Restoring your liability coverage requires a formal Umbrella Policy Reinstatement Letter to address lapses or cancellations. This document confirms your intent to maintain extra protection and ensures continuous financial security against significant claims. Clearly outlining policy details and payment status is essential for a successful appeal to your insurer. To help you draft yours, below are some ready to use template.

Image cover: How to Write an Umbrella Policy Reinstatement Letter: Samples and Templates

Letter Samples List

- Standard Umbrella Policy Reinstatement Letter

- Commercial Umbrella Policy Reinstatement Letter

- Personal Umbrella Policy Reinstatement Letter

- Lapsed Umbrella Policy Reinstatement Letter

- Conditional Umbrella Policy Reinstatement Letter

- Statement of No Loss Umbrella Reinstatement Letter

- Past Due Premium Umbrella Reinstatement Letter

- Underwriting Approved Umbrella Reinstatement Letter

- Grace Period Umbrella Policy Reinstatement Letter

- Final Notice Umbrella Policy Reinstatement Letter

- Agency Requested Umbrella Policy Reinstatement Letter

- Excess Liability Umbrella Policy Reinstatement Letter

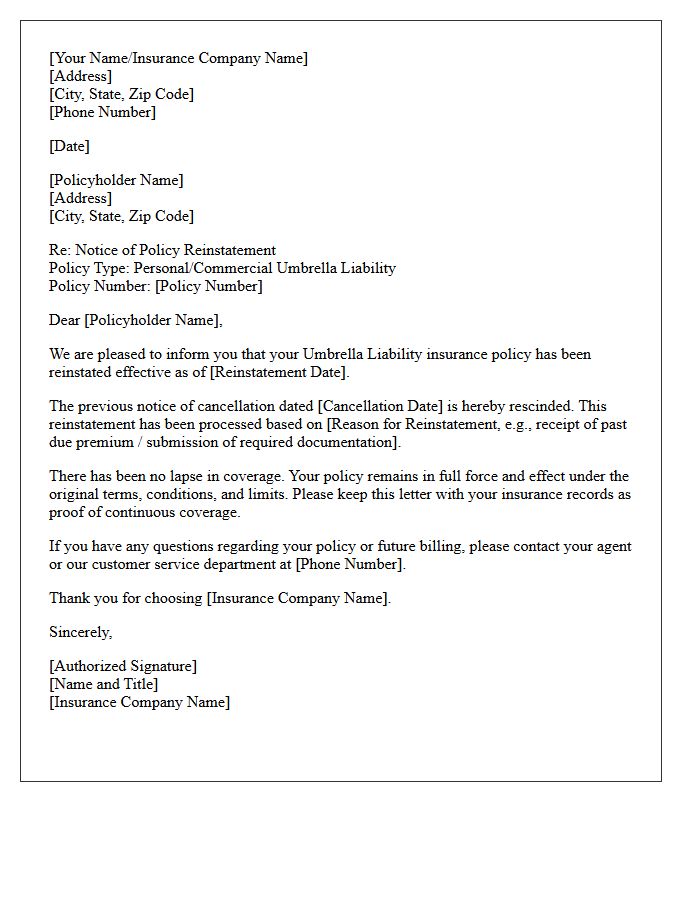

Standard Umbrella Policy Reinstatement Letter

A Standard Umbrella Policy Reinstatement Letter is a formal document issued by an insurer to restore excess liability coverage after a lapse. To ensure legal protection, policyholders must promptly address the reinstatement conditions, which typically include paying outstanding premiums and signing a "no loss" statement. This statement confirms that no claims occurred during the inactive period. Timely processing is essential to maintain your financial safety net, as this policy provides vital protection beyond your primary insurance limits against catastrophic legal or medical expenses.

