A Credit Card Charge-Off Settlement Offer Letter is a formal proposal sent to lenders to resolve defaulted debt for less than the total balance. Negotiating a settlement can stop collection efforts and help repair your financial standing after an account is charged off. To help you negotiate effectively with creditors, below are some ready to use templates.

Image cover: Settling Your Debt: Professional Credit Card Charge-Off Offer Letter Templates

Letter Samples List

- Initial Credit Card Charge-Off Settlement Offer Letter

- Final Notice Credit Card Charge-Off Settlement Offer Letter

- Lump-Sum Payment Credit Card Charge-Off Settlement Offer Letter

- Installment Agreement Credit Card Charge-Off Settlement Offer Letter

- Financial Hardship Credit Card Charge-Off Settlement Offer Letter

- Time-Sensitive Credit Card Charge-Off Settlement Offer Letter

- Pre-Litigation Credit Card Charge-Off Settlement Offer Letter

- Reduced Balance Credit Card Charge-Off Settlement Offer Letter

- Counter-Offer Credit Card Charge-Off Settlement Agreement Letter

- Pay-For-Delete Credit Card Charge-Off Settlement Offer Letter

- Past Due Credit Card Charge-Off Settlement Offer Letter

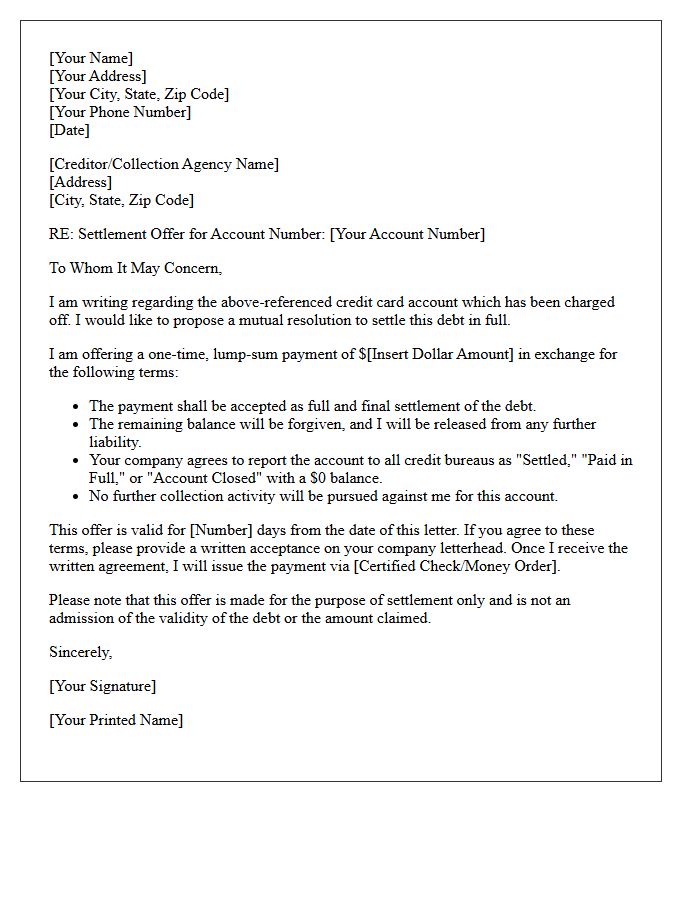

- Mutual Resolution Credit Card Charge-Off Settlement Offer Letter

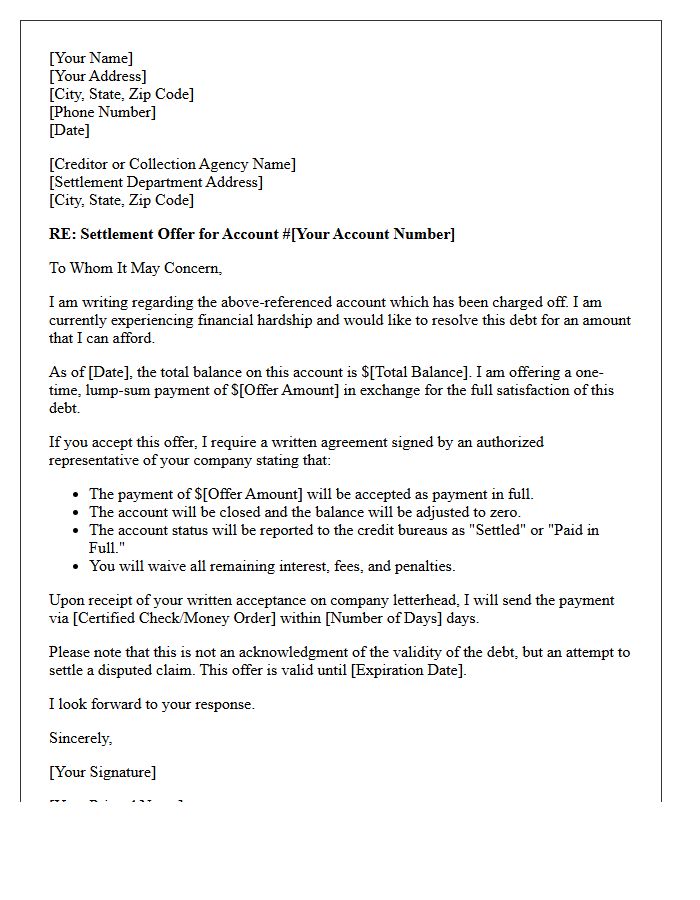

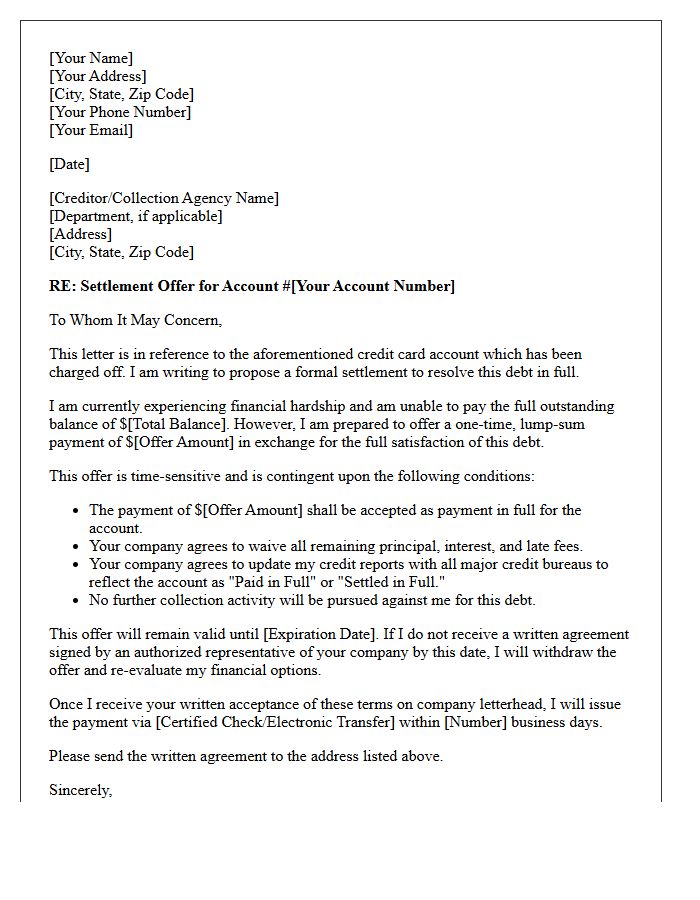

Initial Credit Card Charge-Off Settlement Offer Letter

An initial credit card charge-off settlement offer letter is a formal proposal to resolve delinquent debt for less than the total balance owed. Once an account is charged off, creditors often prefer a lump-sum payment to recover costs rather than pursuing lengthy legal action. Receiving this letter indicates an opportunity to negotiate terms and stop aggressive collection efforts. Ensure any agreement is documented in writing before paying, as a settled account significantly impacts your credit score while legally releasing you from further liability for that specific debt.

