A Loss Mitigation Evaluation Notice is a formal document sent by mortgage servicers to borrowers after reviewing their application for foreclosure alternatives. This notice details the lender's decision regarding options like loan modifications, short sales, or deeds-in-lieu of foreclosure. It outlines approved terms, denial reasons, and essential appeal rights for homeowners. To assist in your communication, below are some ready to use templates.

Image cover: Loss Mitigation Evaluation Notice: Formal Templates and Sending Guidelines

Letter Samples List

- Loss Mitigation Evaluation Approval Letter

- Loss Mitigation Evaluation Denial Letter

- Incomplete Loss Mitigation Application Evaluation Letter

- Loss Mitigation Missing Documents Evaluation Letter

- Loan Modification Evaluation Notice Letter

- Forbearance Plan Evaluation Approval Letter

- Repayment Plan Evaluation Notice Letter

- Short Sale Loss Mitigation Evaluation Letter

- Deed-in-Lieu of Foreclosure Evaluation Letter

- Loss Mitigation Evaluation Appeal Decision Letter

- Trial Period Plan Evaluation Notice Letter

- Loss Mitigation Evaluation Acknowledgment Letter

- Final Loss Mitigation Evaluation Determination Letter

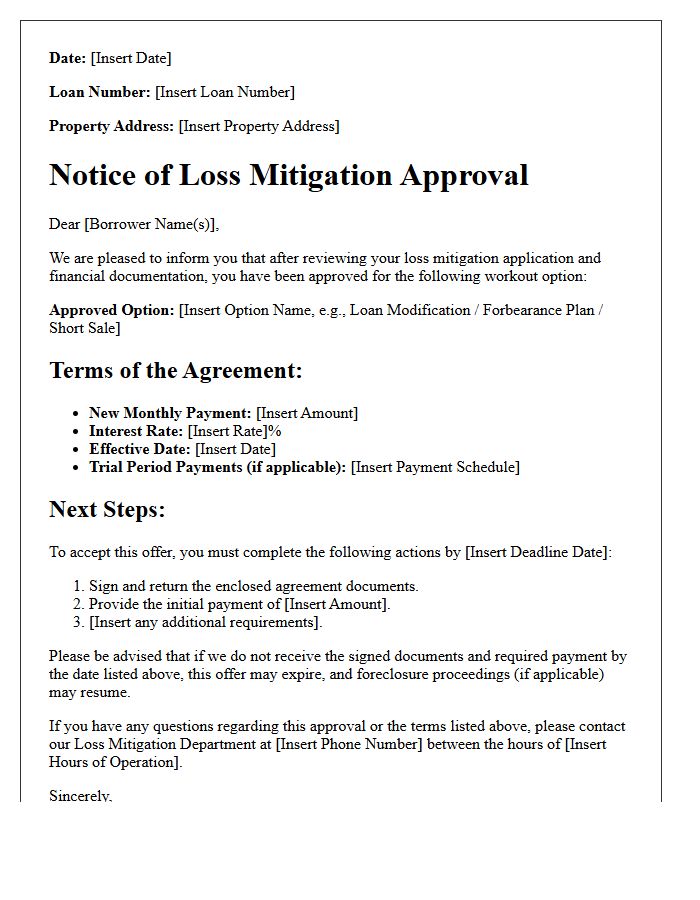

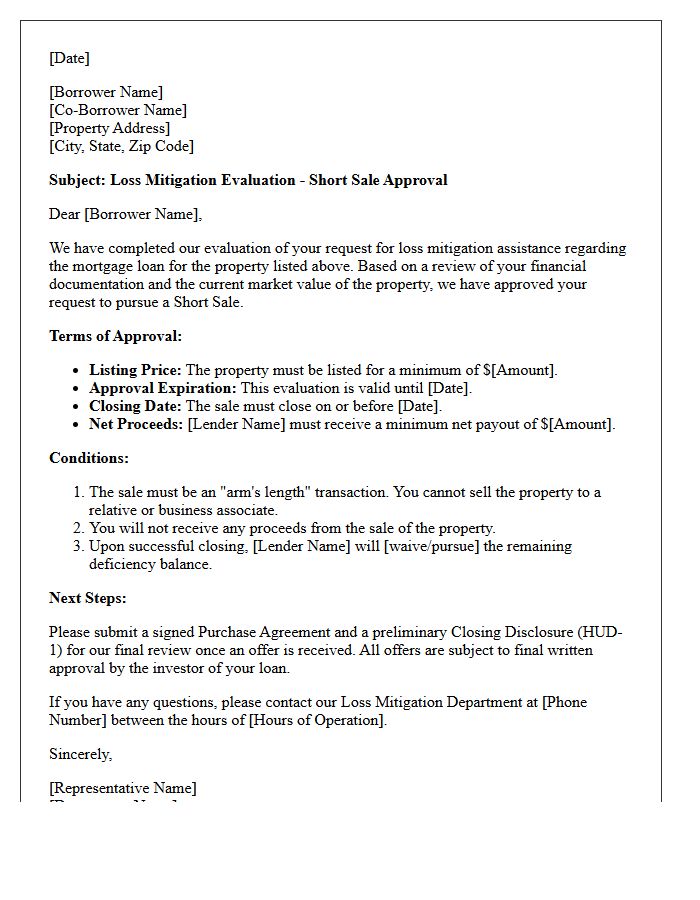

Loss Mitigation Evaluation Approval Letter

