A Commercial Liability Policy Reinstatement Letter is a formal request sent to an insurance provider to restore coverage after a cancellation or lapse. This document explains the reasons for the break in protection and confirms the resolution of outstanding issues, such as missed payments. Ensuring your business remains protected is critical for risk management. Below are some ready to use templates.

Image cover: Professional Templates for Commercial Liability Policy Reinstatement Letters

Letter Samples List

- Commercial Liability Policy Reinstatement Request Letter

- Agency Confirmation of Policy Reinstatement Letter

- Statement of No Loss for Reinstatement Letter

- Past Due Premium Payment Reinstatement Letter

- Lapsed Commercial Liability Reinstatement Letter

- Insurance Carrier Reinstatement Approval Letter

- Commercial Liability Reinstatement Denial Letter

- Agent to Underwriter Reinstatement Appeal Letter

- Reinstatement Pending Underwriting Review Letter

- Notice of Conditional Policy Reinstatement Letter

- Contractor Liability Policy Reinstatement Letter

- Business Liability Grace Period Reinstatement Letter

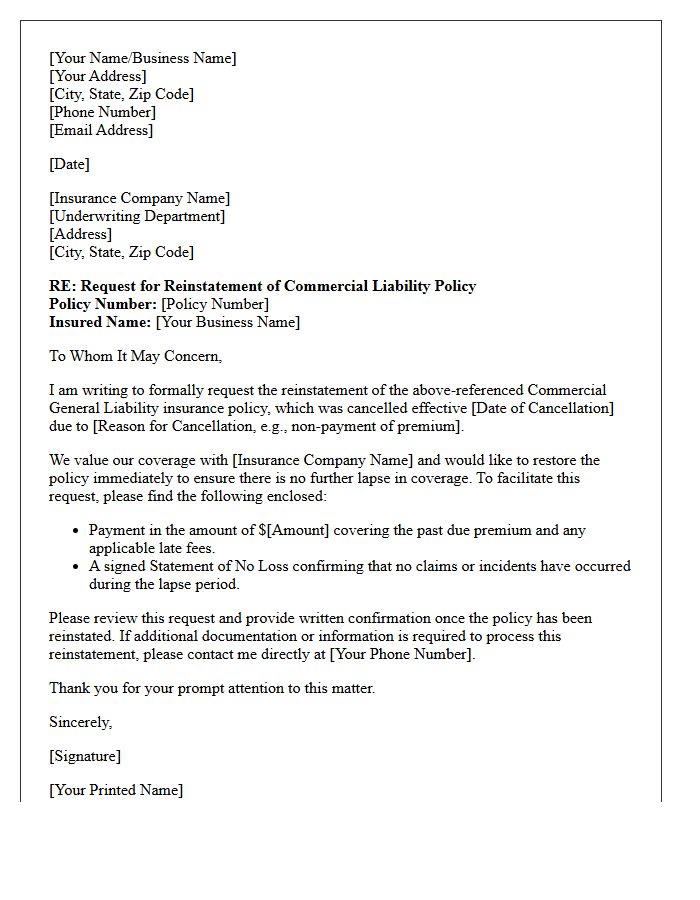

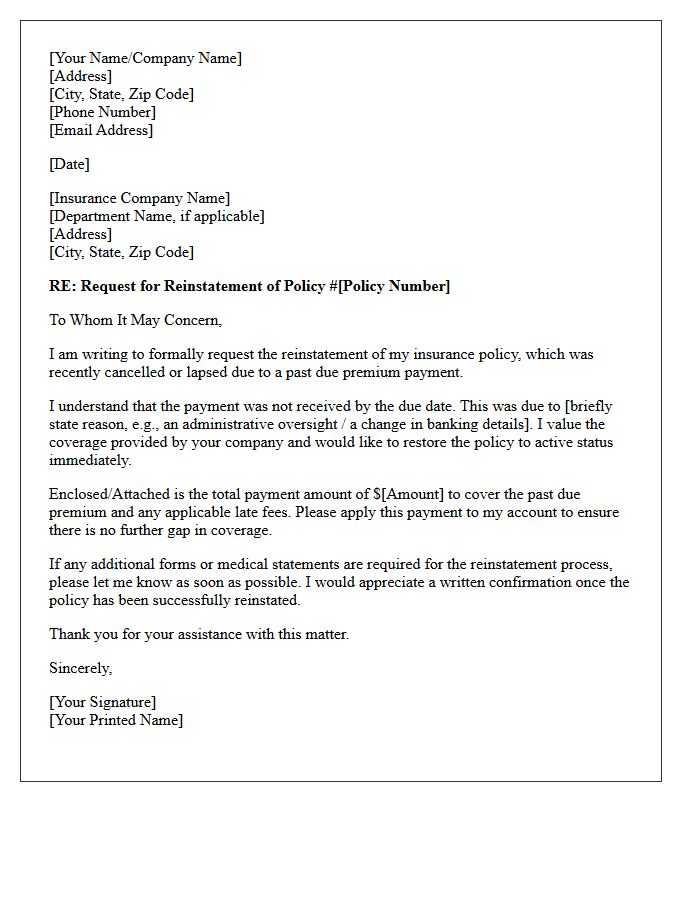

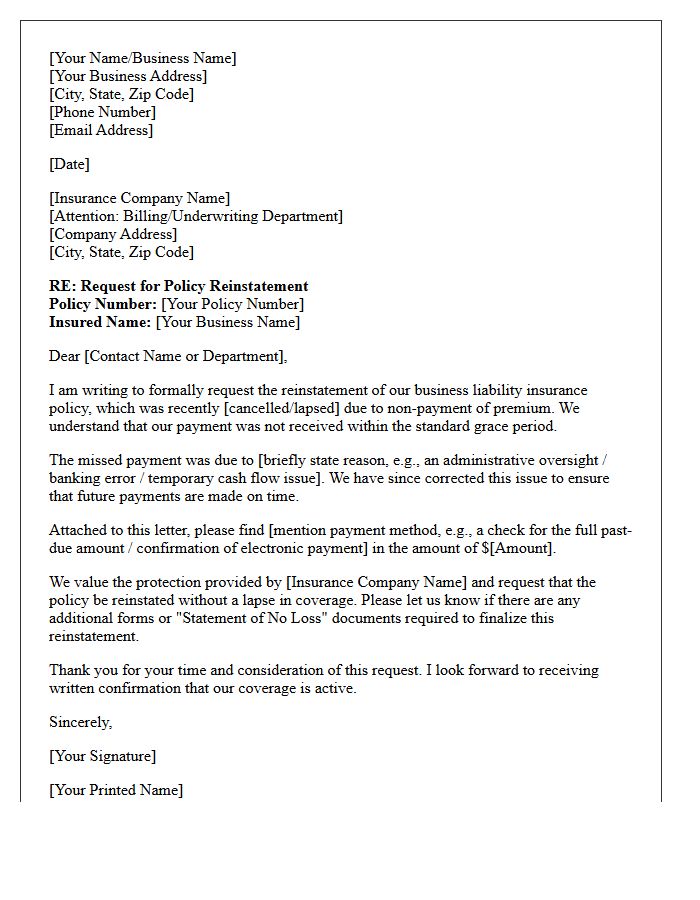

Commercial Liability Policy Reinstatement Request Letter

A Commercial Liability Policy Reinstatement Request Letter is a formal document sent to an insurer to restore canceled coverage. It must clearly state the policy number, the reason for the lapse, and a request to waive termination. To be successful, the insured should include proof of payment for outstanding premiums and a No Loss Statement confirming no claims occurred during the inactive period. Timely submission is critical to avoid a permanent gap in protection, ensuring your business remains legally compliant and shielded from potential third-party legal liabilities.

