A Post-Cancellation Reinstatement Notice is a formal document used to reactivate a policy or service after it has been terminated. This essential communication outlines the terms, outstanding requirements, and effective dates needed to restore coverage and maintain continuity. To simplify your process and ensure legal clarity, below are some ready to use template.

Image cover: Policy Reinstatement Letter Samples: Requesting Coverage Restoration After Cancellation

Letter Samples List

- Standard Policy Reinstatement Approval Letter

- Auto Insurance Post-Cancellation Reinstatement Letter

- Homeowners Coverage Reinstatement Notice Letter

- Commercial Liability Policy Reinstatement Letter

- Late Premium Payment Reinstatement Acceptance Letter

- Life Insurance Post-Cancellation Reinstatement Letter

- Notice of Policy Reinstatement Letter

- Workers Compensation Coverage Reinstatement Letter

- Reinstatement Letter with No Coverage Lapse

- Reinstatement Letter Acknowledging Coverage Gap

- Health Insurance Post-Cancellation Reinstatement Letter

- Agency Notice of Reinstated Insurance Letter

Standard Policy Reinstatement Approval Letter

A Standard Policy Reinstatement Approval Letter is a formal document confirming that your insurance coverage has been officially restored after a lapse. It validates that the insurer accepted your application and outstanding premiums, ensuring no permanent break in protection. This letter outlines the effective date of reactivation and any specific conditions maintained under the original terms. It serves as essential proof of active status, protecting your legal compliance and financial security. Always verify the document to ensure all policy details remain accurate following the reinstatement process.

Auto Insurance Post-Cancellation Reinstatement Letter

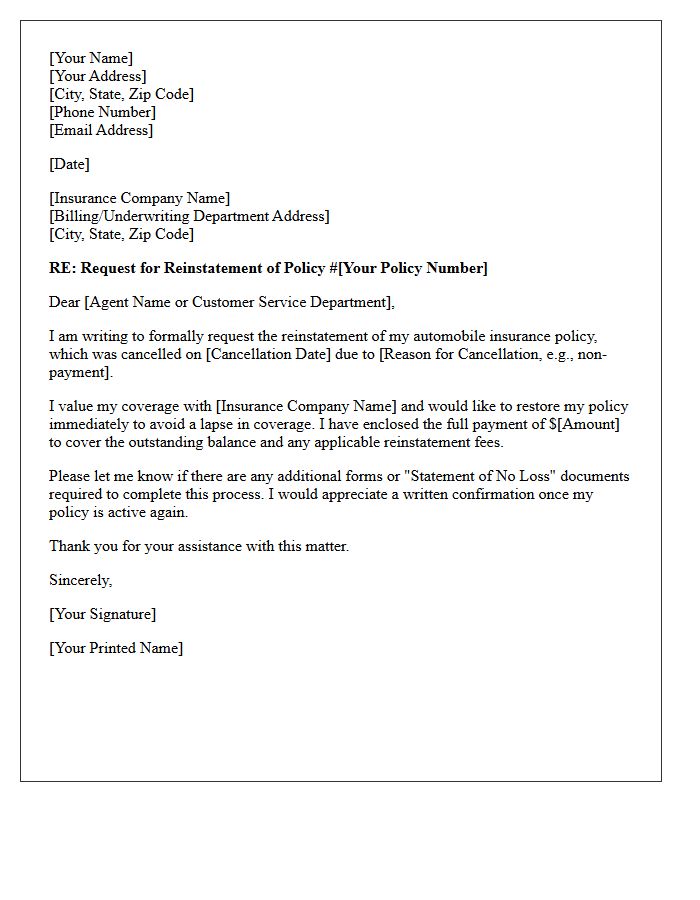

An Auto Insurance Post-Cancellation Reinstatement Letter is a formal request to restore a voided policy. It must address the reason for cancellation, such as a missed payment, and include a "Statement of No Loss" confirming no accidents occurred during the gap. Promptly submitting this letter, along with outstanding premiums, helps you avoid high-risk classifications and legal penalties for driving uninsured. Always follow up with your provider to confirm that continuous coverage has been officially reinstated to maintain your driving eligibility.