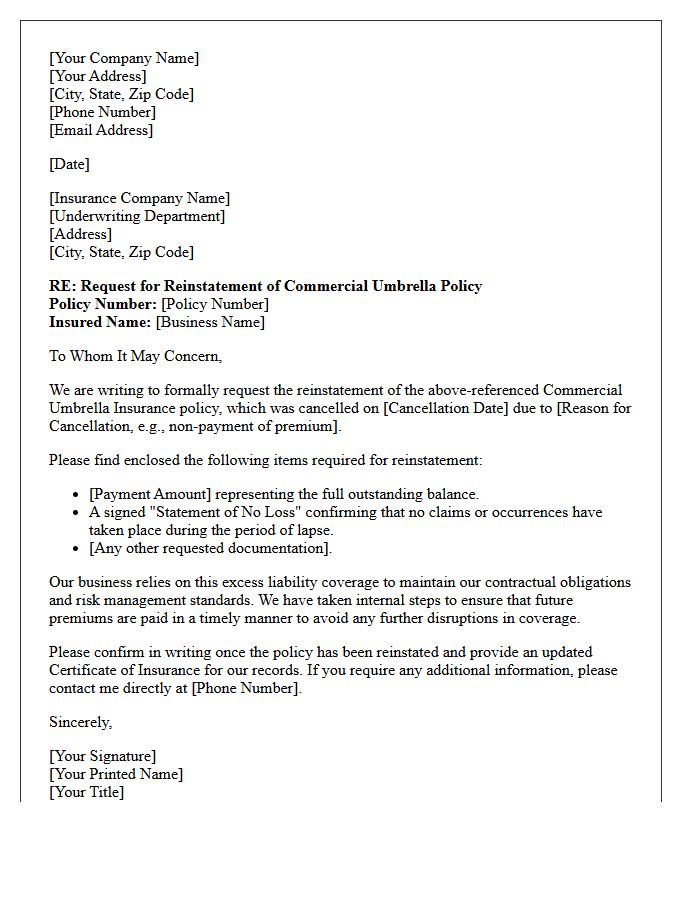

Commercial Umbrella Policy Reinstatement Letter

A Commercial Umbrella Policy Reinstatement Letter is a formal request sent to an insurer to restore a cancelled liability policy. It must clearly address the reason for cancellation, such as non-payment or underwriting issues. Providing proof that outstanding premiums are paid and confirming no losses occurred during the lapse is essential. Approval is at the carrier's discretion and often requires a signed Statement of No Loss. Timely submission is critical to maintaining continuous excess liability coverage and protecting business assets against catastrophic financial claims.