A Loss Mitigation Evaluation Approval Letter is a formal document from your mortgage servicer outlining approved options to avoid foreclosure. It details specific terms for solutions like loan modifications, short sales, or repayment plans. Homeowners must review the expiration date and required actions immediately to secure the offer. This letter serves as legal proof of the lender's commitment to adjust your mortgage terms, provided you meet all eligibility requirements and deadlines. Timely communication and signature submission are essential to finalize your homeownership preservation status and ensure long-term financial stability.

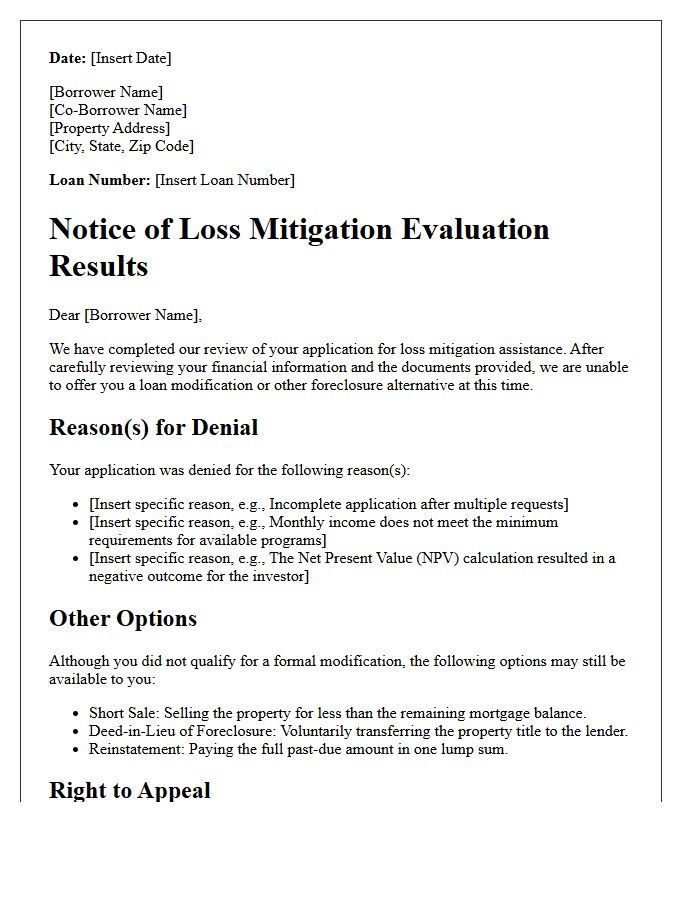

Loss Mitigation Evaluation Denial Letter

Receiving a Loss Mitigation Evaluation Denial Letter is a critical notice from your mortgage servicer explaining why your application for foreclosure alternatives was rejected. The most important thing to know is your right to an appeal, which must typically be filed within 30 days. The letter must provide specific reasons for the denial, such as incomplete documentation or failing investor eligibility requirements. Reviewing these details immediately is essential to identify errors, resubmit corrected information, or pursue other legal remedies to protect your home from foreclosure.