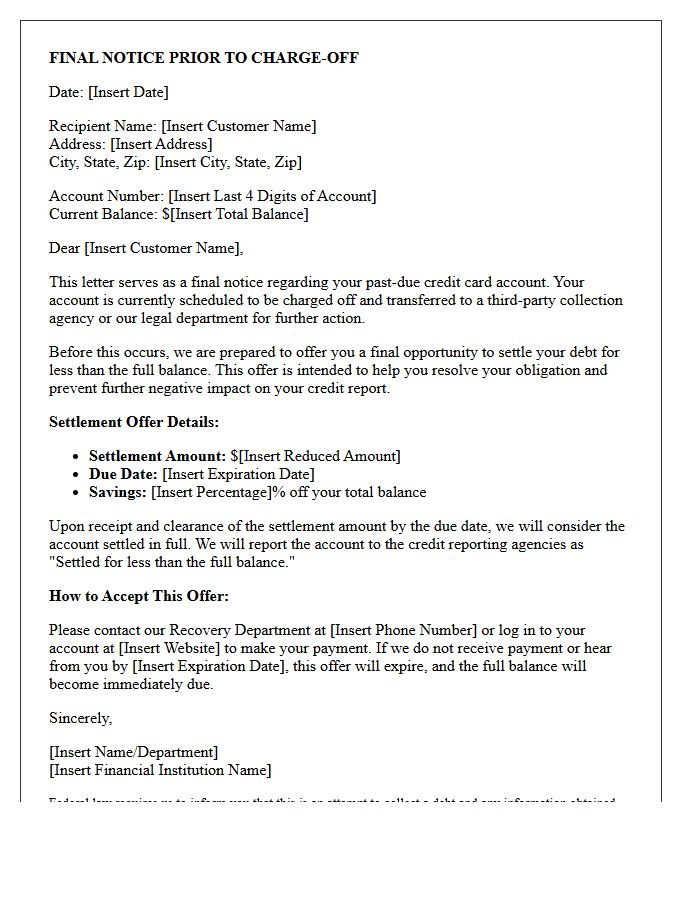

Final Notice Credit Card Charge-Off Settlement Offer Letter

Receiving a Final Notice Credit Card Charge-Off Settlement Offer Letter is a critical opportunity to resolve delinquent debt before it is sold to a third-party collection agency or leads to litigation. This document represents the lender's last attempt to accept a reduced lump-sum payment to satisfy the account. Settling can prevent further credit score damage and stop aggressive collection efforts. Always ensure the agreement is confirmed in writing and verify how the status will be reported to credit bureaus to protect your financial recovery and long-term stability.

