Received an Inflation Guard Adjustment Renewal Notice? This notice informs policyholders that their coverage limits have increased to keep pace with rising construction costs and economic shifts. It ensures your property remains adequately insured against current market values. Understanding these automated adjustments is vital for maintaining comprehensive protection. To help you respond effectively, below are some ready to use template.

Image cover: Inflation Guard Adjustment: Renewal Notice Templates and Communication Guide

Letter Samples List

- Standard Homeowners Inflation Guard Renewal Letter

- Commercial Property Inflation Guard Adjustment Letter

- Annual Policy Renewal and Inflation Guard Notice Letter

- Building Coverage Inflation Guard Update Letter

- Premium Adjustment and Inflation Guard Renewal Letter

- Residential Property Inflation Guard Endorsement Letter

- Business Owner Policy Inflation Guard Renewal Letter

- Automatic Limit Increase and Inflation Guard Letter

- Construction Cost Inflation Guard Adjustment Letter

- Policy Limits Update and Inflation Guard Renewal Letter

- Condominium Association Inflation Guard Notice Letter

- Insurance Valuation Inflation Guard Adjustment Letter

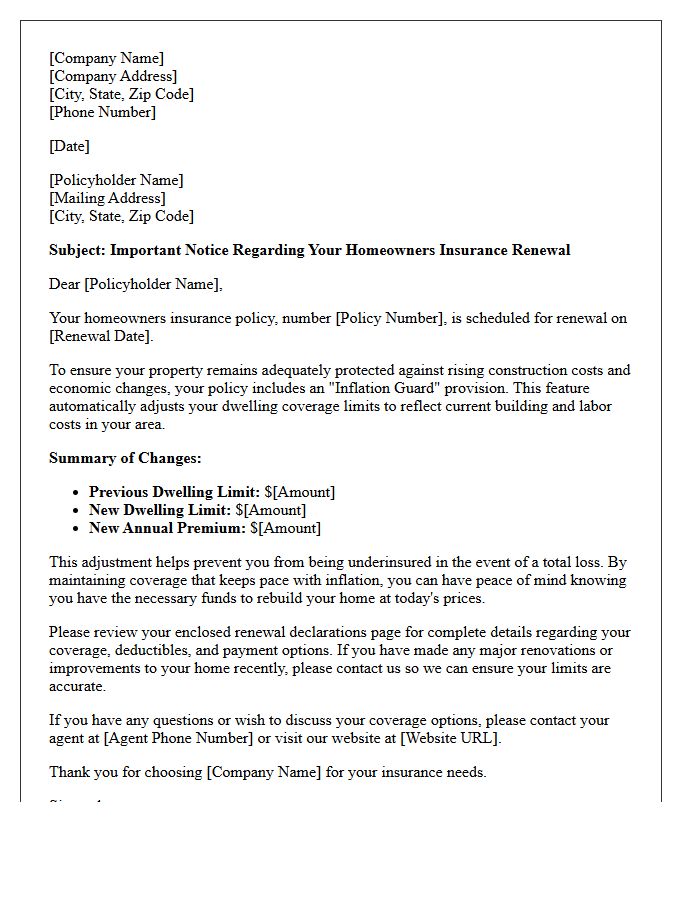

Standard Homeowners Inflation Guard Renewal Letter

A Standard Homeowners Inflation Guard Renewal Letter notifies policyholders of automatic coverage increases designed to keep pace with rising construction costs. The inflation guard endorsement ensures your dwelling limit reflects current market values, preventing underinsurance after a total loss. Review this renewal notice carefully, as the adjustment typically leads to a proportional increase in your annual premium. It is essential to verify that these indexed updates accurately represent your home's replacement cost to maintain comprehensive financial protection against economic fluctuations and labor price spikes.

