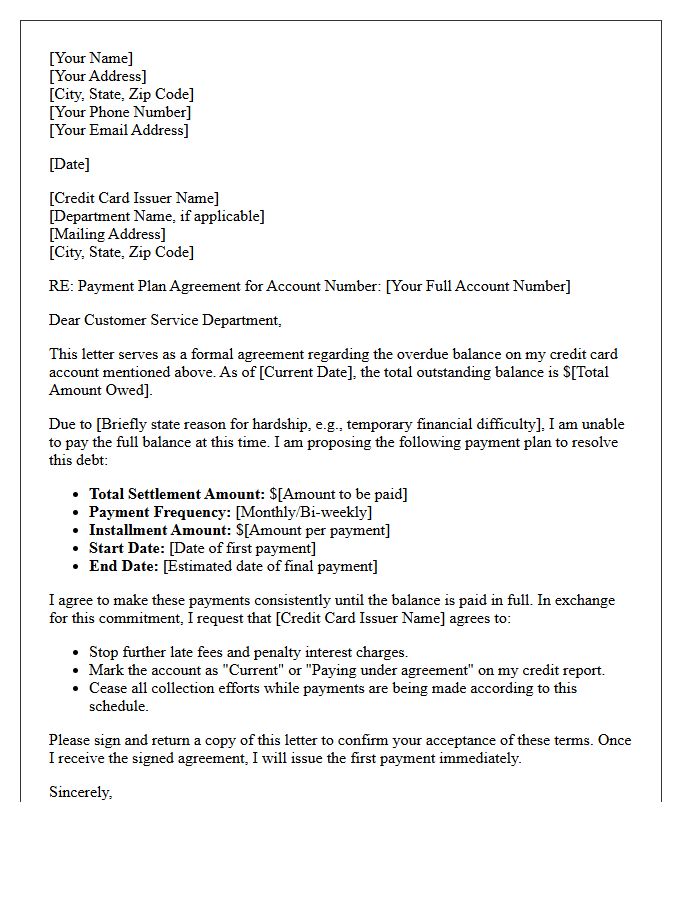

Payment Plan Agreement Letter For Overdue Credit Card Balances

A Payment Plan Agreement Letter is a formal contract between a debtor and a creditor to resolve overdue credit card balances. This document outlines a structured repayment schedule, including specific due dates, installment amounts, and potential interest rate reductions. By formalizing this debt settlement, you protect your legal rights and establish a clear path toward financial recovery. Ensuring the letter is signed by both parties helps prevent aggressive collection actions and provides essential written proof of the modified terms agreed upon to clear your outstanding debt effectively.

