Receiving a Reinstatement Pending Underwriting Review letter means your insurance provider is evaluating your eligibility to restore a lapsed policy. This formal notice indicates that coverage is not yet active, as underwriters must first assess current risks and payment history. Understanding this status is crucial for maintaining protection. To help you respond effectively, below are some ready to use template.

Image cover: Reinstatement Pending Underwriting Review: Sample Letters and Professional Templates

Letter Samples List

- Acknowledgment Of Reinstatement Pending Underwriting Review Letter

- Personal Auto Policy Reinstatement Pending Underwriting Review Letter

- Homeowners Insurance Reinstatement Pending Underwriting Review Letter

- Commercial Liability Reinstatement Pending Underwriting Review Letter

- Workers Compensation Reinstatement Pending Underwriting Review Letter

- Term Life Policy Reinstatement Pending Underwriting Review Letter

- Payment Received And Reinstatement Pending Underwriting Review Letter

- Statement Of No Loss Reinstatement Pending Underwriting Review Letter

- Additional Documentation Required For Reinstatement Pending Underwriting Review Letter

- Property Inspection Subject Reinstatement Pending Underwriting Review Letter

- Post Grace Period Reinstatement Pending Underwriting Review Letter

- Final Status Reinstatement Pending Underwriting Review Letter

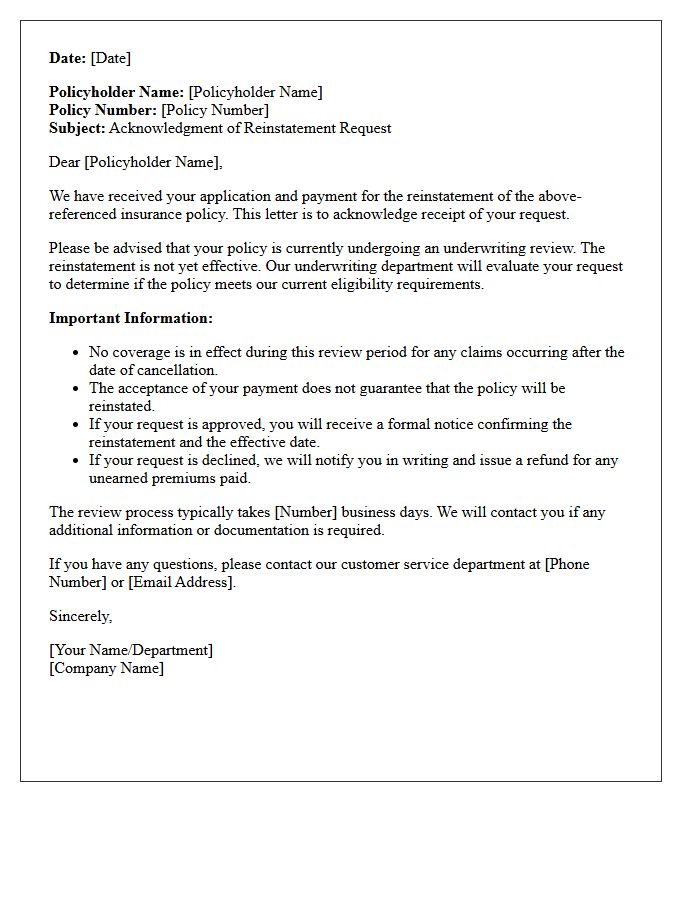

Acknowledgment Of Reinstatement Pending Underwriting Review Letter

An Acknowledgment of Reinstatement Pending Underwriting Review Letter confirms that an insurance provider has received your application and payment to restart a lapsed policy. Receiving this document does not guarantee coverage immediately. Instead, it signifies that the company is currently evaluating your risk profile to determine eligibility. During this underwriting period, your policy status remains uncertain until formal approval is granted. It is crucial to monitor communications for any additional documentation requests or a final decision regarding your insurance protection and effective date.