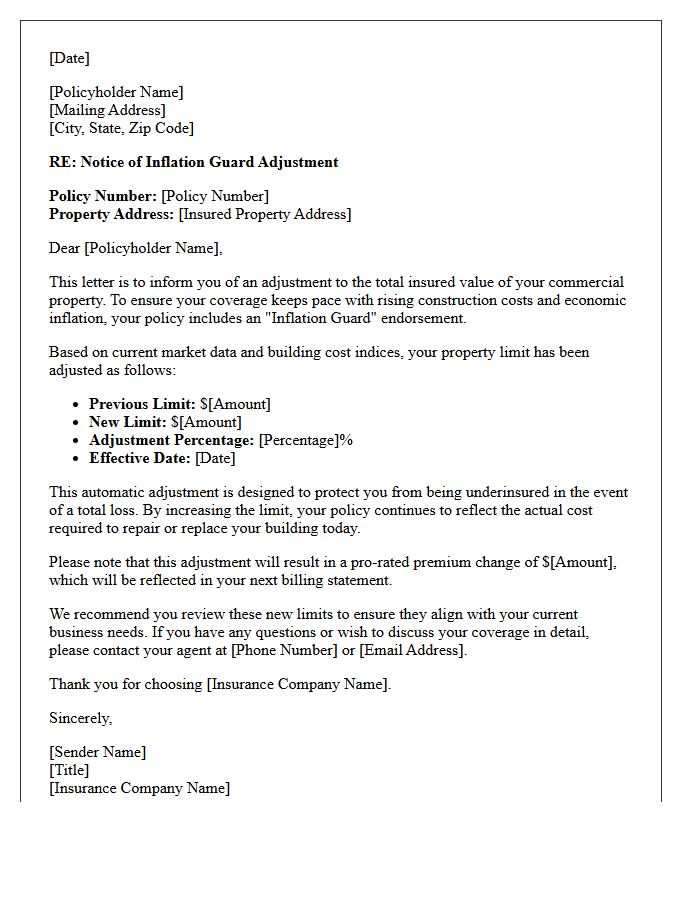

Commercial Property Inflation Guard Adjustment Letter

A Commercial Property Inflation Guard Adjustment Letter notifies policyholders of an automatic increase in insurance coverage limits. This adjustment accounts for rising construction costs and economic inflation, ensuring the property remains fully insured to its true replacement value. By periodically updating limits, this endorsement prevents underinsurance penalties during a claim. It is a critical tool for maintaining financial protection, as it helps property owners avoid out-of-pocket expenses when building materials and labor costs surge unexpectedly. Always review the specific percentage increase to ensure it aligns with current market trends.

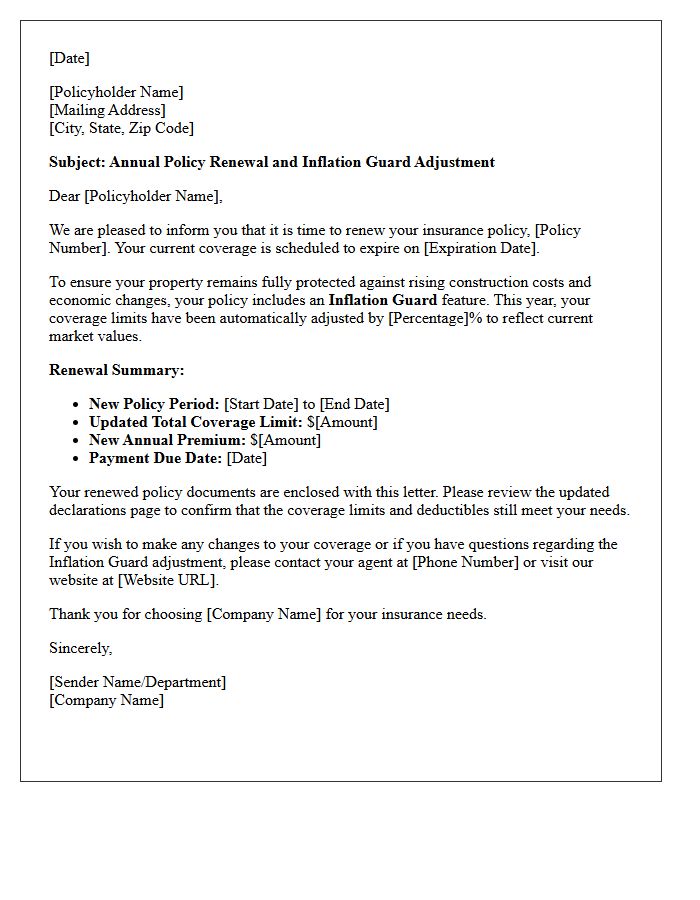

Annual Policy Renewal and Inflation Guard Notice Letter

An Annual Policy Renewal and Inflation Guard Notice is a critical update from your insurer. It confirms your coverage continues for another year while automatically adjusting your dwelling limits to match current construction costs. This Inflation Guard feature prevents underinsurance by accounting for rising labor and material prices. Review this letter carefully to understand new premium costs and ensure your replacement cost coverage remains adequate. If your property has undergone significant renovations, contact your agent immediately to manually update your policy limits beyond these standard inflationary adjustments.

Building Coverage Inflation Guard Update Letter

A Building Coverage Inflation Guard Update Letter is an essential notice informing policyholders about automatic adjustments to their property insurance limits. This proactive measure ensures that coverage keeps pace with rising construction costs and economic trends. By incrementally increasing the insured value, the Inflation Guard protects you from being underinsured during a total loss. It is crucial to review these updates carefully to confirm your replacement cost valuation remains accurate, preventing potential financial gaps when rebuilding your home or commercial structure in today's shifting market.

Premium Adjustment and Inflation Guard Renewal Letter

The Premium Adjustment and Inflation Guard Renewal Letter is a crucial notice informing policyholders about annual coverage increases designed to keep pace with rising costs. This document explains how your benefits automatically adjust to prevent underinsurance due to inflation. Reviewing this letter is essential because it details changes to your monthly premiums and the updated total value of your protection. Understanding these adjustments ensures your policy remains effective over time, maintaining the purchasing power of your coverage without requiring additional medical underwriting or manual updates.

