Receiving a Post-Bankruptcy Discharge Acceleration Notice can be overwhelming, as it signals a creditor's demand for immediate payment of the remaining loan balance. Understanding your legal rights and the impact of the discharge injunction is essential for protecting your financial future. This guide explains how to respond effectively to these notices. Below are some ready to use templates.

Image cover: Navigating Acceleration Notices After Bankruptcy Discharge: Essential Templates and Guidance

Letter Samples List

- Post-Bankruptcy Discharge Mortgage Acceleration Letter

- Notice of Acceleration and Foreclosure Intent Post-Discharge Letter

- Chapter Seven Discharge In Rem Acceleration Letter

- Mortgage Default and Debt Acceleration Post-Bankruptcy Letter

- Post-Discharge Property Lien Acceleration Notice Letter

- Bankruptcy Discharge Acknowledgment and Mortgage Acceleration Letter

- In Rem Foreclosure and Loan Acceleration Demand Letter

- Post-Chapter Thirteen Discharge Mortgage Acceleration Letter

- Notice of Loan Acceleration Following Bankruptcy Discharge Letter

- Retained Lien Acceleration and Foreclosure Warning Letter

- Post-Bankruptcy Discharge Breach and Acceleration Letter

- Mortgage Maturity Acceleration Post-Discharge Notice Letter

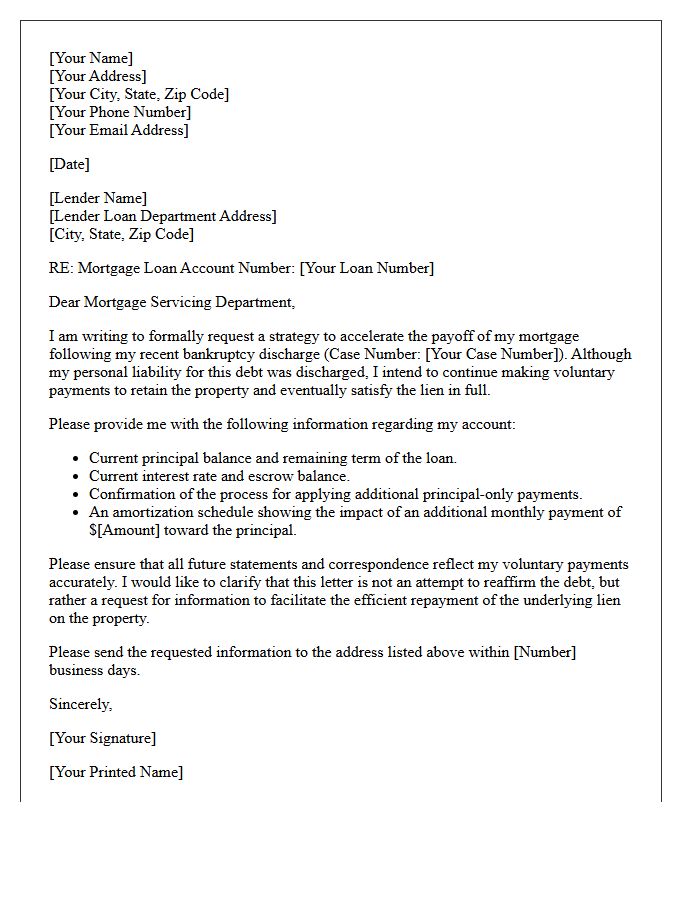

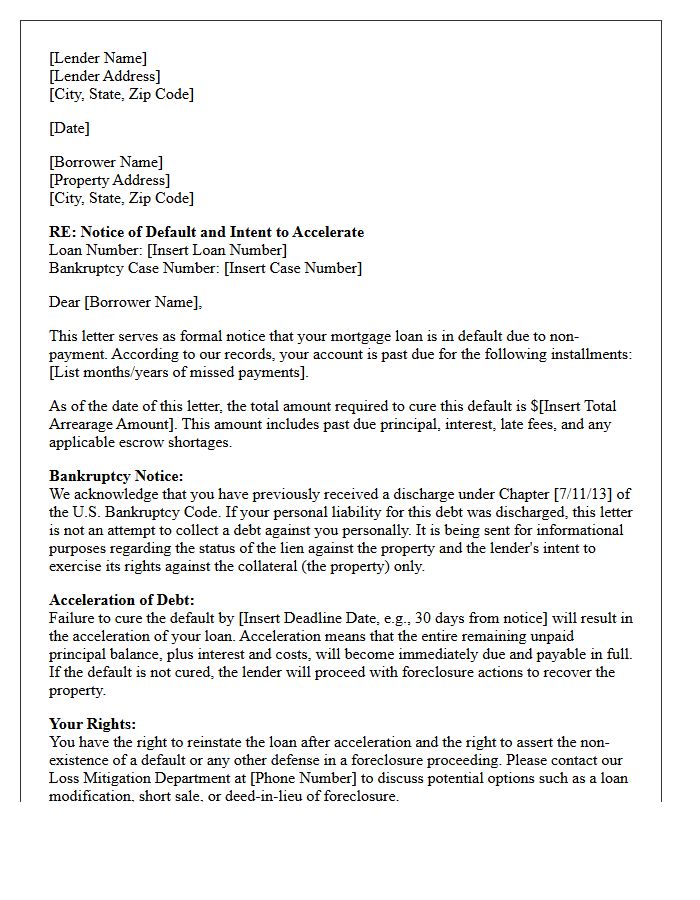

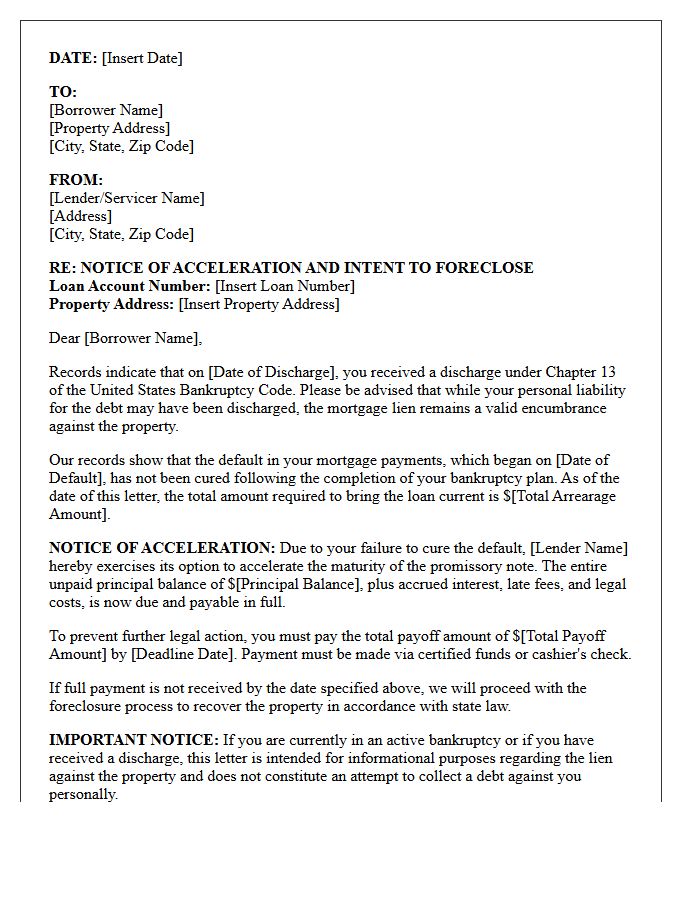

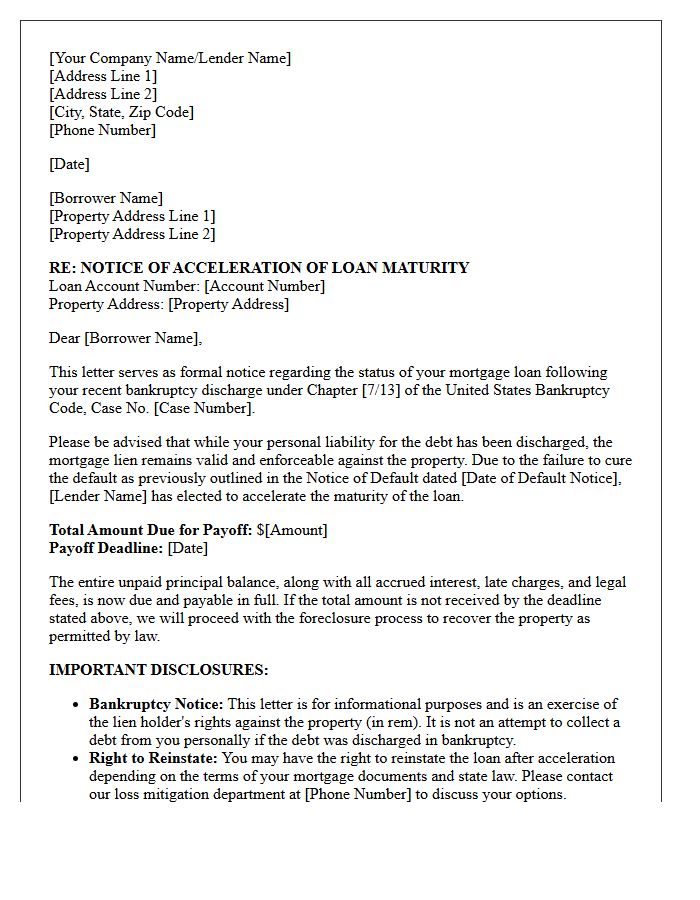

Post-Bankruptcy Discharge Mortgage Acceleration Letter

A post-bankruptcy discharge mortgage acceleration letter notifies borrowers that the lender is demanding the full loan balance immediately due to missed payments. While a bankruptcy discharge eliminates your personal liability, it does not remove the lien on the property. This letter is often a formal legal precursor to foreclosure proceedings. It is crucial to understand that even without personal liability, the lender retains the right to seize the collateral. To keep your home, you must address the default through reinstatement, a loan modification, or a repayment plan.