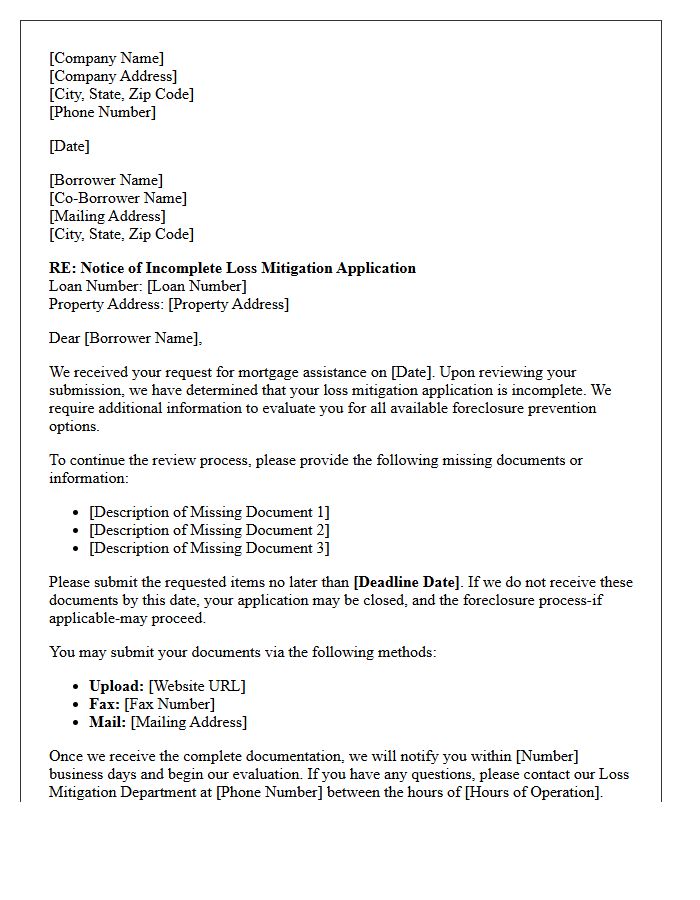

Incomplete Loss Mitigation Application Evaluation Letter

An Incomplete Loss Mitigation Application Evaluation Letter is a critical notice from your mortgage servicer identifying missing documents required for a loan workout. It specifies the deficiency and provides a strict deadline to submit the information. Failing to respond promptly can pause the foreclosure protection process and lead to a denial of assistance. Homeowners must review the checklist carefully and provide all supporting evidence immediately to ensure a full review of their eligibility for options like loan modifications or short sales.

Loss Mitigation Missing Documents Evaluation Letter

A loss mitigation missing documents evaluation letter is a critical notice from your mortgage servicer indicating your application is incomplete. This document lists specific financial proofs or forms required to proceed with a loan modification or foreclosure alternative. You must submit the requested items before the stated deadline to avoid a denial of assistance. Treating this letter with urgency is essential, as the evaluation process remains paused until the file is complete. Always keep copies of everything sent to ensure your homeownership rights are protected during the review period.

Loan Modification Evaluation Notice Letter

A Loan Modification Evaluation Notice Letter is a critical document from your mortgage servicer detailing the decision regarding your request for payment assistance. It specifies whether you are approved for a modified plan, denied, or if more information is required. If approved, the letter outlines new interest rates, monthly payments, and loan terms. If denied, it must state the specific reason and explain your right to appeal. Reviewing this notice promptly is essential to understand your options and prevent foreclosure proceedings on your home.