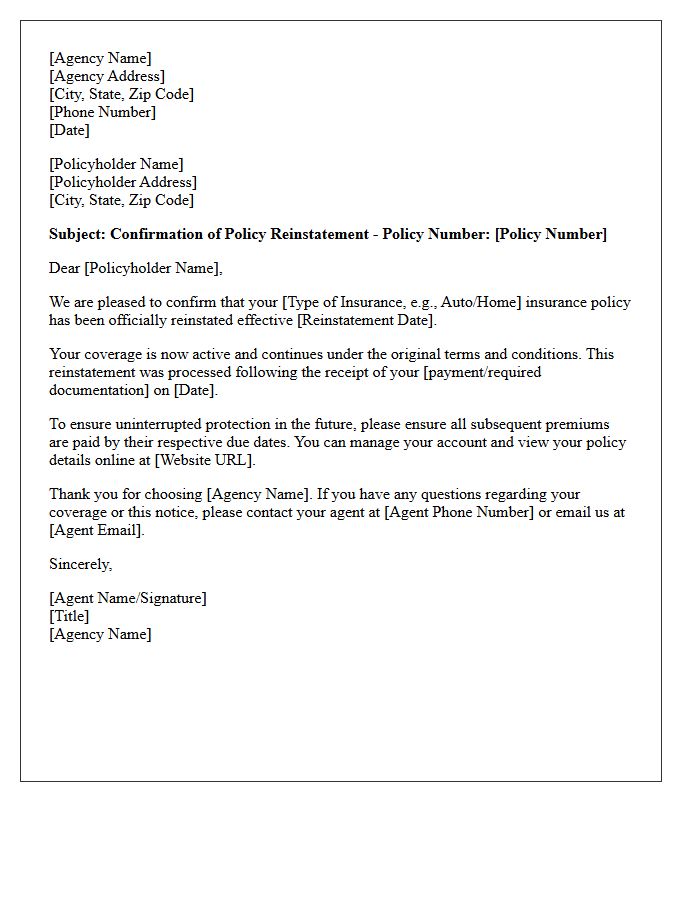

Agency Confirmation of Policy Reinstatement Letter

An Agency Confirmation of Policy Reinstatement Letter is a formal document verifying that a lapsed insurance policy is active again. This letter confirms that the insurer has accepted the reinstatement request and outstanding payments, restoring full coverage benefits. Policyholders should verify the effective date of restoration to ensure there are no gaps in protection. It serves as essential proof for legal and financial purposes, confirming the policy's current in-force status and ensuring that the terms and conditions remain valid following a temporary cancellation or expiration.

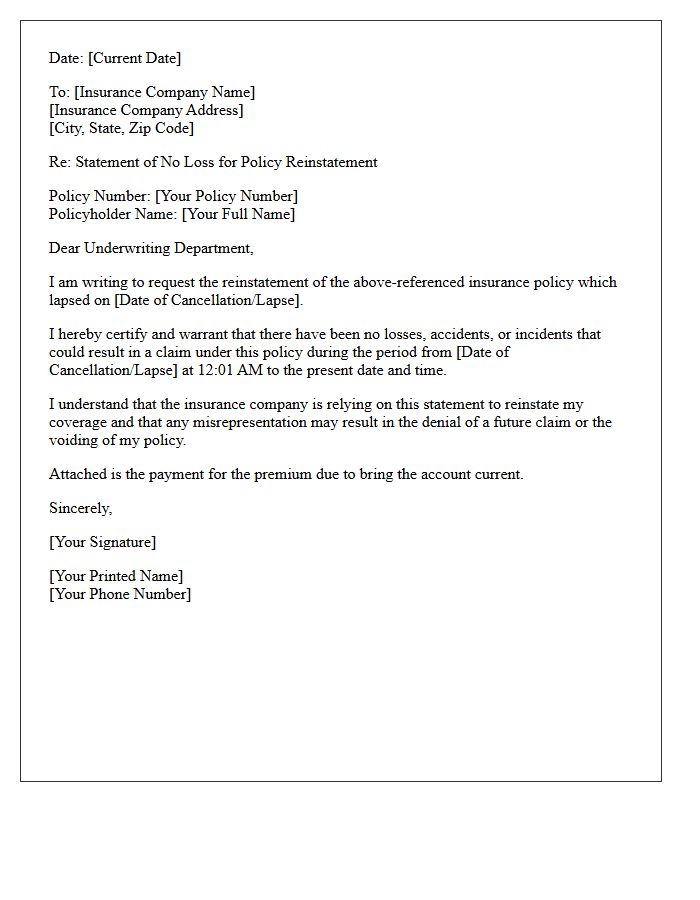

Statement of No Loss for Reinstatement Letter

A Statement of No Loss is a critical document required to reinstate a cancelled insurance policy. It serves as a legal affidavit confirming that no accidents or claims occurred during the period of lapsed coverage. By signing this letter, you verify that your property or vehicle remained undamaged while the policy was inactive. Accuracy is essential, as any misrepresentation constitutes insurance fraud, which can lead to permanent policy denial or legal action. Always submit this statement promptly to restore your protection and maintain continuous coverage history.

