A Co-Signer Debt Validation Notice Letter is a formal legal request sent to creditors to verify the legitimacy and accuracy of a claimed debt. It protects co-signers by demanding proof of their liability and the total amount owed under consumer protection laws. Use this tool to challenge errors and safeguard your credit score. Below are some ready to use templates.

Image cover: Mastering the Co-Signer Debt Validation Process: Expert Templates and Essential Letter Samples

Letter Samples List

- Initial Co-Signer Debt Validation Notice Letter

- Second Request Co-Signer Debt Validation Notice Letter

- Final Notice Co-Signer Debt Validation Letter

- Automobile Loan Co-Signer Debt Validation Notice Letter

- Student Loan Co-Signer Debt Validation Notice Letter

- Personal Loan Co-Signer Debt Validation Notice Letter

- Pre-Legal Action Co-Signer Debt Validation Notice Letter

- Account Verification Co-Signer Debt Validation Letter

- Third-Party Collection Co-Signer Debt Validation Notice Letter

- Post-Default Co-Signer Debt Validation Notice Letter

- Disputed Account Co-Signer Debt Validation Notice Letter

- Delinquent Account Co-Signer Debt Validation Notice Letter

- Original Creditor Co-Signer Debt Validation Notice Letter

- Settlement Negotiation Co-Signer Debt Validation Notice Letter

- Credit Bureau Reporting Co-Signer Debt Validation Notice Letter

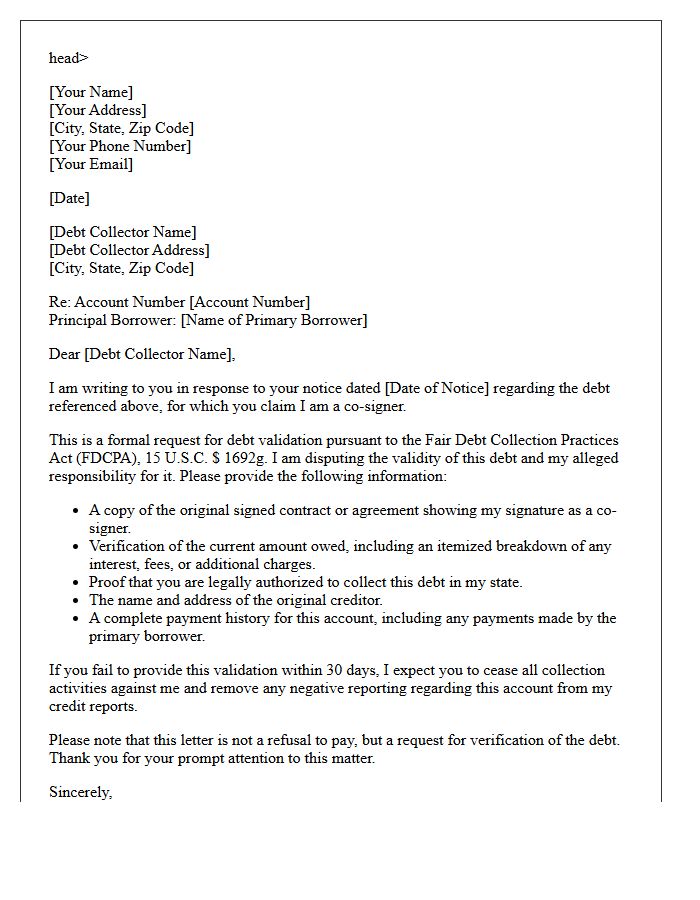

Initial Co-Signer Debt Validation Notice Letter

An Initial Co-Signer Debt Validation Notice Letter is a formal request sent to a creditor or collection agency to verify the legitimacy of a debt. This legal document ensures that the co-signer is not held liable for inaccurate or expired claims. Under the Fair Debt Collection Practices Act (FDCPA), you have the right to demand proof of the original agreement and the exact balance owed. Sending this notice within thirty days of initial contact is crucial for protecting your credit score and exercising your consumer rights before making any payments.