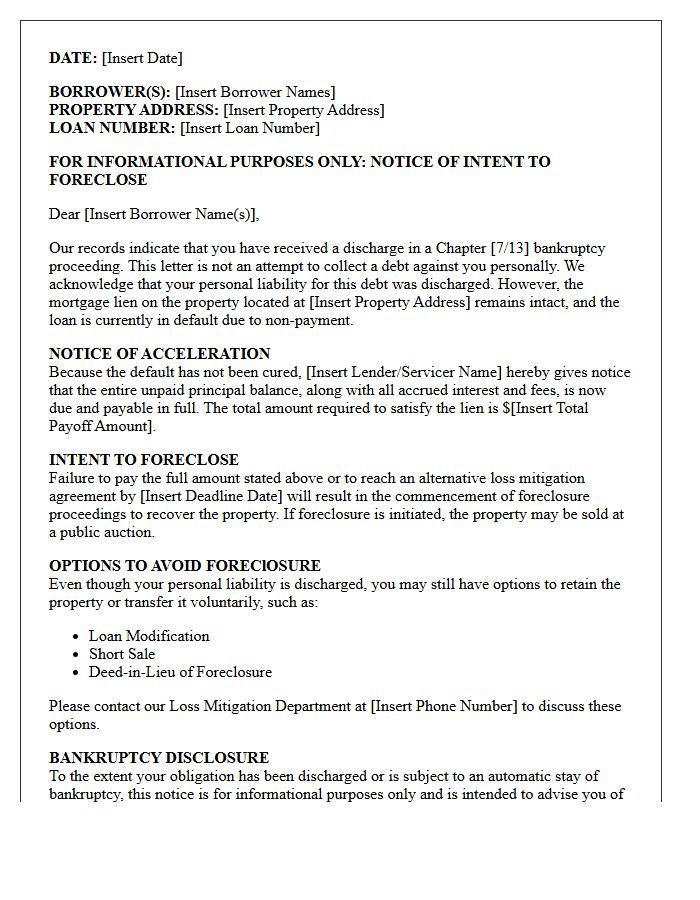

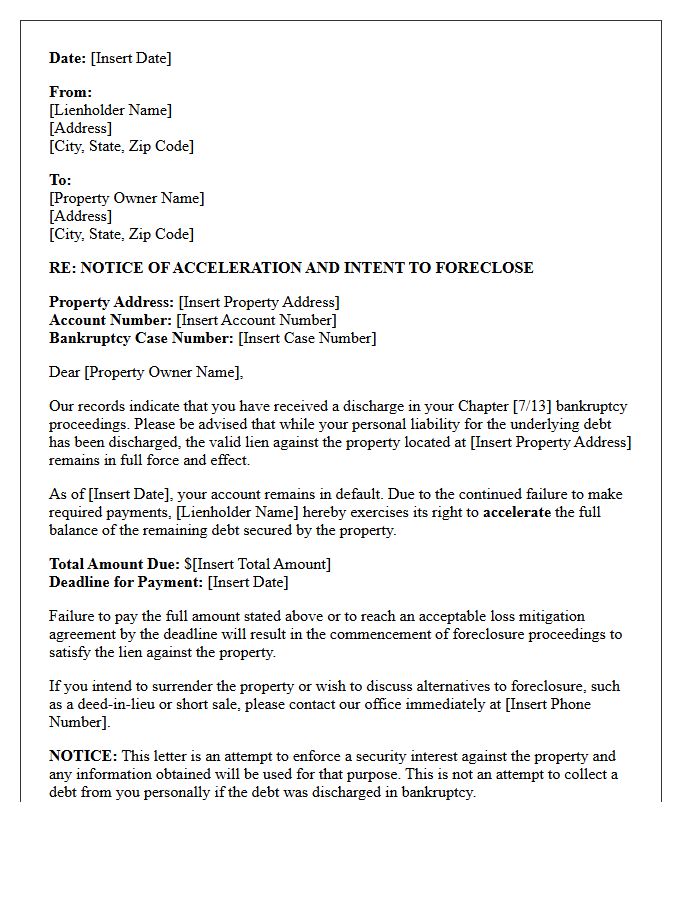

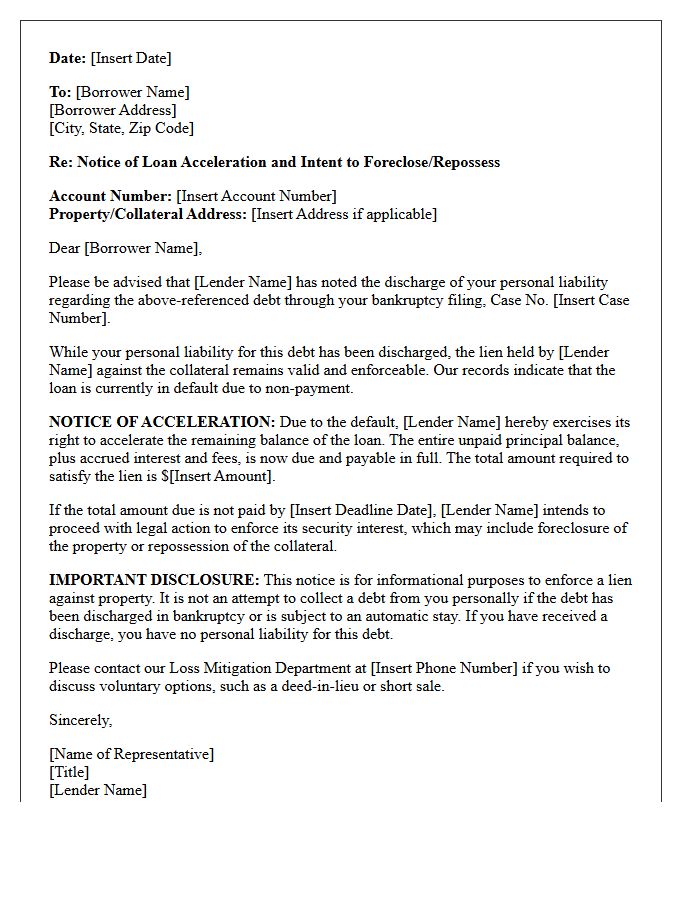

Notice of Acceleration and Foreclosure Intent Post-Discharge Letter

Receiving a Notice of Acceleration and Foreclosure Intent after a bankruptcy discharge is a critical legal warning. While the discharge eliminates your personal liability for the debt, it does not remove the lien on the property. This letter signifies that the lender is initiating the legal process to seize the home due to missed payments. Homeowners should immediately review their options, such as a loan modification or reinstatement, to prevent a trustee sale. Understanding your property rights post-discharge is essential to avoiding permanent loss of your primary residence.

