A Guarantor Debt Validation Notice Letter is a formal legal request used to verify the legitimacy and accuracy of a debt claim against a co-signer. This crucial document ensures creditors provide documented proof of the obligation before collection actions proceed. Protecting your rights as a secondary debtor is essential for financial security. To help you get started, below are some ready to use templates.

Image cover: Guarantor Debt Validation: Essential Notice Templates and Formal Letter Samples

Letter Samples List

- Initial Guarantor Debt Validation Notice Letter

- Secondary Guarantor Debt Validation Notice Letter

- Commercial Guarantor Debt Validation Notice Letter

- Consumer Guarantor Debt Validation Notice Letter

- Guarantor Debt Validation Notice Follow-Up Letter

- Pre-Legal Guarantor Debt Validation Notice Letter

- Guarantor Debt Validation Dispute Response Letter

- Secured Loan Guarantor Debt Validation Notice Letter

- Unsecured Loan Guarantor Debt Validation Notice Letter

- Final Guarantor Debt Validation Warning Letter

- Guarantor Debt Validation Settlement Offer Letter

- Guarantor Debt Validation Notice Letter With Contract Proof

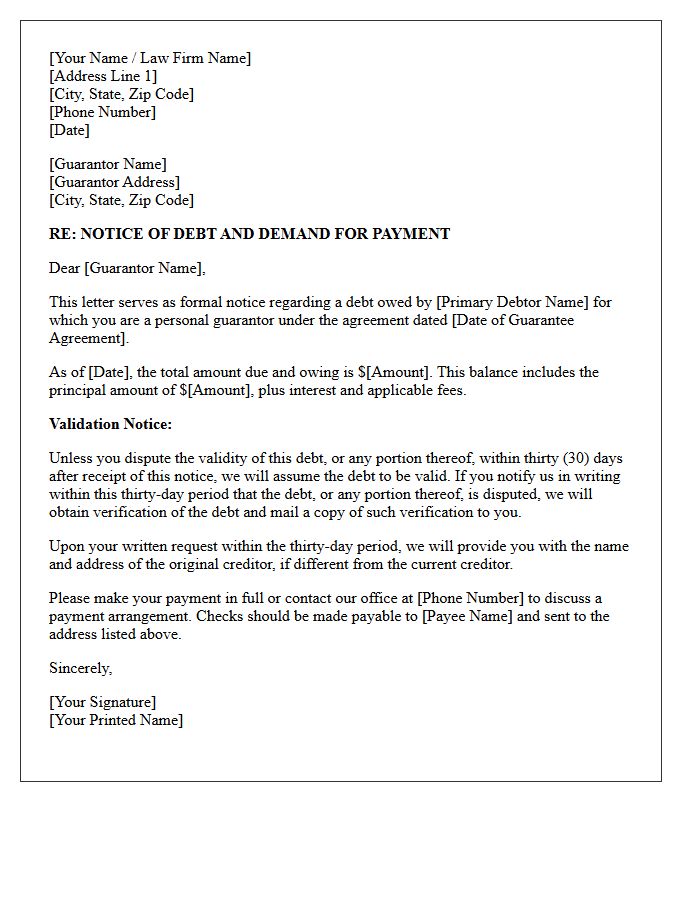

Initial Guarantor Debt Validation Notice Letter

The Initial Guarantor Debt Validation Notice Letter is a critical legal document sent by collectors to inform a secondary liable party of their obligation. Under the Fair Debt Collection Practices Act (FDCPA), this notice must outline the total amount owed and the original creditor's identity. It grants a thirty-day window for the recipient to formally dispute the debt's accuracy in writing. Failure to respond within this timeframe allows the agency to assume the debt is valid, making immediate verification essential for protecting your credit rights and legal standing.

