Lenders issue an Uninsured Property Triggered Acceleration Notice when a borrower fails to maintain required insurance coverage. This legal action demands immediate payment of the full loan balance to protect the mortgagee's collateral from risk. Understanding your obligations is essential to avoid foreclosure and secure your investment. To help you respond effectively, below are some ready to use template.

Image cover: Navigating Uninsured Property: Sample Acceleration Notices and Legal Templates

Letter Samples List

- Uninsured Property Triggered Acceleration Notice Letter

- Notice Of Loan Acceleration Letter Due To Uninsured Property

- Mortgage Default And Acceleration Letter For Lapsed Insurance

- Final Acceleration Demand Letter For Uninsured Collateral

- Breach Of Covenant Letter For Uninsured Property Acceleration

- Notice Of Foreclosure Intent Letter Triggered By Uninsured Property

- Immediate Loan Acceleration Letter For Insurance Default

- Lender Notice Letter For Uninsured Property Acceleration

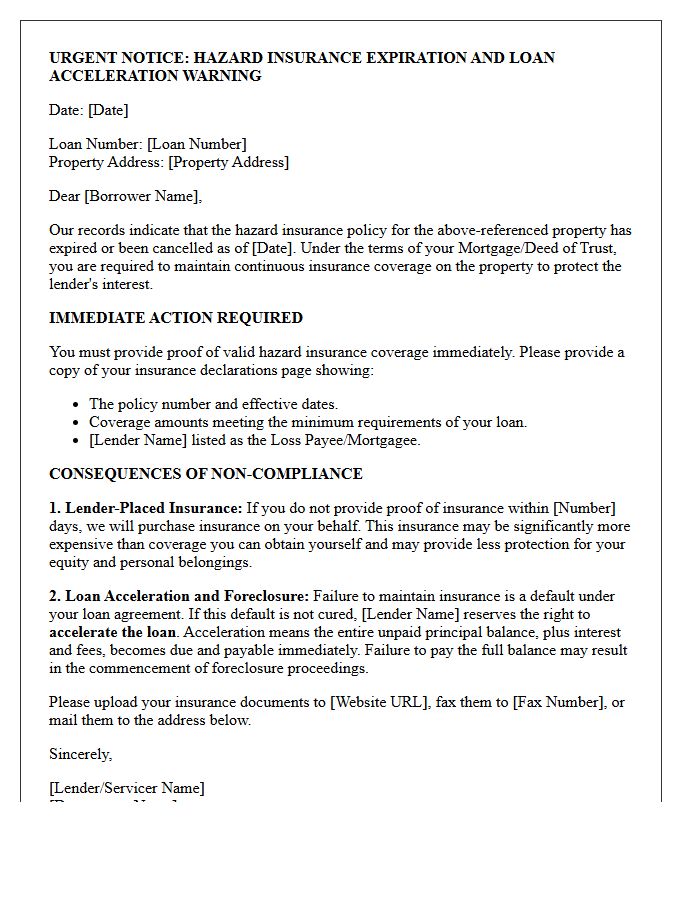

- Hazard Insurance Lapse And Loan Acceleration Warning Letter

- Uninsured Mortgage Asset Acceleration Notification Letter

- Property Insurance Default Acceleration Demand Letter

- Commercial Mortgage Uninsured Property Acceleration Letter

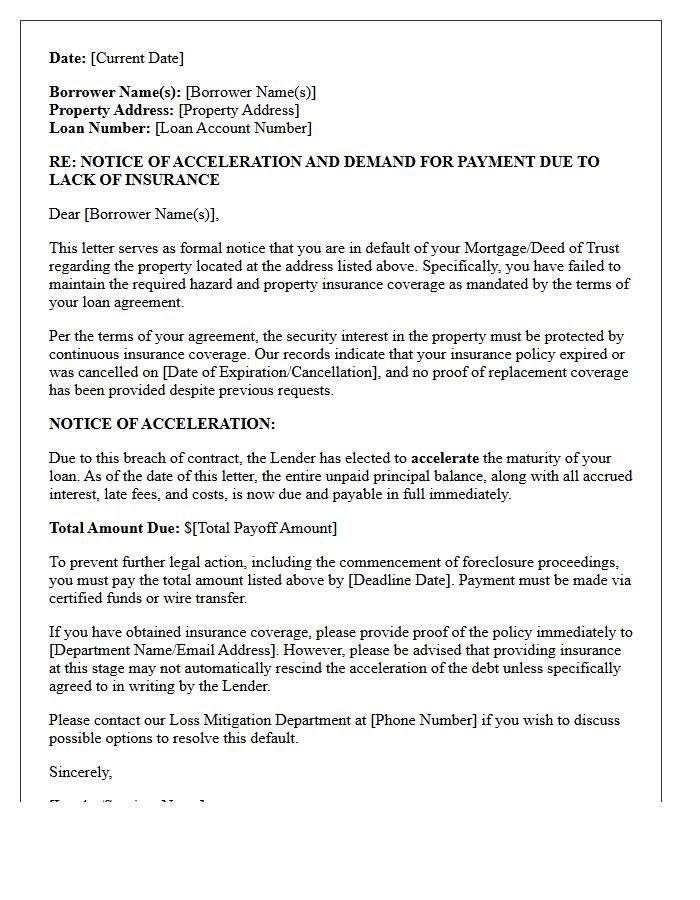

