A Partial Payment Acknowledgment Validation Notice officially confirms receipt of a specific installment while outlining the remaining debt balance. This formal document ensures transparency, maintains accurate financial records, and protects both parties during the repayment process. It serves as essential legal proof of progress toward total debt resolution. To simplify your correspondence, below are some ready to use templates.

Image cover: Professional Partial Payment Acknowledgment: Validation Notice Templates and Guide

Letter Samples List

- Partial Payment Acknowledgment and Debt Validation Letter

- Validation Notice and Partial Payment Receipt Letter

- Remaining Balance Validation and Partial Payment Letter

- Debt Collection Partial Payment Acknowledgment Letter

- Notice of Partial Payment and Account Validation Letter

- First Partial Payment Receipt and Validation Letter

- Outstanding Balance Validation and Payment Acknowledgment Letter

- Consumer Rights Validation and Partial Payment Letter

- Partial Payment Acceptance and Debt Validation Letter

- Account Update Validation and Partial Payment Letter

- Post-Payment Debt Validation Acknowledgment Letter

- Good Faith Partial Payment and Validation Notice Letter

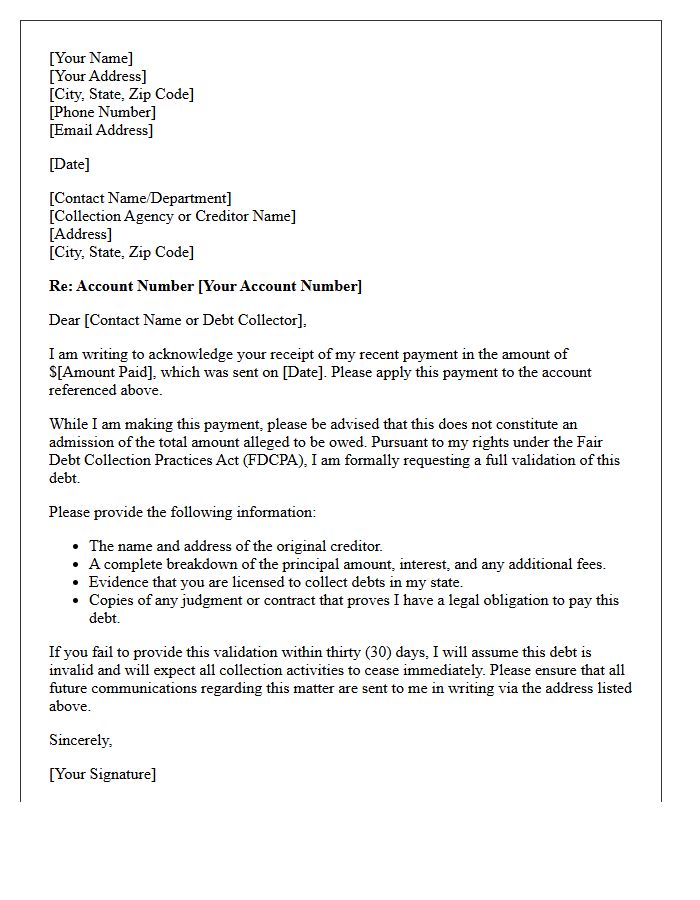

Partial Payment Acknowledgment and Debt Validation Letter

A Partial Payment Acknowledgment confirms receipt of a specific amount toward an outstanding balance. When combined with a Debt Validation Letter, it ensures the creditor or collector legally verifies the debt's accuracy and ownership. Sending these documents protects your rights under fair debt collection laws by preventing unauthorized collections and providing a formal paper trail. Always specify that a partial payment is not an admission of the total debt validity unless explicitly stated, helping to manage liabilities while maintaining legal leverage during negotiations or disputes.

