If your coverage has lapsed due to missed payments, a Life Insurance Policy Reinstatement Letter is the essential first step to restoring your financial protection. This formal request notifies your insurer of your intent to reactivate the policy and settle outstanding balances. Understanding the requirements ensures a smooth recovery of your benefits. To help you begin, below are some ready to use template.

Image cover: Official Guide and Templates for Your Life Insurance Policy Reinstatement Letter

Letter Samples List

- Standard Life Insurance Policy Reinstatement Letter

- Lapsed Life Insurance Policy Reinstatement Letter

- Past Due Premium Life Insurance Reinstatement Letter

- Statement Of Good Health Life Insurance Reinstatement Letter

- Conditional Life Insurance Policy Reinstatement Letter

- Underwriting Review Life Insurance Reinstatement Letter

- Agency Approved Life Insurance Policy Reinstatement Letter

- Denial Of Life Insurance Policy Reinstatement Letter

- Client Request For Life Insurance Reinstatement Letter

- Missing Information Life Insurance Policy Reinstatement Letter

- Grace Period Notice Life Insurance Reinstatement Letter

- Final Confirmation Life Insurance Policy Reinstatement Letter

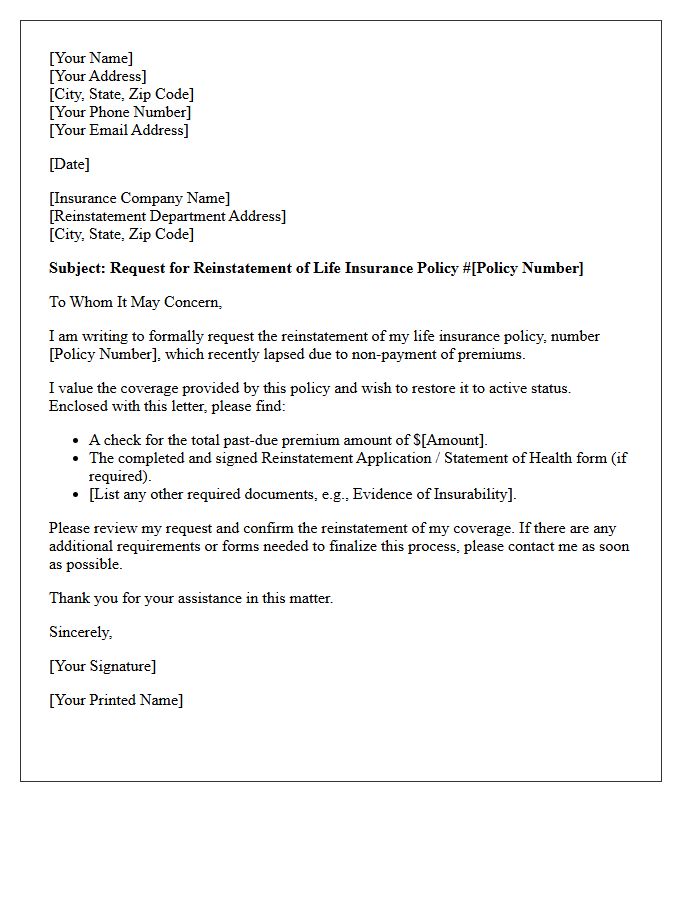

Standard Life Insurance Policy Reinstatement Letter

A Standard Life Insurance Policy Reinstatement Letter is a formal request to restore coverage after a policy has lapsed due to non-payment. To ensure successful reactivation, the policyholder must typically submit evidence of insurability, such as a health questionnaire, alongside all past-due premiums and interest. Timing is critical, as most insurers impose a specific window-often three to five years-for reinstatement. Once approved, this process allows you to maintain your original premium rates and policy terms without purchasing a new, potentially more expensive contract.