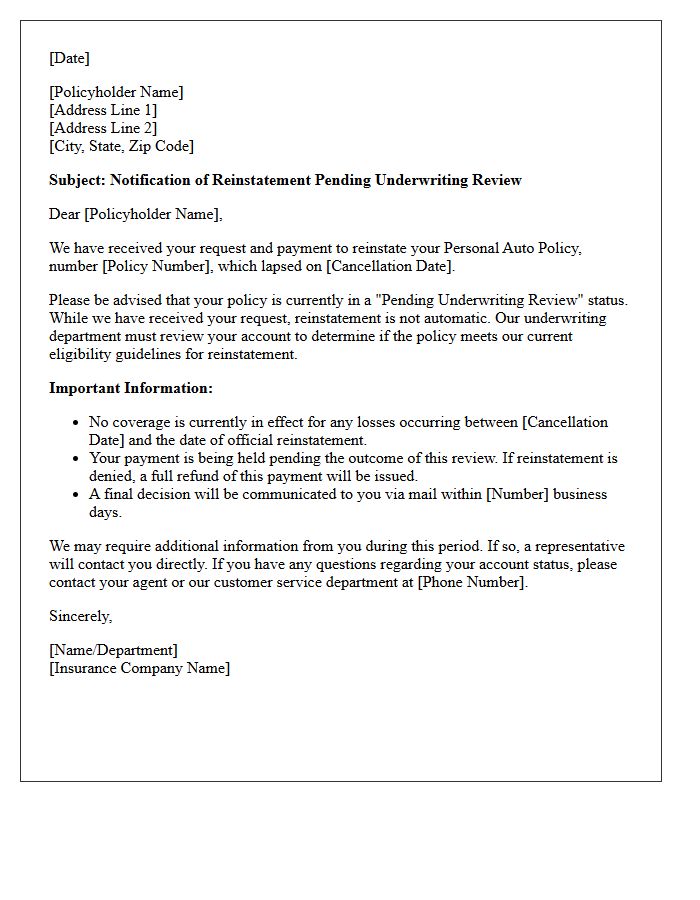

Personal Auto Policy Reinstatement Pending Underwriting Review Letter

A Personal Auto Policy Reinstatement Pending Underwriting Review Letter indicates that your request to restore a lapsed policy is not immediate. The insurance company must reevaluate your risk profile before providing coverage. During this period, you typically have no active insurance coverage, meaning you are driving uninsured. Underwriters check for recent accidents, payment history, or changes in eligibility. Always confirm the effective date of protection in writing, as receipt of this letter does not guarantee that your policy will be reinstated or that claims will be paid.