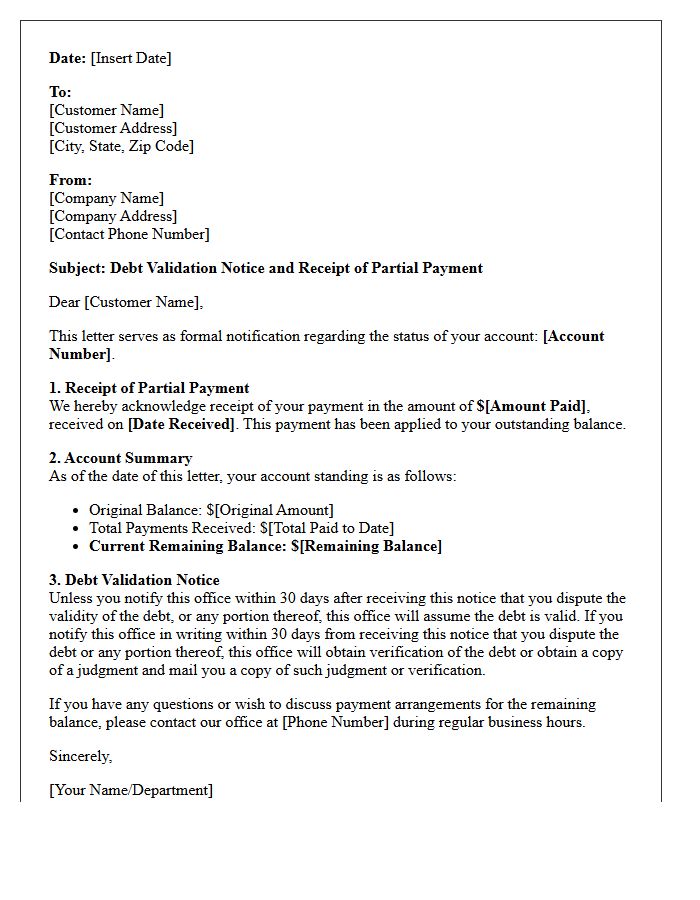

Validation Notice and Partial Payment Receipt Letter

A Validation Notice is a legal requirement under the FDCPA, ensuring consumers receive written proof of a debt's origin and amount. When combined with a Partial Payment Receipt, it acknowledges that a transaction occurred without waiving your right to dispute the remaining balance. Always verify the debt collector's credentials before paying. Keep these documents as essential evidence to track your repayment progress and protect against potential identity theft or inaccurate reporting on your credit file. Clear documentation prevents future legal disputes regarding outstanding liabilities.

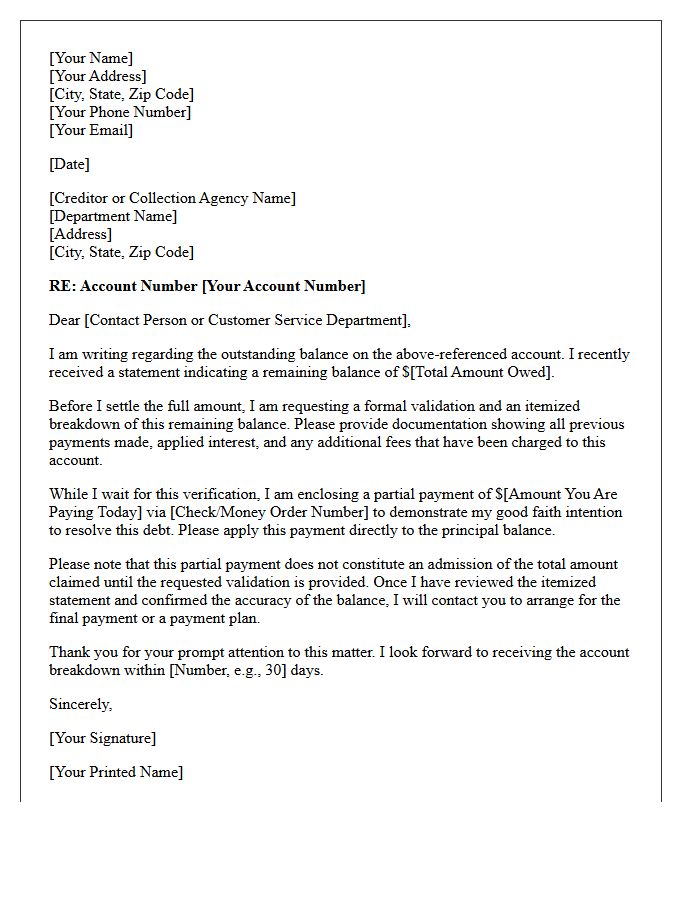

Remaining Balance Validation and Partial Payment Letter

A Remaining Balance Validation is a critical process where a debtor confirms the exact outstanding amount owed to ensure billing accuracy and prevent overpayment. When providing a Partial Payment Letter, the debtor acknowledges the total debt while formalizing a commitment to pay in installments. This documentation protects both parties by establishing a clear payment record and preventing legal disputes. It is essential to include account details, the payment date, and the remaining unpaid balance to maintain financial transparency and avoid potential credit score penalties or collection escalations.

