Negotiating a debt settlement requires a strategic approach to protect your financial rights. If an initial offer is too high, sending a Counter-Offer to Collection Agency Settlement Letter allows you to propose a realistic payment amount or structured plan. This process helps resolve outstanding debts for less than the full balance. To help you start, below are some ready to use templates.

Image cover: Smart Strategies and Templates for Negotiating Your Debt Collection Settlement

Letter Samples List

- Hardship Settlement Counter-Offer Letter

- Lump-Sum Payment Counter-Offer Letter

- Pay-For-Delete Counter-Offer Letter

- Installment Agreement Counter-Offer Letter

- Reduced Percentage Settlement Counter-Offer Letter

- Final Resolution Counter-Offer Letter

- Medical Debt Settlement Counter-Offer Letter

- Credit Card Debt Counter-Offer Letter

- Fixed Income Hardship Counter-Offer Letter

- Good Faith Payment Counter-Offer Letter

- Mutual Release Settlement Counter-Offer Letter

- Time-Barred Debt Settlement Counter-Offer Letter

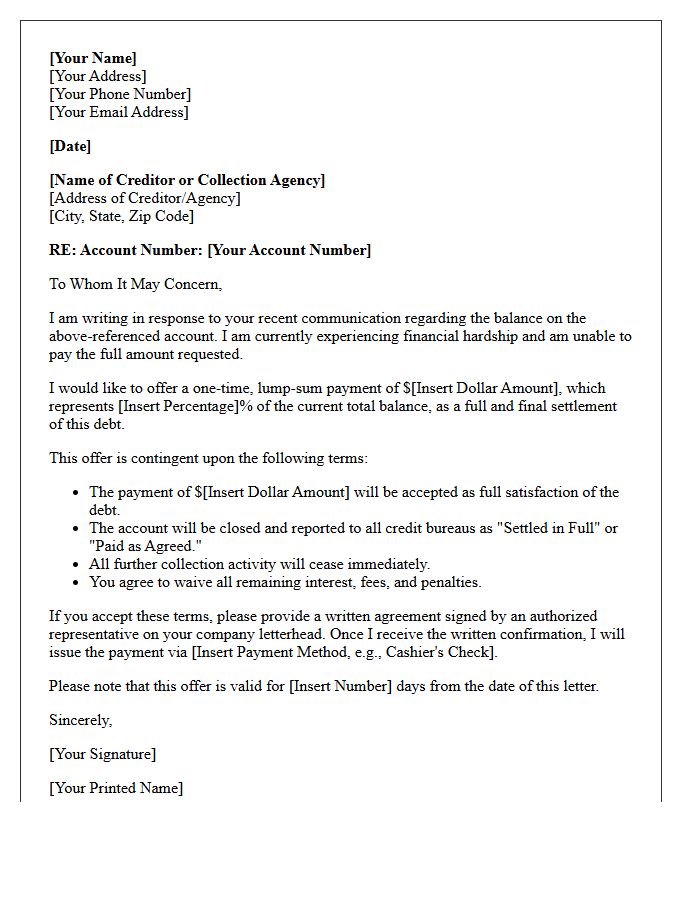

Hardship Settlement Counter-Offer Letter

A Hardship Settlement Counter-Offer Letter is a strategic formal response used to negotiate debt reductions. It allows a debtor to propose a lower, manageable payment amount while explaining their financial insolvency. The document should detail specific financial hardships, such as job loss or medical crises, to justify the request. Including a lump-sum payment offer often incentivizes creditors to accept a fraction of the total balance. If an agreement is reached, ensure the settlement terms are confirmed in writing to legally resolve the debt and prevent future collection actions.

Lump-Sum Payment Counter-Offer Letter

A Lump-Sum Payment Counter-Offer Letter is a formal document used to negotiate a higher settlement amount than initially proposed. It outlines a clear justification for the requested increase, such as outstanding medical expenses, lost wages, or future liabilities. To be effective, the letter must be professional, fact-based, and include supporting evidence. By presenting a well-reasoned valuation of the claim, you increase your chances of reaching a fair agreement and securing a maximum payout before signing a final release of claims or legal settlement.