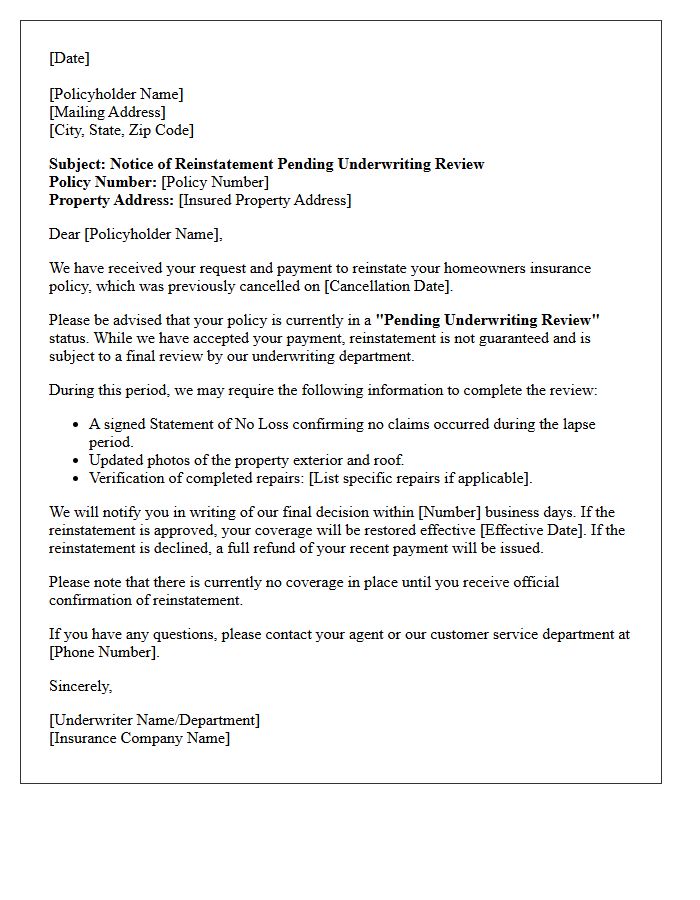

Homeowners Insurance Reinstatement Pending Underwriting Review Letter

A homeowners insurance reinstatement pending underwriting review letter indicates your coverage is temporarily suspended while the insurer reassesses your risk profile. This typically occurs after a payment lapse or property inspection. During this underwriting period, you may lack active protection against damages or liability claims. To resolve this, promptly submit any requested documentation or repairs mentioned in the notice. Reinstatement is not guaranteed until the carrier completes its evaluation and issues a formal confirmation. Always contact your agent immediately to clarify your current coverage status and prevent a permanent policy cancellation.

Commercial Liability Reinstatement Pending Underwriting Review Letter

A Commercial Liability Reinstatement Pending Underwriting Review Letter indicates that your coverage has lapsed, typically due to non-payment or high risk. Receipt of this notice means your request to restore the policy is currently undergoing evaluation. During this phase, you have no active protection. The underwriter must reassess your eligibility and loss history before approving the reinstatement. It is vital to provide any requested documentation immediately to avoid a permanent cancellation. Coverage is only official once you receive a formal confirmation of reinstatement from the insurer.

Workers Compensation Reinstatement Pending Underwriting Review Letter

A Workers Compensation Reinstatement Pending Underwriting Review letter indicates that your coverage has lapsed, but a request to restart the policy is currently being evaluated. Receiving this notice means reinstatement is not guaranteed. The insurance carrier's underwriters must assess your account's risk and payment history before approving coverage. During this pending status, you may have a gap in protection, leaving your business vulnerable to claims and legal penalties. It is essential to provide requested documentation immediately and confirm with your agent when the policy is officially active again.

Term Life Policy Reinstatement Pending Underwriting Review Letter

A Term Life Policy Reinstatement Pending Underwriting Review Letter notifies you that your application to restore a lapsed policy is currently being evaluated. Since your coverage is not yet active, the insurance company must assess your current health status and insurability. This process often requires updated medical questionnaires or exams. You must continue to meet underwriting guidelines to regain protection. Until you receive a formal approval notice and pay outstanding premiums, you remain without coverage. Always respond promptly to information requests to avoid a final denial of your reinstatement request.

Payment Received And Reinstatement Pending Underwriting Review Letter

A Payment Received And Reinstatement Pending Underwriting Review Letter indicates your insurance premium was paid after a policy lapse, but coverage is not yet active. Receipt of funds does not guarantee reinstatement. Instead, the insurance company must manually evaluate your current risk profile. During this underwriting review, the insurer decides whether to restore your policy or issue a refund. It is crucial to understand that a coverage gap may still exist until you receive official confirmation that the policy is fully reinstated and active.