Debt Collection Partial Payment Acknowledgment Letter

A Debt Collection Partial Payment Acknowledgment Letter is a formal document issued by a creditor to confirm receipt of a specific installment. It serves as legal evidence of your payment, ensuring your remaining balance is updated accurately. This letter should clearly state the amount paid, the date received, and the outstanding balance. Retaining these records is essential for debt verification and protecting your consumer rights against future disputes or errors in your credit report during the repayment process.

Notice of Partial Payment and Account Validation Letter

A Notice of Partial Payment and Account Validation Letter is a critical legal tool for consumers disputing debt accuracy. This document formally acknowledges a specific payment while demanding the collector provide verification of the remaining balance. By requesting validation, you exercise your rights under the Fair Debt Collection Practices Act (FDCPA) to ensure the debt is legitimate and the amount is correct. Sending this letter via certified mail creates a paper trail, preventing creditors from claiming full default while you challenge discrepancies or negotiate settlement terms effectively.

First Partial Payment Receipt and Validation Letter

A First Partial Payment Receipt serves as legal proof of your initial transaction toward a debt. Following this, a Validation Letter is essential to confirm the remaining balance and verify the creditor's authority to collect. Always ensure these documents match your records to prevent errors or fraudulent claims. Retaining both files protects your consumer rights and provides a clear paper trail for future credit reporting. Verifying the legitimacy of the debt through official validation ensures that your partial payment is accurately applied toward the total liability.

Outstanding Balance Validation and Payment Acknowledgment Letter

An Outstanding Balance Validation letter serves as a legal safeguard to confirm debt accuracy, protecting consumers under the Fair Debt Collection Practices Act. It mandates that creditors provide verifiable proof of the amount owed before further collection occurs. Once resolved, a Payment Acknowledgment Letter provides essential written evidence that the financial obligation is satisfied. Retaining these documents is crucial for correcting credit reports, preventing double-billing, and ensuring long-term debt resolution. Always verify balances in writing to maintain clear financial records and legal protection against erroneous claims.

Consumer Rights Validation and Partial Payment Letter

A Consumer Rights Validation letter is a vital legal tool used to dispute inaccurate debts and demand proof of a creditor's claim. Combining this with a partial payment offer can help settle balances while maintaining your legal protections. It is crucial to send these documents via certified mail to ensure a paper trail. By formally requesting verification before paying, you prevent debt collectors from pursuing unsubstantiated claims, effectively protecting your credit score and financial standing under the Fair Debt Collection Practices Act (FDCPA).

Partial Payment Acceptance and Debt Validation Letter

When dealing with debt collection, understand that making a partial payment may inadvertently acknowledge the debt's validity, potentially restarting the statute of limitations. Before sending any money, you should issue a debt validation letter to the collector. This formal request mandates that the agency provides legal proof of the amount owed and their authority to collect it. Protecting your consumer rights ensures you do not pay unauthorized claims or forfeit legal defenses by mistake. Always verify the debt in writing before committing to any payment plan.

Account Update Validation and Partial Payment Letter

An Account Update Validation ensures financial records reflect accurate balances after a Partial Payment Letter is issued. This correspondence formally documents a debtor's intent to pay a portion of the debt, which must be legally validated to prevent automated collections errors. It is essential to confirm that the reduced payment is correctly applied to the principal to maintain credit score integrity and avoid legal disputes regarding the remaining balance.

