Receiving a Notice of Force-Placed Insurance Escrow Modification indicates your mortgage servicer has adjusted your monthly payments to cover lender-placed coverage. This typically occurs when your voluntary policy lapses or is insufficient, triggering a change in your escrow account analysis and required reserves. Understanding these adjustments is vital for maintaining your home equity. Below are some ready to use templates.

Image cover: Official Guide: Force-Placed Insurance Escrow Modification Notices and Templates

Letter Samples List

- Initial Notice of Force-Placed Insurance Escrow Modification Letter

- Second Warning Force-Placed Insurance Escrow Modification Letter

- Final Notice of Force-Placed Insurance Escrow Modification Letter

- Hazard Insurance Lapse Force-Placed Escrow Modification Letter

- Flood Insurance Force-Placed Escrow Modification Notice Letter

- Escrow Shortage Due to Force-Placed Insurance Modification Letter

- Notice of Force-Placed Insurance Escrow Payment Modification Letter

- Retroactive Force-Placed Insurance Escrow Modification Letter

- Annual Escrow Analysis Force-Placed Insurance Modification Letter

- Notice of Force-Placed Insurance Cancellation Escrow Modification Letter

- Evidence of Insurance Escrow Modification Reversal Letter

- Windstorm Force-Placed Insurance Escrow Modification Notice Letter

- First Notice of Force-Placed Insurance Escrow Modification Letter

- Final Notice of Force-Placed Insurance Escrow Modification Letter

- Escrow Account Adjustment Due to Force-Placed Insurance Letter

