Lenders and property managers must issue an Adverse Action Letter when an applicant is rejected due to unverifiable income. This formal notice ensures legal compliance under the Fair Credit Reporting Act by clearly explaining why the financial documentation provided did not meet verification standards. To help you maintain professional and legal transparency, below are some ready to use template.

Image cover: Professional Adverse Action Notice Templates for Unverifiable Income

Letter Samples List

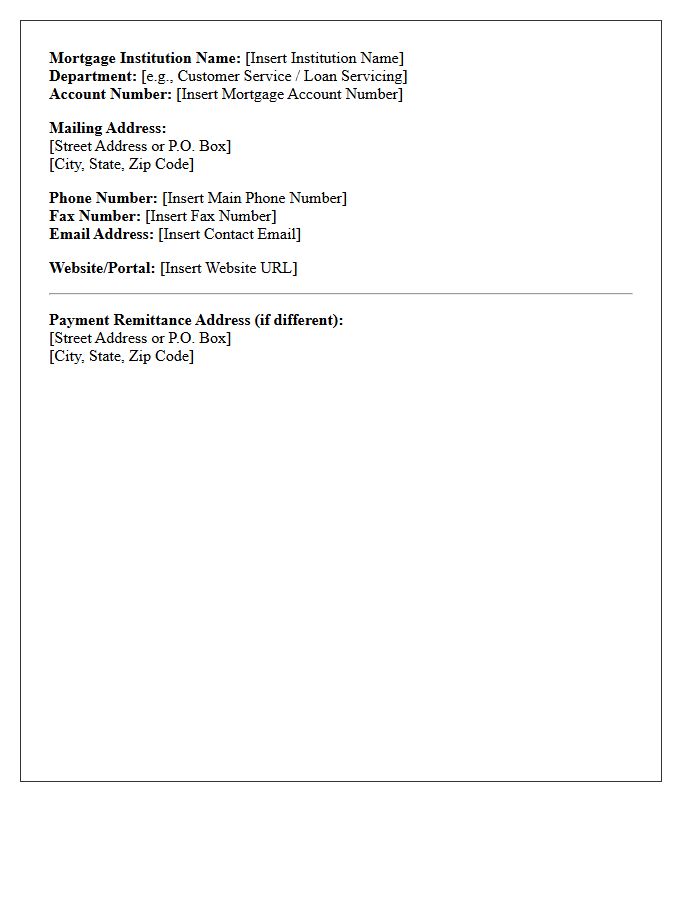

- Mortgage Institution Name and Contact Information

- Date of the Adverse Action Letter Issuance

- Primary Applicant Name and Mailing Address

- Subject Regarding Mortgage Loan Application Status

- Official Adverse Action Letter for Unverifiable Income

- Details of the Requested Mortgage Loan Amount

- Principal Reason for Mortgage Denial

- Specific Explanation Regarding Unverifiable Income Sources

- Disclosure Regarding Consumer Reporting Agency Information

- Consumer Rights Under the Equal Credit Opportunity Act

- Instructions for Appealing the Mortgage Decision

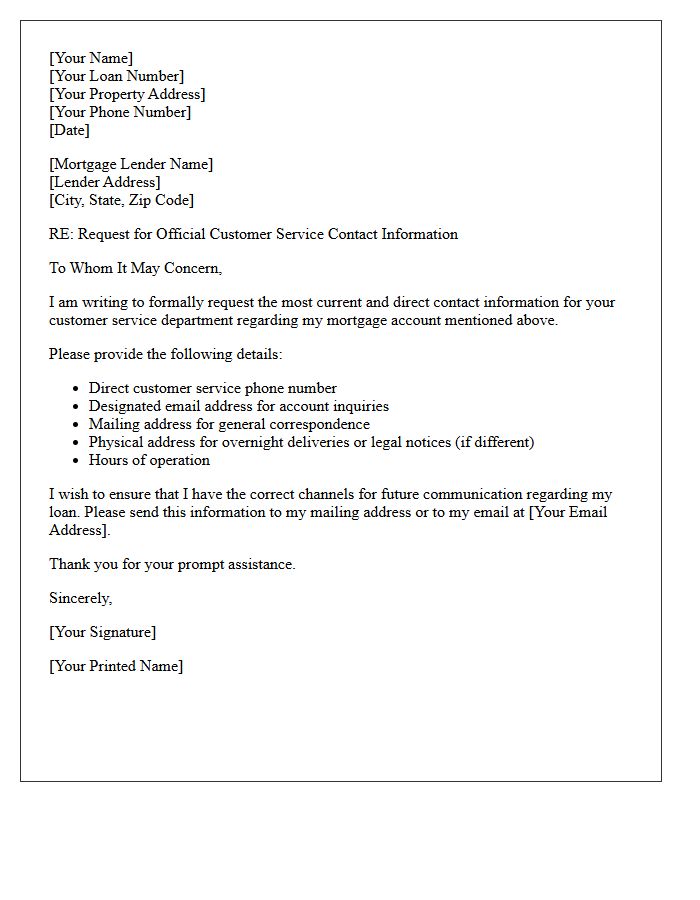

- Mortgage Lender Customer Service Contact Information

- Authorized Signature of the Mortgage Underwriter