Homeowners Coverage Reinstatement Notice Letter

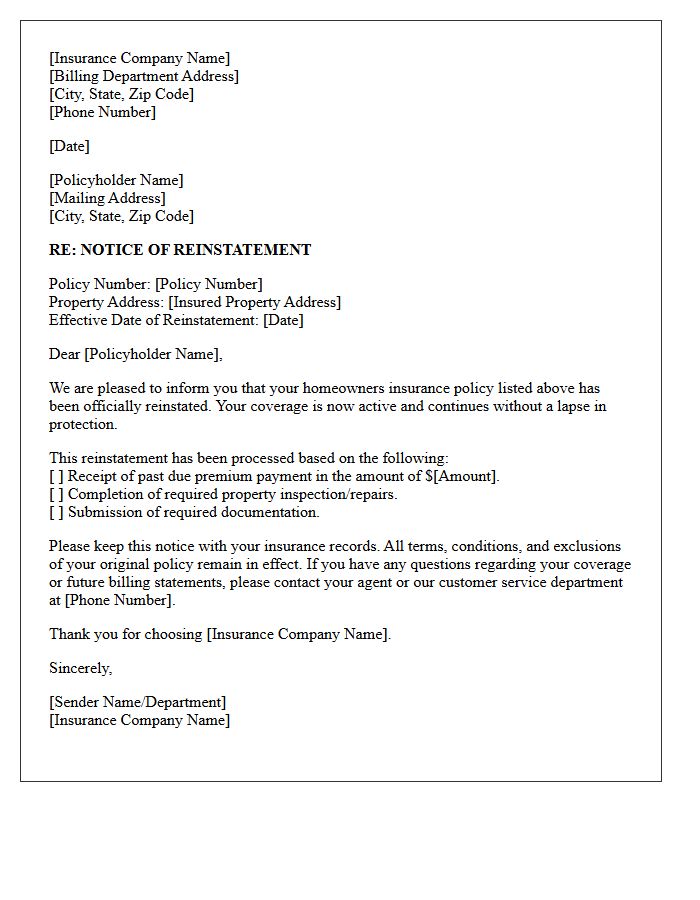

A Homeowners Coverage Reinstatement Notice Letter is a formal document confirming that a previously cancelled or lapsed insurance policy is active again. Receiving this notice means your property protection is restored, eliminating coverage gaps that could leave you financially vulnerable. It typically outlines the effective date of reinstatement and any premium payments required to maintain the policy. Homeowners should verify that all mortgage lenders are notified of this change to ensure compliance with loan requirements and to avoid the costly implementation of force-placed insurance.

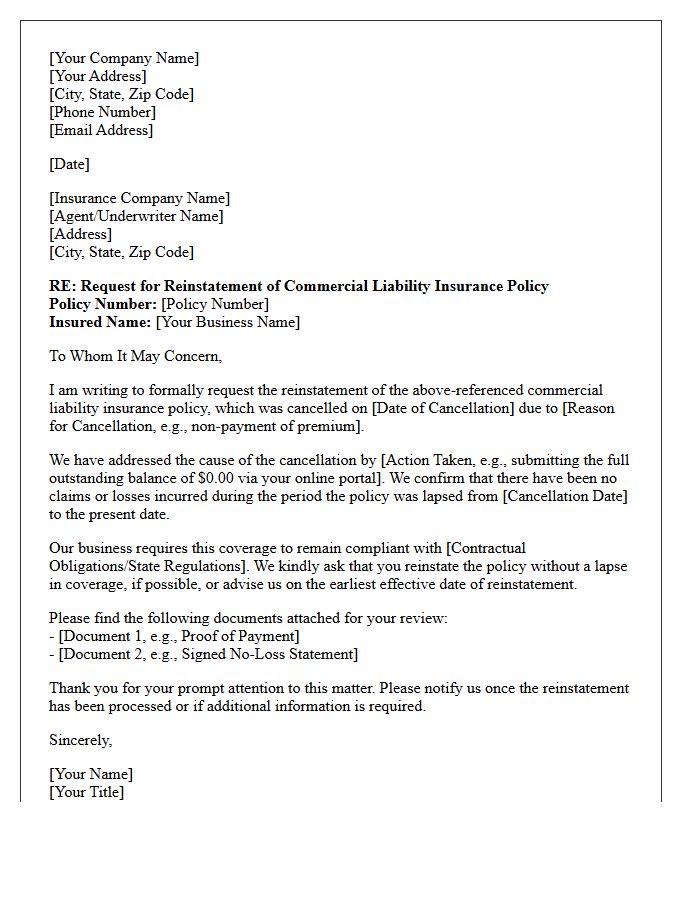

Commercial Liability Policy Reinstatement Letter

A Commercial Liability Policy Reinstatement Letter is a formal document confirming that a previously cancelled or lapsed insurance policy is active again. It serves as legal proof of restored coverage, ensuring your business remains protected against third-party claims. Business owners must verify the reinstatement date and any specific conditions or premiums paid to avoid gaps in protection. Keeping this letter on file is essential for maintaining compliance with contracts and demonstrating continuous financial responsibility to clients and regulatory bodies.