Uninsured Property Triggered Acceleration Notice Letter

An Uninsured Property Triggered Acceleration Notice Letter is a formal legal notification issued by a lender when a borrower fails to maintain required hazard insurance. This breach of the mortgage contract allows the creditor to demand immediate payment of the entire loan balance. To avoid foreclosure, the homeowner must promptly provide proof of coverage or pay the outstanding debt. Receiving this letter indicates a critical risk to property ownership, as it transitions the loan from standard monthly installments to a status of immediate maturity due to lapsed protection.

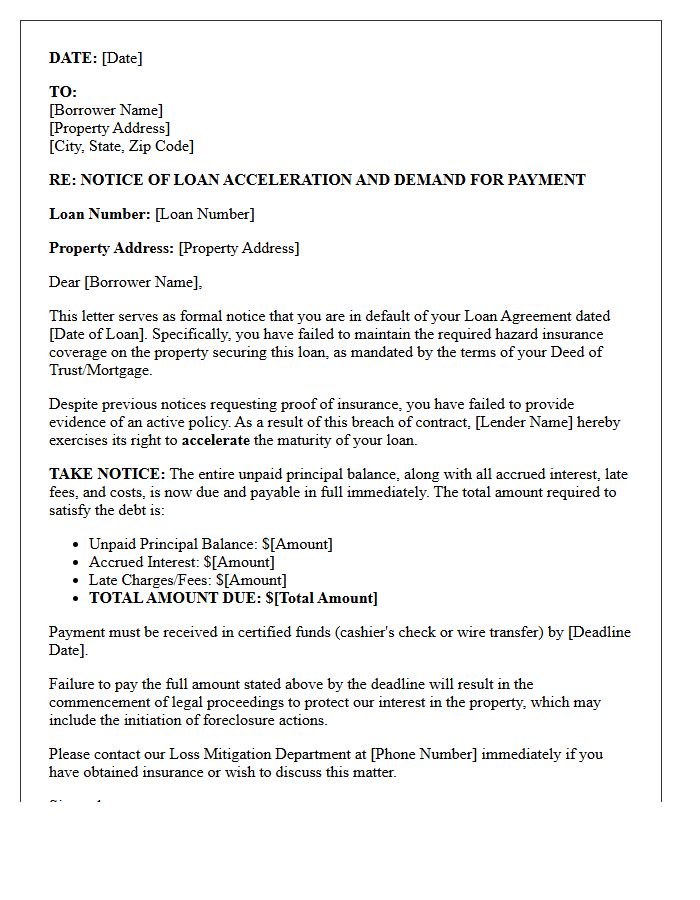

Notice Of Loan Acceleration Letter Due To Uninsured Property

A Notice of Loan Acceleration due to an uninsured property is a critical warning that your mortgage lender is demanding immediate repayment of the entire loan balance. Most loan agreements require continuous hazard insurance to protect the collateral. If coverage lapses, the lender may force-place expensive insurance or declare a default. Receiving this letter means the foreclosure process could begin unless you provide proof of valid insurance or pay the full debt. It is vital to contact your lender immediately to resolve the insurance deficiency and prevent the loss of your home.