Mortgage Institution Name and Contact Information

When managing your home loan, the most critical details are your Mortgage Institution Name and current contact information. This entity, often called the loan servicer, handles your monthly payments, escrow accounts, and tax reporting. Always verify their official website and customer service department phone number to ensure secure communication. Keeping these records accessible allows you to address payment issues, request payoff statements, or discuss refinancing options. Always confirm the mailing address for payments to avoid processing delays or late fees that could impact your credit score.

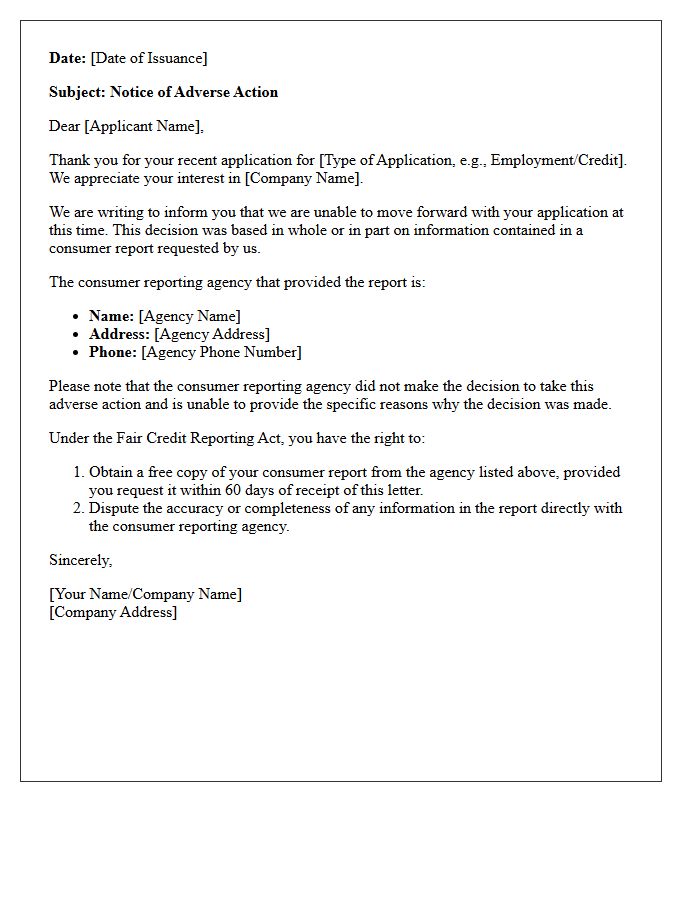

Date of the Adverse Action Letter Issuance

The issuance date of an adverse action letter is critical because it triggers the legal timeline for consumer rights. Under the FCRA and ECOA, creditors must provide this notice within 30 days of a credit decision. For consumers, this date marks the beginning of the 60-day window to request a free copy of their credit report used in the evaluation. Ensuring the date is accurate protects the lender's regulatory compliance while informing the applicant exactly when their notification period and dispute rights officially commenced.