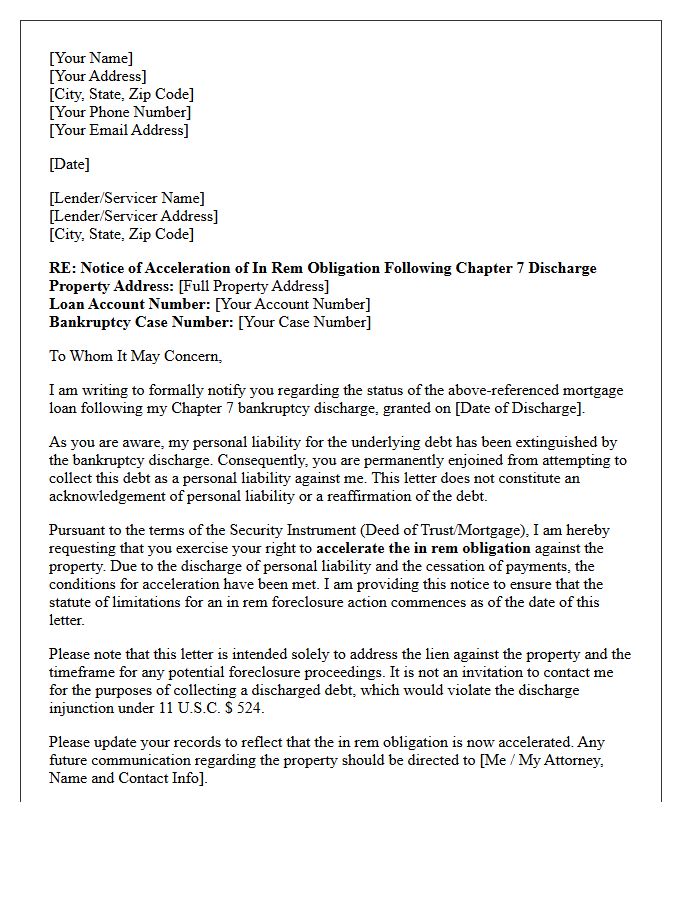

Chapter Seven Discharge In Rem Acceleration Letter

A Chapter Seven Discharge In Rem Acceleration Letter is a formal legal notice sent by mortgage lenders following a bankruptcy. While the Chapter 7 discharge eliminates your personal liability for the debt, the lender retains a lien on the property. This letter signifies the start of the foreclosure process by demanding the full loan balance. It is crucial to understand that while you are protected from collection lawsuits, the lender can still seize the collateral. Homeowners must act quickly to negotiate a modification or voluntary surrender to avoid losing their residence.

Mortgage Default and Debt Acceleration Post-Bankruptcy Letter

Receiving a mortgage default notice after filing for bankruptcy signifies that your lender intends to initiate foreclosure due to missed payments. A critical component is the debt acceleration clause, which demands immediate repayment of the entire loan balance rather than just the arrears. Even if your personal liability was discharged in Chapter 7, the bank retains a lien on the property. To prevent losing your home, you must address the default through a reinstatement, loan modification, or Chapter 13 repayment plan to cure the delinquency and stop the legal foreclosure process.

Post-Discharge Property Lien Acceleration Notice Letter

A Post-Discharge Property Lien Acceleration Notice Letter informs homeowners that while personal liability for a debt was removed via bankruptcy, the enforceable lien remains attached to the collateral. This critical notice warns that the lender intends to initiate foreclosure proceedings unless the remaining secured balance is resolved. It serves as a final legal communication before the property is seized, meaning you must act immediately to negotiate a settlement or reaffirmation agreement to prevent the loss of your home despite the previous debt discharge.