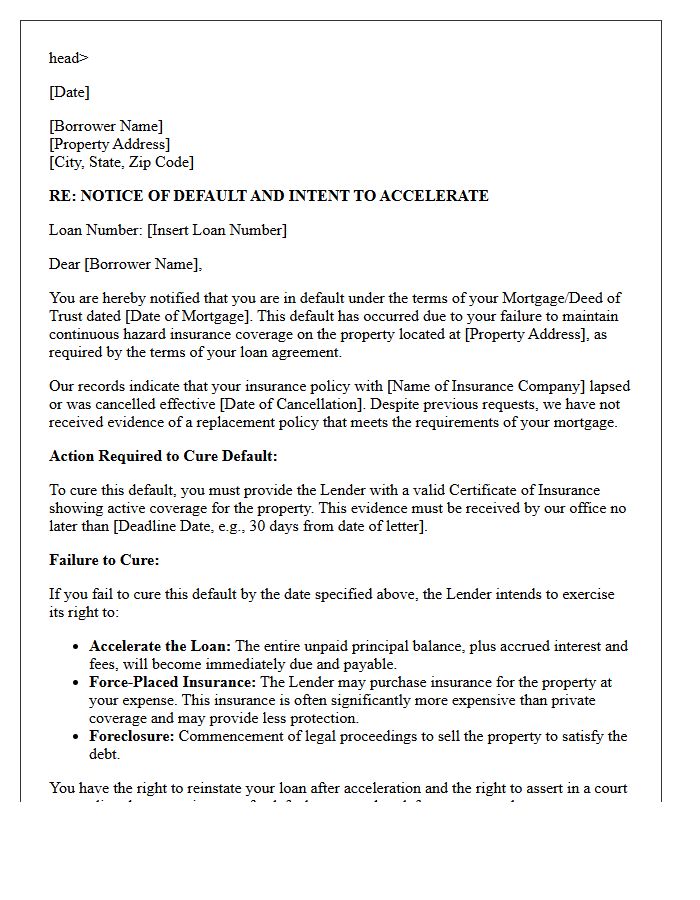

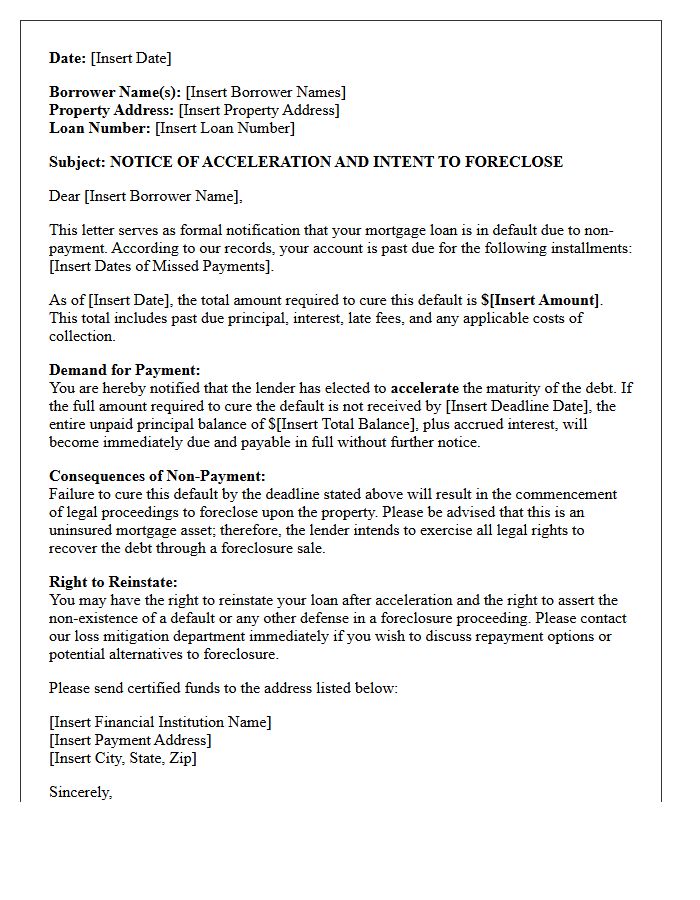

Mortgage Default And Acceleration Letter For Lapsed Insurance

If your property coverage expires, your lender may issue a Mortgage Default And Acceleration Letter. Maintaining active hazard insurance is a mandatory loan covenant. Failure to provide proof of coverage allows the servicer to force-place expensive insurance and demand immediate payment of the entire loan balance. To prevent foreclosure, you must promptly provide valid proof of insurance or pay all outstanding premiums and fees. Acting quickly during this cure period is essential to reinstate your mortgage and protect your home equity from legal action.