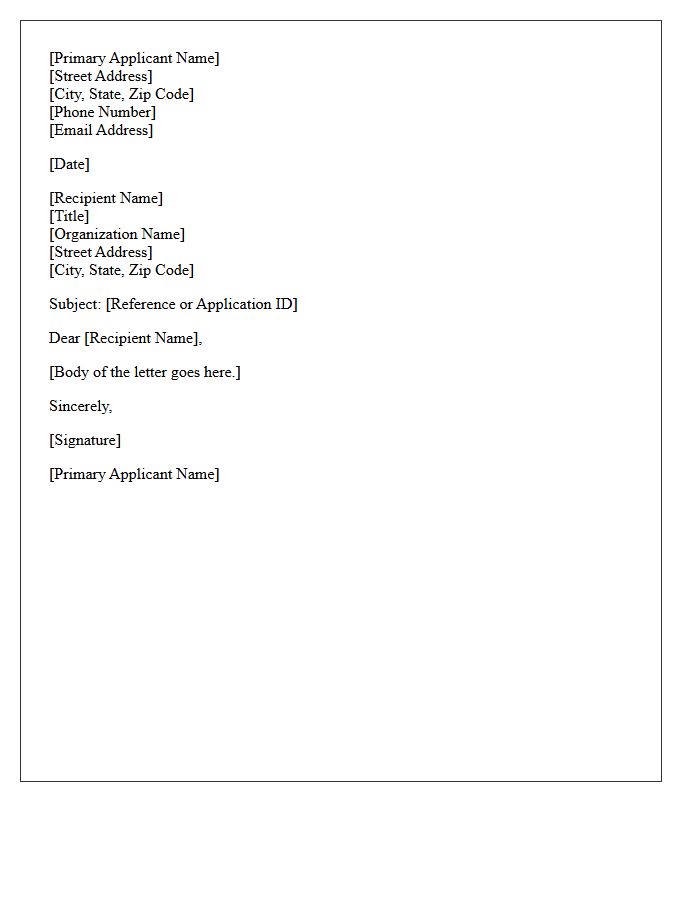

Primary Applicant Name and Mailing Address

The Primary Applicant Name must exactly match your official government identification to ensure legal validity. This individual acts as the main point of contact and bears legal responsibility for the submission. Accurate entry of the Mailing Address is crucial, as it serves as the destination for all formal correspondence, notifications, and physical documents. Always verify the ZIP code and apartment numbers to prevent delivery failures. Consistent information across all forms avoids processing delays and identity verification issues during the evaluation period.

Subject Regarding Mortgage Loan Application Status

Monitoring your mortgage loan application status is essential for a timely closing. Lenders provide updates through various stages, including pre-approval, processing, and underwriting. Staying informed helps you address additional documentation requests immediately, preventing delays in funding. Frequent communication with your loan officer ensures you understand every milestone reached. Always keep a close eye on your approval status to ensure your financial credentials remain stable until the final signing. Proper oversight of these updates is the most effective way to secure your new home without unexpected complications.