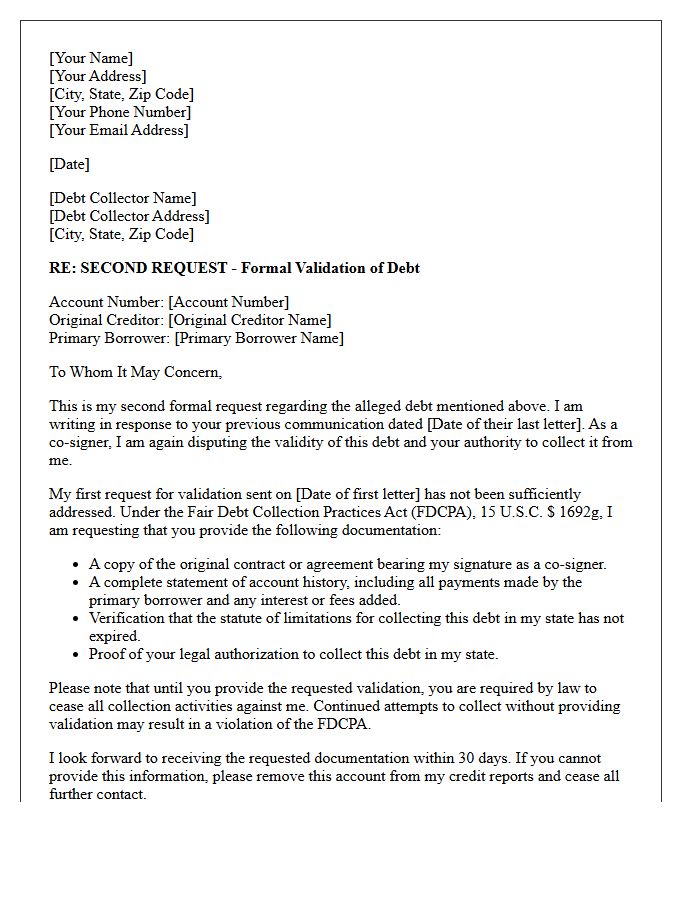

Second Request Co-Signer Debt Validation Notice Letter

A Second Request Co-Signer Debt Validation Notice Letter is a critical follow-up sent when a creditor fails to respond to an initial Debt Validation inquiry. This legal document demands verification of the debt's validity and the co-signer's specific liability. Under the Fair Debt Collection Practices Act (FDCPA), persistent requests protect your credit score from inaccurate reporting. It is essential for documenting a paper trail, ensuring the collector provides evidence of the original agreement before you assume financial responsibility for any outstanding balance or alleged delinquency.