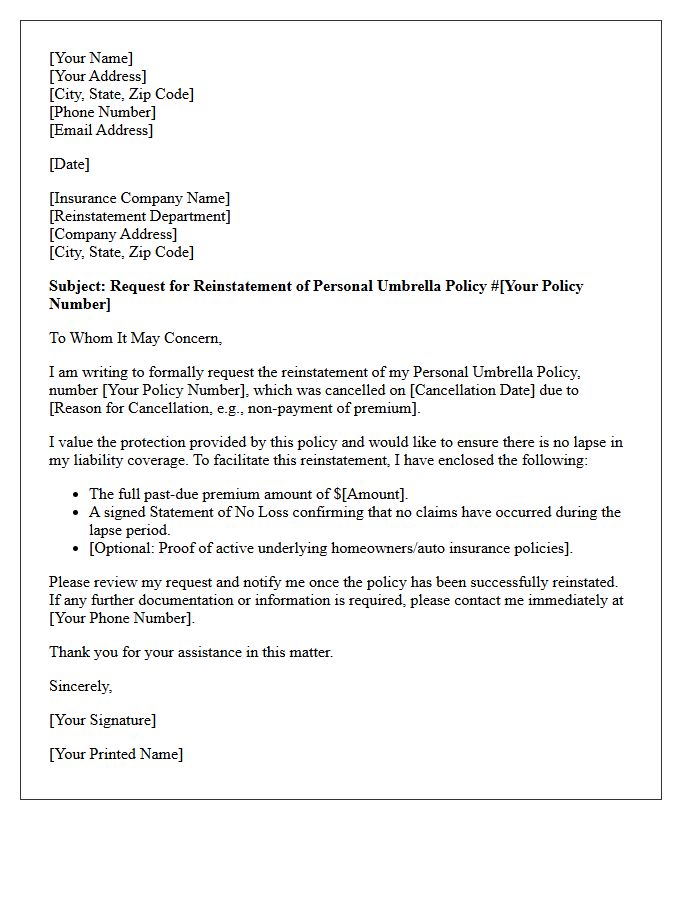

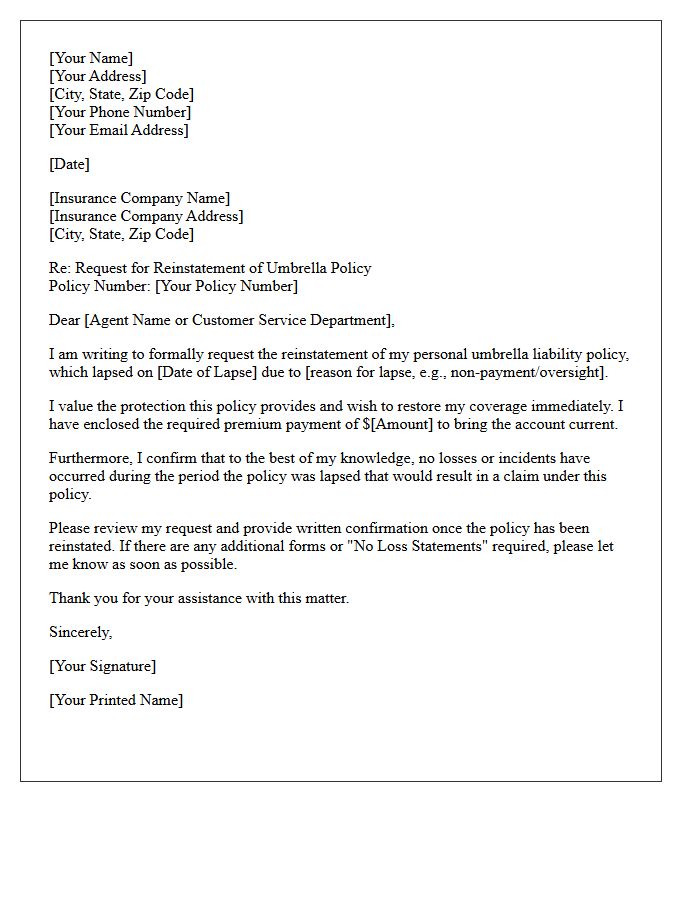

Personal Umbrella Policy Reinstatement Letter

A Personal Umbrella Policy Reinstatement Letter is a formal request to restore liability coverage after a lapse or cancellation. It is crucial to submit this document promptly to avoid unprotected assets and potential legal exposure. The letter must address the reason for termination, such as missed payments, and include a statement confirming there were no pending claims during the uncovered period. Promptly reinstating your policy ensures continuous high-limit protection beyond your standard homeowners or auto insurance, safeguarding your long-term financial security from catastrophic lawsuits.

Lapsed Umbrella Policy Reinstatement Letter

A reinstatement letter is a formal request to restore a canceled umbrella insurance policy. When a policy lapses due to non-payment, you must submit this written document to prove there were no claims during the uncovered period. Promptly addressing a lapse is critical because a gap in liability protection leaves your personal assets vulnerable. Ensure the letter includes your policy number, signature, and payment. Acceptance is at the insurer's discretion, so maintaining continuous coverage is essential to avoid higher premiums or permanent loss of high-limit protection.