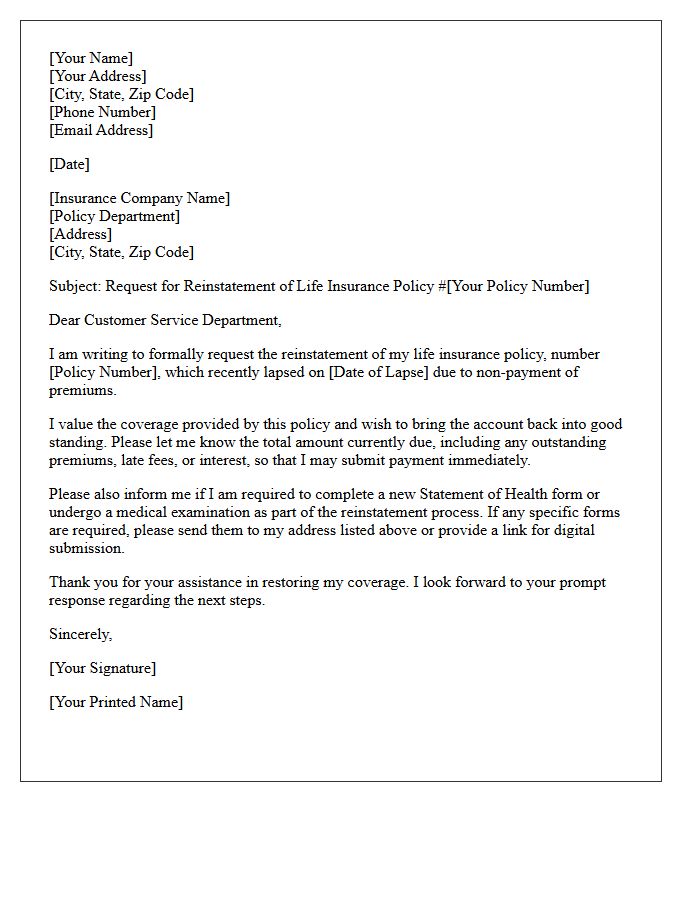

Lapsed Life Insurance Policy Reinstatement Letter

A lapsed life insurance policy reinstatement letter is a formal request to restore coverage after it terminated due to non-payment. To succeed, you must submit this written application within the insurer's specified grace period. Most companies require a statement of good health to prove insurability remains unchanged. Additionally, you must settle all outstanding premiums plus potential interest. Timely action is critical, as waiting too long may necessitate a new medical exam or result in a permanent loss of original policy benefits and rates.

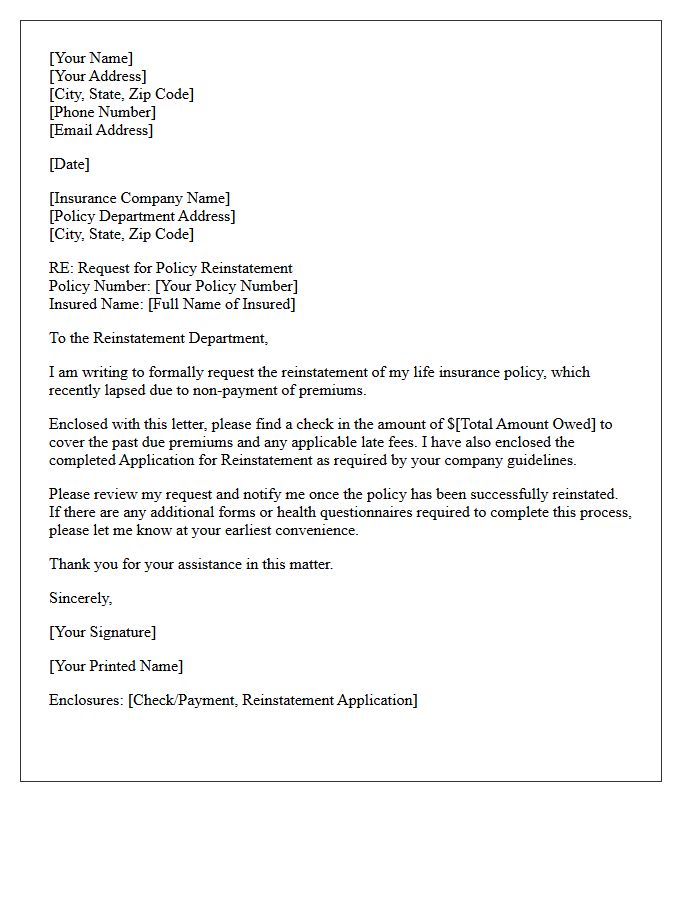

Past Due Premium Life Insurance Reinstatement Letter

A past due premium life insurance reinstatement letter is a formal request to restore a lapsed policy after the grace period ends. To regain coverage, the policyholder must typically submit a reinstatement application, provide updated evidence of insurability, and pay all overdue premiums plus interest. Timely action is essential to avoid permanent loss of benefits and higher rates associated with new policies. Always verify the specific reinstatement requirements with your insurer to ensure continuous financial protection for your beneficiaries.