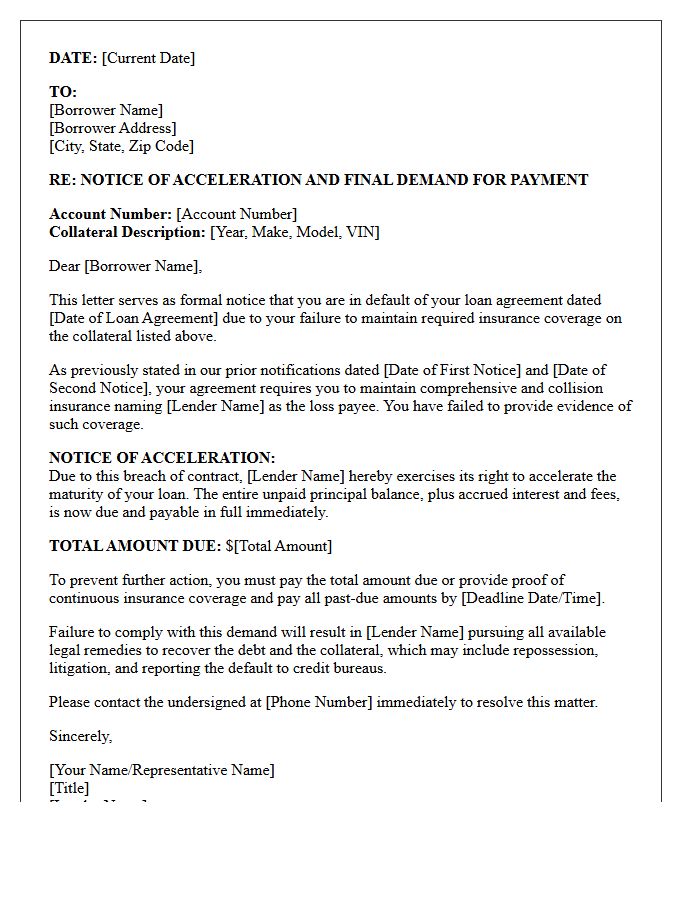

Final Acceleration Demand Letter For Uninsured Collateral

A Final Acceleration Demand Letter is a formal legal notice issued when a borrower fails to maintain required insurance on financed property. This document notifies the debtor that the entire outstanding loan balance is now due immediately. The primary goal is to protect the lender's interest in uninsured collateral that faces potential loss or damage. Failure to respond typically results in repossession or foreclosure actions. Borrowers must provide valid proof of coverage or pay the full balance to prevent the permanent loss of their asset and severe credit damage.

Breach Of Covenant Letter For Uninsured Property Acceleration

A Breach of Covenant Letter for an uninsured property is a formal legal notice issued by a lender when a homeowner fails to maintain required hazard insurance. Since insurance protects the collateral, this violation is a serious default. If the breach is not cured immediately, the lender may exercise the Acceleration clause, demanding the entire mortgage balance be paid at once. To avoid foreclosure, owners must promptly provide proof of coverage or risk the lender implementing expensive force-placed insurance to secure their financial interest in the asset.

Notice Of Foreclosure Intent Letter Triggered By Uninsured Property

Receiving a Notice of Foreclosure Intent due to an uninsured property is a critical legal warning. Lenders require continuous hazard insurance to protect their collateral. If your policy lapses, the bank may implement expensive force-placed insurance or initiate default proceedings. To stop the foreclosure process, you must immediately provide proof of coverage to your servicer. Failing to maintain active insurance violates your mortgage contract, allowing the lender to accelerate the loan. Promptly reinstating a private policy is the most effective way to protect your home equity and legal standing.