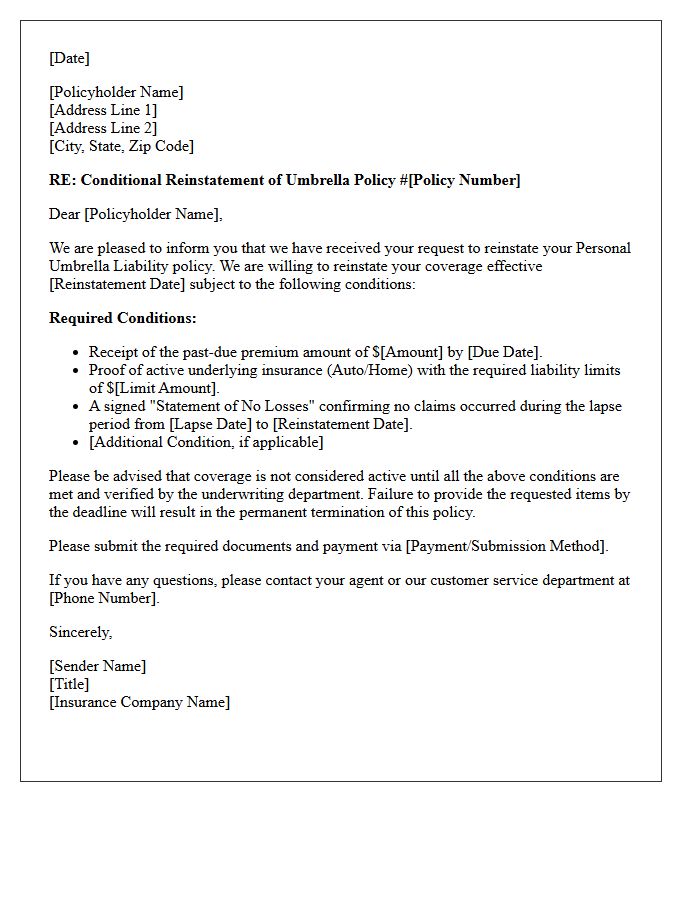

Conditional Umbrella Policy Reinstatement Letter

A Conditional Umbrella Policy Reinstatement Letter is a formal document issued by an insurer outlining requirements to restore lapsed liability coverage. It serves as a binding notice that protection is not yet active. Policyholders must typically provide a signed "No Loss Statement," confirming no claims occurred during the gap, and pay outstanding premiums. Understanding the effective date is critical, as coverage only resumes once the underwriter approves these specific conditions. Failing to comply promptly leaves your personal assets exposed to catastrophic legal claims and significant financial risk.

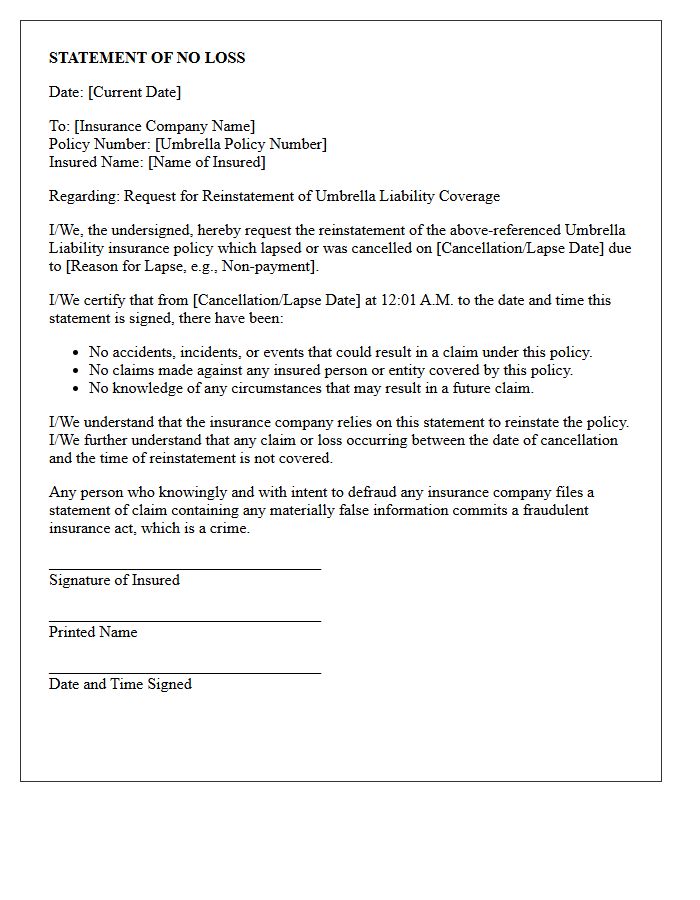

Statement of No Loss Umbrella Reinstatement Letter

A Statement of No Loss is a critical document required to reinstate a lapsed umbrella insurance policy. By signing this letter, the policyholder confirms that no claims or incidents occurred during the period when coverage was inactive. It serves as a legal guarantee to the insurer that they are not inheriting undisclosed liabilities. Providing accurate information is essential, as any misrepresentation can lead to a denial of future claims or the cancellation of your liability protection. Always ensure timely submission to maintain continuous, high-limit financial security.