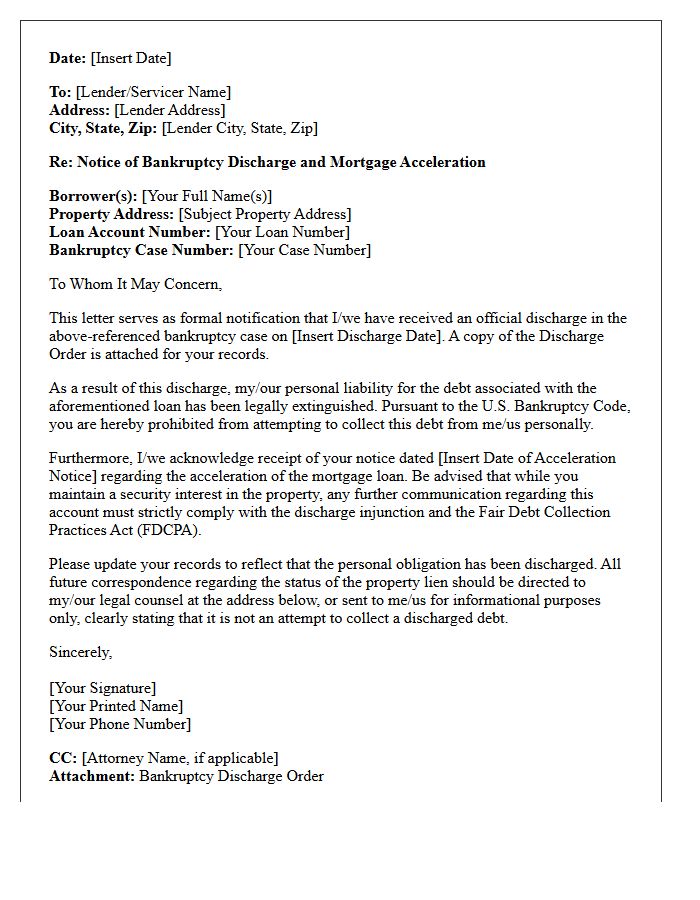

Bankruptcy Discharge Acknowledgment and Mortgage Acceleration Letter

Receiving a Bankruptcy Discharge Acknowledgment confirms you are no longer personally liable for specific debts. However, if you receive a Mortgage Acceleration Letter simultaneously, it indicates the lender is demanding full payment of the remaining balance to avoid foreclosure. While the discharge prevents creditors from suing you for money, the lien remains attached to the property. Understanding this distinction is vital: your credit is protected from deficiency judgments, but the right to foreclose persists if monthly payments are missed. Consult a professional to navigate these conflicting notices effectively.

In Rem Foreclosure and Loan Acceleration Demand Letter

Receiving an In Rem Foreclosure notice signifies that a lender is taking legal action specifically against the property to satisfy a debt, rather than the individual borrower. This often follows a Loan Acceleration Demand Letter, which officially declares the entire mortgage balance due immediately after a default. Understanding this process is critical because it marks the final stage before a property sale. To protect your equity and ownership, you must respond to these legal documents promptly to explore loss mitigation, reinstatement, or foreclosure defense options before the court grants a final judgment.

Post-Chapter Thirteen Discharge Mortgage Acceleration Letter

Receiving a Post-Chapter Thirteen Discharge Mortgage Acceleration Letter often occurs because the bankruptcy discharge eliminates personal liability but does not remove the lien on the property. If payments were missed or the loan was not fully reinstated, the lender may initiate foreclosure. It is crucial to verify if the debt was included in your repayment plan or if the notice is a procedural requirement. Consult your attorney immediately to ensure your mortgage servicer is not violating the discharge injunction or to negotiate a loan modification to save your home.

Notice of Loan Acceleration Following Bankruptcy Discharge Letter

A Notice of Loan Acceleration following a bankruptcy discharge informs borrowers that the lender is demanding immediate repayment of the full loan balance. While a discharge eliminates personal liability, the security interest or lien on the property remains intact. This letter typically serves as a formal precursor to foreclosure proceedings if the default is not cured. It is crucial to understand that even without personal legal obligation to pay, the lender retains the right to seize the collateral to satisfy the outstanding debt according to the original contract terms.