Pay-For-Delete Counter-Offer Letter

A Pay-For-Delete Counter-Offer Letter is a strategic negotiation tool used to improve your credit score. When a collection agency requests payment, you respond by offering to pay the debt only if they completely remove the negative entry from your credit reports. This written agreement is essential because a "paid" collection still harms your rating; only a full deletion provides a recovery boost. Ensure you obtain a signed written acceptance from the creditor before sending any funds to guarantee they honor the terms and clear your financial record.

Installment Agreement Counter-Offer Letter

An Installment Agreement Counter-Offer Letter is a formal response sent to the IRS or tax authorities when their proposed payment terms are unaffordable. This document proposes an alternative monthly amount based on your actual financial capacity and documented living expenses. It is crucial to include a detailed financial statement to justify the lower payment. Submitting this counter-offer can prevent aggressive collection actions like wage garnishments while your proposal is under review. Clear communication ensures you secure a sustainable payment plan that fits your budget without risking default.

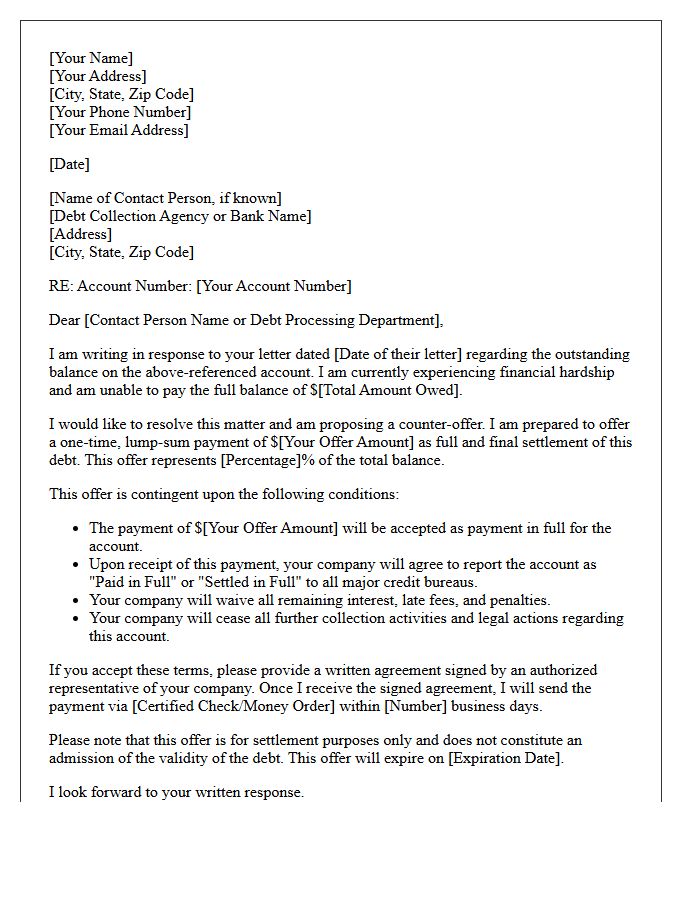

Reduced Percentage Settlement Counter-Offer Letter

A Reduced Percentage Settlement Counter-Offer Letter is a formal document used to negotiate debt by proposing a lump-sum payment lower than the original balance. This strategy aims to resolve outstanding liabilities for a fraction of the total cost. It is essential to clearly state the specific percentage offered and request a written agreement confirming the debt is settled in full. Sending this counter-offer can prevent further collection actions and provide a legally documented path toward financial recovery and improved credit standing through mutual compromise.