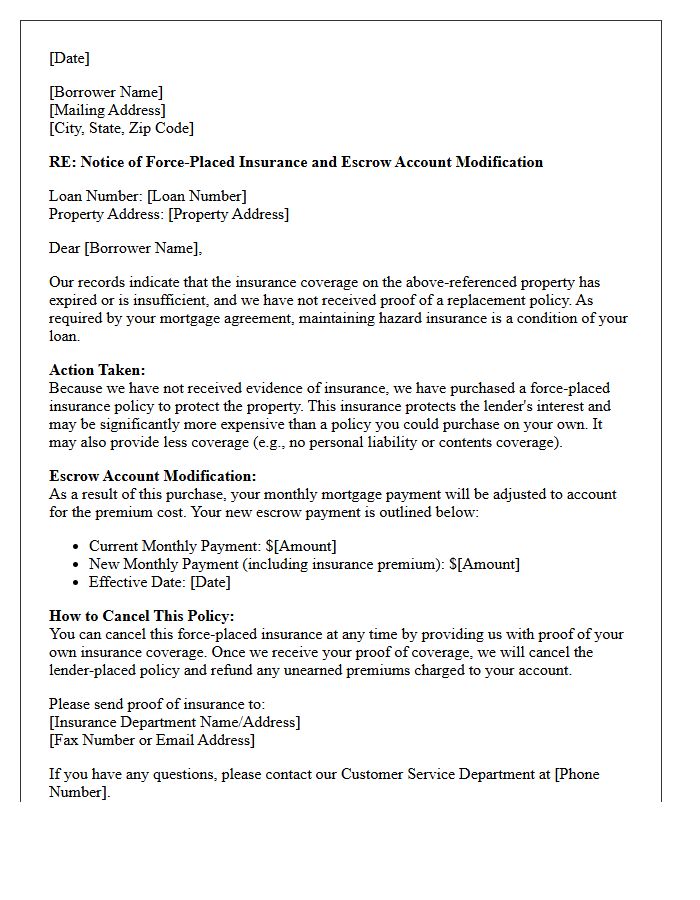

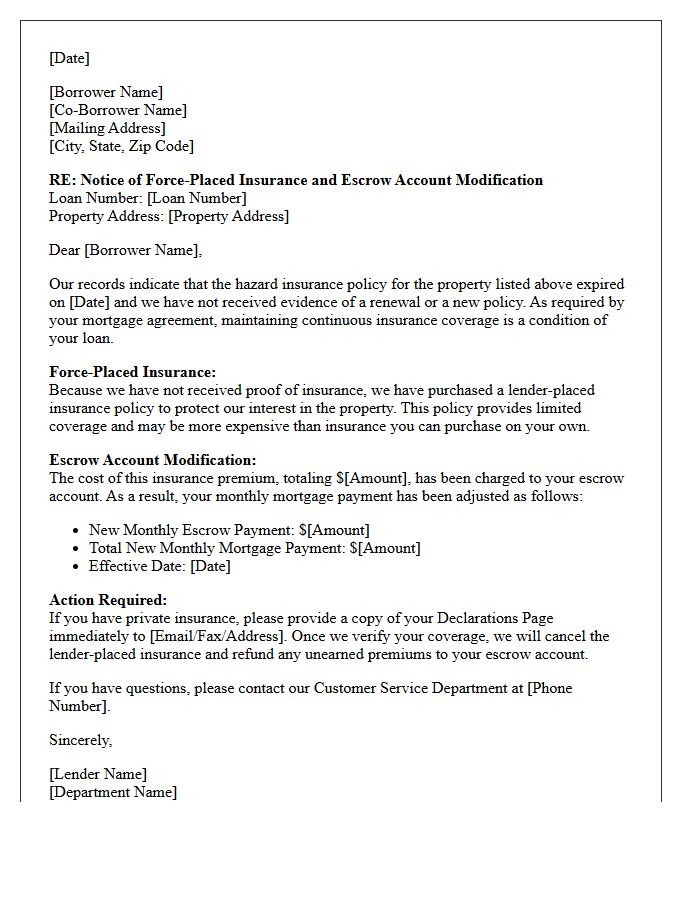

Initial Notice of Force-Placed Insurance Escrow Modification Letter

An Initial Notice of Force-Placed Insurance Escrow Modification Letter informs homeowners that their lender has purchased a property insurance policy because the previous coverage lapsed. This formal notification details the premium costs added to your mortgage balance and the resulting escrow account adjustment. It serves as a final warning to provide proof of voluntary coverage to avoid high-cost lender-placed policies. Reviewing this document immediately is essential to prevent significant increases in monthly payments and ensure your property remains protected under your preferred insurance provider's terms.

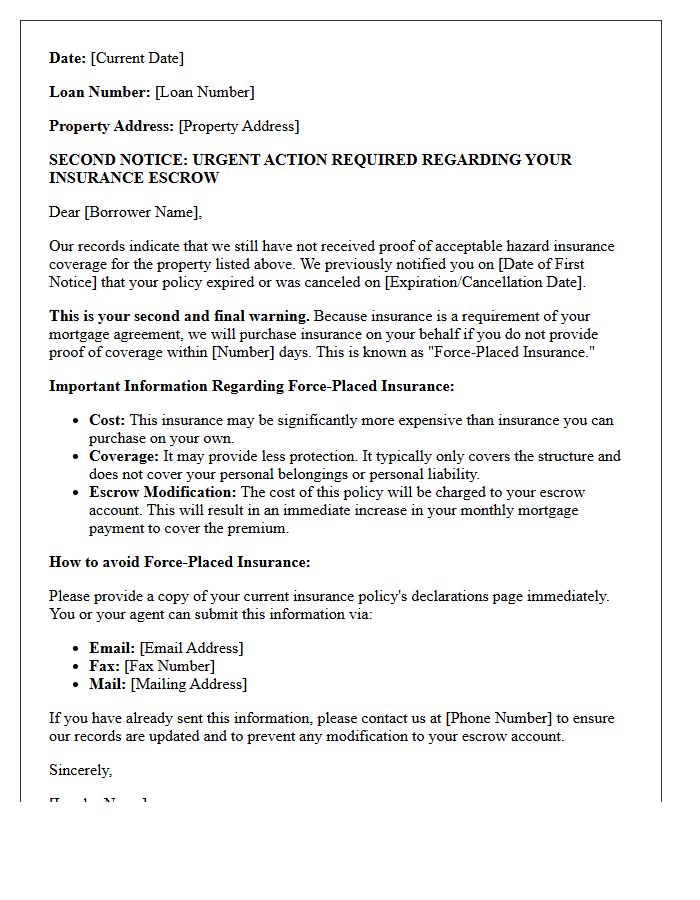

Second Warning Force-Placed Insurance Escrow Modification Letter

A Second Warning Force-Placed Insurance Escrow Modification Letter is a final notice from your lender regarding a lapse in coverage. It warns that because you have not provided proof of valid homeowners insurance, the bank will purchase a policy on your behalf. This forced coverage is typically more expensive and offers less protection than private plans. Receiving this letter means your escrow account will be adjusted to cover these higher premiums, significantly increasing your monthly mortgage payment. You must submit valid insurance documentation immediately to avoid these mandatory costs and financial penalties.