Immediate Loan Acceleration Letter For Insurance Default

An Immediate Loan Acceleration Letter for insurance default is a formal notice from a lender demanding full repayment of the remaining mortgage balance. This occurs when a borrower fails to maintain required property insurance, breaching the loan agreement. The lender exercises an acceleration clause, transitioning the debt from monthly installments to an immediate lump sum. To avoid potential foreclosure, the borrower must quickly provide proof of coverage or pay the entire debt. Timely communication and reinstating a valid policy are critical to resolving this contractual default and protecting homeownership.

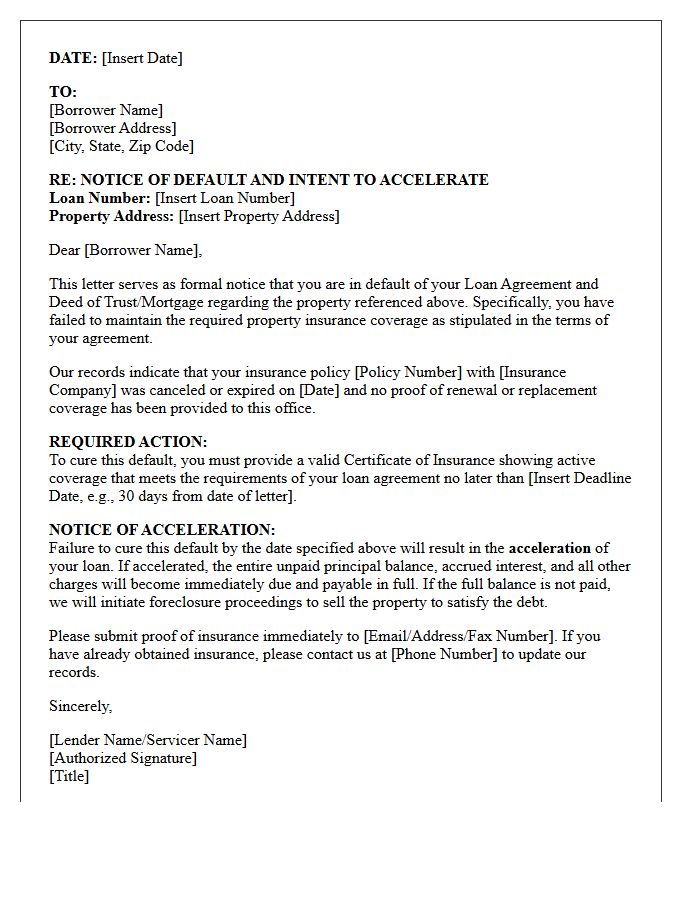

Lender Notice Letter For Uninsured Property Acceleration

A lender notice letter for uninsured property acceleration is a formal warning that your mortgage is in default due to a lapse in hazard insurance. Lenders require continuous coverage to protect their collateral. If you fail to provide proof of insurance, the lender may exercise the acceleration clause, demanding immediate payment of the entire loan balance. To prevent foreclosure, you must quickly provide valid policy details or the lender may implement expensive force-placed insurance to safeguard the asset. Promptly communicating with your servicer is essential to resolve this compliance issue.

Hazard Insurance Lapse And Loan Acceleration Warning Letter

A Hazard Insurance Lapse and Loan Acceleration Warning Letter is a critical legal notice from your mortgage lender. It informs you that your property insurance has expired or been canceled, violating your loan agreement. If you fail to provide proof of coverage immediately, the lender may implement expensive force-placed insurance. More importantly, this breach can trigger loan acceleration, requiring you to pay the entire mortgage balance at once to avoid foreclosure. To protect your home, you must urgently restore your policy and notify your lender to prevent legal action.

Uninsured Mortgage Asset Acceleration Notification Letter

An Uninsured Mortgage Asset Acceleration Notification Letter is a legal warning sent when a borrower defaults on a home loan not covered by default insurance. It signifies that the lender is demanding immediate full payment of the remaining loan balance. Receiving this document indicates the final step before formal foreclosure proceedings begin. To prevent loss of property, homeowners must quickly address the delinquency by paying the total arrears or negotiating a reinstatement plan. Ignoring this notice typically leads to the loss of legal rights to the asset and immediate foreclosure action.

Property Insurance Default Acceleration Demand Letter

A Property Insurance Default Acceleration Demand Letter is a formal legal notice sent when a policyholder fails to maintain required coverage. This document warns that the full loan balance may be accelerated, meaning the entire mortgage becomes due immediately. To avoid foreclosure, the borrower must provide proof of insurance or pay for force-placed coverage obtained by the lender. Timely compliance is critical to prevent the foreclosure process from initiating, as maintaining valid hazard insurance is a fundamental requirement of most mortgage contracts and security instruments.

