A Statement of Good Health is a critical document required by insurance companies to prove your insurability when reviving a lapsed policy. This formal letter confirms you have not suffered serious illnesses or injuries since the original coverage ended. Understanding the correct format ensures a smooth reinstatement process. To help you get started, below are some ready to use template.

Image cover: Professional Statement of Good Health: Reinstatement Letter Samples and Templates

Letter Samples List

- Standard Statement of Good Health for Policy Reinstatement Letter

- Life Insurance Statement of Good Health Reinstatement Letter

- Medical Declaration and Good Health Reinstatement Letter

- Term Life Policy Good Health Declaration Reinstatement Letter

- Health Insurance Lapsed Policy Good Health Reinstatement Letter

- Post-Grace Period Statement of Good Health Reinstatement Letter

- Whole Life Insurance Statement of Good Health Reinstatement Letter

- Agent Attestation and Statement of Good Health Reinstatement Letter

- Client Declaration of Good Health for Reinstatement Letter

- Short-Form Statement of Good Health Reinstatement Letter

- Disability Income Statement of Good Health Reinstatement Letter

- General Agency Statement of Good Health Reinstatement Letter

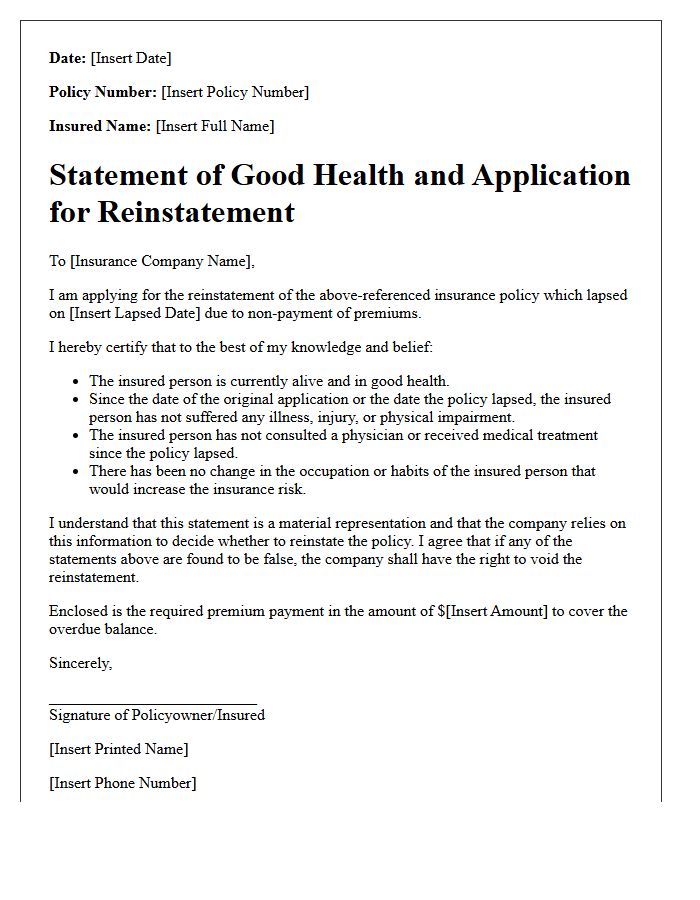

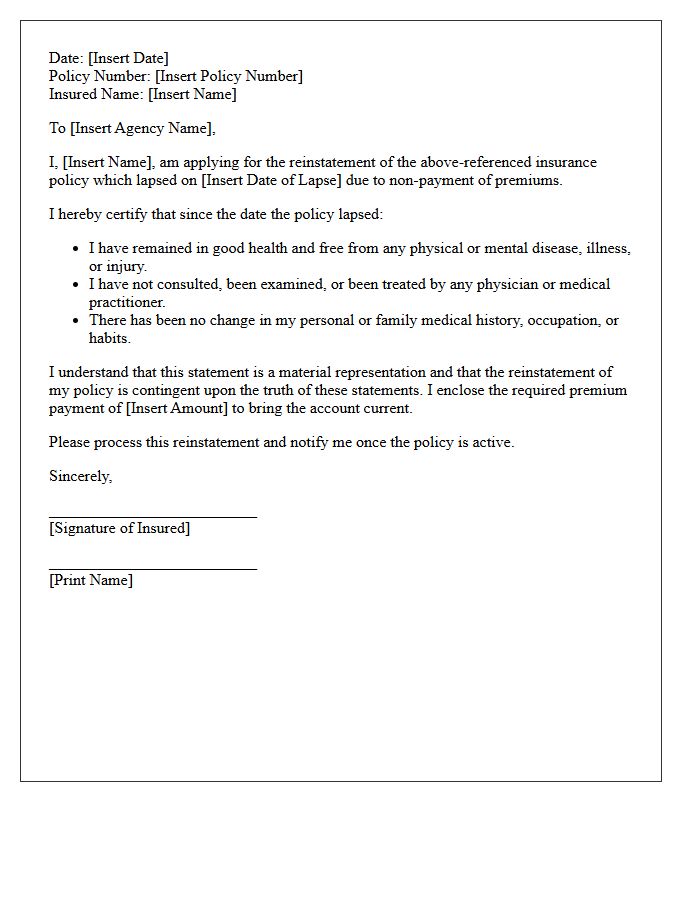