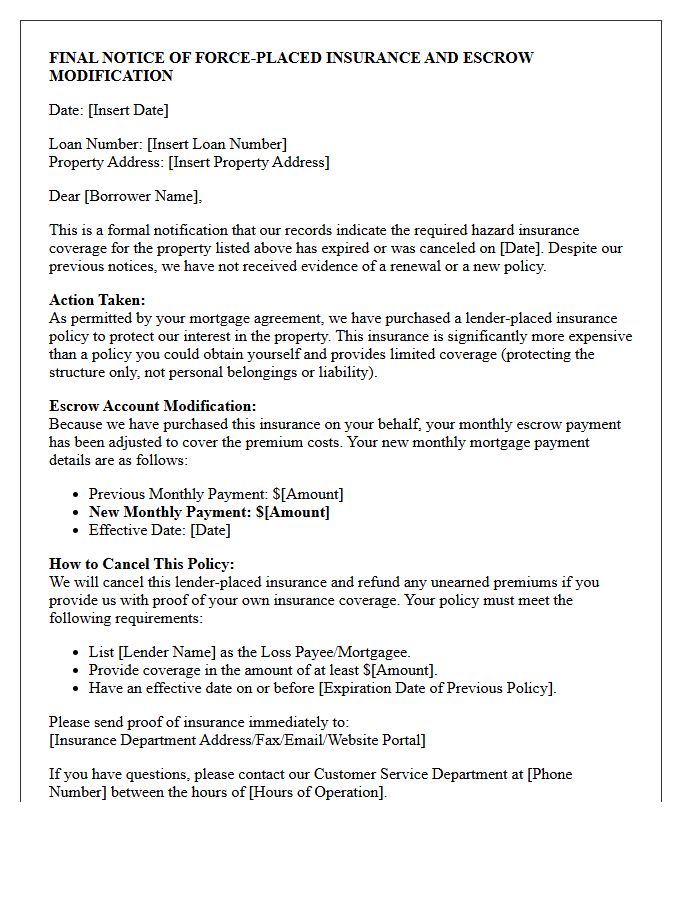

Final Notice of Force-Placed Insurance Escrow Modification Letter

A Final Notice of Force-Placed Insurance Escrow Modification informs homeowners that their lender has purchased a property insurance policy on their behalf because previous coverage lapsed. This letter confirms the final escrow adjustment, leading to significantly higher monthly mortgage payments to recover premium costs. It is critical to provide proof of private insurance immediately to cancel this expensive policy. Failure to act results in increased debt and potential foreclosure risks. Always verify that your lender received your current policy details to avoid these unnecessary financial penalties and maintain proper homeowner protection.

Hazard Insurance Lapse Force-Placed Escrow Modification Letter

A Hazard Insurance Lapse Force-Placed Escrow Modification Letter is a formal notice from your mortgage lender. It confirms that your private policy expired, prompting the lender to purchase force-placed insurance to protect the collateral. This document details the escrow modification, as the high premiums are added to your monthly mortgage payment. It is crucial to provide proof of replacement coverage immediately to cancel this expensive policy and receive a pro-rated refund. Maintaining continuous insurance is a legal requirement under your loan agreement to avoid financial penalties and potential default.