Forbearance Plan Evaluation Approval Letter

A Forbearance Plan Evaluation Approval Letter is a formal document from your mortgage servicer confirming your temporary payment relief. It outlines specific terms, including the duration of the reduced or suspended payment period and the start date. This letter is crucial because it serves as legal proof that your lender has authorized a pause to avoid foreclosure. It also specifies that repayment of the deferred amount is required later, often through a modification, reinstatement, or repayment plan once the forbearance period concludes.

Repayment Plan Evaluation Notice Letter

A Repayment Plan Evaluation Notice Letter is a critical document issued by loan servicers to inform borrowers about their eligibility for loss mitigation options. This letter details whether your application for a mortgage workout was approved or denied. It explicitly outlines the new repayment terms, including updated monthly amounts, duration, and deadlines. Carefully reviewing this notice is essential to avoid foreclosure and ensure your financial stability. If you disagree with the decision, the letter provides specific instructions on how to file an appeal within the required timeframe.

Short Sale Loss Mitigation Evaluation Letter

A Short Sale Loss Mitigation Evaluation Letter is a formal document from a mortgage servicer detailing the approval or denial of a homeowner's request to sell their property for less than the remaining loan balance. This letter outlines specific conditions, such as the minimum net proceeds required and any potential deficiency waiver. It is a critical step in the foreclosure prevention process, confirming that the lender agrees to release the lien upon a successful closing. Homeowners must review all deadlines and tax implications mentioned to ensure full compliance with the settlement terms.

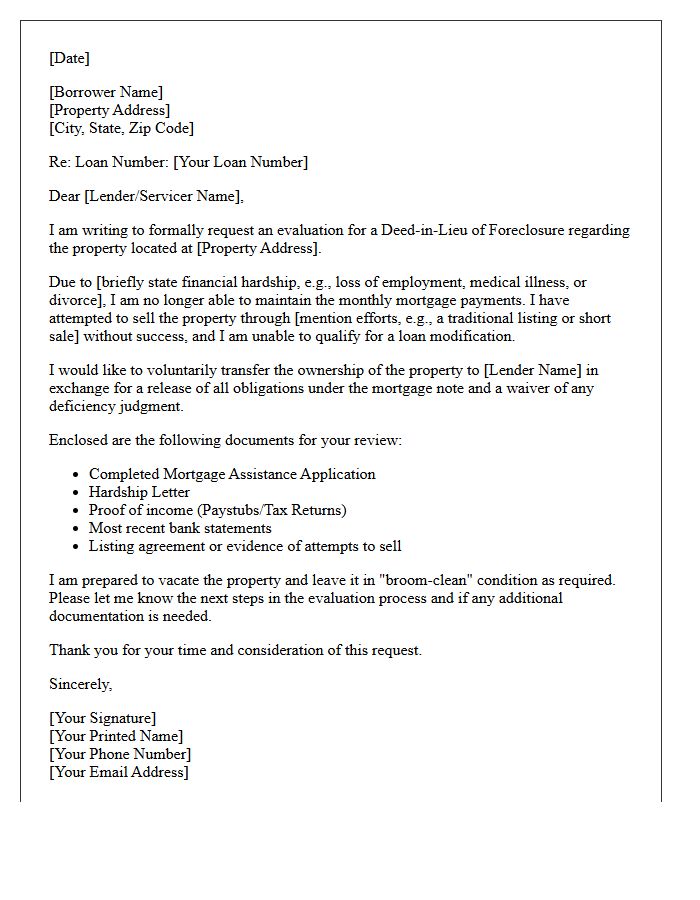

Deed-in-Lieu of Foreclosure Evaluation Letter

A Deed-in-Lieu of Foreclosure Evaluation Letter is a formal document from a mortgage servicer determining your eligibility to voluntarily transfer property ownership to avoid legal proceedings. This letter outlines specific approval conditions, required documentation, and potential financial implications, such as deficiency waivers. Understanding these terms is vital for protecting your credit score and ensuring a smooth transition. Always verify if the agreement includes a release of liability to prevent future debt collection. Receiving this evaluation is a critical step in resolving mortgage delinquency through a structured, non-judicial settlement process.