Past Due Premium Umbrella Reinstatement Letter

A Past Due Premium Umbrella Reinstatement Letter is a formal notification from an insurer regarding a lapsed policy due to non-payment. This document outlines the specific reinstatement requirements, such as settling outstanding balances and potentially submitting a statement of no loss. Act promptly to maintain your excess liability coverage, as a gap in protection leaves your personal assets vulnerable to major lawsuits. Ensuring timely payment helps preserve your financial security and prevents the permanent cancellation of your umbrella policy benefits.

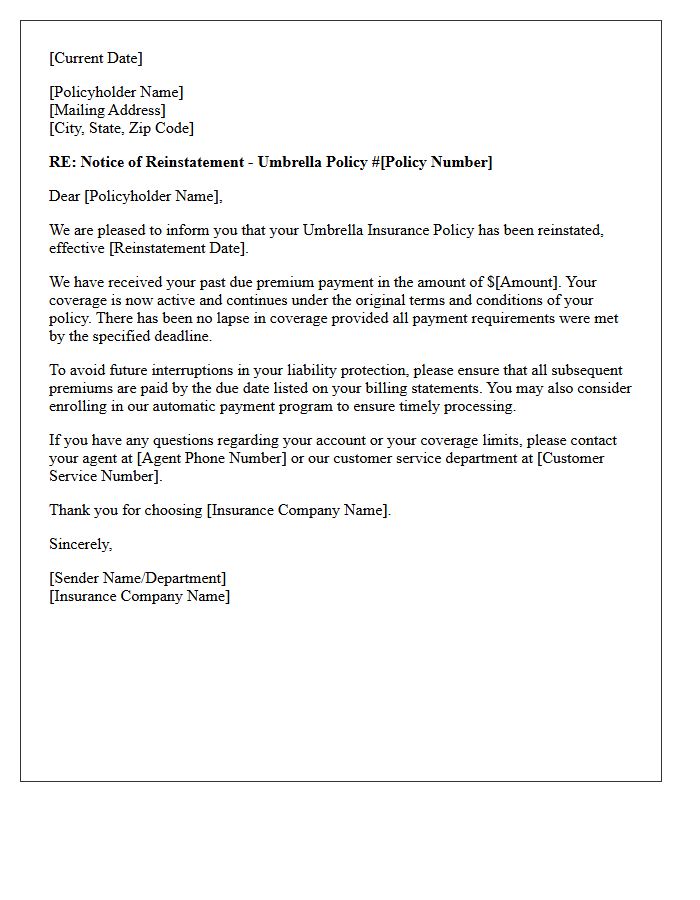

Underwriting Approved Umbrella Reinstatement Letter

An Underwriting Approved Umbrella Reinstatement Letter is a formal document confirming that a lapsed personal or commercial umbrella liability policy is back in force. It signifies that the carrier's underwriters have reviewed and accepted the risk after a payment default or expiration. This letter provides legal proof of continuous coverage and maintains high-limit protection against catastrophic lawsuits. Policyholders must verify the effective date to ensure there are no gaps in liability security, as this restoration preserves the excess layers of financial defense beyond standard underlying policies.

Grace Period Umbrella Policy Reinstatement Letter

A Grace Period Umbrella Policy Reinstatement Letter is a formal request to restore liability coverage after a missed payment. To prevent a permanent lapse in coverage, the policyholder must typically submit this written notice alongside the outstanding premium. It is crucial to confirm that no claims occurred during the inactive window. Prompt action ensures your excess liability protection remains intact, safeguarding personal assets against catastrophic legal claims. Always verify specific state regulations and insurer requirements to guarantee the reinstatement is officially processed and your financial protection is fully restored.