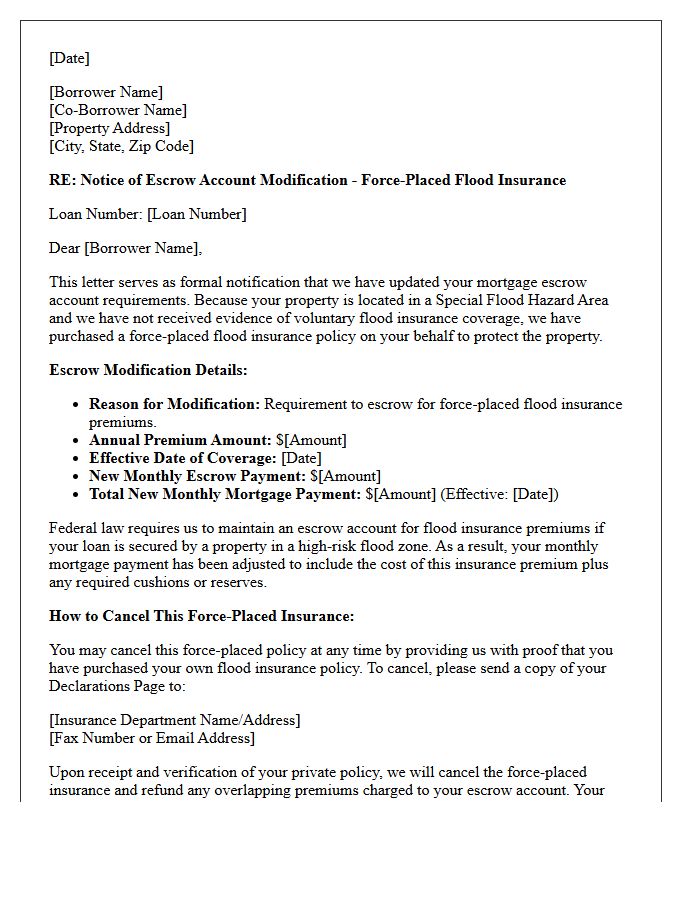

Flood Insurance Force-Placed Escrow Modification Notice Letter

A Force-Placed Escrow Modification Notice informs homeowners that their lender has identified a flood insurance coverage gap. If you fail to provide proof of an active policy, the lender will force-place coverage at your expense. This letter details the updated escrow payments required to cover these premiums. It is crucial to submit your private policy documentation immediately to cancel the expensive force-placed plan and ensure your mortgage compliance remains intact under federal regulations. Always verify the coverage amounts to avoid unnecessary financial penalties and protect your property investment.

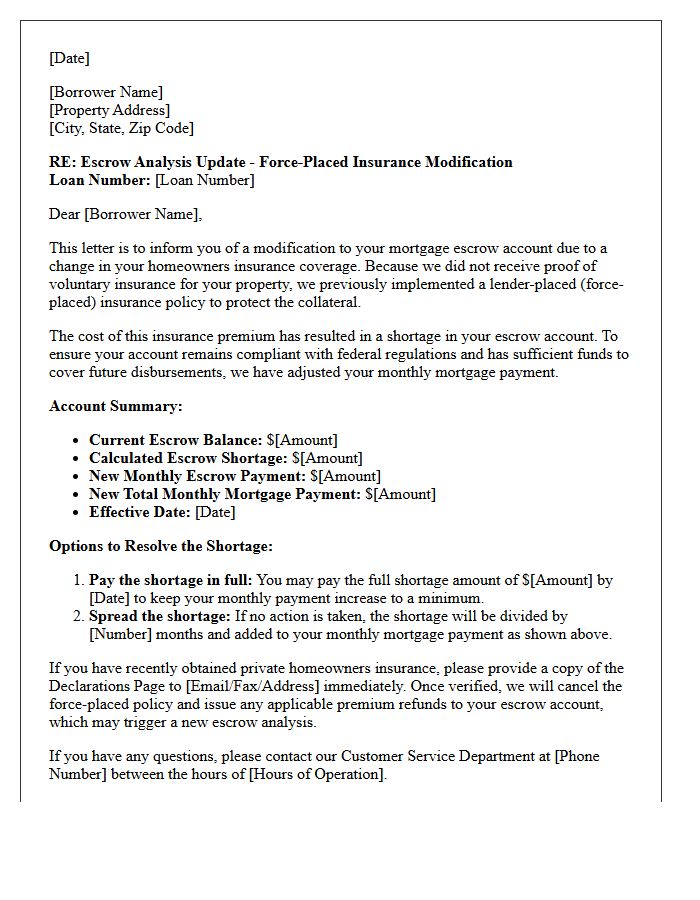

Escrow Shortage Due to Force-Placed Insurance Modification Letter

An escrow shortage occurs when your lender advances funds to cover insurance premiums, often triggered by a Force-Placed Insurance Modification Letter. This notice indicates that your lender purchased a policy on your behalf because your private coverage lapsed or was deemed insufficient. Since forced-placed policies are significantly more expensive than standard insurance, your monthly mortgage payment will increase to recover the deficit and fund the future escrow balance. To resolve this, immediately provide proof of independent coverage to your servicer to cancel the costly lender-placed policy and reduce your escrow obligations.