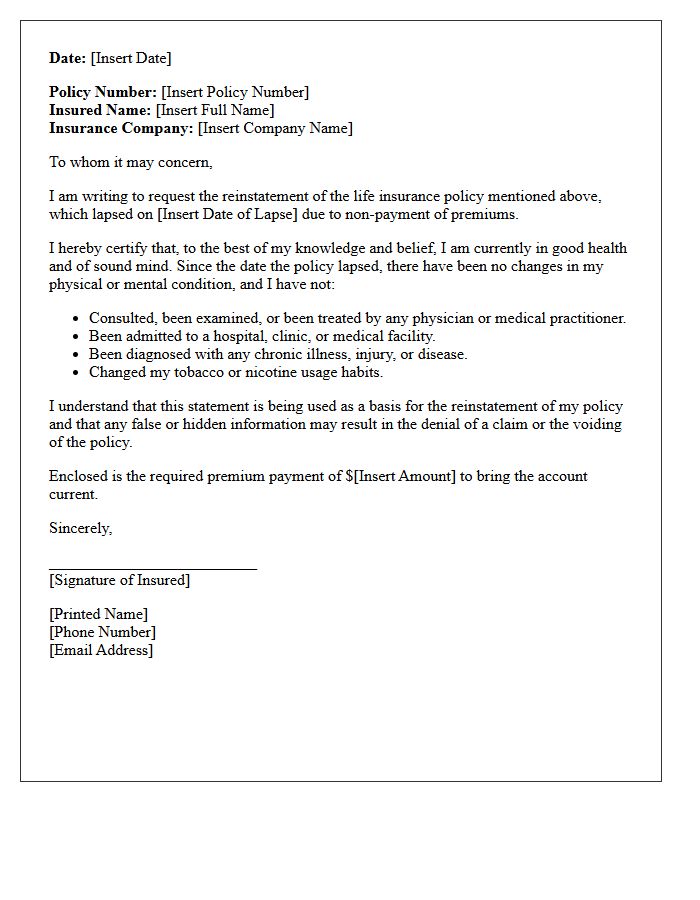

Statement Of Good Health Life Insurance Reinstatement Letter

A Statement of Good Health is a mandatory document required when reinstating a life insurance policy that has lapsed due to non-payment. This self-certification confirms that the insured's medical condition has not deteriorated since the original policy issuance. To successfully restore coverage, the policyholder must honestly disclose any new medical diagnoses or health changes. Insurers use this letter to reassess risk before approving the reinstatement. Providing accurate information is critical, as any material misrepresentation can lead to a future claim denial or the permanent termination of the insurance contract.