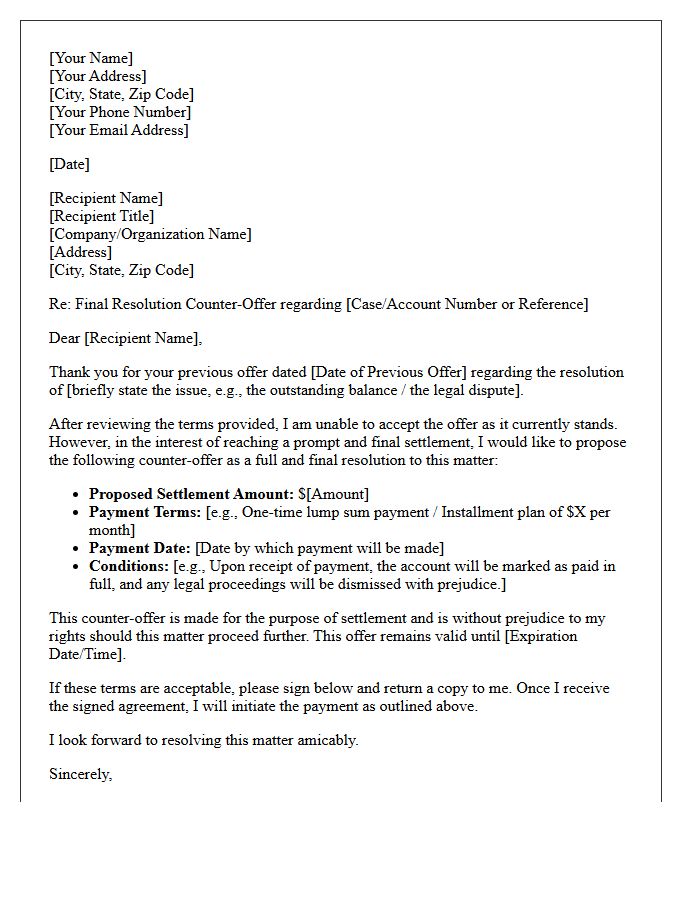

Final Resolution Counter-Offer Letter

A Final Resolution Counter-Offer Letter is a formal document used to reach a settlement in legal or insurance disputes. It represents the last stage of negotiation, presenting a definitive proposal to close the claim. This letter must clearly outline the specific terms, payment amounts, and a release of further liability. It serves as a binding ultimatum, signaling that if the offer is rejected, the parties may proceed to litigation. Precise language is essential to ensure the agreement is legally enforceable and provides a conclusive end to all outstanding grievances.

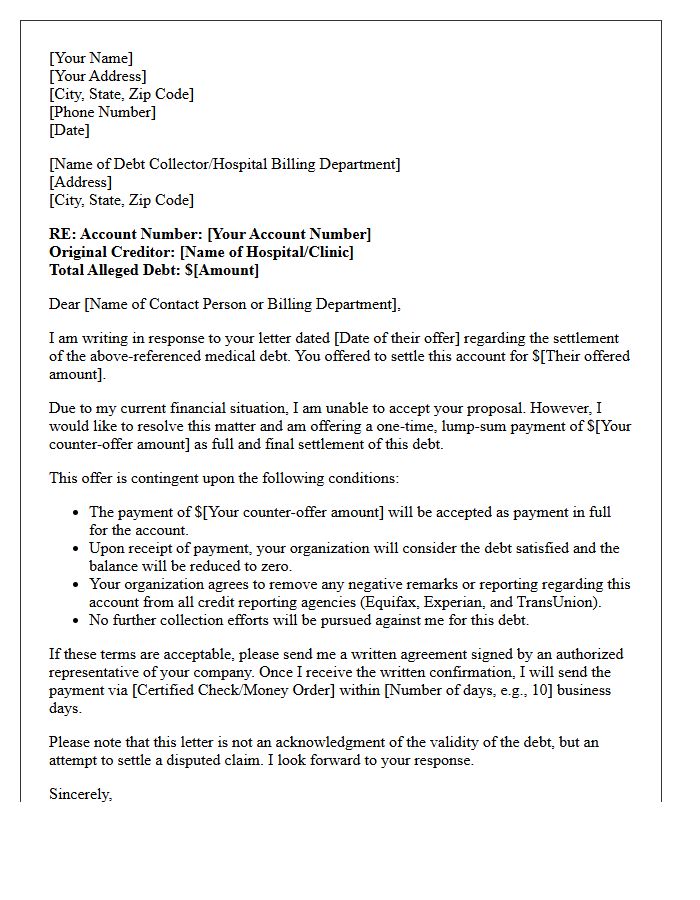

Medical Debt Settlement Counter-Offer Letter

A medical debt settlement counter-offer letter is a strategic tool used to negotiate a reduced payoff amount with healthcare providers or collection agencies. When responding to an initial demand, you should emphasize financial hardship and your inability to pay the full balance. Clearly state a specific, lump-sum amount you can afford, typically starting at 25-40% of the total bill. Crucially, demand a written agreement confirming the account will be marked as "paid in full" before sending funds to protect your credit score and legal rights.