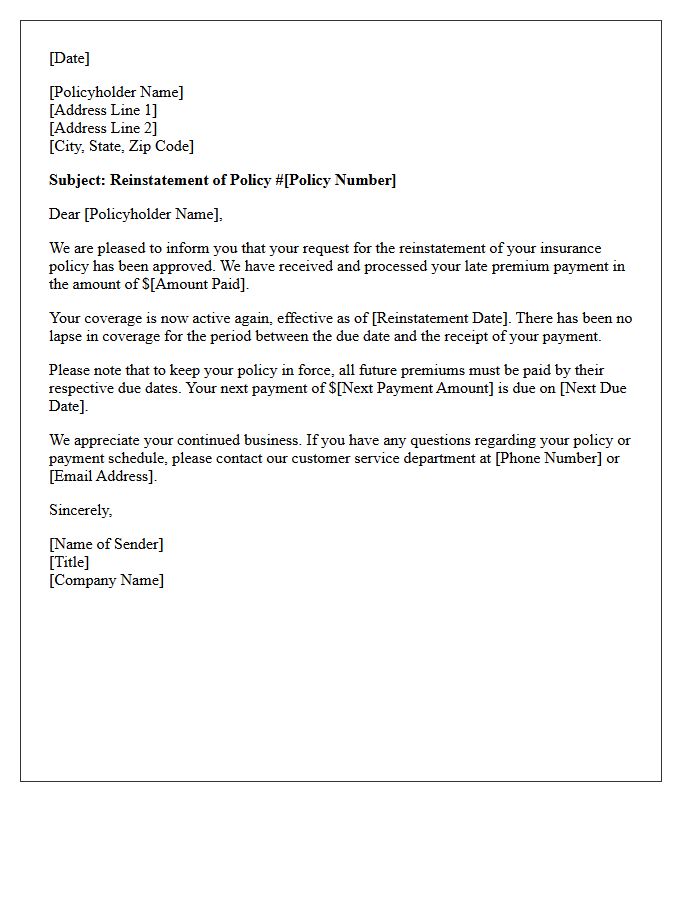

Late Premium Payment Reinstatement Acceptance Letter

A Late Premium Payment Reinstatement Acceptance Letter is a formal document issued by an insurance company confirming that a lapsed policy has been restored. It signifies that the insurer has accepted overdue payments and agrees to maintain continuous coverage despite a temporary break. Policyholders must review this letter to verify the reinstatement date and any specific conditions imposed during the gap period. Timely acknowledgement ensures your financial protection remains active, preventing a permanent loss of benefits and maintaining the original terms of your insurance contract.