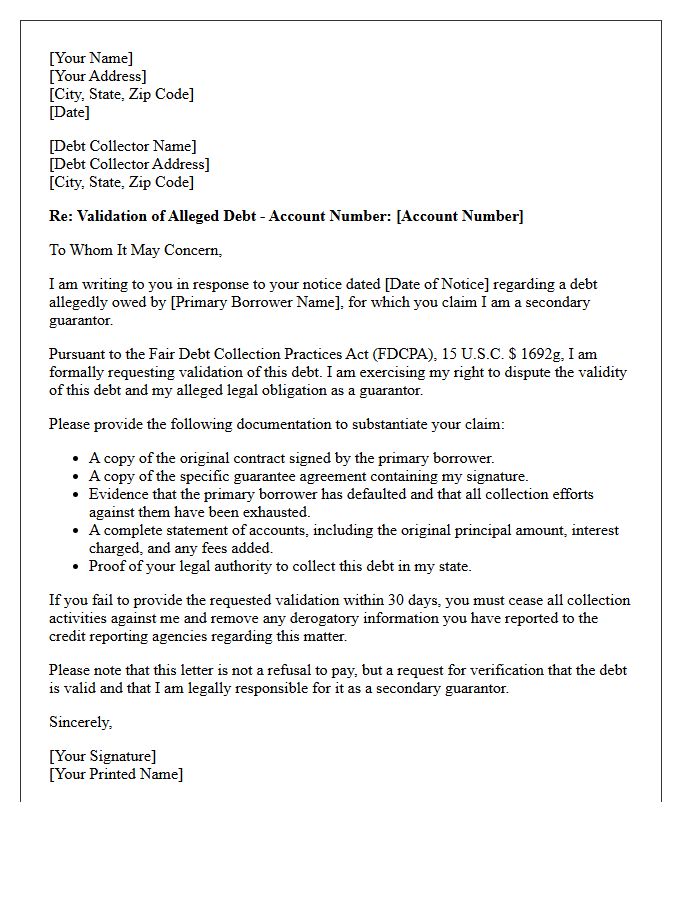

Secondary Guarantor Debt Validation Notice Letter

A secondary guarantor debt validation notice letter is a formal document sent to an individual who co-signed or guaranteed a loan after the primary guarantor. It is crucial to verify the debt's accuracy within 30 days of receipt to protect your consumer rights. This letter ensures that secondary guarantors are not held liable for incorrect balances or unauthorized claims. Validating the debt prevents improper credit reporting and allows you to dispute any discrepancies before legal action is taken, ensuring you only pay what is legally owed under the original guarantee agreement.

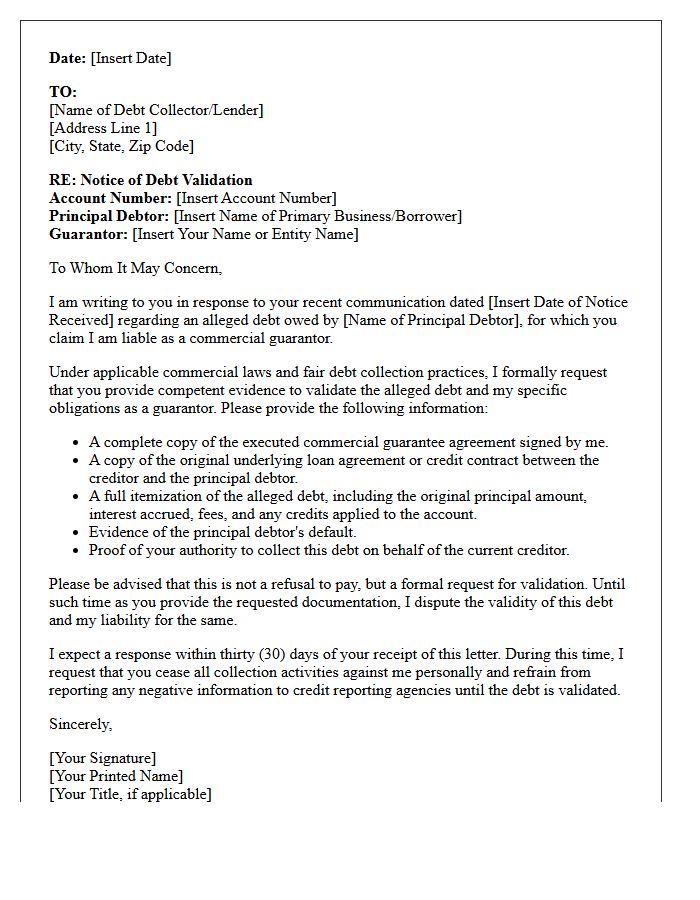

Commercial Guarantor Debt Validation Notice Letter

A Commercial Guarantor Debt Validation Notice Letter is a critical legal document sent to individuals who personally guaranteed a business loan. It serves as formal notification that a debt is being collected from the guarantor following a default. Under specific laws, you have the right to request verification of the debt's accuracy and the collector's authority. Upon receipt, you must act quickly to dispute discrepancies or confirm the total liability amount. Responding within the specified timeframe is essential to protect your personal assets and exercise your legal rights under commercial lending regulations.