Past Due Premium Payment Reinstatement Letter

A Past Due Premium Payment Reinstatement Letter is a formal request to restore a cancelled insurance policy. It must acknowledge the missed deadline and include the full outstanding balance to prove financial commitment. Timely submission is critical because coverage remains inactive until the insurer approves the reinstatement application. Providing an honest explanation for the lapse can expedite the process. Always confirm if a new Statement of Good Health is required to ensure continuous protection against future risks without needing a brand-new policy evaluation.

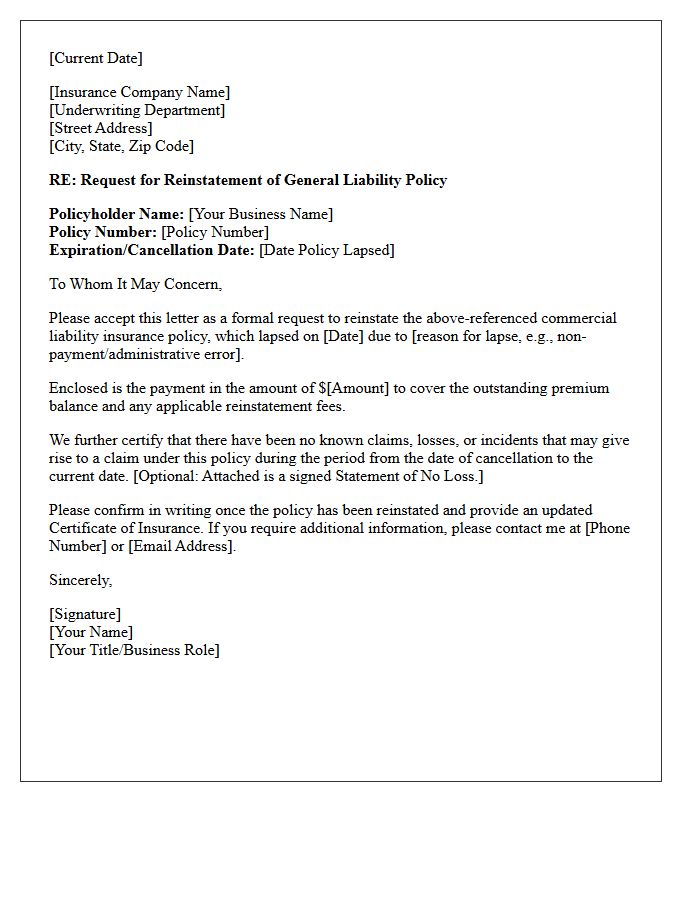

Lapsed Commercial Liability Reinstatement Letter

A Lapsed Commercial Liability Reinstatement Letter is a formal request sent to an insurance carrier to restore a cancelled policy. To ensure approval, the business owner must confirm there were no known losses during the gap in coverage. Providing a detailed explanation for the payment failure or administrative error is essential for underwriting approval. Once accepted, the insurer issues a notice of reinstatement, preventing permanent gaps in protection. Acting quickly is vital to maintain continuous coverage and comply with legal or contractual requirements governing your business operations.

