A Short Sale Deficiency Waiver Notice is a critical legal document confirming that a lender agrees to forgo their right to pursue a borrower for the remaining balance after a property sale. Securing this written release is essential to ensuring complete debt forgiveness and long-term financial recovery. To help you navigate this process, below are some ready to use templates.

Image cover: Short Sale Deficiency Waiver Request: Essential Templates and Sample Letters

Letter Samples List

- Short Sale Deficiency Waiver Notice Letter

- Mortgage Short Sale Approval and Deficiency Waiver Letter

- Deficiency Forgiveness and Short Sale Agreement Letter

- Lender Notice of Deficiency Waiver Letter

- Short Sale Payoff and Deficiency Release Letter

- Final Short Sale Settlement and Waiver Letter

- Mortgage Balance Forgiveness Notification Letter

- Approval Letter for Short Sale and Deficiency Waiver

- Notice of Deficiency Waiver Confirmation Letter

- Promissory Note Release and Deficiency Waiver Letter

- Short Sale Acceptance and Deficiency Discharge Letter

- Unpaid Balance Waiver Notification Letter

- Mortgage Debt Cancellation and Waiver Letter

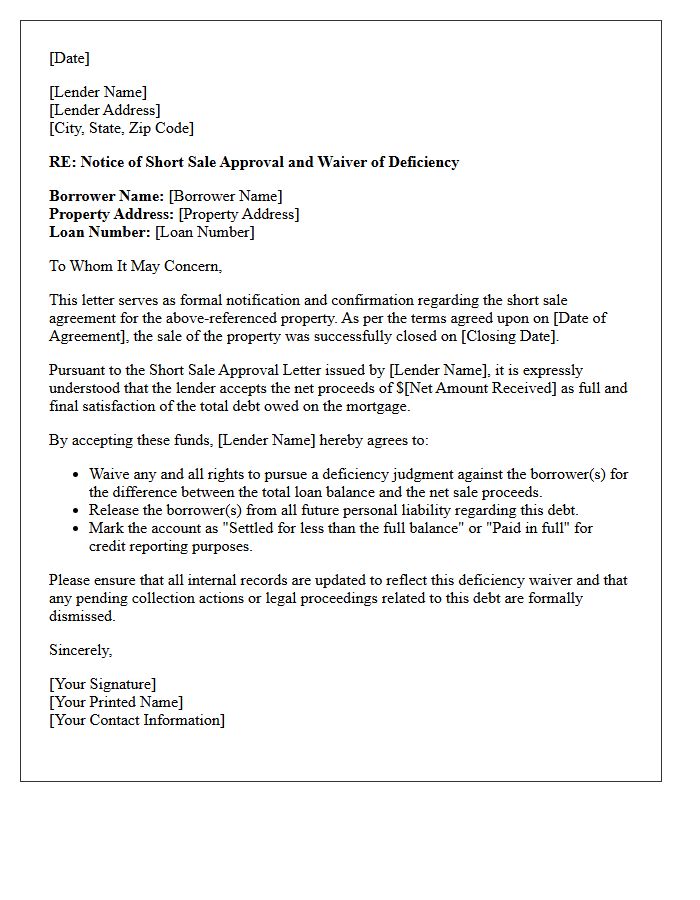

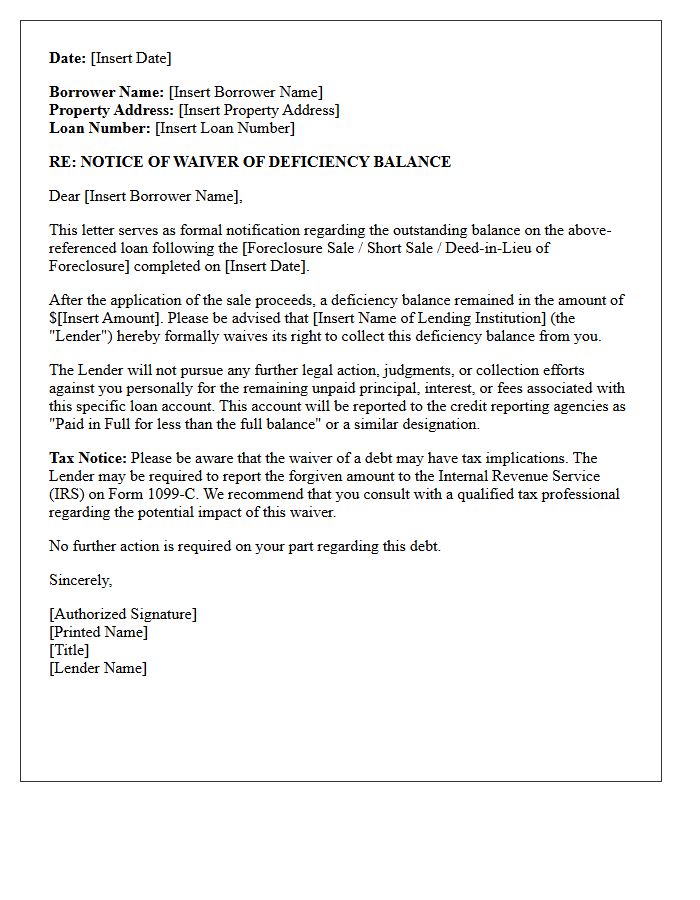

Short Sale Deficiency Waiver Notice Letter

A Short Sale Deficiency Waiver Notice Letter is a critical legal document confirming that a lender agrees to cancel the remaining debt after a home sells for less than the mortgage balance. Without this explicit deficiency waiver, homeowners may remain legally liable for the financial shortfall, potentially facing future collections or lawsuits. Borrowers must ensure the language clearly states the debt is "settled in full" or "waived" to achieve complete financial release. Always verify the letter's authenticity and specific terms before closing to protect against long-term liability and credit damage.