Consumer Guarantor Debt Validation Notice Letter

A Consumer Guarantor Debt Validation Notice Letter is a formal legal document used to verify the legitimacy of an alleged debt. Under the Fair Debt Collection Practices Act, you have the right to request written verification from collectors within thirty days of their initial contact. This process ensures the debt amount is accurate and the collector has the legal authority to pursue payment from you as a guarantor. Sending this letter protects your rights by pausing collection activities until the agency provides substantial proof of the financial obligation.

Guarantor Debt Validation Notice Follow-Up Letter

A guarantor debt validation notice follow-up letter is a critical tool for disputing unverified claims after an initial request. It serves as a formal notice that the collector failed to provide adequate verification of the debt within the legal timeframe. This document protects your rights under the Fair Debt Collection Practices Act (FDCPA) by demanding the removal of unsubstantiated records from your credit profile. Ensuring this paper trail exists is essential for legal protection and prevents collectors from pursuing payment without providing sufficient evidence of your personal liability.

Pre-Legal Guarantor Debt Validation Notice Letter

A Pre-Legal Guarantor Debt Validation Notice Letter is a formal document sent to a co-signer before litigation begins. This notice fulfills the legal requirement to inform you of your right to dispute the alleged debt's validity. It must specify the outstanding balance and the original creditor's identity. Upon receipt, you have a 30-day window to request written verification. Exercising this right forces the collector to halt enforcement actions until they provide proof of your liability, ensuring consumer protection and debt transparency under relevant fair collection laws.

Guarantor Debt Validation Dispute Response Letter

A Guarantor Debt Validation Dispute Response Letter is a formal legal notification sent to creditors or collection agencies. It asserts your rights under the Fair Debt Collection Practices Act to verify the legitimacy and accuracy of a claimed debt. This document demands proof of the original agreement, the exact balance owed, and your legal obligation as a guarantor. Sending this response is crucial for halting collection activities and protecting your credit score while you challenge potential errors, unauthorized charges, or statute of limitations violations regarding the co-signed liability.

Secured Loan Guarantor Debt Validation Notice Letter

A Secured Loan Guarantor Debt Validation Notice Letter is a formal legal document used to verify the legitimacy of a debt claim. It protects guarantors by demanding proof of liability and accurate account balances from creditors. Sending this letter within thirty days of initial contact invokes your rights under consumer protection laws, forcing the lender to provide the original contract and payment history. This process ensures you are not held responsible for invalid, expired, or incorrect debts tied to a primary borrower's default before any collection actions proceed.

Unsecured Loan Guarantor Debt Validation Notice Letter

An Unsecured Loan Guarantor Debt Validation Notice Letter is a formal legal request sent to creditors or collection agencies. Its primary purpose is to demand verified evidence that you are legally responsible for a debt as a guarantor. Under the Fair Debt Collection Practices Act, this letter requires the collector to provide the original contract and proof of the outstanding balance. Sending this document is a crucial step to prevent identity theft or inaccurate reporting, ensuring you are not held liable for unauthorized or expired financial obligations.

Final Guarantor Debt Validation Warning Letter

A Final Guarantor Debt Validation Warning Letter is a critical formal notice issued before legal action or credit reporting occurs. It provides the last opportunity for a guarantor to verify the legitimacy, amount, and origin of a debt they co-signed. Upon receiving this, you must act within the specified timeframe to dispute inaccuracies or arrange payment. Failure to respond often results in immediate litigation or severe damage to your credit score. Always cross-reference the claim against original loan agreements to ensure your legal liability remains valid under current financial regulations.