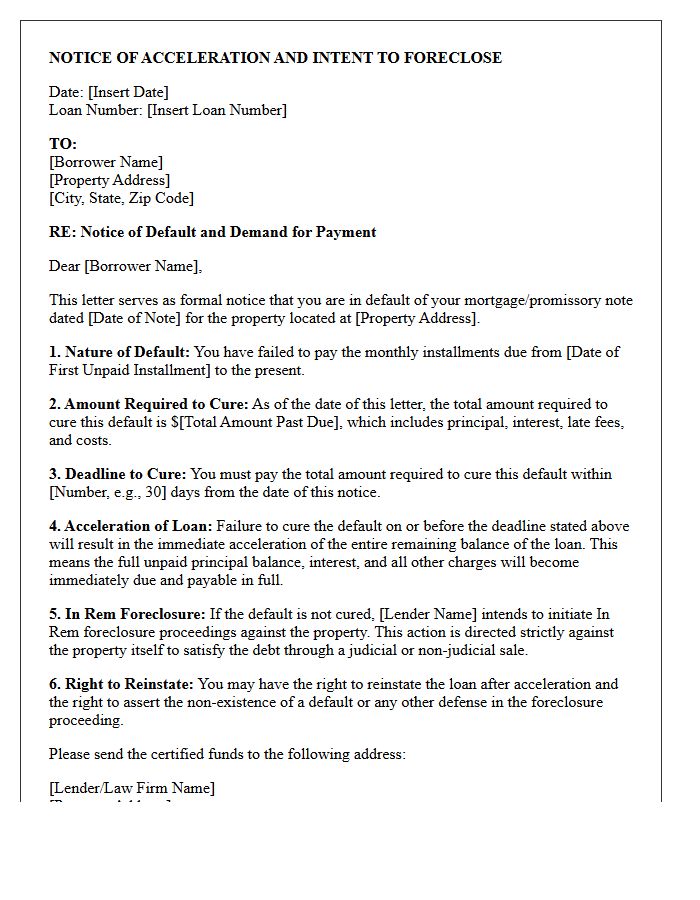

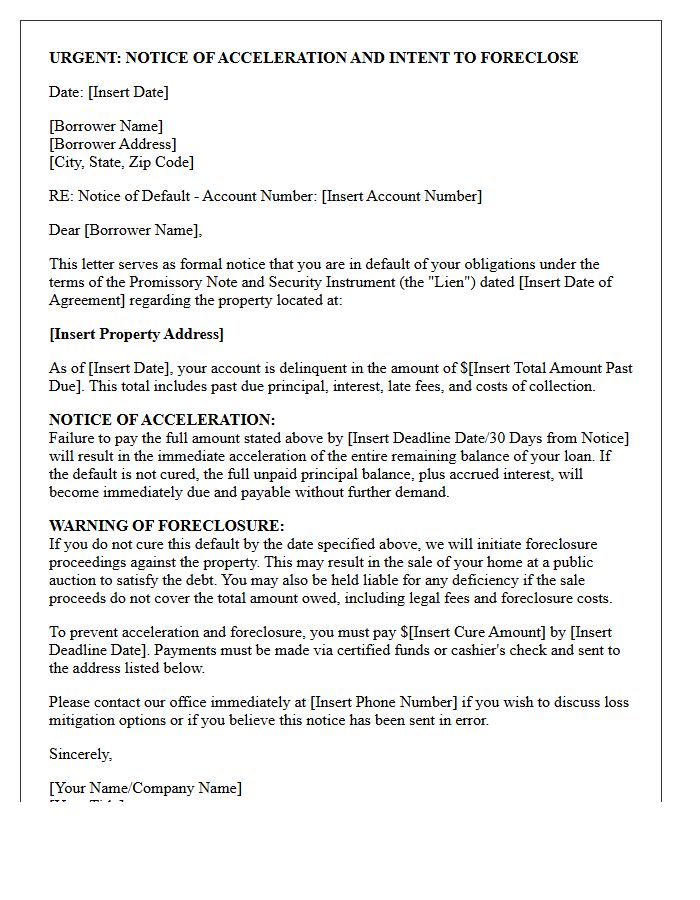

Retained Lien Acceleration and Foreclosure Warning Letter

A Retained Lien Acceleration and Foreclosure Warning Letter is a formal legal notice sent when a borrower defaults on a mortgage. This document officially notifies the homeowner that the lender is accelerating the debt, making the entire loan balance due immediately. It serves as a final demand for payment before the foreclosure process begins. Understanding this letter is critical because it outlines the specific cure date to resolve the delinquency. Failure to act within this timeframe allows the lender to legally seize and sell the property to recover the outstanding balance.