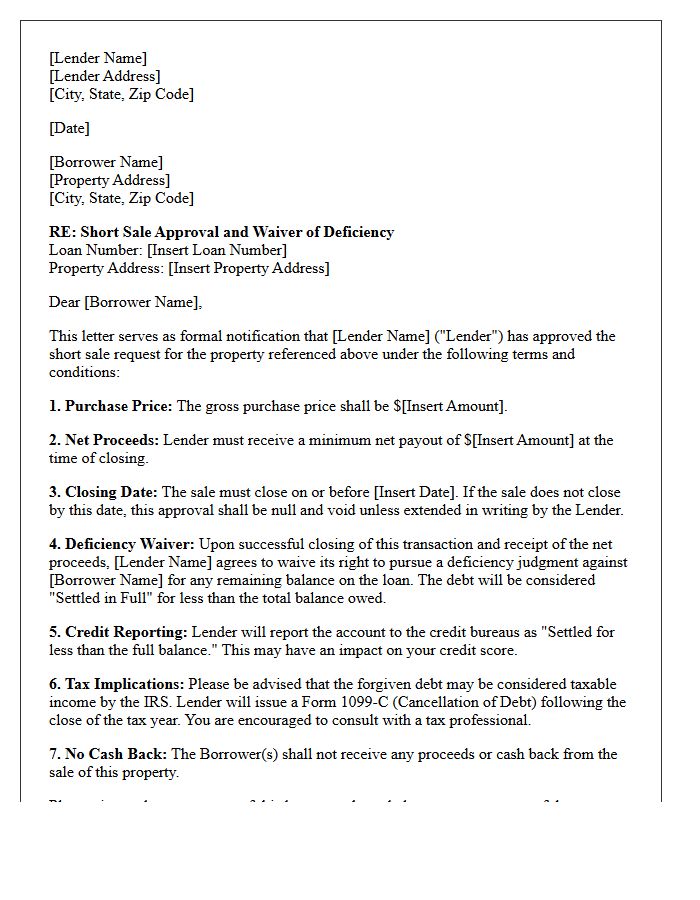

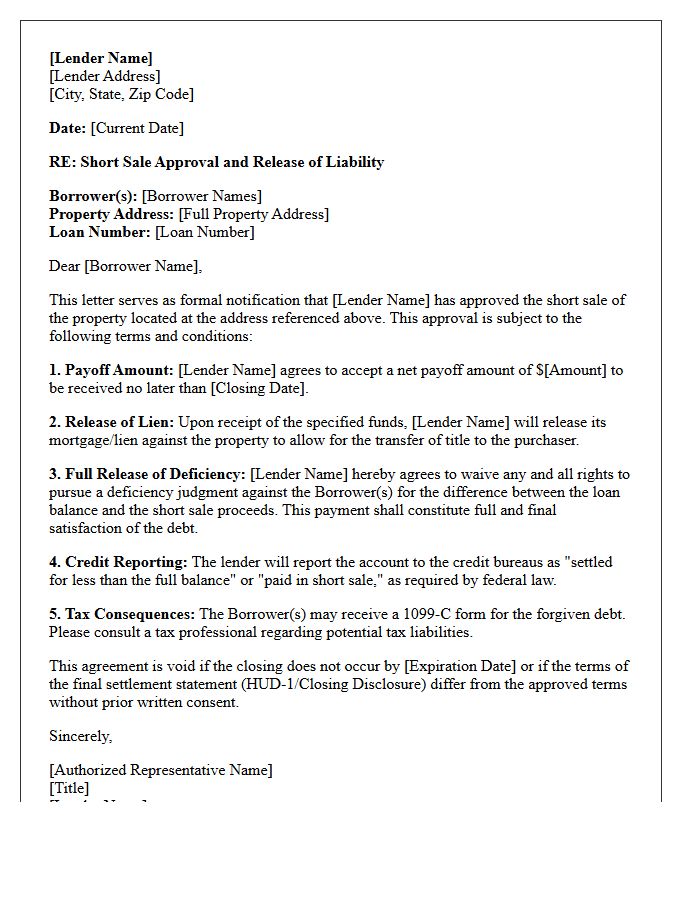

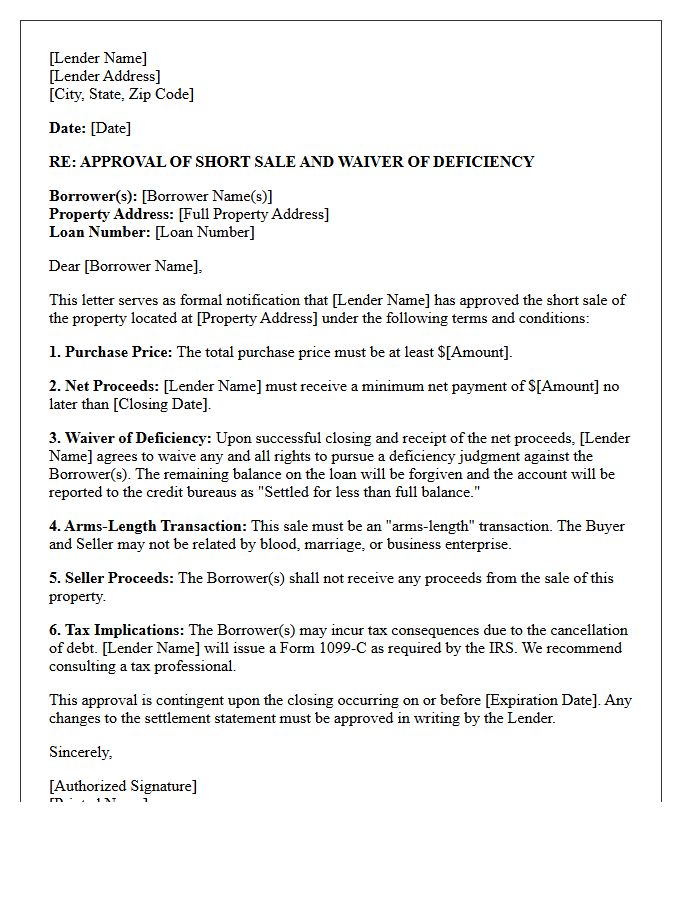

Mortgage Short Sale Approval and Deficiency Waiver Letter

A Mortgage Short Sale Approval occurs when a lender agrees to accept less than the total loan balance to release their lien. However, securing the sale is only half the battle. You must obtain a formal Deficiency Waiver Letter to ensure the lender legally forfeits their right to pursue you for the remaining unpaid debt. Without this specific language, the bank may later seek a personal judgment or sell the debt to collectors. Always verify that the approval letter explicitly states the debt is considered fully satisfied.