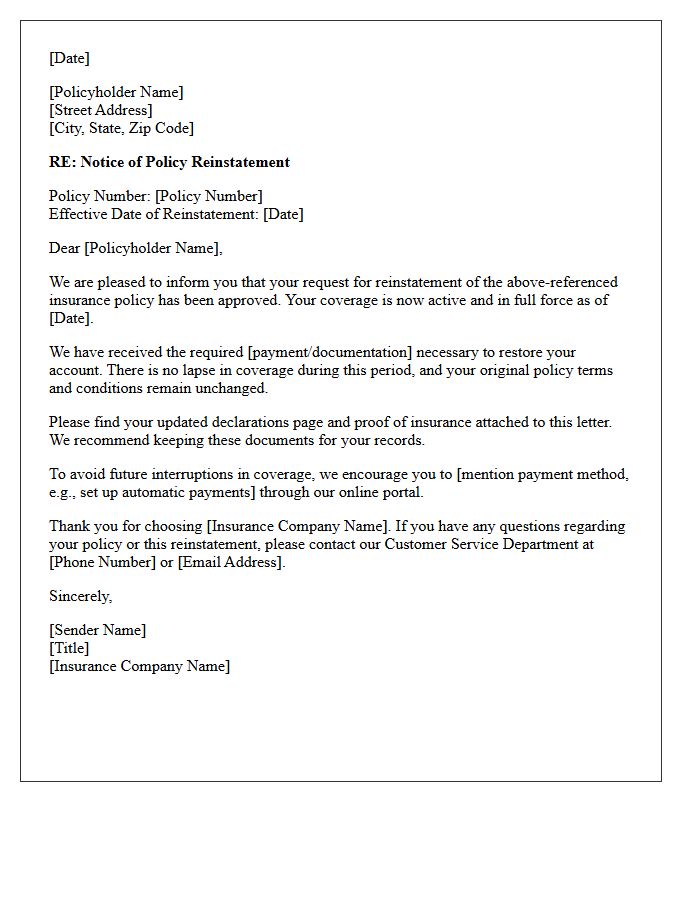

Insurance Carrier Reinstatement Approval Letter

An Insurance Carrier Reinstatement Approval Letter is a formal document confirming that a previously canceled or lapsed policy is once again active. This letter is crucial because it validates your continuous coverage, protecting you from financial liability during claims. Upon receipt, verify the reinstatement date and any specific conditions or fees required by the insurer. Keeping this approval on file is essential for proving compliance to lenders or state agencies and ensuring there are no gaps in your professional or personal protection.

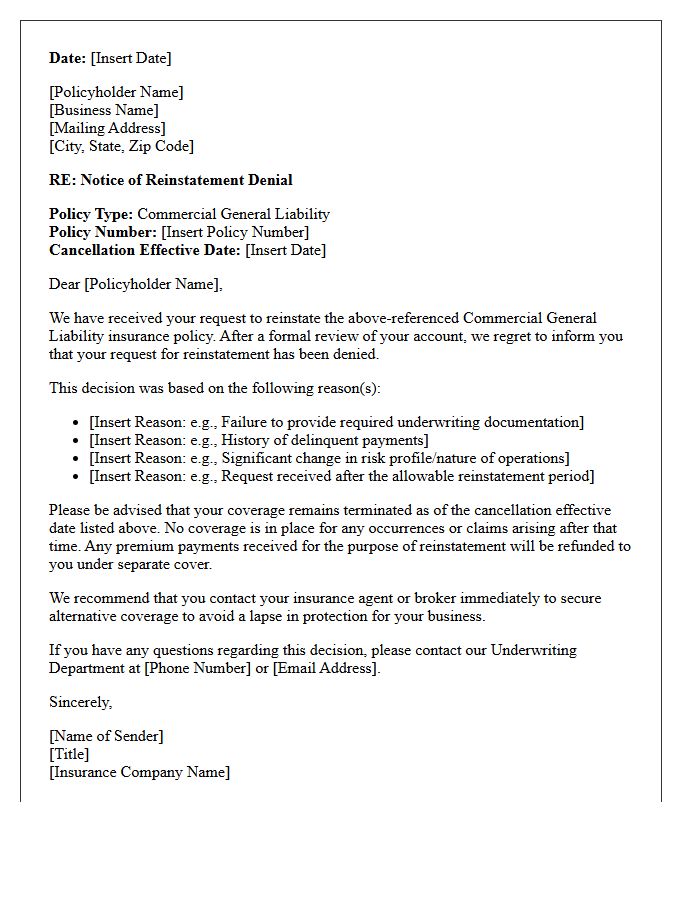

Commercial Liability Reinstatement Denial Letter

A Commercial Liability Reinstatement Denial Letter is a formal notification from an insurer rejecting a policyholder's request to reactivate canceled coverage. This document typically cites specific reasons for the refusal, such as frequent late payments, hazardous changes in business operations, or excessive claims history. Receiving this letter indicates a permanent lapse in protection, leaving the business legally and financially vulnerable. Business owners should immediately seek alternative coverage to avoid a coverage gap, as operating without active liability insurance poses a significant risk to corporate assets and professional reputation.