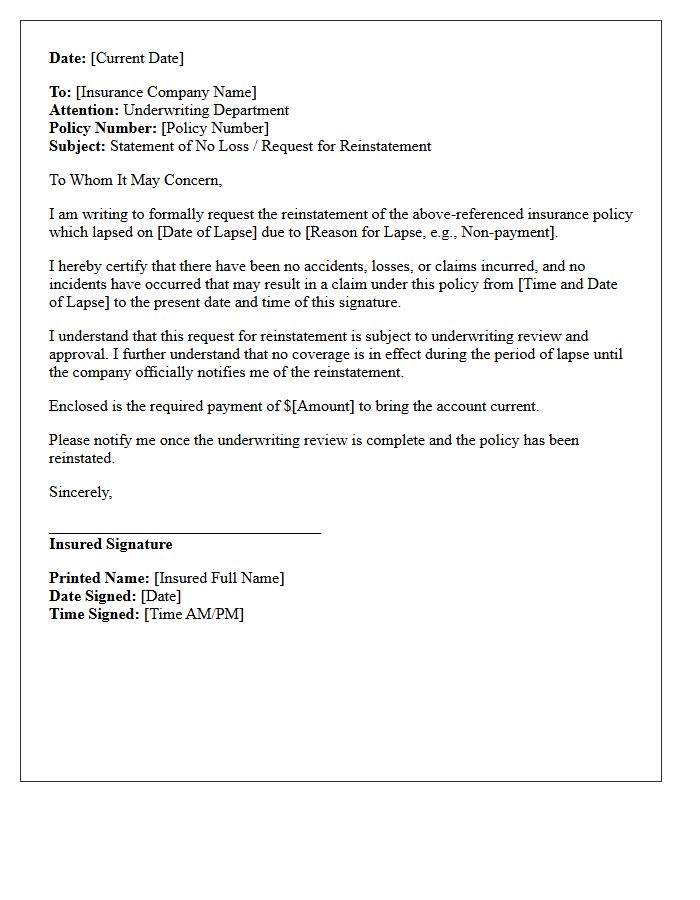

Statement Of No Loss Reinstatement Pending Underwriting Review Letter

A Statement of No Loss is a critical document required when an insurance policy has lapsed. By signing it, you confirm that no claims or losses occurred during the coverage gap. The term Reinstatement Pending Underwriting Review means your request to restart the policy is not yet guaranteed. The insurance company must evaluate your eligibility and risk profile before officially restoring coverage. Providing false information on this letter is considered insurance fraud and will void your policy, leaving you personally liable for any undisclosed incidents during the inactive period.

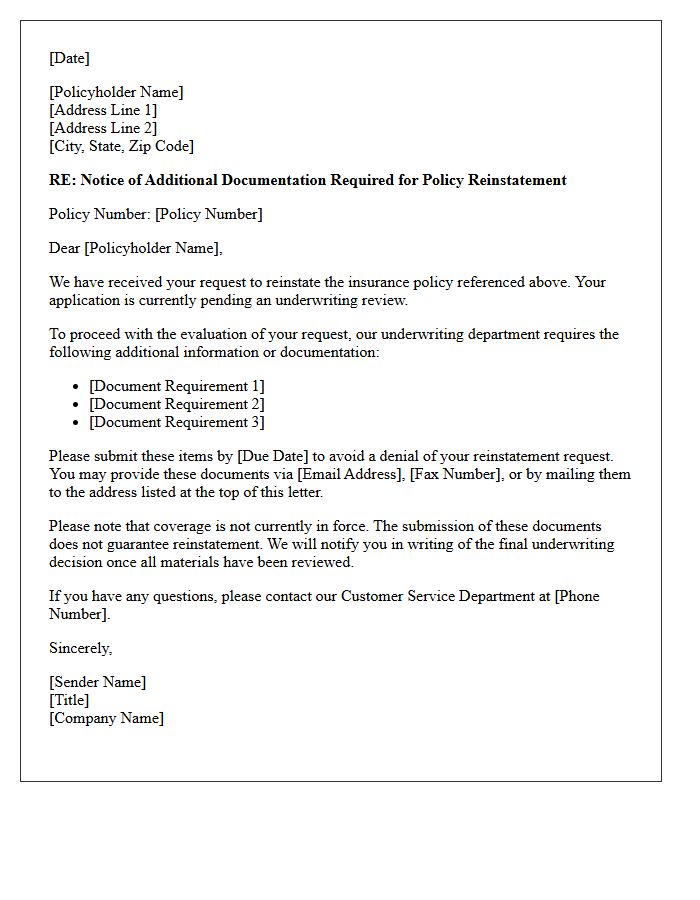

Additional Documentation Required For Reinstatement Pending Underwriting Review Letter