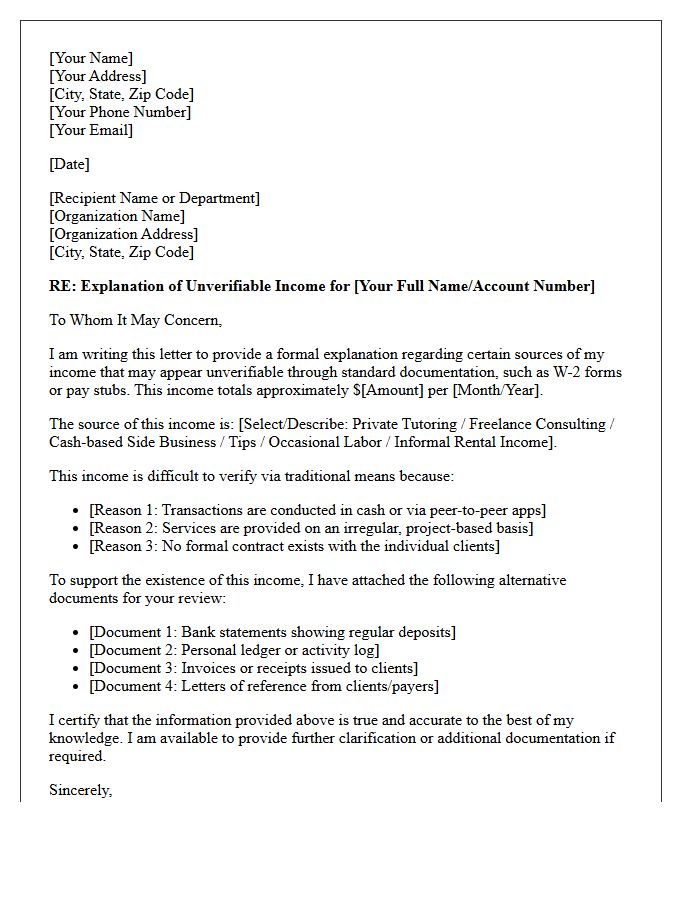

Official Adverse Action Letter for Unverifiable Income

An official adverse action letter for unverifiable income is a mandatory legal notice sent when a creditor denies an application due to an inability to confirm earnings. Under the Equal Credit Opportunity Act, lenders must provide specific reasons for the rejection. This document protects consumers by ensuring transparency and fair lending practices. It typically outlines the applicant's right to request a detailed statement of reasons and provides contact information for the Consumer Financial Protection Bureau to address potential disputes or reporting inaccuracies during the verification process.

Details of the Requested Mortgage Loan Amount

When determining your mortgage loan amount, it is crucial to understand that the total reflects the purchase price minus your down payment. Lenders assess this figure against your debt-to-income ratio and the property's appraised value. The requested sum directly influences your monthly installments and the total interest paid over time. Borrowers must ensure the amount aligns with their financial capacity to maintain long-term affordability while securing favorable interest rates through a lower loan-to-value percentage.

Principal Reason for Mortgage Denial

The debt-to-income ratio (DTI) is the primary reason for mortgage denial. Lenders evaluate your monthly gross income against recurring debts to ensure financial stability. A high DTI suggests you may struggle with additional loan payments. Other significant factors include a low credit score, insufficient down payment funds, or unstable employment history. Maintaining a balanced budget and improving your creditworthiness are essential steps to securing home financing approval and achieving long-term affordability.

Specific Explanation Regarding Unverifiable Income Sources

Lenders often struggle to approve applications involving unverifiable income sources because they lack official documentation like tax returns or paystubs. Common examples include cash tips, informal side gigs, or unrecorded private payments. To qualify for financing, borrowers must provide alternative evidence, such as consistent bank statements or detailed ledgers. Without a clear paper trail, financial institutions cannot accurately assess debt-to-income ratios or repayment capacity. Maintaining transparent records is essential for converting irregular earnings into recognized, stable income for mortgage or loan approvals.