Standard Statement of Good Health for Policy Reinstatement Letter

A Standard Statement of Good Health is a mandatory document used to reinstate a lapsed insurance policy. By signing this letter, the policyholder confirms that their medical condition has not significantly changed since the original coverage date. This statement provides the insurer with evidence of insurability, ensuring no new high-risk illnesses have developed. Providing accurate information is critical, as any material misrepresentation discovered during the underwriting review or a future claim process can lead to a denial of benefits or permanent policy cancellation.

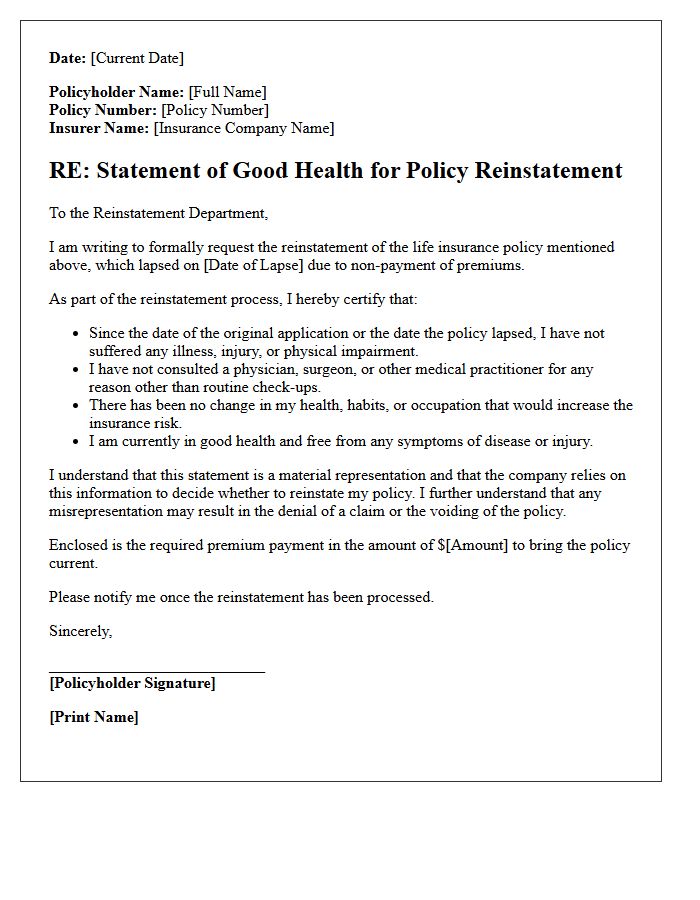

Life Insurance Statement of Good Health Reinstatement Letter

A Statement of Good Health is a mandatory legal document required during the reinstatement process of a lapsed life insurance policy. It serves as a formal declaration that your medical status has not declined since the original coverage ended. Insurers use this letter to reassess underwriting risk before reactivating benefits. Providing accurate information is critical, as any material misrepresentation discovered later could lead to a claim denial. Always submit this form promptly alongside overdue premiums to ensure your financial protection is successfully restored without undergoing a full new medical exam.