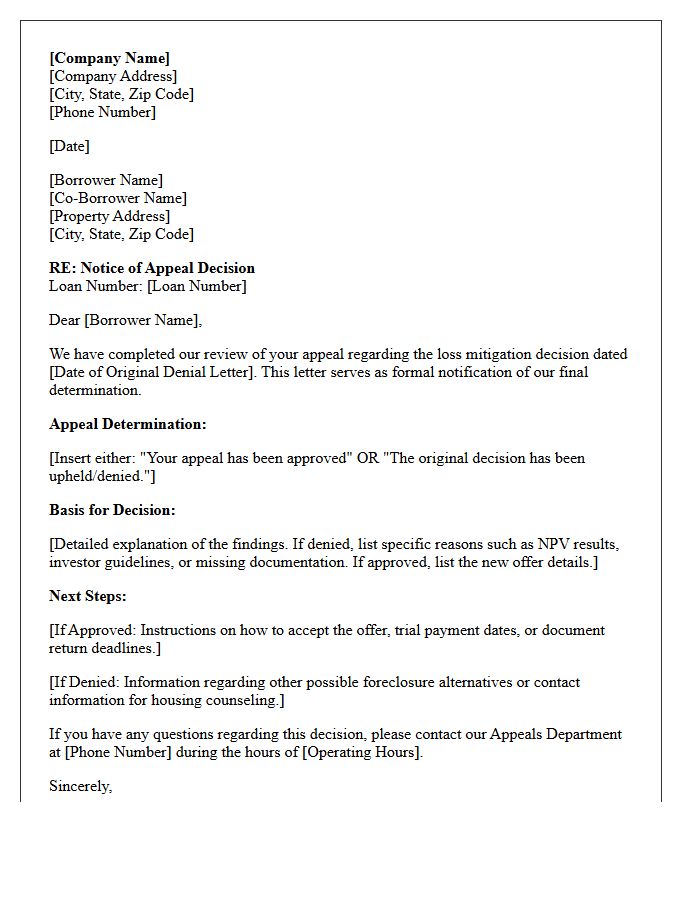

Loss Mitigation Evaluation Appeal Decision Letter

A Loss Mitigation Evaluation Appeal Decision Letter is the final written determination issued by a mortgage servicer after reviewing a borrower's challenge to a loan modification denial. This document specifies whether the original decision was upheld or overturned based on a de novo review by personnel not involved in the initial assessment. It is critical to understand that this letter represents the conclusion of the formal internal appeals process. If the denial is sustained, the borrower must immediately explore alternative foreclosure prevention options or seek legal counsel to protect their property rights.