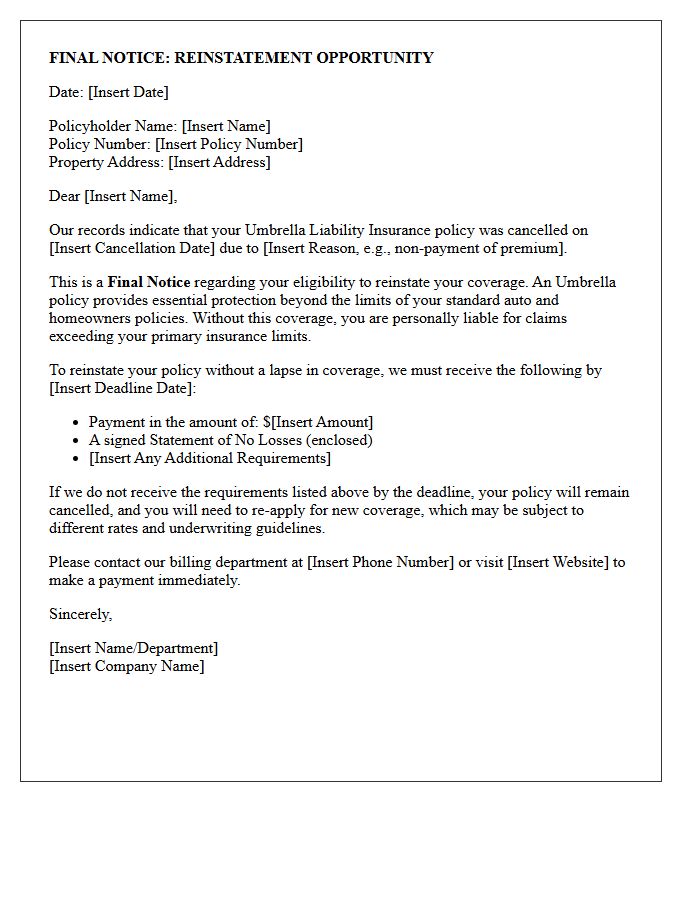

Final Notice Umbrella Policy Reinstatement Letter

A Final Notice Umbrella Policy Reinstatement Letter is a critical notification from an insurer regarding the restoration of your liability coverage. It confirms that a previously canceled or lapsed policy is active again, typically after outstanding premiums are paid or specific conditions are met. This document is essential for maintaining your personal asset protection. Always verify the effective date of the reinstatement to ensure there are no gaps in your excess liability insurance, as this policy provides vital security beyond your standard homeowners or auto coverage limits.

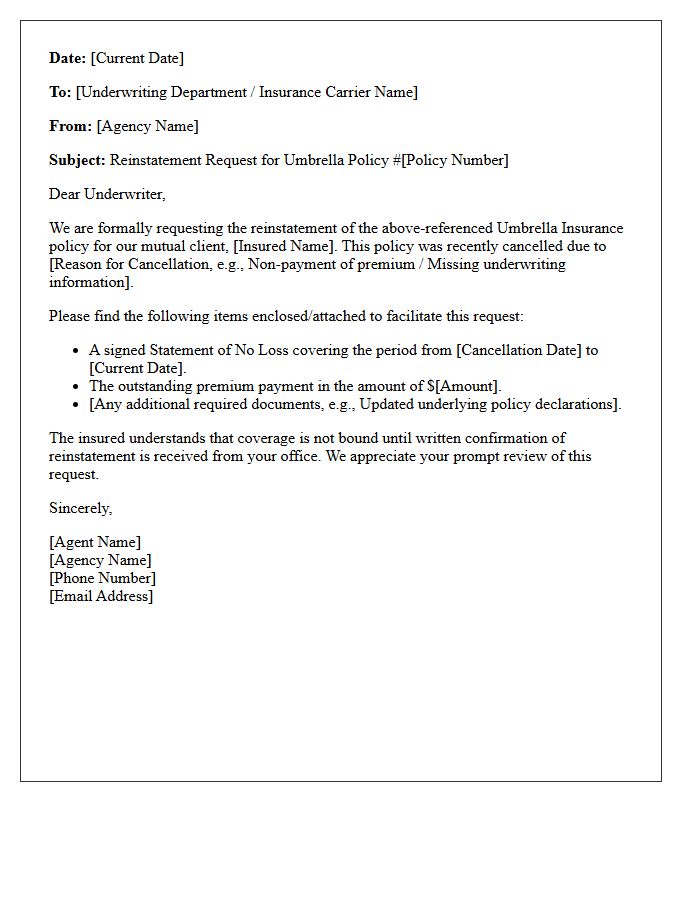

Agency Requested Umbrella Policy Reinstatement Letter

An Agency Requested Umbrella Policy Reinstatement Letter is a formal document sent by an insurance provider or broker to restore a lapsed liability policy. It is crucial to address the underlying cause of the cancellation, such as non-payment or missing underwriting data, to ensure continuous excess coverage. Promptly submitting this request helps maintain your financial protection against catastrophic legal claims. Always verify that all outstanding requirements are met before submission to guarantee the insurer approves the reinstatement without a permanent gap in your insurance history.