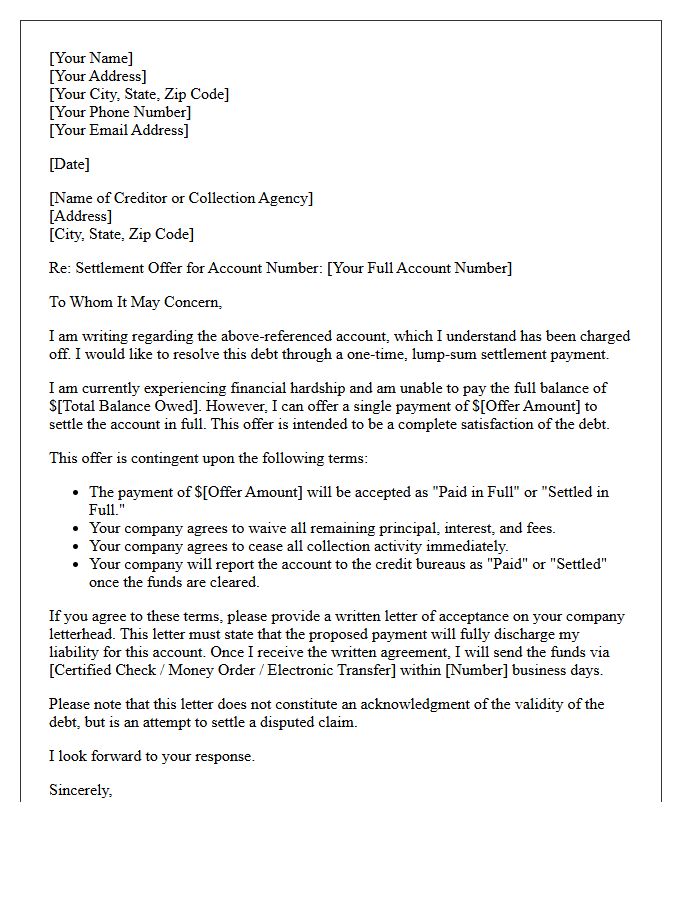

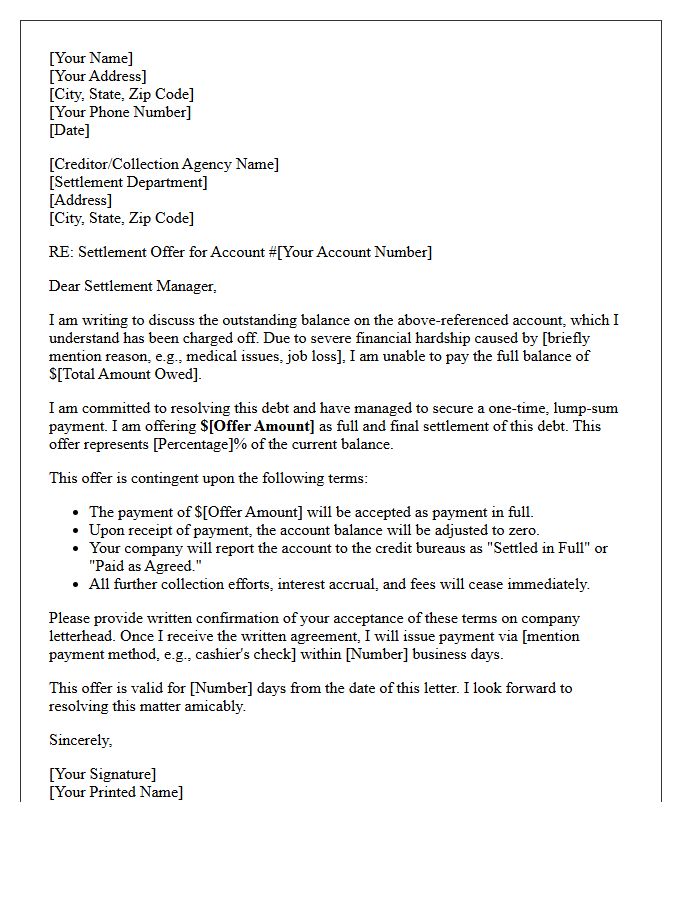

Lump-Sum Payment Credit Card Charge-Off Settlement Offer Letter

A credit card charge-off settlement offer letter is a formal proposal to resolve delinquent debt for less than the full balance. Accepting a lump-sum payment can save significant money and stop aggressive collection efforts. However, it is crucial to ensure the agreement is documented in writing before sending funds. Confirm that the creditor will report the account as "settled in full" to credit bureaus. While this avoids further legal action, be aware that forgiven debt over $600 may trigger taxable income liabilities reported via a 1099-C form.