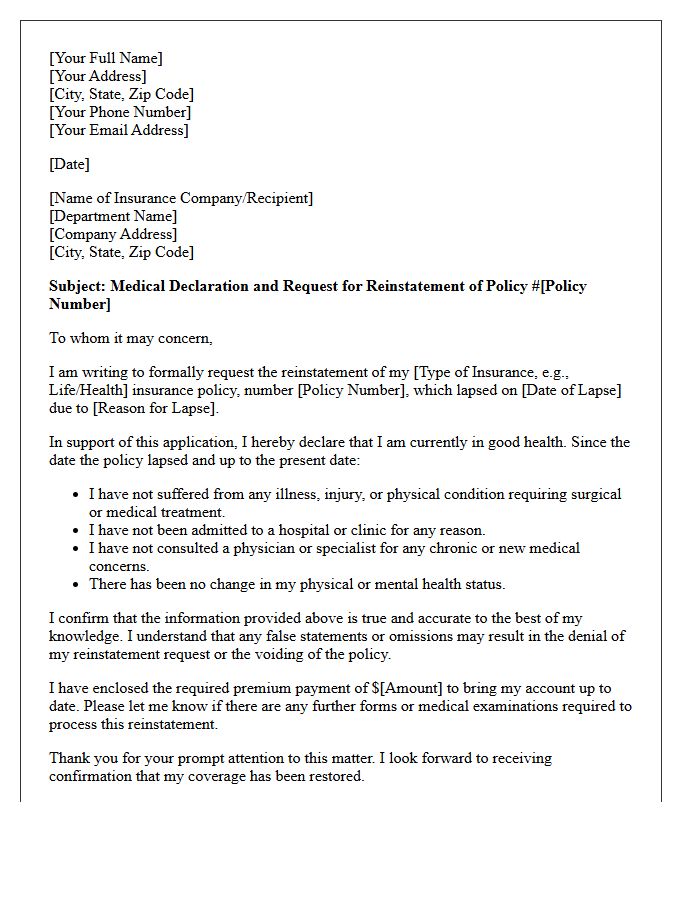

Medical Declaration and Good Health Reinstatement Letter

A Medical Declaration and Good Health Reinstatement Letter are essential documents for restoring a lapsed insurance policy. Policyholders must formally attest to their current physical condition, disclosing any new illnesses or injuries since the original coverage began. Accuracy is critical, as any misrepresentation can lead to claim denials or policy voidance. This legal statement confirms that the insured remains an acceptable risk for the provider. Ensuring a transparent health disclosure facilitates a smooth reinstatement process, protecting your financial security and maintaining continuous insurance protection without requiring a completely new application.

Term Life Policy Good Health Declaration Reinstatement Letter

When your coverage lapses due to unpaid premiums, a reinstatement requires a formal "Good Health Declaration." This legal document confirms you have maintained continuous medical stability since the original policy issue date. Insurers use this letter to reassess risk before restoring your term life insurance benefits. It is vital to provide full disclosure regarding new diagnoses or lifestyle changes, as inaccuracies can lead to future claim denials. Timely submission of this declaration, alongside outstanding payments, ensures your beneficiaries remain protected without requiring a completely new underwriting process.

Health Insurance Lapsed Policy Good Health Reinstatement Letter

When a health insurance policy lapses due to missed premiums, insurers may offer a pathway for reinstatement. A Good Health Statement is a formal letter required to confirm the applicant has remained in good physical condition during the coverage gap. This document ensures no new medical risks emerged while inactive. It must be signed and submitted promptly to restore benefits without a waiting period. Providing accurate details in this reinstatement letter is critical to avoid claim denials or future policy cancellations based on non-disclosure of health changes.

Post-Grace Period Statement of Good Health Reinstatement Letter

A Post-Grace Period Statement of Good Health Reinstatement Letter is a formal document required to restore a lapsed insurance policy. Once the grace period ends, coverage terminates for non-payment. To reactivate the plan, the policyholder must sign this attestation confirming they remain in good health and have not suffered new illnesses or injuries since the lapse. This process typically involves paying all overdue premiums and is subject to insurer approval to ensure the risk profile has not changed significantly before full protection is reinstated.