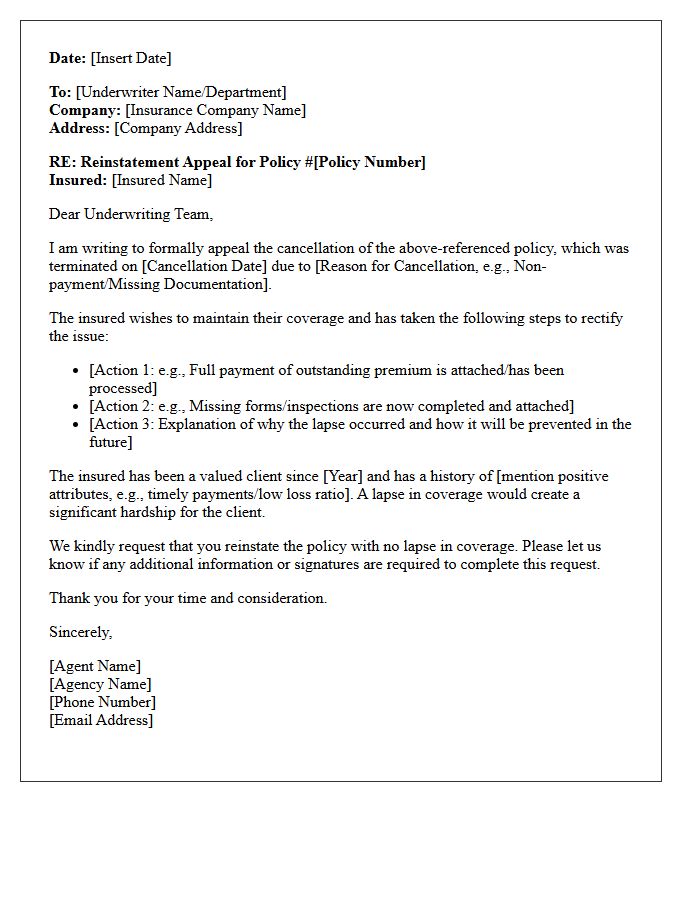

Agent to Underwriter Reinstatement Appeal Letter

An Agent to Underwriter Reinstatement Appeal Letter is a formal request to restore a cancelled insurance policy. The primary goal is to address the specific grounds for termination, such as missed payments or increased risk. A successful appeal must provide verifiable evidence of corrective actions and demonstrate the client's long-term value. Time is critical; agents should highlight mitigating circumstances and ensure all outstanding requirements are met. Professionalism and factual clarity are essential to convince the underwriter that the policy remains a sustainable and low-risk investment for the carrier.