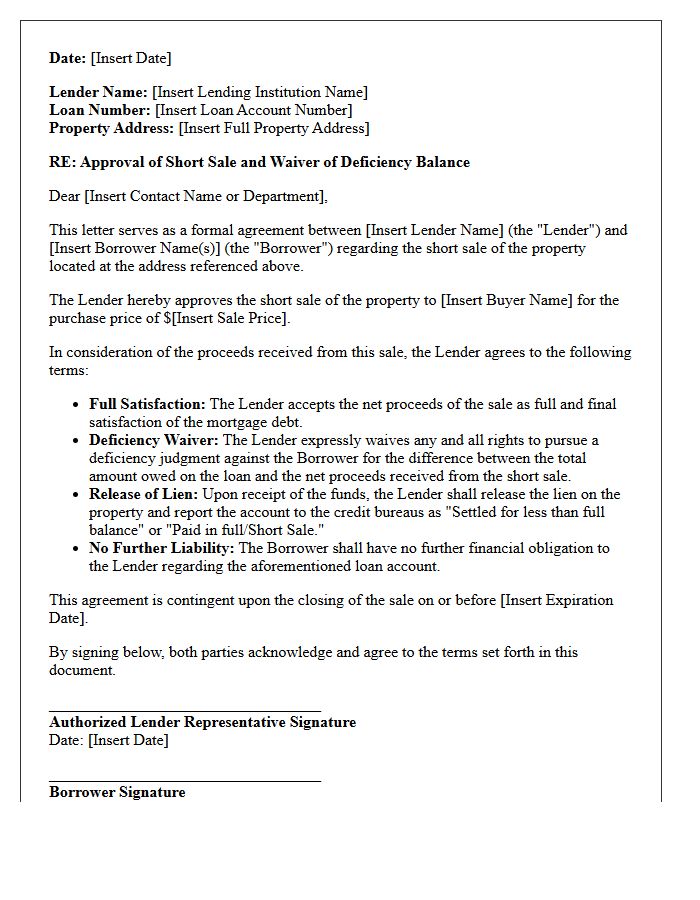

Deficiency Forgiveness and Short Sale Agreement Letter

A Deficiency Forgiveness clause within a Short Sale Agreement Letter is critical for protecting your financial future. Without specific language stating the lender waives their right to pursue the remaining loan balance, you may still be legally liable for the deficiency. This document must clearly confirm that the sale proceeds are accepted as full satisfaction of the debt. Ensuring the letter includes a release of liability prevents future collection actions or legal judgments, effectively providing a clean slate after the property is sold for less than the total mortgage amount owed.

Lender Notice of Deficiency Waiver Letter

A Lender Notice of Deficiency Waiver Letter is a formal document where a financial institution agrees to forgive the remaining balance on a loan after a short sale or foreclosure. This letter provides legal protection by ensuring the lender waives their right to pursue the borrower for the shortfall. It is a critical component of debt settlement, protecting individuals from future collection actions or deficiency judgments. Always confirm the waiver is unconditional and clearly states that the account is considered paid in full to ensure complete financial release.

Short Sale Payoff and Deficiency Release Letter

A short sale payoff and deficiency release letter is a critical legal document issued by a lender during a real estate short sale. It confirms the bank accepts a payoff amount lower than the total mortgage balance. Most importantly, it should contain language explicitly waiving the right to pursue a deficiency judgment against the borrower. Without this specific release, the lender may legally demand the remaining debt later. Always verify that the letter confirms the account is considered "settled in full" to ensure complete financial protection after the property is sold.