Whole Life Insurance Statement of Good Health Reinstatement Letter

A Statement of Good Health is a mandatory document required when reviving a lapsed whole life insurance policy. To initiate reinstatement, the policyholder must declare that their physical condition remains unchanged since the original issue date. This letter protects the insurer from new risks developed during the coverage gap. Accurately completing this form is crucial, as any undisclosed medical changes can lead to a denial of benefits. Once approved, and all back-premiums plus interest are paid, your lifelong death benefit and cash value accumulation are fully restored.

Agent Attestation and Statement of Good Health Reinstatement Letter

An Agent Attestation and Statement of Good Health are critical documents required to reinstate a lapsed life insurance policy. The agent confirms the client's current status, while the policyholder signs a Statement of Good Health to verify no significant medical changes occurred since the coverage ended. These forms ensure the underwriting risk remains acceptable to the insurer. Timely submission is essential to restore protection without undergoing a full new application process, maintaining the original policy terms and guaranteed benefits effectively.

Client Declaration of Good Health for Reinstatement Letter

A Client Declaration of Good Health is a mandatory document required to reinstate a lapsed insurance policy. It serves as a formal statement confirming that the insured person's medical status has not declined since the original coverage ended. Insurers use this attestation to assess current risk before restoring benefits. Accurate disclosure is vital, as any misrepresentation found during the underwriting process can lead to future claim denials or permanent policy termination. Always ensure all health changes are truthfully documented to maintain continuous and valid protection.

Short-Form Statement of Good Health Reinstatement Letter

A short-form statement of good health is a reinstatement letter used to restore a lapsed life insurance policy. This document requires the policyholder to confirm they have not experienced major medical changes since the original coverage ended. By signing this attestation, you verify your current physical condition remains stable to avoid full medical underwriting again. It is a simplified process, but accuracy is vital, as any misrepresentation of your health status can lead to a future claim denial or policy cancellation by the insurer.

Disability Income Statement of Good Health Reinstatement Letter

A Disability Income Statement of Good Health is a mandatory legal document required when reinstating a lapsed insurance policy. It serves as a formal declaration that your medical condition has not changed since the original coverage ended. Insurers use this to assess underwriting risk before restoring benefits. You must disclose any new illnesses or injuries accurately to avoid claim denials. Submitting this reinstatement letter promptly ensures continuous financial protection against potential loss of income due to future disability.

General Agency Statement of Good Health Reinstatement Letter

A General Agency Statement of Good Health Reinstatement Letter is a critical document required to reactivate a lapsed insurance policy. It serves as a formal declaration by the policyholder confirming that their medical status has not declined since the original coverage ended. The primary goal is to verify insurability without requiring a full new exam. To ensure successful processing, the applicant must provide truthful updates regarding recent illnesses or surgeries. Timely submission of this signed statement, along with outstanding premiums, is essential for maintaining continuous financial protection and original policy benefits.

What is a Statement of Good Health for insurance reinstatement?

A Statement of Good Health is a formal declaration signed by a policyholder confirming that they have not experienced significant changes in their medical condition, injuries, or illnesses since their insurance policy lapsed. It is a mandatory requirement for the reinstatement process to prove the individual remains insurable under the original terms.

When is a Statement of Good Health letter required for reinstatement?

This letter is typically required when a life, health, or disability insurance policy has lapsed due to non-payment of premiums beyond the grace period. Insurance companies use this document to reassess risk before agreeing to reactivate the coverage without requiring a full new medical examination.

What key information must be included in a reinstatement health statement?

The document must include the policy number, the full name of the insured, and a specific confirmation that no new symptoms, diagnoses, or hospitalizations have occurred since the lapse date. It must also be signed and dated by the policyholder to verify that all provided medical information is true and accurate.

Can a reinstatement request be denied based on the Statement of Good Health?

Yes, if the Statement of Good Health reveals new high-risk medical conditions or significant changes in health status, the insurer may deny the reinstatement request. In such cases, the company may offer to reinstate the policy with higher premiums, exclude certain conditions, or require the individual to apply for a brand-new policy.

Is a Statement of Good Health the same as a medical exam?

No, a Statement of Good Health is a self-reported attestation of your current medical status, whereas a medical exam involves physical tests by a healthcare professional. While the statement is often sufficient for short-term lapses, insurers reserve the right to request a full paramedical exam if the statement indicates potential health risks.

Comments