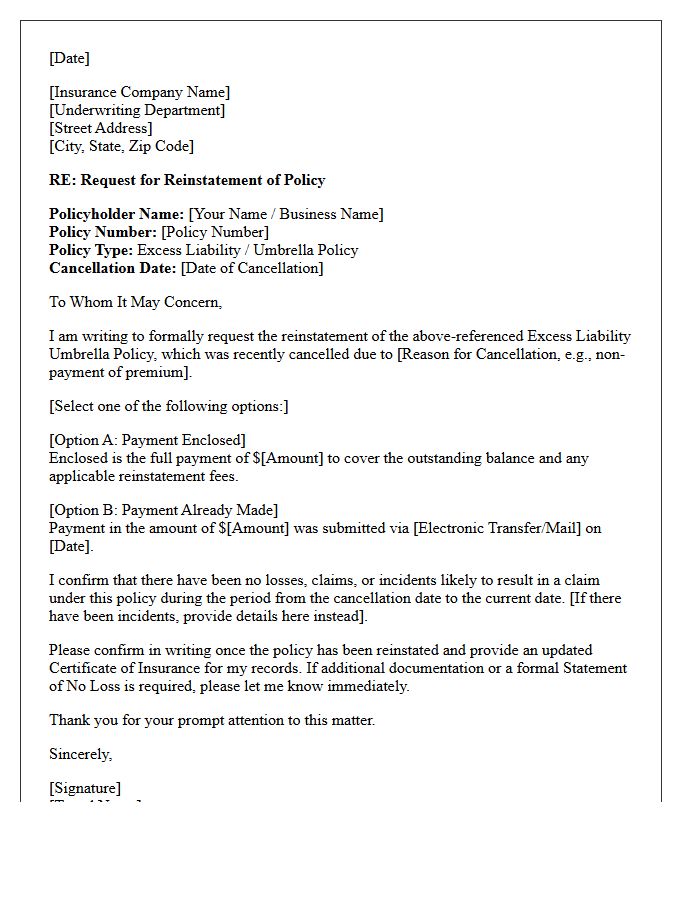

Excess Liability Umbrella Policy Reinstatement Letter

An Excess Liability Umbrella Policy Reinstatement Letter is a critical legal document issued by an insurer to restore coverage after a lapse or cancellation. This letter confirms that the policy is active again, often following the payment of overdue premiums or the resolution of underwriting issues. It is essential to verify the reinstatement date to ensure there are no gaps in protection. Maintaining a continuous insurance history through this document protects your assets against catastrophic claims that exceed primary policy limits.

What is an Umbrella Policy Reinstatement Letter?

An Umbrella Policy Reinstatement Letter is a formal written request sent by a policyholder to an insurance provider asking to restore an excess liability policy that has lapsed or been cancelled, typically due to non-payment or underwriting issues.

What should be included in an umbrella insurance reinstatement request?

The letter should include the policy number, the date of cancellation, the reason for the lapse, a formal request to reinstate coverage, and any required documentation such as a Statement of No Loss or proof of payment.

Is a Statement of No Loss required for umbrella policy reinstatement?

Yes, most insurers require a signed Statement of No Loss along with the reinstatement letter to confirm that no liability claims or incidents occurred during the period when the umbrella coverage was inactive.

How long do I have to send a reinstatement letter after my policy cancels?

The "reinstatement window" varies by insurer, but most companies allow a request within 15 to 30 days of cancellation. If the lapse exceeds this timeframe, you may be required to apply for a brand-new policy at current market rates.

Can an insurance company deny an umbrella policy reinstatement request?

Insurance companies reserve the right to deny reinstatement based on the duration of the lapse, a change in risk profile, or a history of frequent payment issues. If denied, the carrier will issue a formal notice detailing why the coverage cannot be restored.

Comments