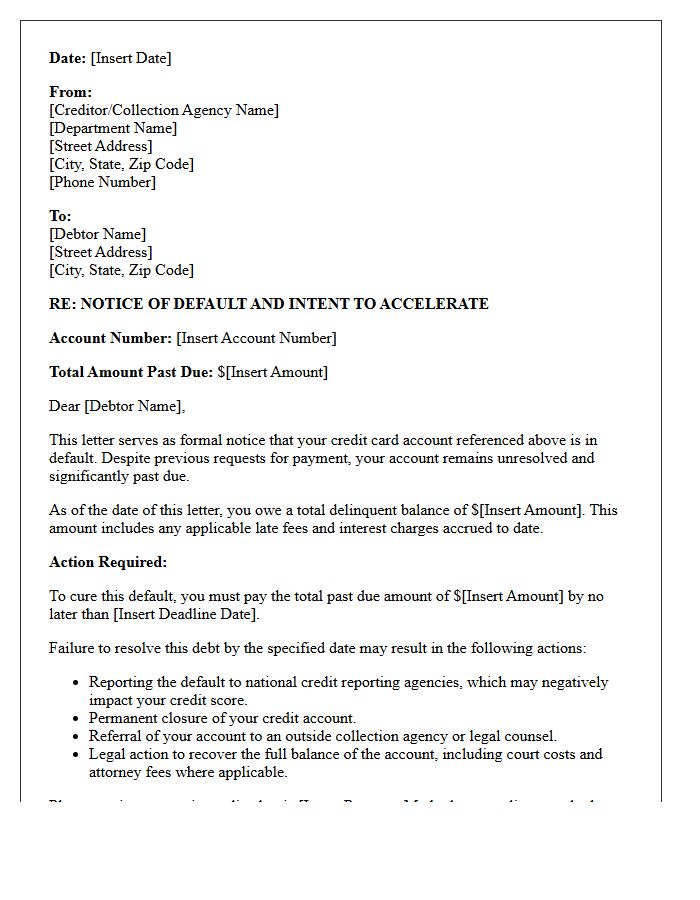

Notice Of Default Letter For Unresolved Credit Card Debt

Receiving a Notice of Default is a critical warning that your credit card account is being closed due to persistent non-payment. This formal letter signifies that you have breached your contract, and the creditor intends to initiate legal action or transfer the balance to a collection agency. To protect your financial future, you must respond immediately to avoid a judgment or severe credit score damage. Negotiating a repayment plan or settlement during this grace period is the most effective way to prevent further litigation and aggressive recovery efforts.

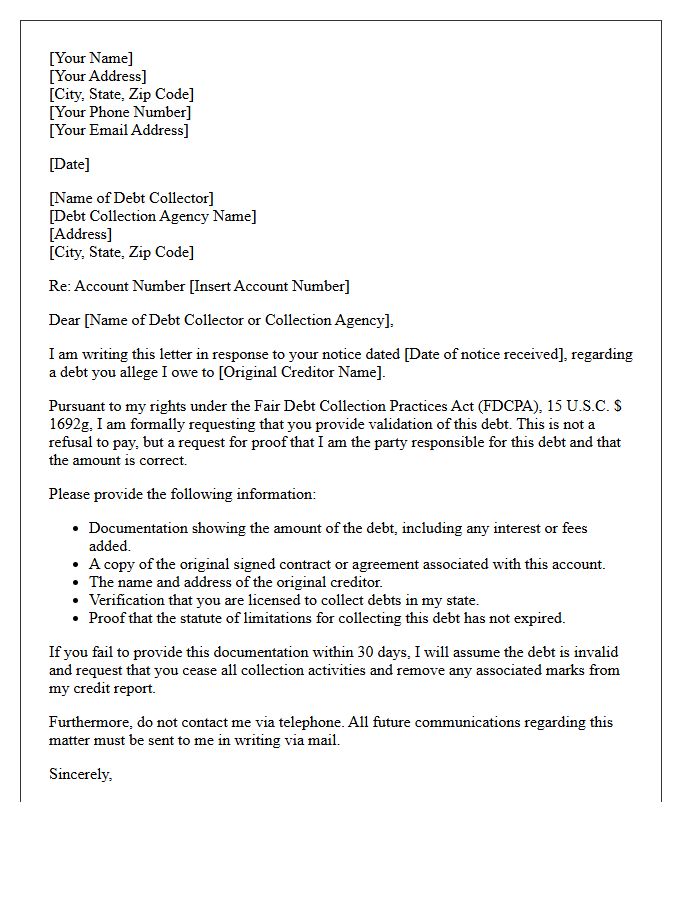

Debt Validation Notice Letter For Credit Card Consumers

A Debt Validation Notice is a critical legal document debt collectors must send within five days of initial contact. This letter provides essential details, including the amount owed and the original creditor's name. As a credit card consumer, you have a 30-day window to dispute the debt in writing. Once disputed, the collector must cease all communication until they provide official verification of the account. Reviewing this notice ensures you are not paying expired, incorrect, or fraudulent charges while protecting your legal rights under the Fair Debt Collection Practices Act.