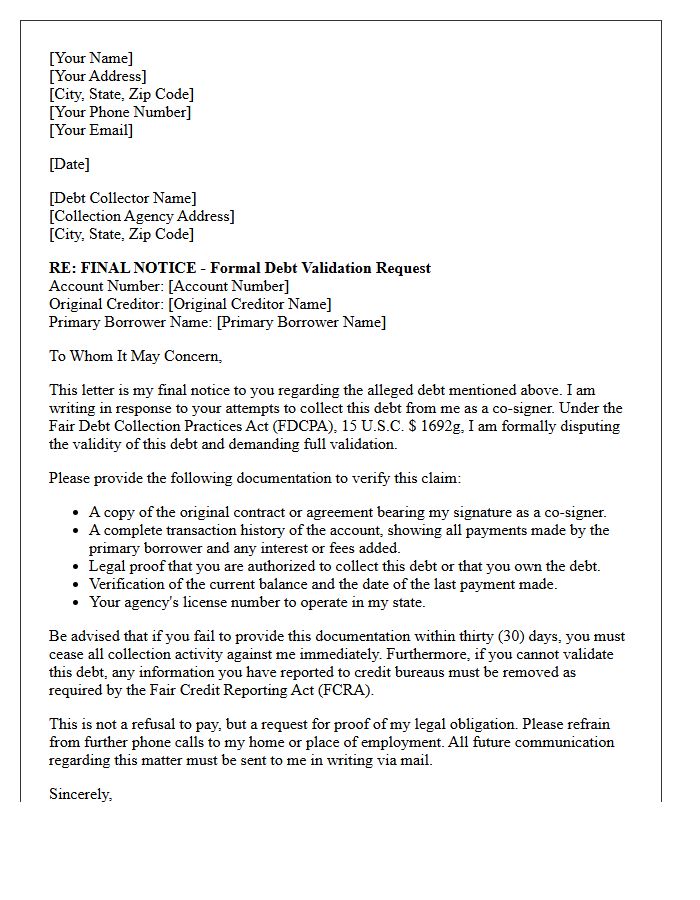

Final Notice Co-Signer Debt Validation Letter

A Final Notice Co-Signer Debt Validation Letter is a critical legal document sent to demand proof of an alleged debt before final collection actions. As a co-signer, you have the right to request verification of the original agreement, payment history, and the collector's authority to pursue you. Sending this formal dispute within the statutory timeframe stops harassment and protects your credit score. Ensuring the debt is validated prevents you from being held liable for incorrect amounts or expired obligations under the Fair Debt Collection Practices Act.

Automobile Loan Co-Signer Debt Validation Notice Letter

An Automobile Loan Co-Signer Debt Validation Notice Letter is a critical legal tool used to verify the accuracy of a claimed deficiency balance. Under the Fair Debt Collection Practices Act (FDCPA), co-signers have the right to request written proof of the debt's validity, including the original contract and payment history. Sending this formal notice disputes potential errors and prevents unauthorized collection activities. It ensures that the creditor proves the co-signer's legal obligation before any negative reporting or legal action occurs, protecting your credit score and financial rights during the recovery process.

Student Loan Co-Signer Debt Validation Notice Letter

A Student Loan Co-Signer Debt Validation Notice Letter is a formal legal request sent to creditors to verify the accuracy and legitimacy of a debt. It ensures that the co-signer is not being held liable for incorrect amounts or expired claims. Under the Fair Debt Collection Practices Act, you have thirty days to dispute the debt once notified. Sending this letter forces the agency to provide proof of the debt's validity, including the original contract and payment history, protecting your credit score and financial rights from predatory collection practices.

Personal Loan Co-Signer Debt Validation Notice Letter

A Personal Loan Co-Signer Debt Validation Notice Letter is a formal legal request used to verify the legitimacy of a debt. When a lender demands payment from a co-signer, this document requires them to provide verifiable evidence of the original contract and the exact balance owed. Under the Fair Debt Collection Practices Act, consumers have thirty days to dispute the claim. Sending this letter ensures that the co-signer is not held liable for inaccurate, expired, or fraudulent collections, protecting their credit score and financial rights from predatory practices.

Pre-Legal Action Co-Signer Debt Validation Notice Letter

A Pre-Legal Action Co-Signer Debt Validation Notice Letter is a critical formal warning sent before a creditor initiates litigation. This document notifies the co-signer of their legal liability for an outstanding balance and provides a final opportunity to dispute the debt's accuracy. Under the Fair Debt Collection Practices Act (FDCPA), recipients have thirty days to request verification. Ignoring this notice can lead to lawsuits, wage garnishment, or severe credit score damage. It serves as an essential procedural step to ensure transparency and protect consumer rights before entering the court system.

Account Verification Co-Signer Debt Validation Letter

An Account Verification Co-Signer Debt Validation Letter is a formal legal request used to dispute or confirm the legitimacy of a debt. It requires a creditor to provide documented proof that the co-signer is legally liable for the specific balance. This process ensures the debt is accurate, within the statute of limitations, and properly calculated before any payment is made. By demanding verification, co-signers protect their credit scores from errors and ensure the original lender has the legal right to collect the funds from them directly.

Third-Party Collection Co-Signer Debt Validation Notice Letter

A Third-Party Collection Co-Signer Debt Validation Notice Letter is a formal document used to verify the legitimacy of a debt claim against a secondary liable party. It is essential to request this validation within thirty days of initial contact to exercise your rights under the Fair Debt Collection Practices Act. This letter forces the collector to provide proof of the original agreement and the exact balance owed. Sending this notice can prevent identity theft, stop harassment, and ensure that co-signers are not held responsible for inaccurate or expired financial obligations.

Post-Default Co-Signer Debt Validation Notice Letter

A Post-Default Co-Signer Debt Validation Notice Letter is a critical legal document sent after a primary borrower defaults. It formally notifies the co-signer of their legal liability for the outstanding balance. Under federal law, you have the right to request debt verification to ensure the amount is accurate and the collector has the authority to seek payment. Reviewing this notice immediately is essential to protect your credit score and understand your options for dispute or settlement before further legal action or collection efforts escalate against your personal assets.