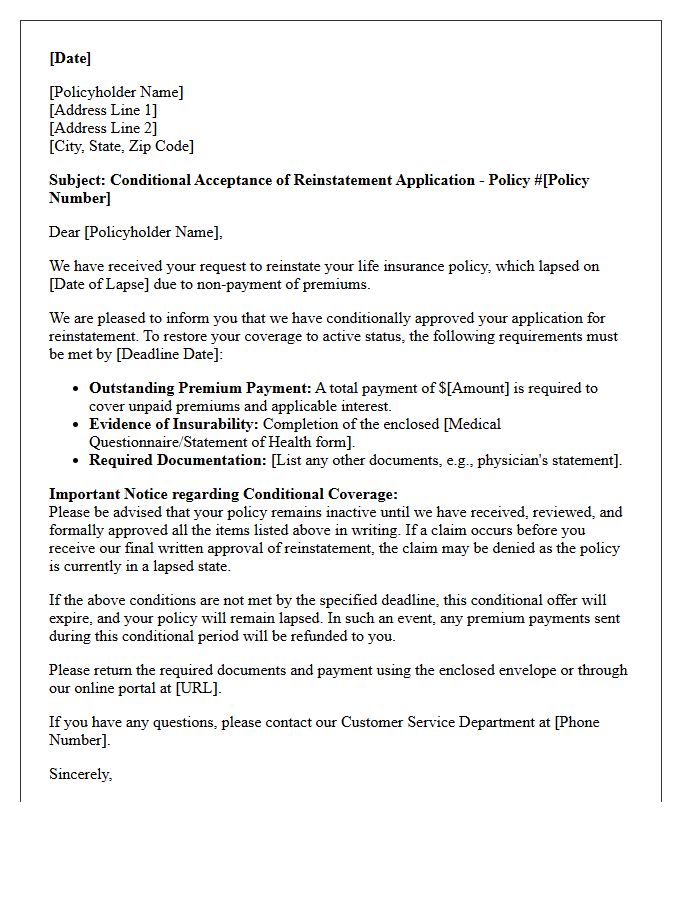

Conditional Life Insurance Policy Reinstatement Letter

A conditional life insurance policy reinstatement letter is a formal request to restore lapsed coverage. It typically requires the policyholder to provide evidence of insurability, such as a new medical questionnaire, to prove they still meet underwriting standards. Approval is not guaranteed; the insurer evaluates current health risks before reinstating the original terms. Additionally, the policyowner must pay all overdue premiums plus accumulated interest. This process is critical for maintaining long-term financial security without undergoing a completely new application process at an older age.

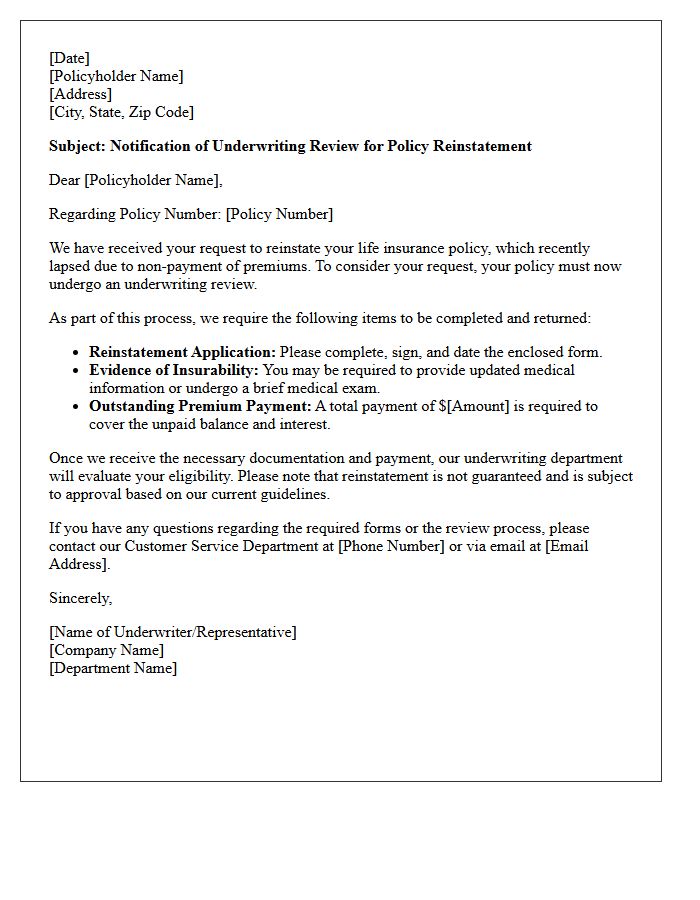

Underwriting Review Life Insurance Reinstatement Letter

An Underwriting Review is the critical process where insurers reassess your medical and financial eligibility after a policy lapses. When you receive a Life Insurance Reinstatement Letter, it signifies that the company requires updated health evidence to restore coverage. You must disclose any medical changes occurring since the original issue date. Approval is not guaranteed; the insurer evaluates current risk levels to decide if original terms still apply. Timely submission of the reinstatement application and payment of past-due premiums are essential to successfully reactivate your death benefit protection.