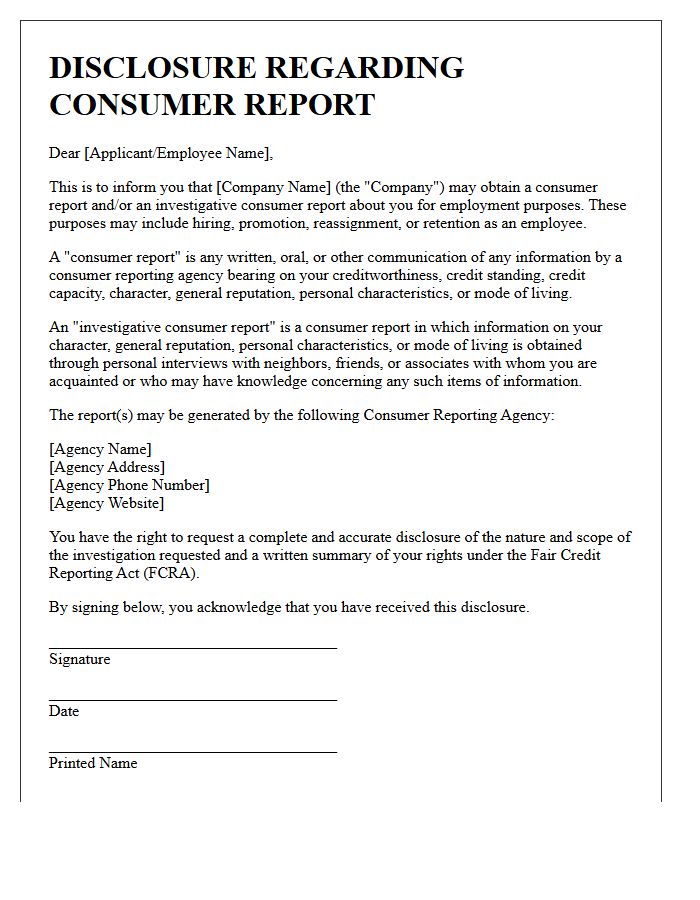

Disclosure Regarding Consumer Reporting Agency Information

A Disclosure Regarding Consumer Reporting Agency Information is a legally required notification informing you that a background check may be conducted for employment or credit purposes. Under the Fair Credit Reporting Act (FCRA), organizations must provide this as a standalone document before obtaining your report. It ensures transparency by alerting you that your personal history, including criminal records or financial data, will be evaluated. You have the right to know which agency provides the data and to dispute inaccuracies to protect your consumer rights and privacy.