Post-Payment Debt Validation Acknowledgment Letter

A Post-Payment Debt Validation Acknowledgment Letter is a formal document sent to a creditor or collection agency after a debt has been settled. Its primary purpose is to confirm that the balance is officially zero and that the obligation is fulfilled. This written confirmation serves as vital legal evidence to prevent future collection attempts on the same account. It is essential for ensuring accurate credit reporting, as it compels the agency to update your file, protecting your financial reputation from lingering errors or duplicate claims regarding resolved liabilities.

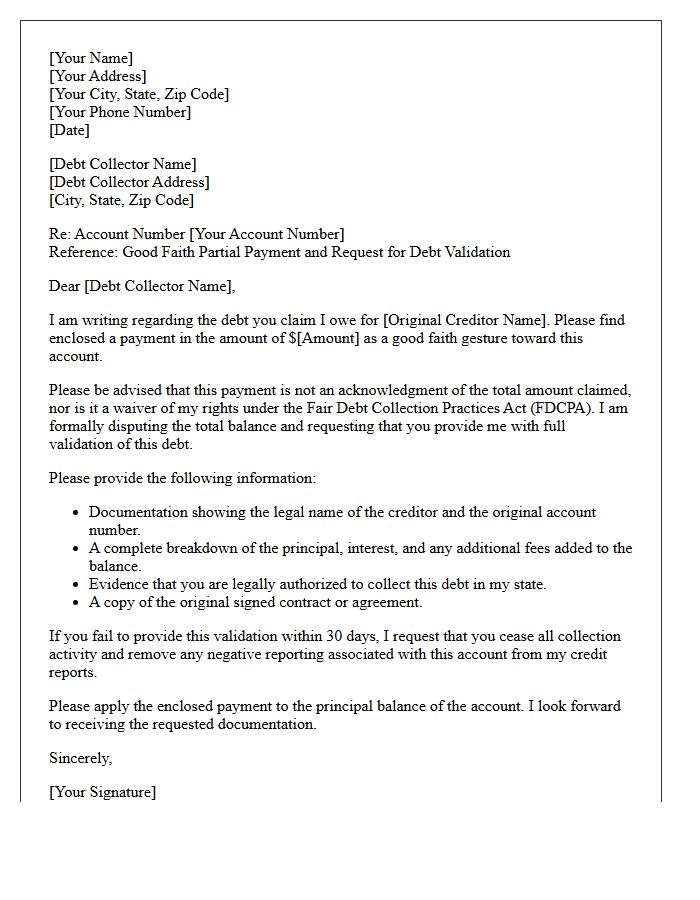

Good Faith Partial Payment and Validation Notice Letter

A Validation Notice Letter is a critical legal document sent by debt collectors to confirm a debt's details. If you disagree with the amount, you must dispute it in writing within 30 days. Sending a Good Faith Partial Payment can demonstrate your willingness to resolve the debt; however, be cautious, as this may restart the statute of limitations on an expired debt. Always verify the debt's accuracy before making payments to protect your consumer rights and maintain your financial standing.

What is a Partial Payment Acknowledgment Validation Notice?

A Partial Payment Acknowledgment Validation Notice is an official document sent by a creditor or service provider to confirm the receipt of a payment that does not cover the full outstanding balance. It validates the specific amount received while detailing the remaining debt still owed by the account holder.

Does receiving a partial payment acknowledgment mean my debt is settled?

No, receiving this notice does not indicate that the debt is settled in full. It serves only as a validation of the specific transaction amount processed. Unless explicitly stated as a "settlement in full," the account remains active with a pending balance that requires further payment.

What information should be included in a payment validation notice?

A standard notice should include the date the payment was received, the payment method used, the specific amount credited to the account, the current remaining balance, and the deadline for the next payment to avoid late fees or collection actions.

How does a partial payment validation affect my credit score?

The acknowledgment notice itself does not affect your credit score; however, the act of making a partial payment rather than a full payment may impact your credit. While it demonstrates an intent to pay, the account may still be reported as "past due" or "partially paid" to credit bureaus if the minimum required amount is not met.

Can I use this notice as legal proof of payment?

Yes, the Partial Payment Acknowledgment Validation Notice serves as a primary receipt and legal record of the transaction. It protects the consumer by providing documented evidence of the amount paid, ensuring the creditor cannot claim non-payment for that specific portion of the debt.

Comments