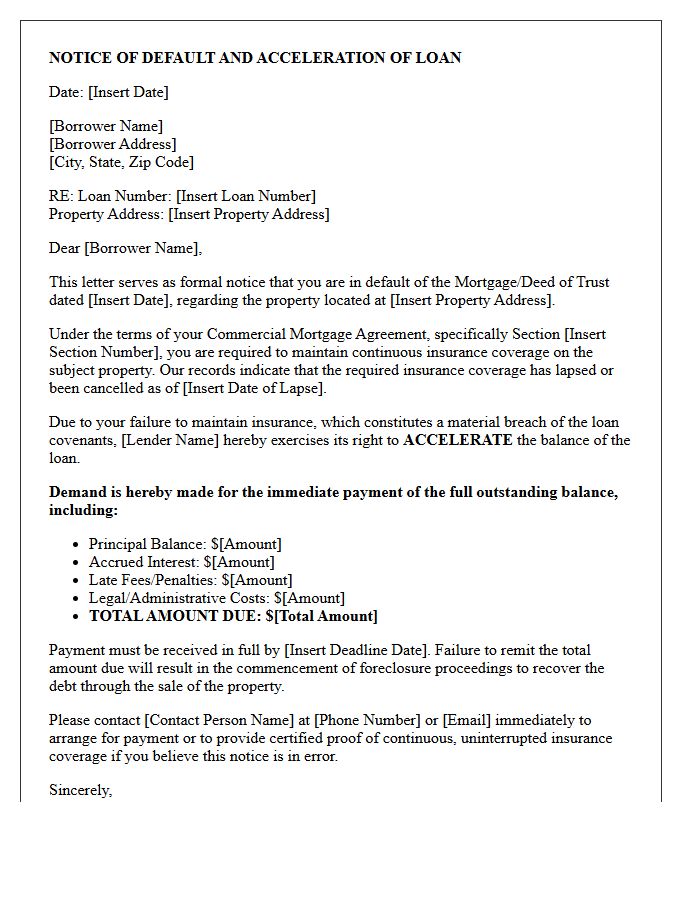

Commercial Mortgage Uninsured Property Acceleration Letter

A Commercial Mortgage Uninsured Property Acceleration Letter is a formal legal notice issued when a borrower fails to maintain required insurance coverage. This default allows the lender to trigger an acceleration clause, demanding immediate full repayment of the outstanding loan balance. Since the collateral is unprotected, the lender views the risk as critical. Receiving this letter is a final warning before foreclosure proceedings begin. To resolve the issue, borrowers must immediately provide proof of valid insurance or negotiate a reinstatement to prevent total loss of the property.

What is an Uninsured Property Triggered Acceleration Notice?

An Uninsured Property Triggered Acceleration Notice is a formal legal notification from a mortgage lender stating that the full loan balance is due immediately because the borrower has failed to maintain required hazard or homeowners insurance on the property.

Can a lender call a loan due if the insurance policy lapses?

Yes, most standard mortgage contracts include a "covenant to insure" clause. If the property becomes uninsured, it poses a significant risk to the lender's collateral, allowing them to trigger the acceleration clause and demand full payment of the debt.

What happens after receiving an acceleration notice for lack of insurance?

Once the notice is issued, the borrower typically has a strictly defined cure period to provide proof of valid insurance. Failure to reinstate coverage or pay the full loan balance may result in the lender initiating foreclosure proceedings.

How can I stop a mortgage acceleration triggered by an insurance lapse?

To stop the acceleration, you must immediately obtain a valid insurance policy that meets the lender's requirements and provide the Declarations Page as proof. You should also contact the lender's loss mitigation department to confirm receipt and ensure the acceleration status is rescinded.

What is "force-placed insurance" in the context of an acceleration notice?

Force-placed insurance is a policy a lender purchases on your behalf when your coverage lapses. While it may temporarily satisfy the insurance requirement, it is often significantly more expensive and provides less coverage than private insurance, and its implementation does not always prevent a lender from issuing an acceleration notice if the loan is already in default.

Comments