A Conditional Approval Pending Sale of Current Residence Letter is a formal document issued by lenders to homebuyers. It confirms mortgage approval contingent upon the successful closing of the buyer's existing property. This letter helps sellers evaluate offer risks while securing financing for your next move. If you need to draft one, below are some ready to use templates.

Image cover: Mastering the Home Sale Contingency: Templates and Guide for Conditional Approval Letters

Letter Samples List

- Standard Conditional Approval Pending Sale of Current Residence Letter

- Preliminary Mortgage Conditional Approval Pending Sale of Current Residence Letter

- Contingent Home Loan Approval Pending Sale of Current Residence Letter

- Purchase Mortgage Conditional Approval Pending Sale of Current Residence Letter

- Underwriting Conditional Approval Pending Sale of Current Residence Letter

- Time-Sensitive Conditional Approval Pending Sale of Current Residence Letter

- Conventional Loan Conditional Approval Pending Sale of Current Residence Letter

- Government Backed Mortgage Conditional Approval Pending Sale of Current Residence Letter

- Veterans Affairs Loan Conditional Approval Pending Sale of Current Residence Letter

- Jumbo Mortgage Conditional Approval Pending Sale of Current Residence Letter

- Relocation Conditional Approval Pending Sale of Current Residence Letter

- Portfolio Loan Conditional Approval Pending Sale of Current Residence Letter

- Bridge Financing Conditional Approval Pending Sale of Current Residence Letter

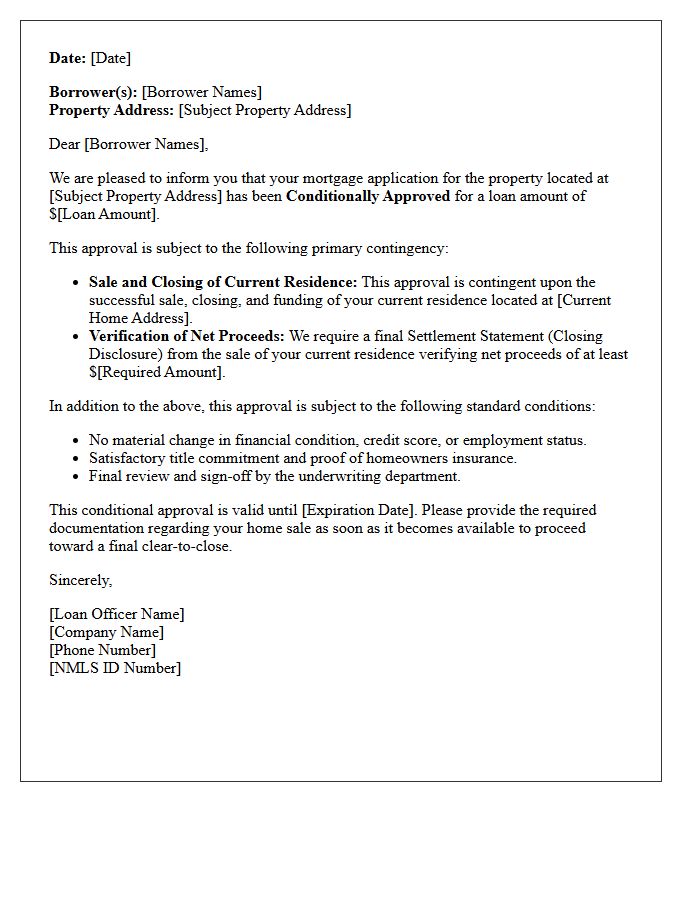

Standard Conditional Approval Pending Sale of Current Residence Letter

A Conditional Approval Letter pending the sale of a current residence is a critical document in real estate. It confirms a lender will provide financing only after the borrower successfully settles their existing home's equity and debt. This contingency protects the lender from high debt-to-income ratios. For sellers, this letter indicates a qualified buyer, though it carries more risk than a non-contingent offer. Understanding this contingency is essential for managing closing timelines and ensuring a seamless transition between properties during a synchronized real estate transaction.