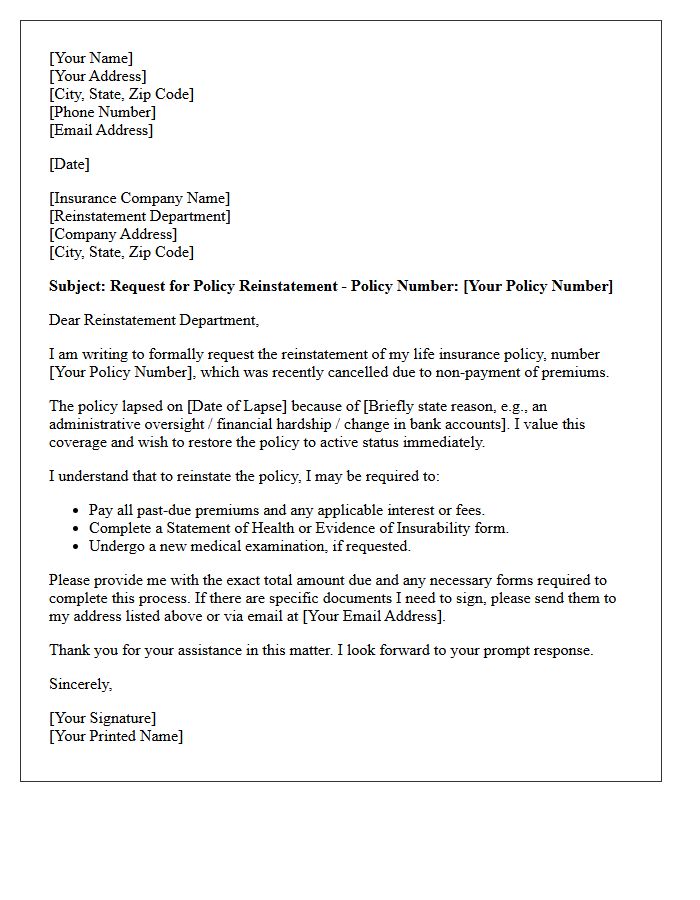

Life Insurance Post-Cancellation Reinstatement Letter

A life insurance post-cancellation reinstatement letter is a formal request to restore a lapsed policy. To regain coverage, policyholders must typically submit this written application along with overdue premiums and interest. The reinstatement process often requires a new statement of health or medical evidence to prove continued insurability. Acting quickly is essential, as most insurers impose a strict time limit, often three to five years, for restoration. Successfully reinstating a policy allows you to maintain original premium rates and benefits without undergoing a full new underwriting cycle.