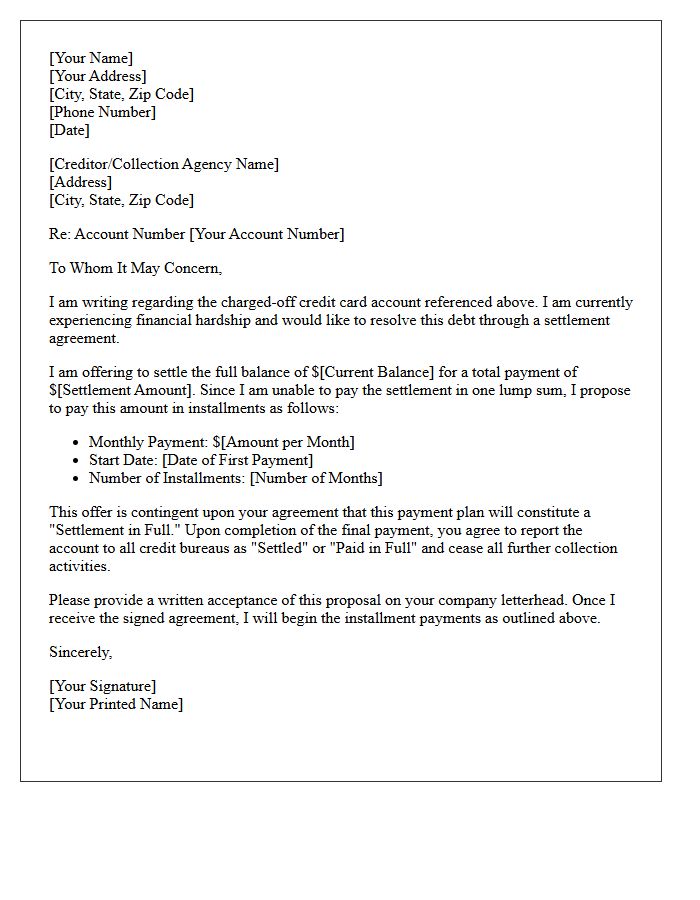

Installment Agreement Credit Card Charge-Off Settlement Offer Letter

An Installment Agreement Credit Card Charge-Off Settlement Offer Letter is a formal proposal to resolve delinquent debt for less than the total balance owed. By requesting structured monthly payments, this document helps consumers settle charged-off accounts without a single lump-sum payment. It is crucial to ensure the letter specifies that once the final installment is paid, the account status will be updated to "settled in full." Always obtain a signed confirmation from the creditor before sending payments to legally protect your financial interests and improve your credit history over time.

Financial Hardship Credit Card Charge-Off Settlement Offer Letter

A financial hardship charge-off settlement offer letter is a formal proposal to resolve delinquent debt for less than the full balance. Once a creditor deems an account uncollectible, they may accept a lump-sum payment to close the file. It is crucial to obtain this agreement in writing before sending funds. Ensure the letter explicitly states that the debt will be marked as "settled in full" or "paid" to prevent future collections. This process can significantly impact your credit score, so professional negotiation is often recommended to protect your long-term financial standing.

Time-Sensitive Credit Card Charge-Off Settlement Offer Letter

Receiving a Time-Sensitive Credit Card Charge-Off Settlement Offer is a critical opportunity to resolve defaulted debt for less than the full balance. Acting before the deadline prevents the account from being sold to aggressive third-party debt collectors or resulting in legal action. While a settlement can improve your debt-to-income ratio, it will likely be reported as "settled for less than full balance," impacting your credit score. Always ensure you receive the agreement in writing and understand the potential tax implications of forgiven debt before making a final payment.

Pre-Litigation Credit Card Charge-Off Settlement Offer Letter

A pre-litigation credit card charge-off settlement offer letter is a formal proposal sent by a creditor or collection agency to resolve outstanding debt before legal action commences. This document typically offers a reduced lump-sum payment or a structured settlement plan to close the account permanently. Receiving this letter is a critical opportunity to negotiate and prevent a lawsuit. It is essential to verify the debt's validity and ensure any agreed-upon terms are documented in writing to protect your credit report and stop further collection efforts.