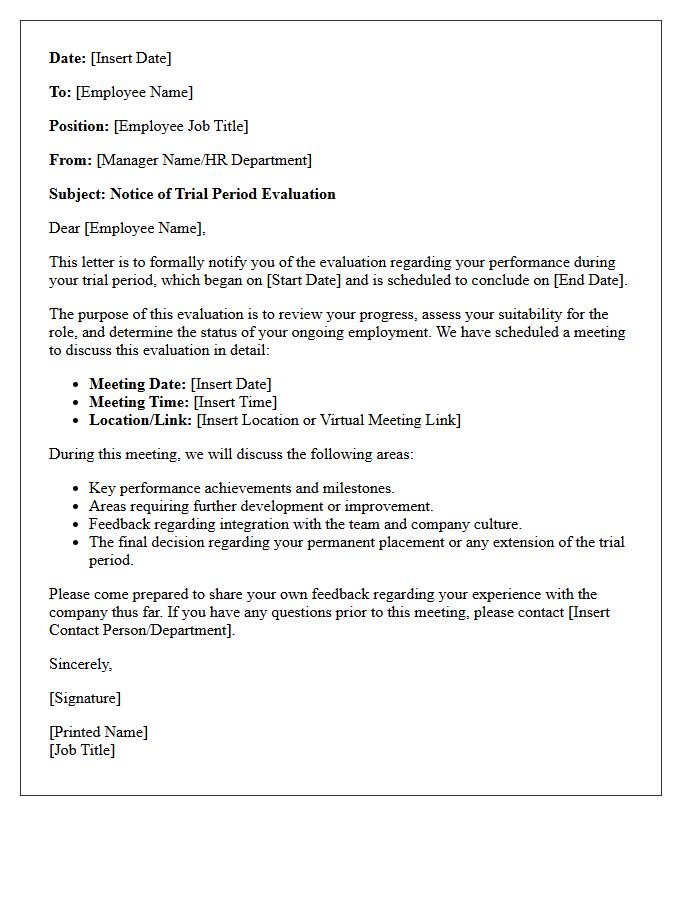

Trial Period Plan Evaluation Notice Letter

A Trial Period Plan Evaluation Notice Letter is a critical document sent by mortgage servicers to inform homeowners about their eligibility for a loan modification. It outlines the specific terms, monthly payment amounts, and the duration of the trial phase. Successfully completing this period by making all payments on time is essential to securing a permanent modification. Homeowners should review the deadlines and required documentation carefully to avoid foreclosure and ensure long-term housing stability through this formal assessment process.

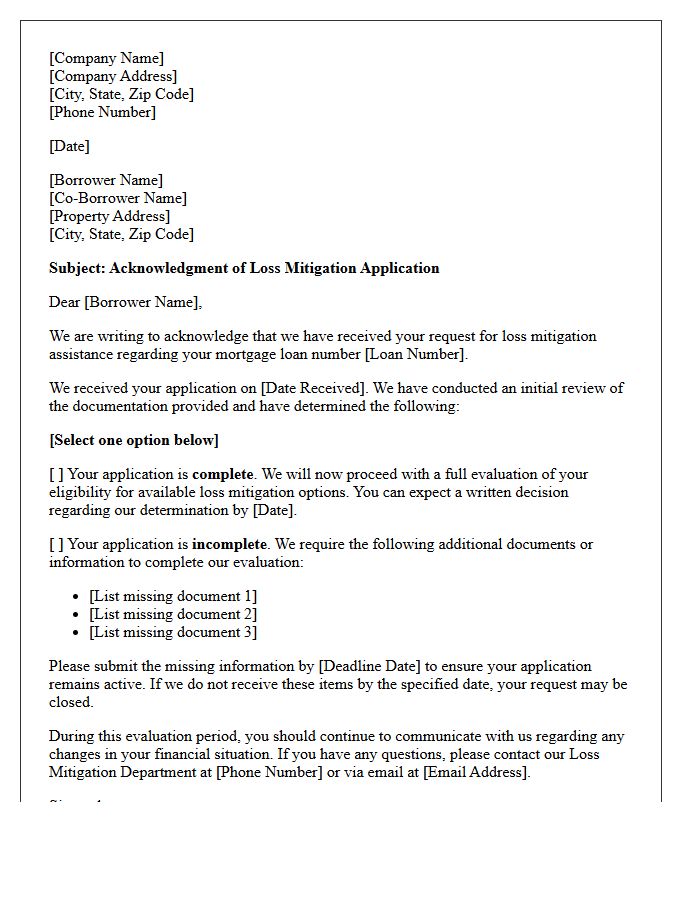

Loss Mitigation Evaluation Acknowledgment Letter

The Loss Mitigation Evaluation Acknowledgment Letter is a formal notice from your mortgage servicer confirming receipt of your assistance application. It is crucial because it lists the specific mitigation options being reviewed, such as loan modifications or short sales. This document establishes a legal timeline for the lender to evaluate your file. Reviewing it immediately ensures all submitted financial documentation is complete. If any information is missing, you must respond promptly to maintain your foreclosure protection and ensure your application moves forward for a final decision.