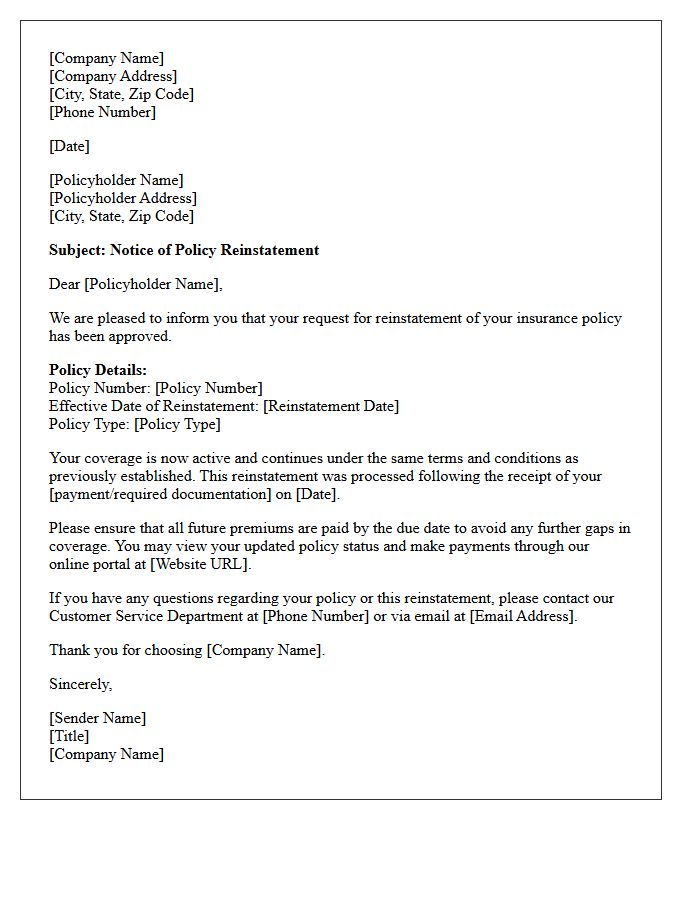

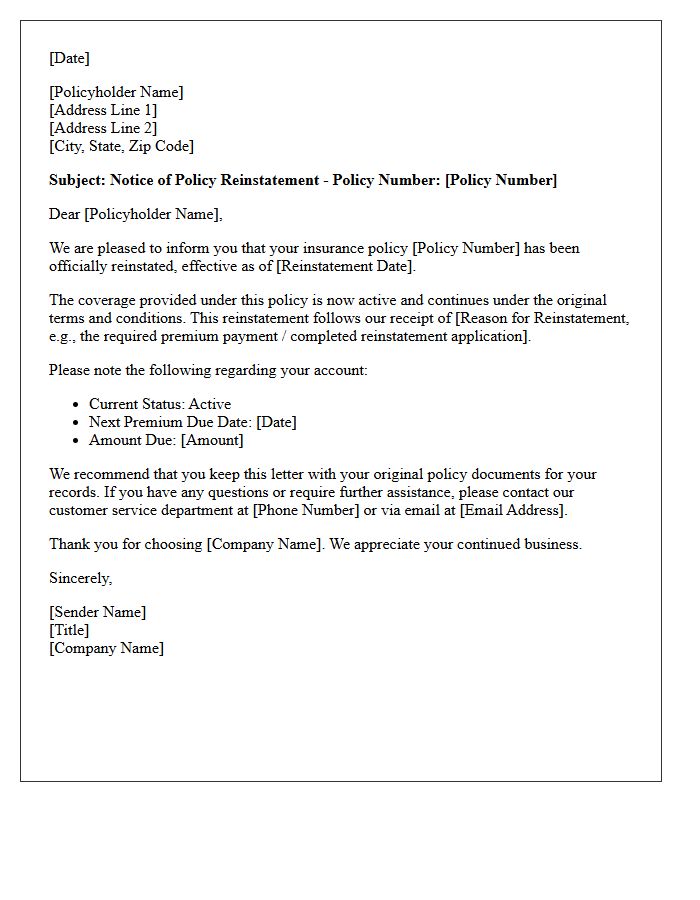

Notice of Policy Reinstatement Letter

A Notice of Policy Reinstatement Letter confirms that your insurance coverage is active again after a lapse. It is the formal response to a reinstatement application and payment of overdue premiums. This document is vital because it restores your financial protection and provides proof of continuous coverage to third parties. Always verify the effective date listed in the letter to ensure there are no gaps in your protection. Keep this record safely as it serves as legal evidence that your policy terms and benefits are fully restored.

Workers Compensation Coverage Reinstatement Letter

A Workers Compensation Coverage Reinstatement Letter is a formal notice confirming that a previously cancelled or lapsed insurance policy is active again. This document is essential for maintaining legal compliance and protecting employees from workplace injuries. To ensure continuous protection, employers must resolve outstanding issues, such as unpaid premiums or missing audits, which triggered the initial termination. Always verify the reinstatement date to avoid coverage gaps and potential regulatory fines. Keeping this letter on file serves as vital proof of insurance for contracts, audits, and state regulatory requirements.

Reinstatement Letter with No Coverage Lapse

A reinstatement letter with no coverage lapse is a formal request to restore an insurance policy as if it never expired. The reinstatement process ensures that protection remains continuous, protecting you from potential out-of-pocket liabilities for incidents occurring during the processing period. To qualify, policyholders must typically pay all outstanding premiums and submit a signed Statement of No Loss, confirming no claims occurred while the policy was technically inactive. This maintaining of uninterrupted coverage is essential for avoiding future premium hikes and satisfying legal or contractual requirements.

Reinstatement Letter Acknowledging Coverage Gap

A reinstatement letter acknowledging a coverage gap is a formal document used to restore an inactive insurance policy. It is crucial to understand that this letter confirms protection was not active during the lapse period. By signing, the policyholder accepts full financial liability for any incidents occurring while the policy was void. This document typically requires a statement of no loss to verify no claims are pending. Reinstating coverage helps maintain continuous history, but the coverage gap remains a permanent part of your insurance record, potentially affecting future premium rates.

Health Insurance Post-Cancellation Reinstatement Letter

A reinstatement letter is a formal request to restore coverage after a policy cancels due to non-payment. You must clearly state your policy number and the specific reason for the lapse, such as financial hardship or administrative error. Most insurers require this letter alongside the full outstanding premium payment. Timeliness is critical, as many providers only offer a limited grace period for reinstatement. Submitting a compelling, honest explanation increases your chances of avoiding a total loss of benefits and maintaining continuous medical protection without new waiting periods.

Agency Notice of Reinstated Insurance Letter

An Agency Notice of Reinstated Insurance Letter is a critical document confirming that a previously cancelled or expired insurance policy is now active again. Receiving this notice means your coverage is restored, protecting you from financial liability and potential legal penalties. It typically details the reinstatement date and any required premium payments made to resolve the lapse. Always verify that the information matches your records to ensure continuous legal compliance and to maintain uninterrupted protection against unforeseen risks or claims.

What is a Post-Cancellation Reinstatement Notice?

A Post-Cancellation Reinstatement Notice is a formal document issued by an insurance provider or service entity confirming that a previously terminated policy or contract has been restored to active status without a lapse in coverage.

How can I request a reinstatement after my policy has been cancelled?

To request reinstatement, you must typically contact your provider immediately, settle any outstanding premium balances, and provide a statement of no loss to certify that no claims occurred during the period the policy was inactive.

Is there a deadline for filing a Post-Cancellation Reinstatement Notice?

Most providers have a specific "reinstatement window," usually ranging from 10 to 30 days following the cancellation date. If this timeframe passes, you may be required to apply for a entirely new policy at current market rates.

Will my coverage remain the same after receiving a reinstatement notice?

In most cases, a successful reinstatement restores your original policy terms, limits, and deductibles as they existed prior to the cancellation, provided all back-payments and administrative fees are satisfied.

What are the common reasons a reinstatement request might be denied?

Reinstatement may be denied if there is a history of frequent payment lapses, if a claim occurred during the period of cancellation, or if the request is submitted outside of the provider's allowed grace period.

Comments