Credit Card Debt Counter-Offer Letter

A Credit Card Debt Counter-Offer Letter is a strategic negotiation tool used to propose a settlement amount lower than your current balance. It formally outlines your financial hardship and suggests a lump-sum payment or revised installment plan to satisfy the debt. Sending this letter helps establish a paper trail and can prevent aggressive collection actions. Key elements include your account details, a specific settlement percentage, and a request for a "paid in full" status update on your credit report upon completion of the agreed payment.

Fixed Income Hardship Counter-Offer Letter

A Fixed Income Hardship Counter-Offer Letter is a strategic formal response sent to creditors or lenders when their initial repayment proposal is unaffordable. This document negotiates lower monthly payments based on a verifiable limited budget, such as Social Security or pensions. It is crucial to provide a detailed financial statement to prove your inability to meet standard terms. Sending this letter can prevent default and secure more sustainable debt management terms tailored to your specific economic constraints, protecting your essential living expenses from aggressive collection efforts.

Good Faith Payment Counter-Offer Letter

A Good Faith Payment Counter-Offer Letter is a strategic debt settlement tool used to negotiate lower repayment terms. It demonstrates your willingness to pay a portion of the debt while formally stating financial hardship. By proposing a specific lump-sum payment or revised installment plan, you initiate a legal paper trail. This document is essential for protecting your rights, potentially preventing litigation, and securing a written agreement that the creditor will consider the account "settled in full" upon receipt of the negotiated funds.

Mutual Release Settlement Counter-Offer Letter

A Mutual Release Settlement Counter-Offer Letter is a formal legal response used to renegotiate terms after an initial settlement proposal. Its primary purpose is to reach a binding agreement that permanently resolves a dispute. Crucially, the document must outline specific liability waivers, ensuring both parties forfeit the right to pursue future claims regarding the matter. By clearly defining revised financial figures or performance obligations, this counter-offer serves as a critical tool for risk mitigation and finality, protecting all signatories from further litigation once the compromise is accepted and signed.

Time-Barred Debt Settlement Counter-Offer Letter

A Time-Barred Debt Settlement Counter-Offer Letter is a legal response to collectors pursuing expired debts beyond the statute of limitations. Sending this document protects your rights by acknowledging the debt is legally uncollectible while offering a voluntary settlement to clear your credit report. It is crucial to explicitly state that the payment is not an admission of liability, as any partial payment or formal acknowledgment could restart the clock on the collection period. Use this letter to maintain leverage and prevent aggressive litigation on ancient financial obligations.

How do I respond to a debt collection settlement offer?

You should respond by sending a formal counter-offer letter via certified mail. Acknowledge the debt without admitting full liability, state your financial hardship, and propose a specific lump-sum amount (typically 25% to 50% of the balance) or a structured payment plan that fits your budget.

What should be included in a counter-offer letter to a collection agency?

Your counter-offer letter should include your account number, the date, a clear statement that you are disputing the total amount owed, your proposed settlement figure, and a request for a "pay for delete" agreement to remove the negative mark from your credit report.

Is it better to settle for a lump sum or monthly payments?

Collection agencies usually prefer a one-time lump-sum payment and are often willing to accept a lower total percentage (e.g., 30-40% of the debt) compared to monthly payment plans, which may require you to pay a higher percentage of the total balance over time.

Will a debt settlement hurt my credit score?

Settling a debt for less than the full amount may result in a "Settled for less than full balance" notation on your credit report, which can impact your score. To minimize damage, negotiate a "pay for delete" agreement where the agency agrees to remove the collection entry entirely upon payment.

Should I get a settlement agreement in writing before paying?

Yes, never send money to a collection agency until you have a signed settlement agreement in writing. This document must explicitly state the agreed-upon amount, that it constitutes "full satisfaction" of the debt, and that the agency will cease all further collection activities on this account.

Comments