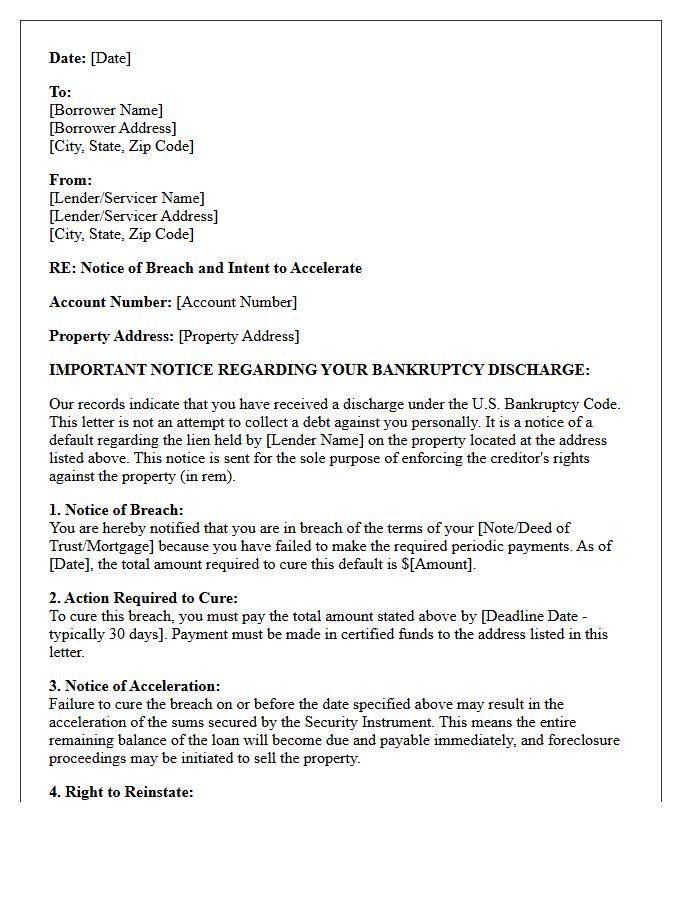

Post-Bankruptcy Discharge Breach and Acceleration Letter

A discharge injunction prevents creditors from collecting debts personally after bankruptcy. However, if a homeowner fails to make payments, the lender may issue an acceleration letter to demand the full mortgage balance before starting foreclosure. If the lender attempts to hold you personally liable for a discharged debt rather than just pursuing the property, they may be in breach of court orders. Documenting these communications is essential to prove a stay violation and protect your legal rights during the recovery process.

Mortgage Maturity Acceleration Post-Discharge Notice Letter

The Mortgage Maturity Acceleration Post-Discharge Notice Letter is a critical document sent by lenders after a borrower receives a Chapter 7 bankruptcy discharge. It serves as formal notification that the acceleration clause has been triggered due to default. While the borrower is no longer personally liable for the debt, the lender retains the right to foreclose on the property to recover the balance. Understanding this notice is essential, as it marks the final step before legal proceedings begin, often serving as the last opportunity to negotiate a loan modification or settlement.

What is a Post-Bankruptcy Discharge Acceleration Notice?

A Post-Bankruptcy Discharge Acceleration Notice is a formal communication from a lender, typically a mortgage servicer, informing the borrower that the full balance of the loan is now due because of a default. While the bankruptcy discharge removes your personal liability for the debt, the notice signifies the lender's intent to proceed with foreclosure against the property to satisfy the lien.

Does receiving an acceleration notice mean I am personally liable for the debt?

No, if the debt was successfully discharged in a Chapter 7 or Chapter 13 bankruptcy, you are no longer personally liable for the deficiency. However, the bankruptcy discharge does not remove the voluntary lien (the mortgage) from the property title. The acceleration notice is a procedural step required for the lender to exercise its right to seize the collateral through foreclosure.

Can a lender send an acceleration notice after a bankruptcy stay is lifted?

Yes. Once the automatic stay is lifted or the bankruptcy case is closed and the discharge is granted, the lender regains the legal right to enforce its security interest in the property. If payments were not reaffirmed or maintained during the bankruptcy process, the lender may issue an acceleration notice as the final step before initiating a foreclosure sale.

What should I do if I receive an acceleration notice after my bankruptcy?

If you wish to keep the property, you must contact your servicer immediately to discuss loss mitigation options, such as a loan modification or a reinstatement. If you intended to surrender the home during bankruptcy, the notice confirms the lender is moving forward with the legal process to take possession of the home, and you should monitor the foreclosure timeline to plan your relocation.

Is an acceleration notice a violation of the bankruptcy discharge injunction?

Generally, it is not a violation as long as the notice is strictly an "in rem" action against the property rather than an "in personam" attempt to collect money from you personally. Most notices include specific "bankruptcy disclaimers" stating that the letter is for informational purposes or property enforcement only and is not an attempt to collect a discharged debt.

Comments