Disputed Account Co-Signer Debt Validation Notice Letter

A Disputed Account Co-Signer Debt Validation Notice Letter is a formal legal request sent to creditors to verify the accuracy and legitimacy of a claimed debt. As a co-signer, you possess the same rights as the primary borrower to demand proof of the obligation, including original contracts and payment histories. Filing this dispute within thirty days of initial contact halts collection activities until the agency provides verification. This essential document protects your credit score from erroneous reporting and ensures you are not held liable for unauthorized or inaccurate charges assigned to your name.

Delinquent Account Co-Signer Debt Validation Notice Letter

A Debt Validation Notice is a critical legal protection for a co-signer facing a delinquent account. Under the FDCPA, this letter demands that collectors provide verifiable proof of the debt's validity and your legal obligation to pay. Sending this request within thirty days of initial contact halts collection activities until evidence is provided. It ensures you are not held liable for inaccurate amounts or unauthorized charges. Always use certified mail to maintain a legal paper trail, protecting your credit score and consumer rights against aggressive or fraudulent collection attempts.

Original Creditor Co-Signer Debt Validation Notice Letter

An Original Creditor Co-Signer Debt Validation Notice Letter is a critical document for disputing liability. When a primary borrower defaults, the co-signer often receives a collection notice. Sending this letter requires the creditor to provide competent evidence of the debt and the co-signer's legal obligation to pay. It is essential for protecting your credit score and ensuring the creditor adheres to the Fair Debt Collection Practices Act (FDCPA). Always send this notice via certified mail within thirty days of the initial contact to preserve your consumer rights effectively.

Settlement Negotiation Co-Signer Debt Validation Notice Letter

A Settlement Negotiation Co-Signer Debt Validation Notice Letter is a formal legal document used to dispute or verify the accuracy of a claimed debt. Before committing to a settlement, it is critical to demand evidence that the collector has the legal right to pursue the balance. This letter protects co-signers by freezing collection activities until debt validation is provided. Always ensure the notice is sent via certified mail to maintain a paper trail, ensuring your consumer rights under the FDCPA are fully enforced before negotiating any payment terms.

Credit Bureau Reporting Co-Signer Debt Validation Notice Letter

A Credit Bureau Reporting Co-Signer Debt Validation Notice Letter is a formal legal request used to verify the legitimacy of a debt before it impacts your credit score. As a co-signer, you have the right to demand written proof of the original agreement and the exact balance owed. Sending this notice within thirty days of initial contact forces the collection agency to cease reporting until the debt is validated. This ensures your credit profile remains protected from inaccurate or fraudulent claims caused by the primary borrower's default or administrative errors.

What is a Co-Signer Debt Validation Notice Letter?

A Co-Signer Debt Validation Notice Letter is a formal written request sent to a debt collector demanding proof that the co-signer is legally responsible for a specific debt. Under the Fair Debt Collection Practices Act (FDCPA), this letter forces the agency to provide evidence of the original contract and the exact balance owed before they can continue collection efforts.

When should a co-signer send a debt validation request?

A co-signer should send this letter within 30 days of receiving the initial notice of collection. Promptly mailing this request legally obligates the debt collector to cease all collection activities, including reporting to credit bureaus, until they provide the required verification documents.

What information must be included in a co-signer debt validation letter?

The letter should include the co-signer's name and contact information, the account number referenced in the collection notice, a formal statement disputing the debt, and a demand for the original creditor's name and proof of the co-signing agreement. It is important to state that the request is being made under the FDCPA.

Can a debt collector contact a co-signer after receiving a validation letter?

No, once a debt collector receives a timely validation letter, they must stop all communication with the co-signer until they provide the requested proof. If they continue to demand payment or mark the debt as "verified" on a credit report without providing documentation, they may be in violation of federal law.

How does a debt validation letter protect a co-signer's credit score?

By sending a validation letter, a co-signer prevents the debt collector from reporting the debt as an undisputed late payment while the investigation is pending. If the collector cannot produce the original signed contract or proof of the debt's accuracy, they must stop reporting the item entirely, protecting the co-signer's credit profile from unfair damage.

Comments