The Additional Documentation Required For Reinstatement Pending Underwriting Review Letter indicates that your insurance policy is not yet active. To avoid a permanent lapse in coverage, you must submit specific evidence, such as proof of repairs or updated medical records, as requested by the insurer. Underwriters use these documents to evaluate risk before deciding to restore your policy status. Failure to provide this information within the specified timeframe typically results in a formal denial of reinstatement, leaving you without protection and potentially facing higher future premiums.

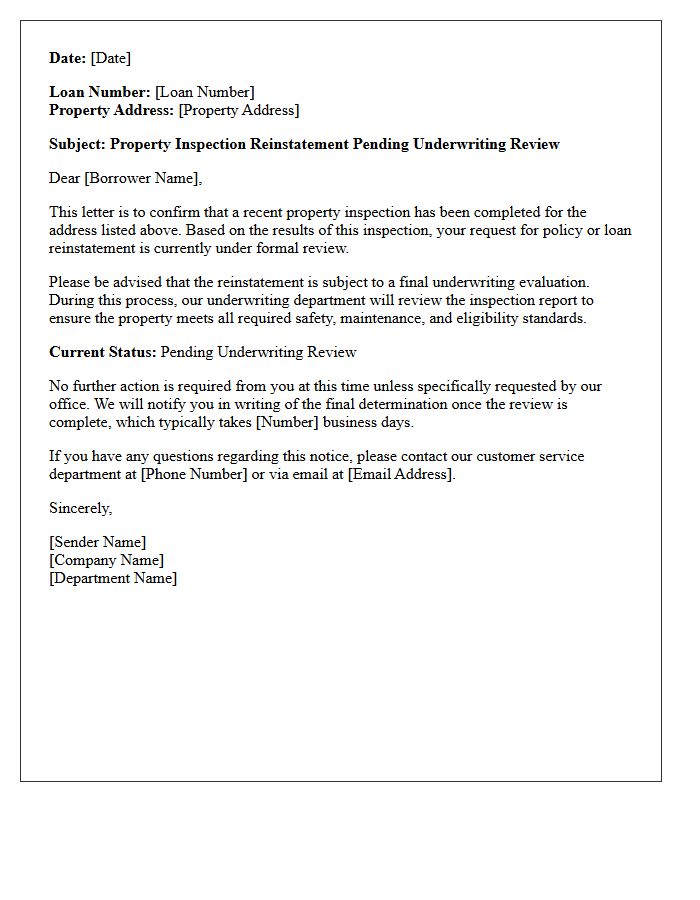

Property Inspection Subject Reinstatement Pending Underwriting Review Letter

A Property Inspection Subject Reinstatement Pending Underwriting Review Letter notifies homeowners that an insurance policy reinstatement is not yet finalized. It indicates that while a property inspection has been completed, the coverage remains conditional. The underwriting department must manually review the inspection report to verify the home's condition and risk eligibility. Homeowners should promptly address any identified hazards or maintenance issues mentioned in the letter to avoid a final denial. Coverage is only fully restored once the insurer confirms the risks align with their established safety guidelines and policy standards.