Residential Property Inflation Guard Endorsement Letter

A Residential Property Inflation Guard Endorsement is a vital insurance add-on that automatically increases your dwelling coverage limits to keep pace with rising construction costs. This ensures you are not underinsured if inflation spikes or material prices climb. By adjusting your policy limits annually, it protects your home's replacement cost value without requiring manual updates. Without this endorsement, a major claim could leave you with significant out-of-pocket expenses because your original policy limit may no longer cover the modern price of labor and building supplies.

Business Owner Policy Inflation Guard Renewal Letter

A Business Owner Policy (BOP) renewal letter often includes an Inflation Guard provision. This essential feature automatically increases your property coverage limits to keep pace with rising construction costs and economic changes. It ensures you are not underinsured if a total loss occurs. When reviewing your renewal, verify the annual percentage increase applied to your building and personal property. Maintaining adequate valuation is critical to avoid coinsurance penalties and ensure your business assets remain fully protected against modern replacement expenses in a fluctuating market.

Automatic Limit Increase and Inflation Guard Letter

An Automatic Limit Increase and Inflation Guard letter notifies policyholders that their coverage limits are rising to keep pace with economic changes. This adjustment ensures your insurance protection remains adequate as construction costs and property values grow. While this helps prevent underinsurance, it typically results in a higher premium. Reviewing these updates is essential to confirm the new valuation aligns with your current needs and that you are not paying for unnecessary coverage levels during inflationary periods.

Construction Cost Inflation Guard Adjustment Letter

A Construction Cost Inflation Guard Adjustment Letter is a critical document used to update property replacement values based on rising market prices. It ensures that insurance coverage keeps pace with the increasing costs of labor and materials, such as steel or lumber. By implementing this inflation guard, property owners avoid being underinsured during a total loss. This proactive adjustment protects your investment from valuation gaps caused by economic shifts, guaranteeing that your policy limits remain sufficient to rebuild at current market rates without unexpected financial shortfalls.

Policy Limits Update and Inflation Guard Renewal Letter

A Policy Limits Update and Inflation Guard Renewal Letter notifies policyholders of automatic adjustments to their coverage totals. To account for rising construction costs and economic inflation, insurers increase your dwelling limits to ensure you remain fully insured. Reviewing this renewal notice is essential to confirm your property is not underinsured. While these updates enhance financial protection, they typically result in a premium increase. Always compare the adjusted limits against current market values to maintain adequate coverage and avoid out-of-pocket expenses after a total loss.

Condominium Association Inflation Guard Notice Letter

A Condominium Association Inflation Guard Notice Letter is a formal communication informing owners of automatic adjustments to property insurance coverage. This provision ensures the policy limit increases annually to keep pace with rising reconstruction costs and economic inflation. It is vital for maintaining adequate protection against underinsurance during a loss. Residents should review these updates to understand how the inflation guard impact their monthly assessment fees and overall financial stability of the association, ensuring the building remains fully protected against market fluctuations.

Insurance Valuation Inflation Guard Adjustment Letter

An Insurance Valuation Inflation Guard Adjustment Letter notifies policyholders about automatic increases in coverage limits. This adjustment ensures your property insurance keeps pace with rising construction costs and economic changes. Without this feature, inflation could leave you underinsured, resulting in significant out-of-pocket expenses after a loss. Reviewing this letter is essential to confirm your replacement cost remains accurate. While it protects your investment, it typically leads to a modest premium increase reflected in your renewal statement to maintain adequate financial protection for your assets.

What is an Inflation Guard Adjustment Renewal Notice?

An Inflation Guard Adjustment Renewal Notice is a notification sent by an insurance provider during policy renewal that informs the policyholder of an automatic increase in coverage limits. This adjustment is designed to ensure that property insurance keeps pace with rising construction costs and economic inflation.

Why did my insurance coverage amount increase on my renewal notice?

Your coverage increased because of the Inflation Guard endorsement, which periodically adjusts your dwelling limit to reflect the current market costs of labor and materials. This proactive measure prevents you from being underinsured in the event of a total loss during periods of high inflation.

How is the Inflation Guard percentage determined?

The adjustment percentage is typically based on regional construction cost indexes and inflationary data provided by third-party valuation services. This ensures that the replacement cost of your home remains accurate relative to local economic shifts.

Will an Inflation Guard adjustment increase my insurance premium?

Yes, because the total amount of insurance coverage (Limit of Liability) is increasing, the premium will usually rise accordingly. You are paying for a higher level of protection to match the increased value and rebuild cost of your property.

Can I opt out of the Inflation Guard Adjustment?

While most experts advise keeping the adjustment to maintain full replacement cost protection, many insurers allow you to request a manual adjustment or removal of the endorsement. However, doing so may leave you with a "co-insurance" penalty or insufficient funds to rebuild after a claim.

Comments