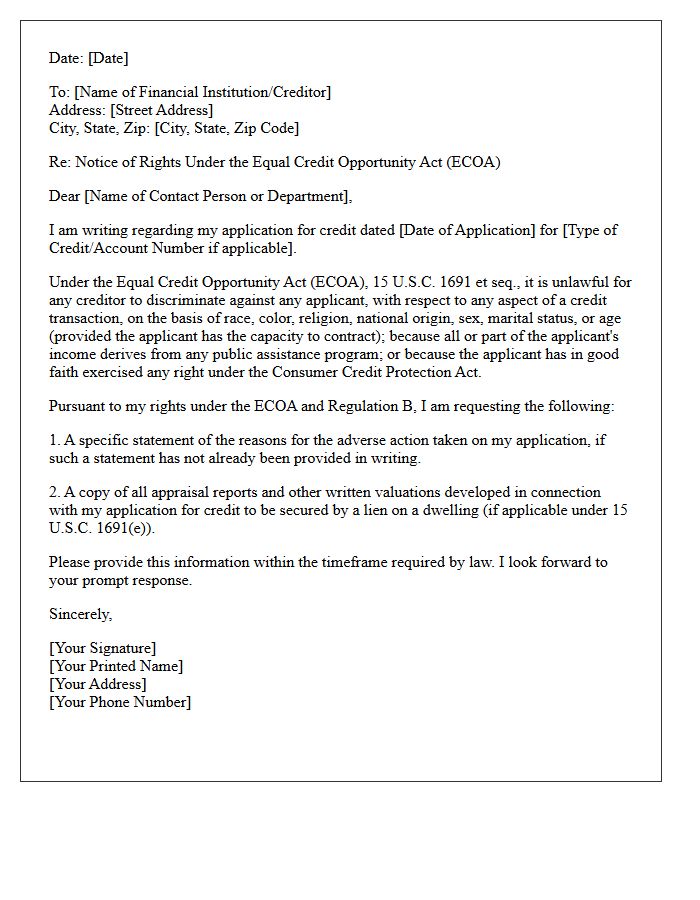

Consumer Rights Under the Equal Credit Opportunity Act

The Equal Credit Opportunity Act (ECOA) ensures fairness by prohibiting lenders from discriminating based on race, religion, national origin, sex, marital status, or age. It guarantees your right to a statement of reasons if your credit application is denied or unfavorable terms are offered. Lenders must evaluate you solely on creditworthiness and income stability. If you face a credit denial, the law mandates notification within 30 days. Understanding these protections helps you challenge bias and promotes equitable access to loans, mortgages, and credit cards in the financial marketplace.

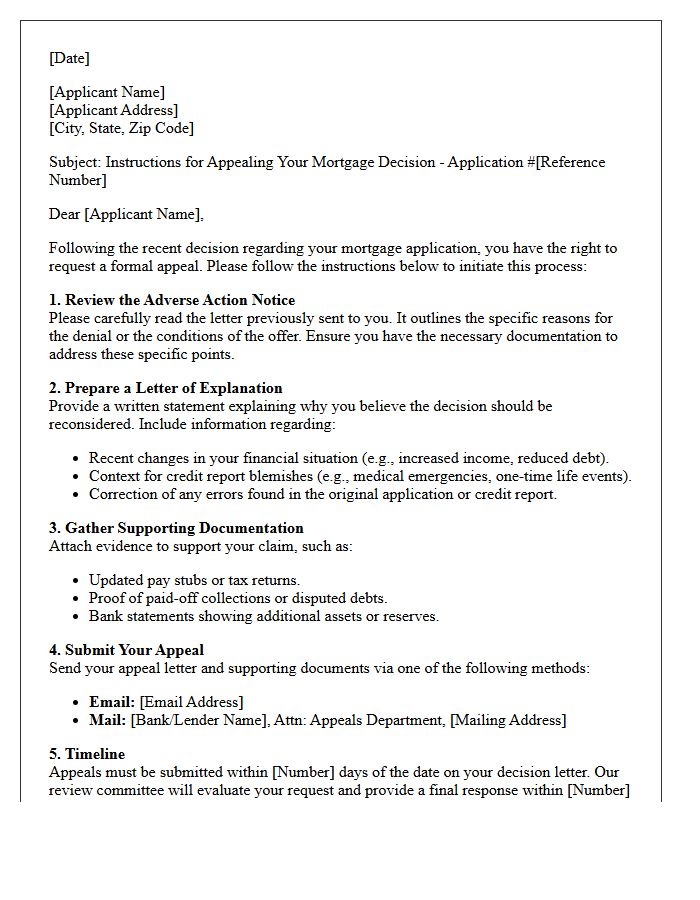

Instructions for Appealing the Mortgage Decision

To challenge a loan rejection, you must first request an Adverse Action Notice from your lender. This document explains the specific reasons for denial, such as low credit scores or high debt-to-income ratios. Review your credit report for inaccuracies and file formal disputes if errors exist. Prepare a detailed rebuttal letter addressing each concern with supporting financial evidence, such as proof of income or assets. Timely action is essential; most lenders have a strict window for reconsidering an application. Persistent documentation is the key to successfully overturning a negative mortgage decision.

Mortgage Lender Customer Service Contact Information

Finding your mortgage lender's contact information is essential for managing your home loan effectively. Most institutions provide customer service details on your monthly billing statement or through their official mobile app. You should keep their phone number and online portal login accessible to discuss payment options, escrow adjustments, or payoff quotes. If you encounter financial difficulties, contacting their loss mitigation department immediately is the most important step to explore assistance programs and avoid delinquency. Always verify contact details directly through the lender's verified website to prevent potential phishing scams.