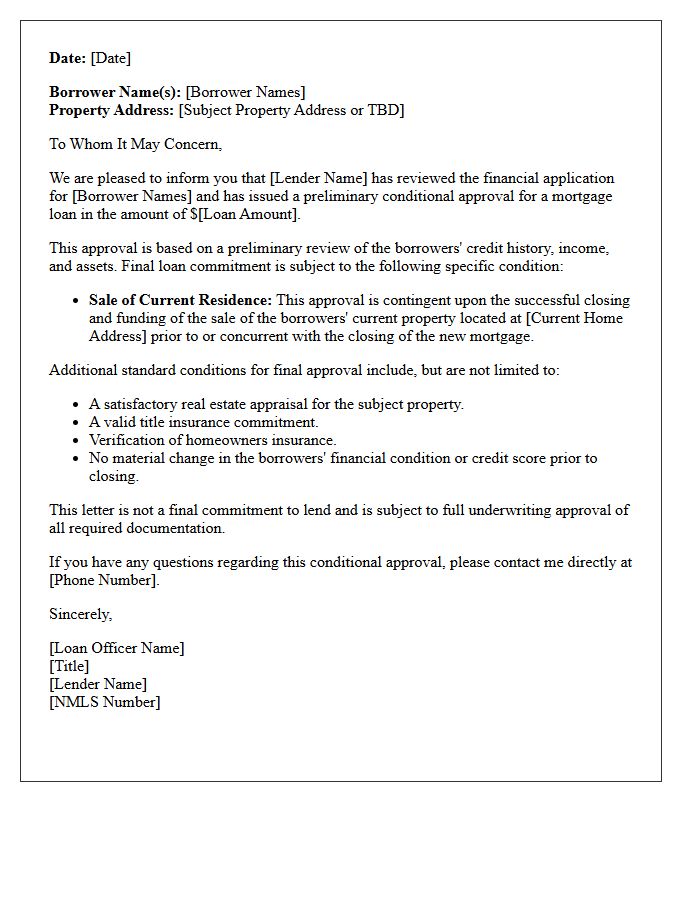

Preliminary Mortgage Conditional Approval Pending Sale of Current Residence Letter

A Preliminary Mortgage Conditional Approval Pending Sale of Current Residence Letter is a lender's commitment to finance your new home, provided you first finalize the sale of your existing property. This document proves your creditworthiness while protecting the lender from the risk of carrying two mortgages simultaneously. It is essential for buyers who need home equity for a down payment. Having this letter strengthens your negotiating position with sellers by demonstrating that your financing is secured, contingent only upon closing your current real estate transaction.