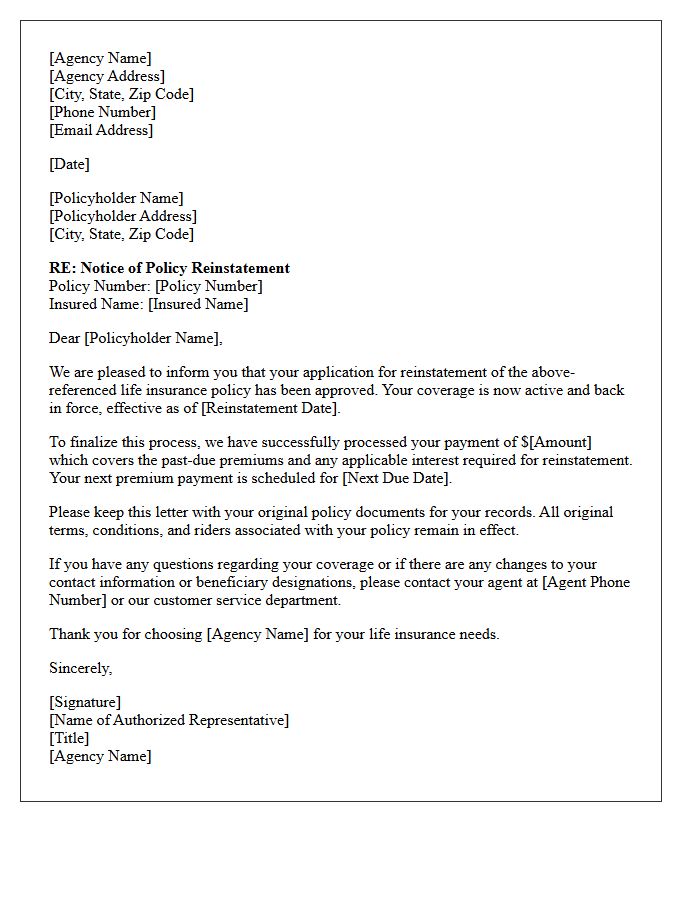

Agency Approved Life Insurance Policy Reinstatement Letter

An Agency Approved Life Insurance Policy Reinstatement Letter is a formal request to restore a lapsed policy after missed premium payments. It serves as a legal bridge to regain coverage without purchasing a new contract. The document typically requires a statement of good health and full payment of overdue premiums plus interest. Using an agency-approved template ensures all underwriting requirements are met, speeding up the reinstatement process. Timely submission is critical, as most insurers only allow this window for a limited period, typically three to five years from the lapse date.

Denial Of Life Insurance Policy Reinstatement Letter

Receiving a denial of life insurance policy reinstatement letter indicates the insurer has rejected your request to restore lapsed coverage. This typically occurs due to adverse underwriting findings, such as new health issues or high-risk lifestyle changes discovered during the application process. It is crucial to review the specific reason for denial cited in the document. You have the right to request a copy of the medical evidence used and can appeal the decision if the information is inaccurate or if you can provide additional evidence of insurability.

Client Request For Life Insurance Reinstatement Letter

A Life Insurance Reinstatement Letter is a formal request sent to an insurer to restore a policy that has lapsed due to non-payment. To increase approval chances, clearly state your policy number and the reason for the missed premiums. Most insurers require a Statement of Health to prove you are still insurable. Promptly providing the required back payments and interest is essential for reactivation. Always confirm the specific reinstatement period allowed by your provider to ensure your coverage remains valid and your beneficiaries stay protected.

Missing Information Life Insurance Policy Reinstatement Letter

When drafting a Missing Information Life Insurance Policy Reinstatement Letter, you must provide all outstanding details requested by the carrier to restore lapsed coverage. Common requirements include updated medical records, evidence of insurability, or payment records. Promptly submitting this missing data is crucial to maintain your original policy benefits and avoid higher premiums associated with new applications. Ensure your letter includes the policy number and clear explanations for previous omissions to expedite the underwriting review and successfully reactivate your financial protection.

Grace Period Notice Life Insurance Reinstatement Letter

A life insurance grace period notice alerts policyholders that a missed premium payment must be settled within typically 30 to 31 days to prevent coverage lapse. If the policy expires, you must submit a reinstatement letter to restore protection. This process often requires evidence of insurability, such as a health questionnaire, and payment of all overdue premiums plus interest. Act promptly during the grace period to avoid the risk of higher rates or potential denial of coverage based on changes in your medical history since the original policy issue date.