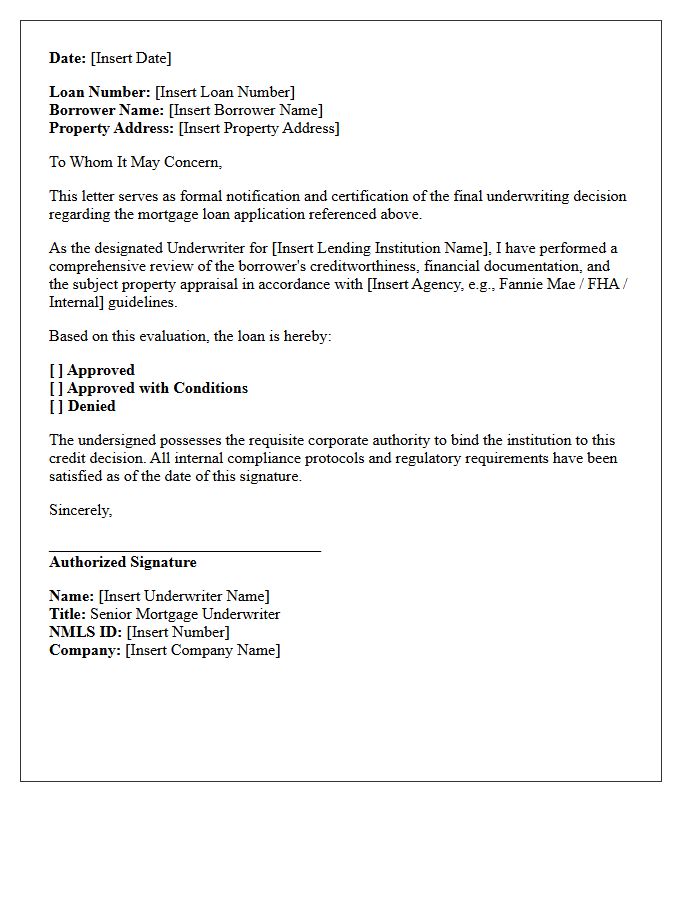

Authorized Signature of the Mortgage Underwriter

The Authorized Signature of a mortgage underwriter represents the final formal approval of a home loan application. This endorsement signifies that the underwriter has meticulously verified the borrower's financial documentation, creditworthiness, and collateral value against specific lending guidelines. It acts as a binding legal validation, confirming that the risk level is acceptable for the financial institution. Without this specific authorization, the mortgage cannot proceed to the closing stage, making it the most critical step in securing funding for a property purchase.

What is an adverse action letter for unverifiable income?

An adverse action letter for unverifiable income is a formal notification sent to a loan or rental applicant stating that their application was denied because the provided proof of earnings could not be authenticated or did not meet the lender's verification standards.

Why did I receive an adverse action notice for income verification?

You received this notice because the creditor or landlord was unable to confirm your stated income through third-party sources, tax transcripts, or employer contact, or the documents provided (such as pay stubs or bank statements) were deemed insufficient or inconsistent.

Does a denial for unverifiable income affect my credit score?

No, receiving an adverse action letter does not directly impact your credit score. However, the hard inquiry performed during the application process may cause a temporary, minor dip in your credit rating.

Can I dispute a denial based on unverifiable income?

Yes. If you believe your income was verified incorrectly, you should contact the lender immediately to provide additional documentation, such as certified tax returns, 1099 forms, or a letter from your CPA to substantiate your earnings.

What information must be included in an adverse action letter regarding income?

Under the Equal Credit Opportunity Act (ECOA), the letter must include the specific reason for denial (unverifiable income), the name and address of the credit reporting agency used, and a statement of the applicant's right to obtain a free copy of their credit report.

Comments