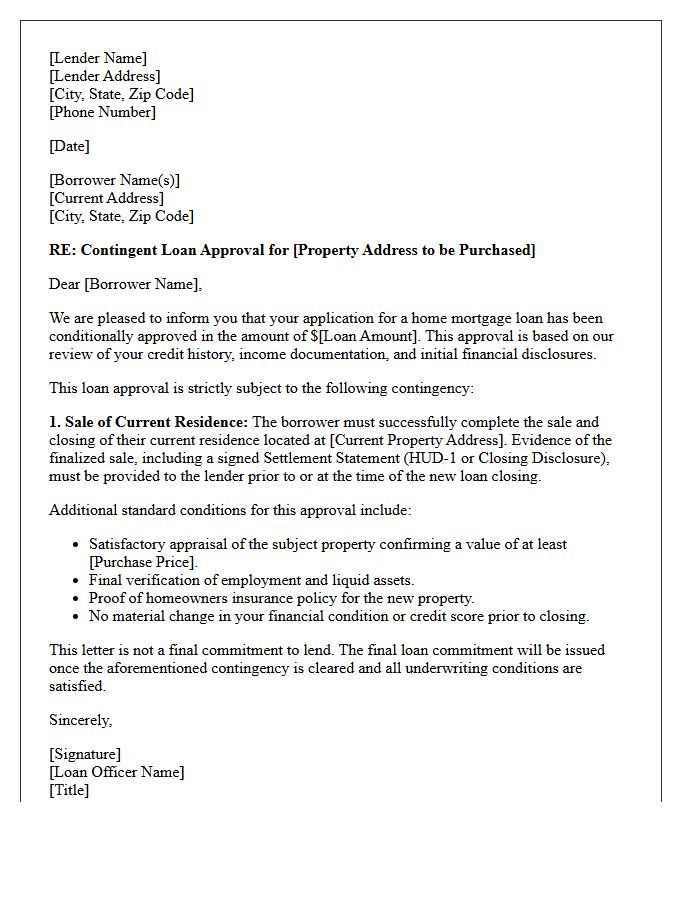

Contingent Home Loan Approval Pending Sale of Current Residence Letter

A Contingent Home Loan Approval letter confirms a lender will finance your new property provided your current residence sells first. This document is essential for buyers who rely on existing equity to fund a down payment or meet debt-to-income requirements. It signals to sellers that you are financially qualified, though the purchase remains dependent on your successful closing. Understanding this contingency is vital, as it protects your earnest money while informing the seller of potential timing risks associated with your pending home sale.

Purchase Mortgage Conditional Approval Pending Sale of Current Residence Letter

A Conditional Approval Letter pending the sale of your current residence is a mortgage commitment contingent on your existing home equity. This document proves you are qualified for a new loan once your current property closes. It is essential for buyers who need proceeds from a sale to cover the down payment or debt-to-income requirements. Sellers view this as a risk, so providing a signed sales contract for your old home strengthens your offer by showing the contingency is near completion, ensuring a smoother transition to your new mortgage.

Underwriting Conditional Approval Pending Sale of Current Residence Letter

An Underwriting Conditional Approval Pending Sale of Current Residence Letter is a formal document issued by a lender. It states that your new mortgage is approved, provided you successfully close the sale of your existing home first. This condition ensures you have the necessary equity for a down payment and eliminates the risk of carrying two concurrent monthly payments. It protects the lender's debt-to-income ratio requirements. Once your current residence is officially sold and verified, the lender will clear the contingency to finalize your new loan funding.

Time-Sensitive Conditional Approval Pending Sale of Current Residence Letter

A Time-Sensitive Conditional Approval indicates a lender will fund your loan only after your current residence is sold. This document is critical in competitive markets because it includes a "kick-out clause," allowing sellers to accept other offers if you cannot fulfill the contingency quickly. It proves financial backing while highlighting the sale dependency risk. Buyers must act fast to finalize their existing home sale to secure the new property, as this approval expires once the stipulated deadline passes without a successful closing.

Conventional Loan Conditional Approval Pending Sale of Current Residence Letter

A conditional approval pending the sale of a current residence means your lender has verified your credit and income but requires a settlement statement (HUD-1) from your existing home before finalizing the new mortgage. This contingency ensures your debt-to-income ratio remains stable by eliminating the previous housing payment. To avoid delays, provide a signed sales contract for your current property early. This letter proves you are a qualified buyer, provided your home equity is unlocked and existing debt is cleared prior to the new closing date.

Government Backed Mortgage Conditional Approval Pending Sale of Current Residence Letter

A Conditional Approval Pending Sale letter signifies that a lender will finance your new government-backed mortgage only after your current home sells. This document ensures the borrower meets debt-to-income ratios by eliminating the existing housing liability. It is a critical piece of mortgage financing that proves to sellers you are qualified, provided your equity is liquidated. Understanding this condition is essential for contingent offers, as it bridges the transition between properties while maintaining strict federal lending guidelines and financial stability during the home-buying process.

Veterans Affairs Loan Conditional Approval Pending Sale of Current Residence Letter

A VA Loan Conditional Approval letter signifies that a lender will finance your new home once your current residence is sold. This document ensures you meet credit and income standards, but the final funding depends on eliminating the existing mortgage debt to satisfy debt-to-income (DTI) ratios. Providing a signed sales contract for your old property is typically required to clear this contingency. This letter strengthens your offer to sellers by proving you are a qualified buyer awaiting only the equity or debt relief from your pending sale.