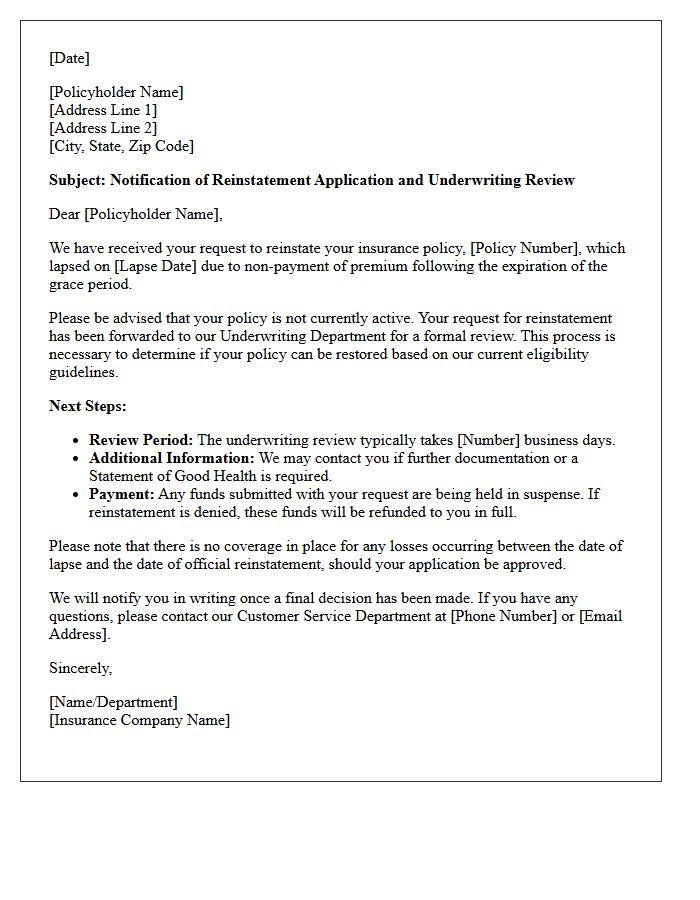

Post Grace Period Reinstatement Pending Underwriting Review Letter

A Post Grace Period Reinstatement Pending Underwriting Review Letter informs policyholders that their insurance coverage has lapsed due to non-payment. To restore protection, you must submit a reinstatement application and any overdue premiums. Receiving this letter means your coverage is not active; instead, it is undergoing evaluation by an underwriter to determine eligibility based on current risk factors. During this underwriting review, the insurer decides whether to approve or decline the request. Coverage is not guaranteed until you receive a formal confirmation of active status from the insurance company.

Final Status Reinstatement Pending Underwriting Review Letter

A Final Status Reinstatement Pending Underwriting Review Letter indicates your insurance policy is in a conditional state. It confirms that the company received your request and payment, but coverage is not yet active. Underwriters must perform a comprehensive risk assessment to determine if you qualify for reinstatement. During this critical underwriting review period, you may experience a gap in coverage. It is essential to provide any requested documentation promptly to avoid a permanent cancellation and ensure your protection is officially restored by the carrier.

What does a "Reinstatement Pending Underwriting Review" letter mean?

This letter indicates that your request to reactivate a lapsed insurance policy is currently being evaluated by the underwriting department. The insurer is assessing your current risk profile, such as health changes or property condition, before deciding whether to restore coverage.

Why did I receive a reinstatement pending underwriting review notice?

You received this notice because your insurance policy lapsed due to non-payment or expiration, and you have submitted a request to restart it. Because the policy was not active for a period, the company must re-verify that you still meet their eligibility and risk requirements.

How long does the underwriting review process take for policy reinstatement?

The review process typically takes between 5 to 10 business days, though it can vary depending on the complexity of the risk. During this time, the underwriter may request additional documentation, such as medical records or a statement of good health, to finalize their decision.

Am I covered while my reinstatement is pending underwriting review?

No, you generally do not have insurance coverage while your reinstatement is pending review. Coverage is only restored once the underwriting department formally approves the application and you receive a confirmation of reinstatement. Any claims occurring during this "gap" period are typically not covered.

What are the possible outcomes of an underwriting review for reinstatement?

The underwriting department will issue one of three decisions: approval, where your policy is restored under original or new terms; a request for more information; or a denial. If denied, the insurer will provide a reason, and any unearned premiums or reinstatement fees paid during the application process are usually refunded.

Comments