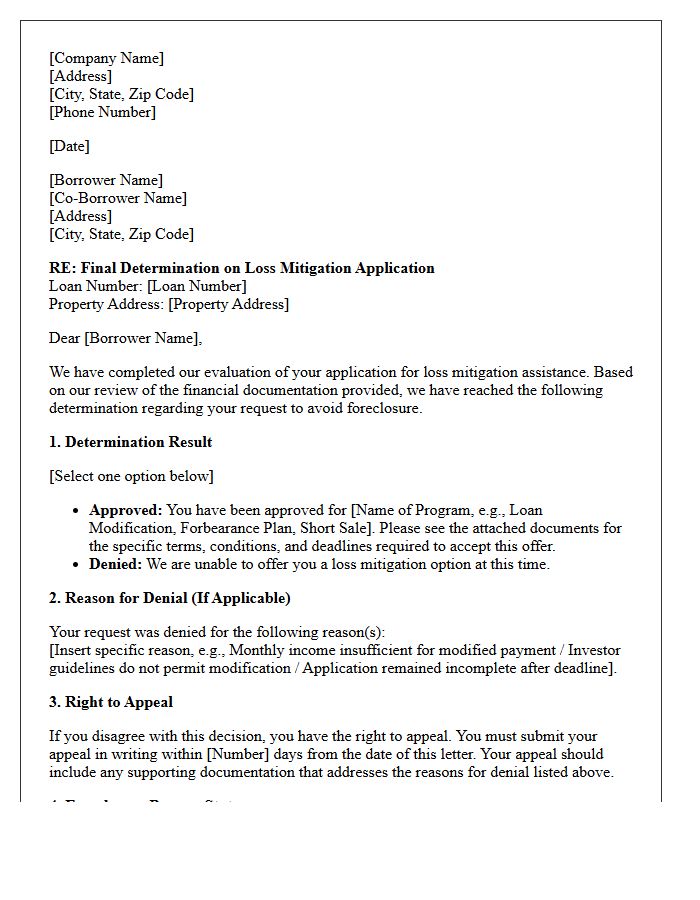

Final Loss Mitigation Evaluation Determination Letter

A Final Loss Mitigation Evaluation Determination Letter is a formal notice from your mortgage servicer detailing the outcome of your foreclosure prevention application. This critical document specifies whether you have been approved for options like a loan modification, short sale, or deed-in-lieu. If denied, the letter must provide specific reasons for the decision and outline your right to appeal. Reviewing this letter immediately is vital, as it contains strict deadlines for accepting offers or contesting a denial to protect your homeownership rights.

What is a Loss Mitigation Evaluation Notice?

A Loss Mitigation Evaluation Notice is a formal letter sent by a mortgage servicer to a borrower after reviewing their loss mitigation application. This notice details the servicer's decision regarding available foreclosure prevention options, such as a loan modification, short sale, or deed-in-lieu of foreclosure.

How long does a lender have to send a Loss Mitigation Evaluation Notice?

Under federal CFPB guidelines, mortgage servicers generally must evaluate a complete loss mitigation application and provide a written evaluation notice within 30 days of receiving the completed package.

What information is included in a Loss Mitigation Evaluation Notice?

The notice must include the specific outcome for each available foreclosure alternative, the reasons for any denial, instructions on how to appeal the decision, and deadlines for accepting any offered trial period plans or permanent modifications.

Can I appeal the decision in my Loss Mitigation Evaluation Notice?

Yes, if your application was submitted more than 90 days before a scheduled foreclosure sale and was denied for any loan modification option, you typically have 14 days from the date of the notice to file a formal appeal with the servicer.

What should I do after receiving a Loss Mitigation Evaluation Notice?

You should immediately review the document to determine if you were approved for a workout plan. If an offer is made, you must respond by the stated deadline to accept the terms; if denied, you should evaluate the reasons provided and determine if you have grounds for an appeal or need to pursue a different loss mitigation strategy.

Comments