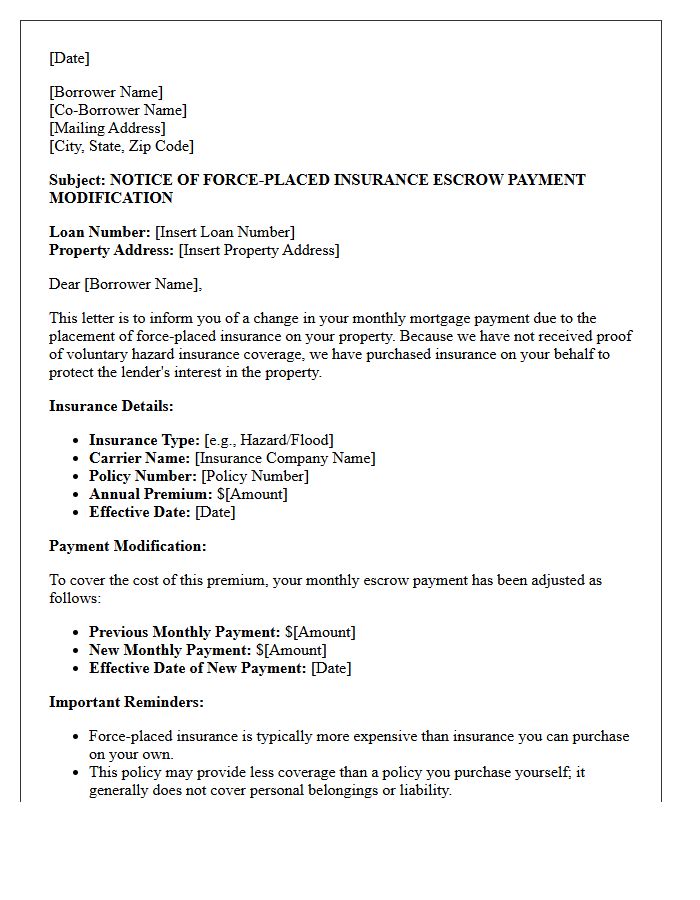

Notice of Force-Placed Insurance Escrow Payment Modification Letter

A Notice of Force-Placed Insurance Escrow Payment Modification informs borrowers that their lender has purchased a property insurance policy because the borrower's own coverage lapsed. This letter confirms the cost of the premium and details how your monthly mortgage payment will increase to cover the escrow shortage. It is critical to provide proof of active private insurance immediately to cancel this expensive policy. Once valid coverage is verified, the lender must refund overlapping premiums and adjust your escrow account, ensuring your loan balance remains accurate and protected.

Retroactive Force-Placed Insurance Escrow Modification Letter

A Retroactive Force-Placed Insurance Escrow Modification Letter notifies homeowners that their mortgage servicer purchased lender-placed coverage for a past period when private insurance lapsed. This notice confirms a recalculation of your escrow account to recover unpaid premiums. It is vital to provide proof of continuous coverage immediately to cancel these backdated charges. Failure to act results in significantly higher monthly mortgage payments and potential escrow shortages. Review the effective dates carefully to ensure you are not being double-billed for periods where independent insurance was active.

Annual Escrow Analysis Force-Placed Insurance Modification Letter

An Annual Escrow Analysis review ensures your account remains balanced to cover taxes and Force-Placed Insurance premiums. When a lender secures coverage because your private policy lapsed, this Modification Letter serves as formal notice of adjusted monthly payments. It outlines the increased costs associated with lender-placed protection, which is typically more expensive and offers less coverage than standard plans. Understanding this document is vital to managing your mortgage escrow and ensuring your property remains protected while you work to reinstate voluntary insurance and lower your total housing expenses.

Notice of Force-Placed Insurance Cancellation Escrow Modification Letter

A Notice of Force-Placed Insurance Cancellation occurs when a lender terminates a lender-placed policy because you provided proof of your own coverage. This trigger often leads to an Escrow Modification Letter, which outlines updated monthly mortgage payments. It is crucial to review this document to ensure your escrow account balance is adjusted and any unearned premiums are properly refunded. Promptly verifying these changes prevents overpayment and confirms your personal homeowners insurance is active and accepted by your mortgage servicer to avoid future lapses.