Jumbo Mortgage Conditional Approval Pending Sale of Current Residence Letter

A Jumbo Mortgage Conditional Approval Pending Sale of Current Residence Letter is a lender's commitment to finance a high-value home, provided your existing property sells first. This document is crucial for high-net-worth buyers who need equity from their current home to meet strict debt-to-income (DTI) ratios or down payment requirements. It signals to sellers that your financing is secure, contingent only on the successful closing of your current residence. Obtaining this letter strengthens your offer in competitive luxury markets by demonstrating financial transparency and mortgage eligibility despite temporary liquidity constraints.

Relocation Conditional Approval Pending Sale of Current Residence Letter

A Relocation Conditional Approval Pending Sale of Current Residence Letter is a formal document issued by a lender during the mortgage process. It confirms that a homebuyer is approved for a new loan, provided they successfully close the sale of their existing property first. This contingency protects lenders by ensuring the borrower has sufficient equity and meets debt-to-income requirements. For sellers, receiving an offer with this letter indicates a serious buyer, though it introduces a timing dependency on a secondary real estate transaction to finalize the funding.

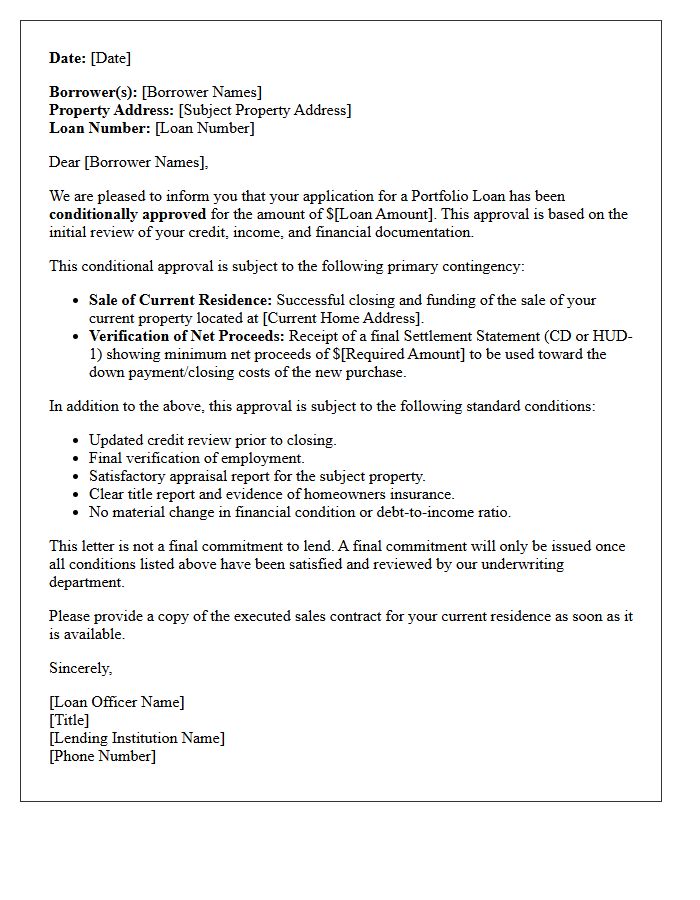

Portfolio Loan Conditional Approval Pending Sale of Current Residence Letter

A Portfolio Loan Conditional Approval Pending Sale of Current Residence Letter is a formal document issued by a lender. It confirms a borrower is qualified for a new mortgage, contingent upon the successful closing and sale of their existing home. This letter is crucial for buyers who need the home equity from their current property to fund the down payment or satisfy debt-to-income requirements. It reassures sellers that the financing is secure, provided the buyer's prior residence sells, effectively managing the financial transition between two properties under specialized portfolio lending guidelines.