Guarantor Debt Validation Settlement Offer Letter

A Guarantor Debt Validation Settlement Offer Letter is a formal document used to dispute or settle a debt when you have co-signed for another party. It serves to request legal verification of the debt's validity while simultaneously proposing a reduced payment to resolve the obligation. This dual-purpose strategy ensures the creditor proves their legal right to collect before any funds are exchanged. Utilizing this letter protects your credit score and provides a written record of the settlement agreement, preventing future collection attempts on the remaining balance once the offer is accepted.

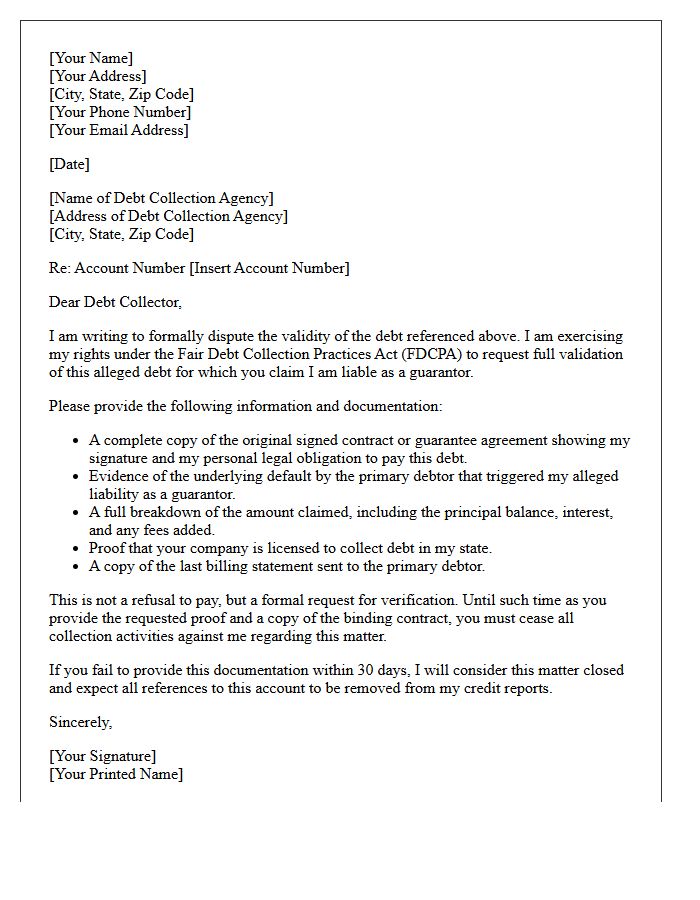

Guarantor Debt Validation Notice Letter With Contract Proof

A Guarantor Debt Validation Notice Letter is a formal legal request used to dispute an alleged debt. When a collection agency contacts you regarding a secondary liability, you must demand contractual proof linking you to the original agreement. This process requires the collector to provide a signed contract showing your specific guarantee terms. If they fail to produce verified documentation of the underlying obligation within thirty days, they must cease all collection activities. Validating the debt ensures you are not held liable for unauthorized claims or expired legal obligations.

What is a Guarantor Debt Validation Notice Letter?

A Guarantor Debt Validation Notice Letter is a formal written request sent to a debt collector or creditor demanding proof that a guarantor is legally obligated to pay a specific debt. Under the Fair Debt Collection Practices Act (FDCPA), this document compels the collector to provide evidence of the guarantee agreement and the accuracy of the total amount claimed.

When should I send a validation letter as a debt guarantor?

You should send a debt validation letter within 30 days of receiving the initial "dunning" notice or collection letter. Acting within this window preserves your legal rights to dispute the debt and prevents the collector from assuming the debt is valid by default.

What information must be included in a Guarantor Debt Validation request?

The letter should include your full name, the account number, and a specific demand for the original signed guarantee contract, a breakdown of all interest and fees, and proof that the collector is legally authorized to collect the debt in your state.

Can a debt collector contact me after I send a validation letter?

Once a debt collector receives your validation notice, they must cease all collection activities until they provide the requested verification. If they fail to provide adequate documentation, they cannot legally continue to report the debt to credit bureaus or pursue payment from you as the guarantor.

Does signing as a guarantor mean I am responsible for the full debt?

Yes, typically a guarantor is secondary liable for the entire balance if the primary borrower defaults. However, by sending a validation letter, you can ensure that the creditor is following the specific terms of the guarantee agreement and that the statute of limitations for collection has not expired.

Comments