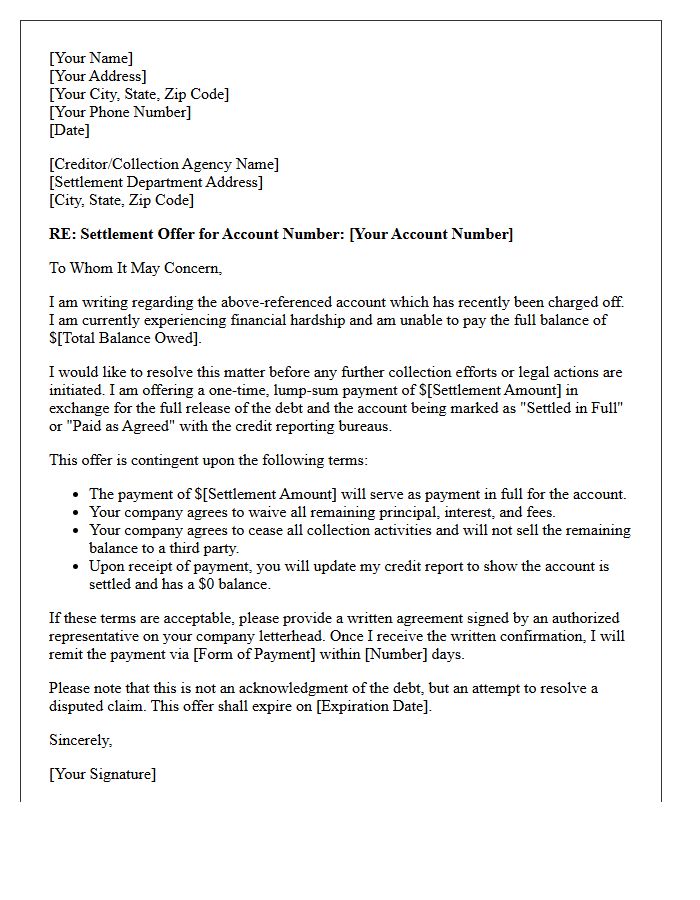

Reduced Balance Credit Card Charge-Off Settlement Offer Letter

A reduced balance settlement offer is a formal proposal from a creditor or collection agency to resolve your debt for less than the total amount owed. Receiving this letter means the account has likely been marked as a charge-off, signifying it as a loss on their records. Before paying, ensure you obtain a written agreement confirming the payment in full status. While settling improves your debt-to-income ratio, it may leave a negative mark on your credit report. Always verify the debt's validity and statute of limitations before responding to the offer.

Counter-Offer Credit Card Charge-Off Settlement Agreement Letter

A Counter-Offer Credit Card Charge-Off Settlement Agreement Letter is a formal proposal sent to creditors to resolve delinquent debt for less than the full balance. It is a critical tool for debt negotiation after an account has been charged off. This document should clearly state your proposed lump-sum payment or structured plan, request a "paid in full" status on your credit report, and demand written acceptance before payment. Sending this letter helps protect your legal rights and ensures the settlement terms are documented to prevent future collection efforts on the remaining balance.

Pay-For-Delete Credit Card Charge-Off Settlement Offer Letter

A Pay-For-Delete settlement letter is a strategic negotiation tool used to remove negative marks from your credit profile. When dealing with a charge-off, this formal request proposes full or partial payment in exchange for the creditor completely deleting the account entry from credit bureaus. Rather than simply marking it as "paid," a successful agreement restores your credit score by eliminating the derogatory history. Always ensure the creditor provides written 1acceptance of these terms before sending funds to guarantee legal accountability and effective credit restoration.

Past Due Credit Card Charge-Off Settlement Offer Letter

A past due credit card charge-off settlement offer letter is a formal proposal to resolve delinquent debt for less than the total balance. When an account is charged off, the creditor deems it uncollectible, often selling it to a collection agency. Receiving this letter provides an opportunity to negotiate a lump-sum payment or structured plan. Ensure the agreement is documented in writing before paying to guarantee the account is marked as settled. This action can prevent further legal escalation, though it will impact your credit report for seven years.

Mutual Resolution Credit Card Charge-Off Settlement Offer Letter

A mutual resolution credit card charge-off settlement offer letter is a formal proposal to resolve delinquent debt for less than the full balance. Once an account is charged off, the creditor deems it uncollectible, though the obligation remains. Receiving this letter allows you to negotiate a lump-sum payment or structured plan to satisfy the debt. It is crucial to obtain the agreement in writing before paying to ensure the account is reported as settled to credit bureaus, preventing further collection efforts and helping to stabilize your financial profile.

What is a credit card charge-off settlement offer letter?

A credit card charge-off settlement offer letter is a formal written proposal sent by either a creditor or a debtor to resolve an outstanding delinquent debt for less than the full balance owed. This document outlines the specific settlement amount, payment terms, and the agreement to mark the account as settled with the credit bureaus.

Should I accept a settlement offer after my credit card is charged off?

Accepting a settlement offer can be beneficial if you cannot afford the full balance, as it stops further collection efforts and prevents legal action. However, while it resolves the debt, it may still negatively impact your credit score, though typically less so than an active, unpaid charge-off or a judgment.

What key details should be included in a charge-off settlement agreement?

A valid settlement agreement should clearly state the total debt amount, the agreed-upon reduced payment, the deadline for payment, and a written guarantee that the creditor will report the account as "settled in full" or "paid as agreed" to major credit reporting agencies.

Can I negotiate the terms of a settlement offer letter?

Yes, you can negotiate the terms of a settlement offer. Most creditors are willing to accept between 30% and 50% of the total balance in a lump sum. You should always provide a counter-offer in writing and ensure the final agreed-upon terms are documented in a revised letter before making any payments.

How does a settled charge-off affect my credit report?

A settled charge-off will remain on your credit report for seven years from the date of the original delinquency. While the "settled" status is better than an "unpaid" status for future lenders, your credit score may not see an immediate increase until you begin rebuilding your credit history with new, positive trade lines.

Comments