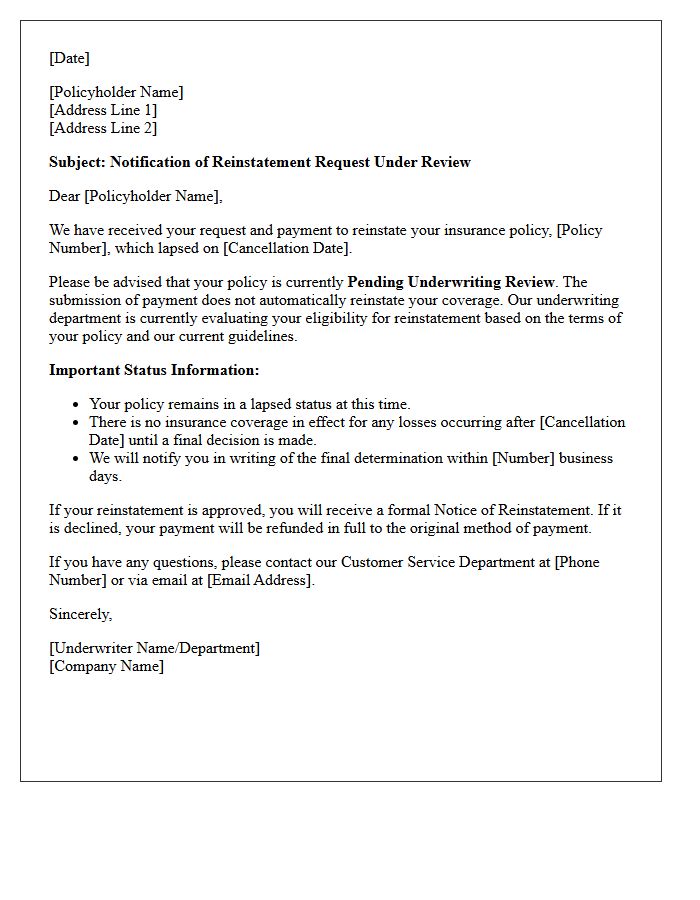

Reinstatement Pending Underwriting Review Letter

A Reinstatement Pending Underwriting Review letter indicates that your lapsed insurance policy is being evaluated for reactivation. Receiving this notice means the insurer is assessing your current risk profile before committing to coverage. During this period, you typically have no protection, and the company may request updated medical or financial information. It is crucial to provide any requested documents quickly to avoid a final denial of coverage. Always confirm if a premium payment is required upfront to keep the application active during the formal review process.

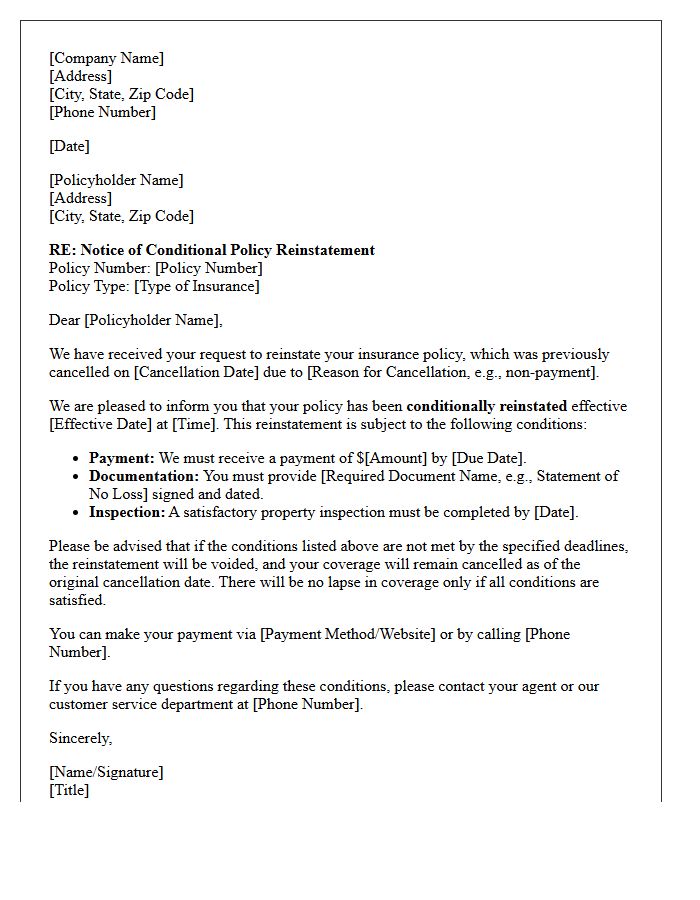

Notice of Conditional Policy Reinstatement Letter

A Notice of Conditional Policy Reinstatement Letter outlines the specific requirements to restore a lapsed insurance policy. Receiving this document means your coverage is currently inactive, but the insurer offers a limited opportunity to regain protection. To successfully reinstate, you must typically pay outstanding premiums and provide a statement of good health or evidence of insurability. It is crucial to meet all deadlines and conditions specified in the letter, as coverage is not guaranteed until the company formally approves your application and processes your payment.