Evidence of Insurance Escrow Modification Reversal Letter

An Evidence of Insurance Escrow Modification Reversal Letter is a formal notice confirming that a previous change to your mortgage escrow account has been canceled. This typically occurs when a homeowner provides updated proof of coverage, resolving a perceived insurance lapse. It is crucial to review this document to ensure your monthly mortgage payment accurately reflects the correct tax and insurance disbursements. This letter serves as vital legal documentation that your lender has reinstated your original payment structure and acknowledged your active insurance policy, preventing unnecessary force-placed insurance charges.

Windstorm Force-Placed Insurance Escrow Modification Notice Letter

A Windstorm Force-Placed Insurance Escrow Modification Notice informs homeowners that their lender has purchased a windstorm policy because their voluntary coverage lapsed. This letter details an escrow account adjustment, as the lender advances funds for the premium and subsequently increases your monthly mortgage payment to recover costs. It is critical to provide proof of your own insurance immediately to cancel this expensive force-placed policy and restore your original payment schedule. Always verify that the coverage limits meet your lender's requirements to avoid future escrow shortages or payment spikes.

First Notice of Force-Placed Insurance Escrow Modification Letter

A First Notice of Force-Placed Insurance Escrow Modification Letter informs homeowners that their lender has identified a lapse in coverage. If you fail to provide proof of active hazard insurance, the lender will purchase a policy on your behalf. This force-placed insurance is typically much more expensive and provides less protection than private policies. The notice outlines how your monthly mortgage payment will increase to cover the new escrow disbursements. It is critical to submit your valid policy declarations page immediately to avoid these high costs and maintain adequate home protection.

Final Notice of Force-Placed Insurance Escrow Modification Letter

A Final Notice of Force-Placed Insurance Escrow Modification informs homeowners that their lender has officially purchased a property insurance policy because the previous coverage lapsed. This force-placed insurance is typically more expensive and provides less protection than private policies. The letter confirms a mandatory adjustment to your monthly mortgage escrow payment to cover these premiums. To stop this action and lower your costs, you must immediately provide proof of active insurance to your lender to cancel the lender-placed policy and seek a refund for unearned premiums.

Escrow Account Adjustment Due to Force-Placed Insurance Letter

Receiving an escrow account adjustment letter often stems from force-placed insurance, which occurs when a lender purchases coverage because your primary policy lapsed. This lender-placed insurance is typically much more expensive and provides less protection than private plans. The adjustment results in a higher monthly mortgage payment to recover the premium costs. To resolve this, you must immediately provide your lender with proof of continuous coverage to cancel the force-placed policy and potentially receive a refund for the overlapping premium period, restoring your original escrow balance.

What is a Notice of Force-Placed Insurance Escrow Modification?

A Notice of Force-Placed Insurance Escrow Modification is a formal communication sent by a mortgage servicer informing the borrower that the cost of lender-placed insurance has changed, resulting in an adjustment to their monthly escrow payment and overall mortgage obligation.

Why did my escrow payment change due to force-placed insurance?

Your escrow payment changed because the premium for the insurance policy purchased by your lender-required when voluntary coverage lapses-has been updated. This modification ensures the escrow account maintains a sufficient balance to cover the new premium cost and any required minimum cushions.

Can I cancel a force-placed insurance escrow modification?

Yes, you can cancel the modification by providing your mortgage servicer with proof of private homeowners insurance that meets your lender's requirements. Once valid proof of voluntary coverage is processed, the lender will cancel the force-placed policy and refund any overlapping premiums to your escrow account.

How does force-placed insurance affect my mortgage escrow account?

Force-placed insurance typically carries higher premiums than private insurance, which increases the total annual disbursements from your escrow account. This leads to a higher monthly escrow requirement and may result in an escrow shortage that needs to be repaid over time.

What should I do if I receive a Force-Placed Insurance Escrow Modification notice?

Upon receiving this notice, you should first verify if your private insurance policy has lapsed. If you have active coverage, send the declarations page to your servicer immediately; if you do not have coverage, you should shop for a private policy to replace the more expensive force-placed option and lower your monthly payment.

Comments