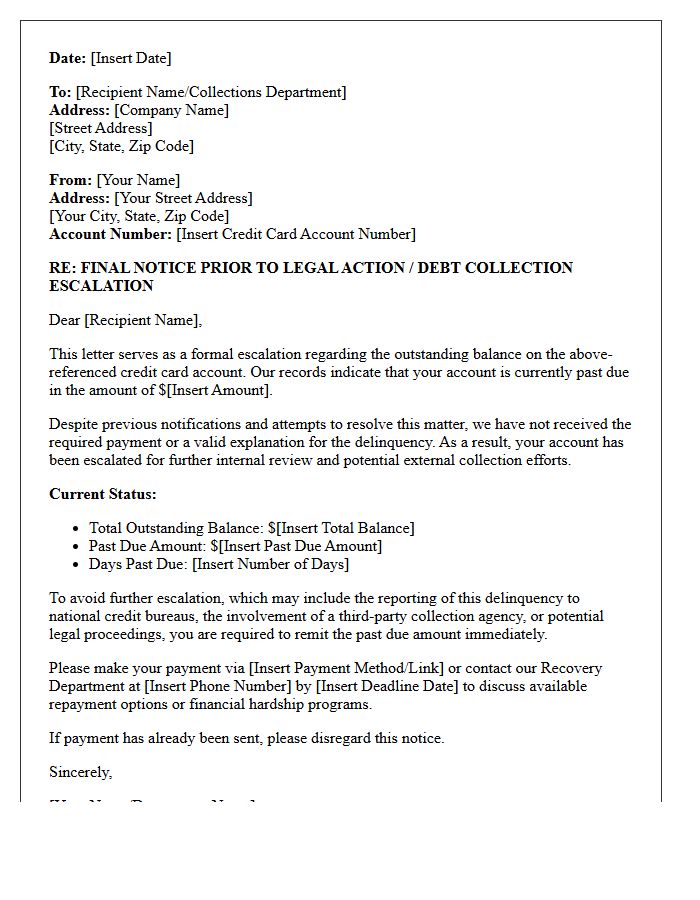

Account Escalation Letter For Unpaid Credit Card Balances

An Account Escalation Letter is a final formal notice issued when credit card balances remain unpaid after initial collection efforts. This document signifies that your debt is being moved to a legal department or a third-party agency for advanced recovery actions. Receiving this letter is critical because it warns of imminent consequences, including litigation, wage garnishment, or severe credit score damage. To avoid court proceedings, you must promptly contact the issuer to negotiate a settlement or repayment plan before the account reaches a point of no return.

Intent To Sue Notification Letter For Defaulted Credit Card Accounts

An Intent to Sue Notification is a final legal warning sent by creditors or collection agencies before initiating a lawsuit for defaulted credit card accounts. This letter signifies that internal collection efforts have failed and the account is moving toward litigation to obtain a court judgment. Receiving this notice is critical because it represents your last opportunity to negotiate a settlement or arrange a payment plan to avoid wage garnishment and asset seizure. You must verify the debt's accuracy and respond promptly to protect your legal rights and prevent a default judgment.

What is a second reminder letter for an overdue credit card balance?

A second reminder letter is a formal notice sent by a credit card issuer to a cardholder who has failed to respond to an initial late payment notification. It serves as a final courtesy warning before the account is escalated to a collections department or incurs more severe penalties.

When is a second payment reminder typically sent?

Most financial institutions send a second reminder letter when a credit card payment is 30 to 60 days past due. This letter follows the initial "friendly reminder" and indicates that the delinquency is becoming a serious matter that could affect the user's credit standing.

What are the consequences of ignoring a second credit card reminder?

Ignoring a second reminder can lead to a significant drop in your credit score, the assessment of late fees, an increase in your APR (Penalty APR), and the potential suspension of your credit privileges. Furthermore, the debt may be sold to a third-party collection agency if left unpaid.

Does a second reminder letter affect my credit score?

The letter itself does not lower your score, but the underlying delinquency does. Once a payment is 30 days overdue, the issuer typically reports the late payment to major credit bureaus, which can negatively impact your credit history for up to seven years.

How should I respond to a second notice for an overdue balance?

You should immediately pay the minimum amount due to stop further collection actions. If you cannot afford the payment, contact the credit card issuer's hardship department to discuss a repayment plan, a temporary deferment, or a settlement to prevent the account from going into default.

Comments