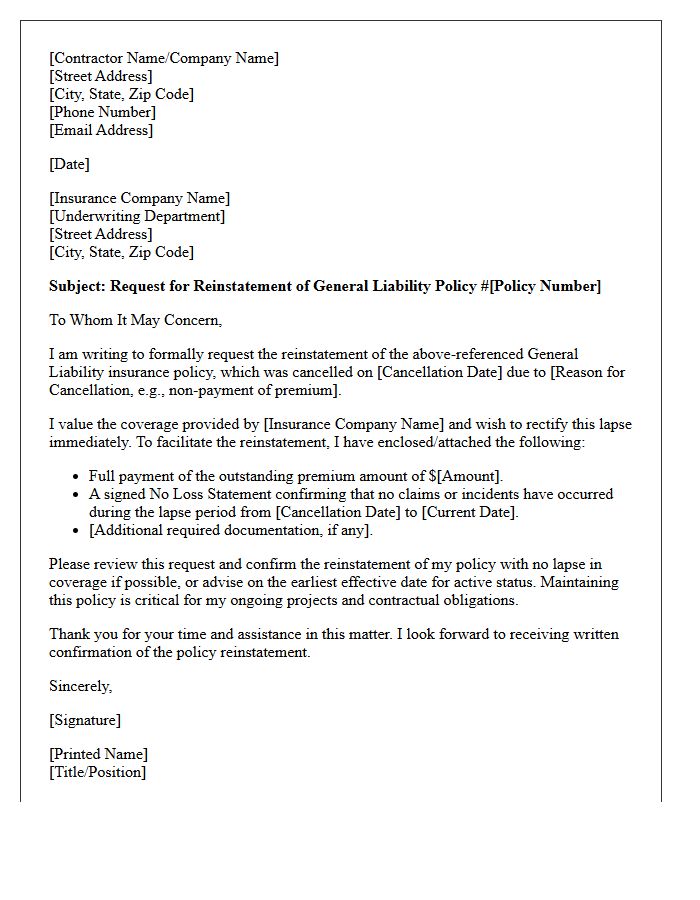

Contractor Liability Policy Reinstatement Letter

A Contractor Liability Policy Reinstatement Letter is a formal document issued by an insurer to restore coverage after a lapse or cancellation. It confirms that the reinstatement process is complete, ensuring the policyholder is legally protected and compliant with project requirements. Understanding the effective date is critical, as coverage may not be retroactive, leaving past gaps uninsured. Contractors must promptly address outstanding premiums or documentation requested in the letter to maintain active liability protection and avoid future policy termination or increased insurance costs.

Business Liability Grace Period Reinstatement Letter

A Business Liability Grace Period Reinstatement Letter is a formal request sent to an insurance provider to restore a cancelled policy. This document is essential when coverage lapses due to missed premium payments during the allowed grace period. To ensure successful reinstatement, business owners must explain the cause of the payment delay, provide proof of outstanding funds, and confirm that no claims occurred during the lapse. Timely submission is critical to avoid permanent loss of coverage and potential legal exposure for your business operations.

What is a commercial liability policy reinstatement letter?

A commercial liability policy reinstatement letter is an official document sent by an insurance carrier to a policyholder confirming that a previously cancelled or lapsed insurance policy has been restored to active status without a gap in coverage.

What information must be included in a reinstatement request letter?

A formal reinstatement request should include the business name, the specific policy number, the reason for the initial cancellation (such as non-payment), a request for continuous coverage, and a signature from the authorized policyholder or agent.

What are the common requirements to reinstate a cancelled commercial policy?

Insurance companies typically require the payment of all past-due premiums, a signed "Statement of No Losses" confirming no claims occurred during the lapse period, and potentially a reinstatement fee before issuing a formal letter of restoration.

Does a reinstatement letter guarantee there was no gap in coverage?

Yes, if the reinstatement letter specifies that the policy is restored "nunc pro tunc" or without a lapse, it confirms that the business remained continuously insured from the original effective date despite the temporary cancellation notice.

How long does it take to receive a formal reinstatement confirmation?

Once the outstanding premium is paid and the required "No Loss" affidavit is submitted, most commercial insurers issue the reinstatement letter within 24 to 48 business hours to ensure the business meets its contractual and legal obligations.

Comments