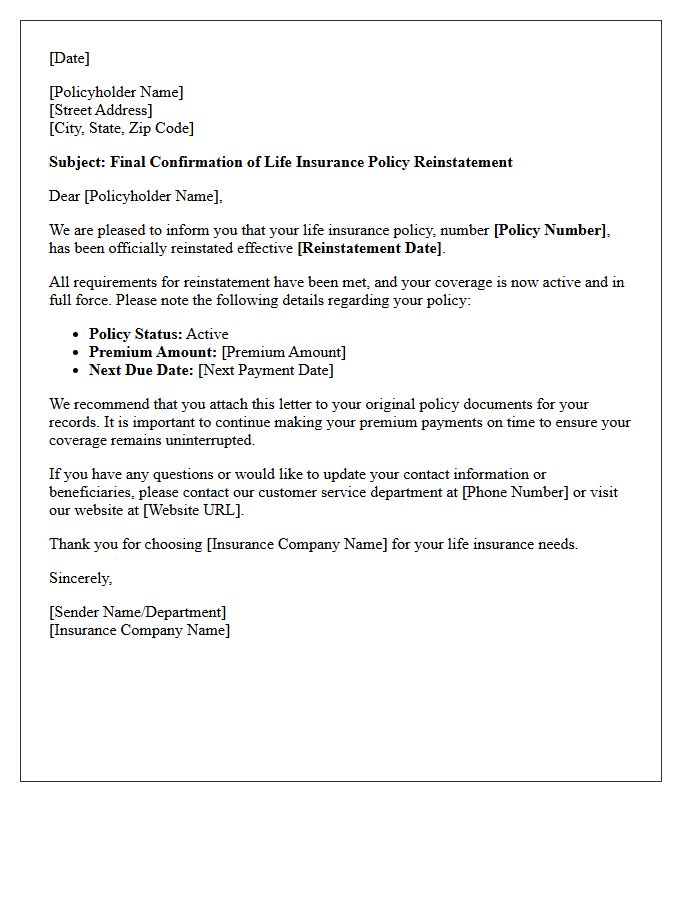

Final Confirmation Life Insurance Policy Reinstatement Letter

A final confirmation letter for life insurance reinstatement validates that your coverage is officially active after a lapse. This essential document confirms the insurer has approved your application, received overdue premiums, and restored all contract benefits. It serves as legal proof of protection, detailing your reinstatement date and any updated policy terms. Policyholders must verify these details immediately to ensure continuous financial security for beneficiaries. Keep this confirmation with your original policy records to prevent future coverage disputes or claims issues regarding the policy's standing.

What is a life insurance policy reinstatement letter?

A life insurance policy reinstatement letter is a formal written request sent by a policyholder to an insurance company asking to restore a lapsed policy. This letter typically accompanies a reinstatement application and payment for overdue premiums to put the coverage back in force.

When should I write a reinstatement letter for my life insurance?

You should write a reinstatement letter as soon as you realize your policy has lapsed due to non-payment, typically after the 31-day grace period has expired. Most insurers allow reinstatement within two to five years of the lapse date, provided you meet their specific underwriting requirements.

What key information must be included in a reinstatement request?

A formal reinstatement request should include your full name, policy number, the date the policy lapsed, and a clear statement of your intent to reactivate the coverage. You should also include a brief explanation for the missed payments and express your willingness to provide updated evidence of insurability if required.

Will I need a medical exam to reinstate my life insurance policy?

Whether a medical exam is required depends on your insurer's guidelines and how long the policy has been lapsed. If the policy has been inactive for more than a few months, the company usually requires "evidence of insurability," which may include a new health questionnaire or a standard medical examination.

Are there additional costs associated with reinstating a lapsed policy?

Yes, to reinstate a policy, you are generally required to pay all back-due premiums plus interest charged by the insurance company. While this may be expensive, it is often more cost-effective than buying a new policy, as you retain the original premium rates based on your younger age at the time of initial purchase.

Comments