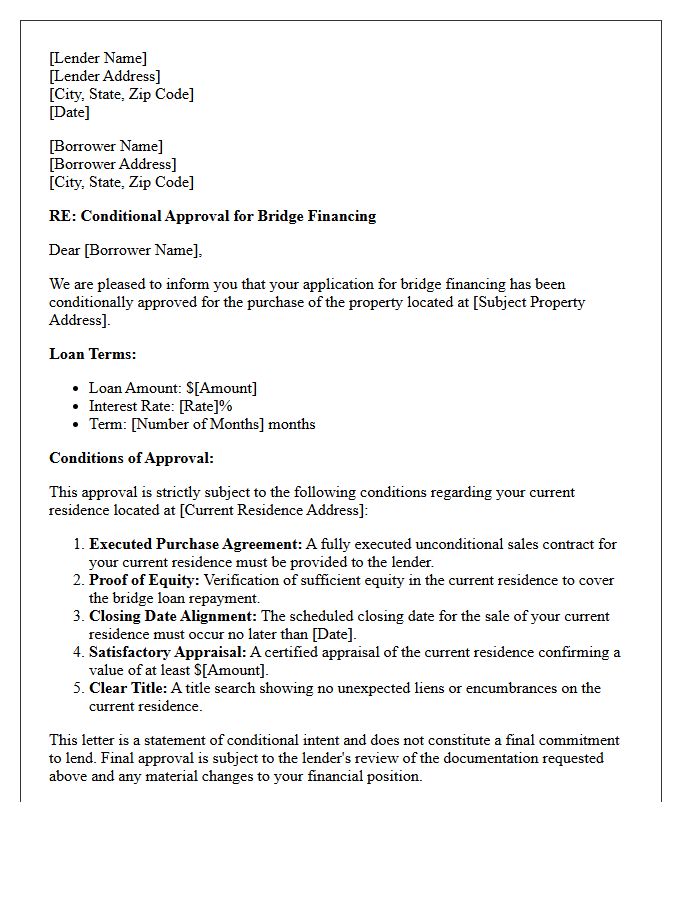

Bridge Financing Conditional Approval Pending Sale of Current Residence Letter

A bridge financing conditional approval pending sale of current residence letter is a temporary funding document used by homeowners to bridge the gap between two properties. It confirms a lender's willingness to provide short-term capital to purchase a new home before the existing one is sold. The most critical requirement is providing a binding purchase agreement for the current residence to mitigate risk. This letter serves as proof to sellers that you possess the financial capacity to close the transaction despite having equity locked in your unsold property.

What is a Conditional Approval Pending Sale of Current Residence Letter?

This is a formal document issued by a lender stating that a borrower is approved for a new mortgage on the condition that their current home is sold and closed before the new loan is finalized. It ensures the borrower has the necessary liquidity and debt-to-income ratio to support the new mortgage payments.

Why do lenders require a home sale contingency for mortgage approval?

Lenders require this contingency to mitigate financial risk. If a borrower carries two mortgages simultaneously, their debt-to-income (DTI) ratio may exceed allowable limits, increasing the likelihood of default. The letter confirms the new loan is only valid once the existing debt is liquidated.

What information is included in a Conditional Approval Pending Sale letter?

The letter typically includes the specific loan amount, the interest rate, a list of remaining conditions, and the explicit requirement for a "Settlement Statement" (CD) from the sale of the current residence to prove the debt has been paid off and sufficient equity has been realized.

Can I make an offer on a new home with a conditional approval letter?

Yes, you can make an offer, but sellers will view it as a "contingent offer." While the letter proves you are creditworthy, the purchase of the new home is legally dependent on the successful closing of your current property, which may affect your negotiating power in competitive markets.

How do I clear the "Pending Sale" condition from my mortgage commitment?

To clear this condition, you must provide your lender with the final signed Closing Disclosure or ALTA statement from the sale of your previous home. The lender will verify that the previous mortgage is satisfied and that you have the required cash proceeds for your new down payment and closing costs.

Comments