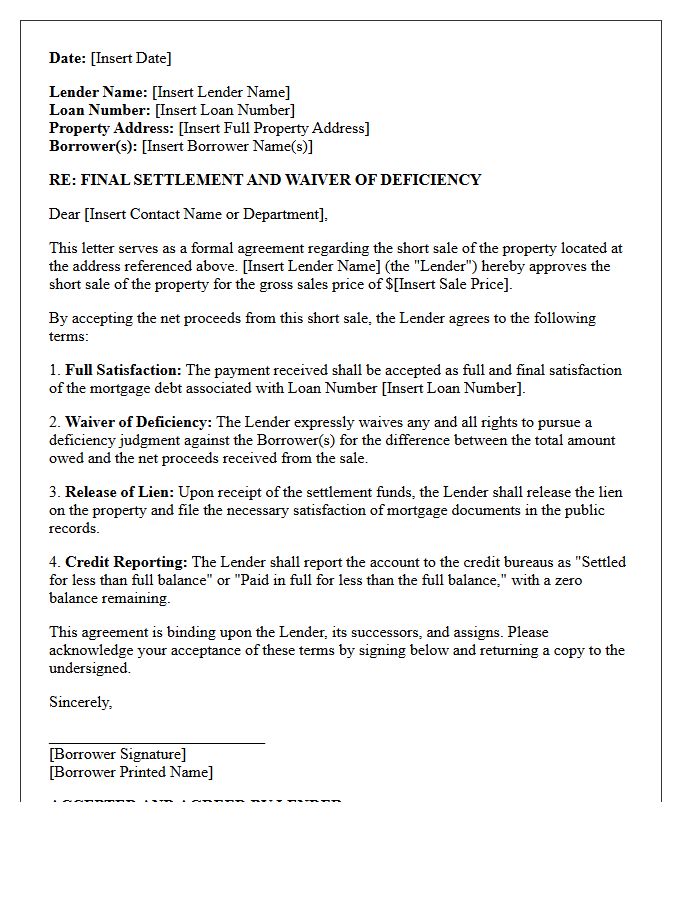

Final Short Sale Settlement and Waiver Letter

A final short sale settlement and waiver letter is the most critical document in a short sale transaction. It provides official confirmation that the lender has accepted a payoff for less than the total balance owed. Most importantly, it should include a deficiency waiver, which explicitly states the lender waives their right to pursue the borrower for the remaining debt. Without this specific language, the lender could legally seek a personal judgment later. Always verify that the letter confirms the account is settled in full and reported as satisfied to credit bureaus.

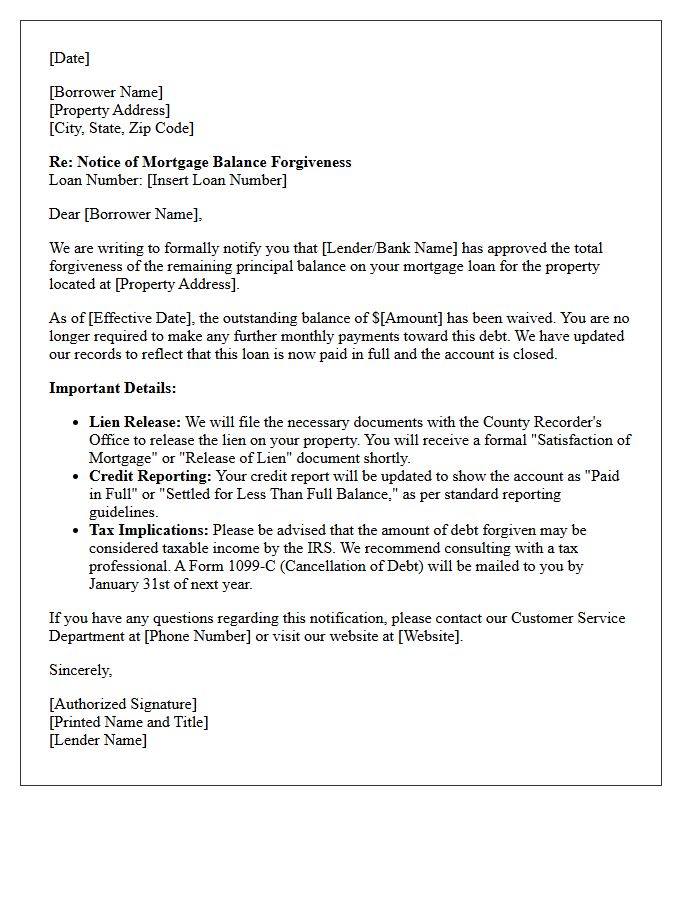

Mortgage Balance Forgiveness Notification Letter

A Mortgage Balance Forgiveness Notification Letter is a legal document from a lender confirming that a specific portion of your debt is canceled. This usually occurs after a successful loan modification, short sale, or settlement agreement. Receiving this letter is critical because it serves as official proof that you are no longer liable for the forgiven amount. However, it is essential to consult a tax professional, as the IRS often treats forgiven debt as taxable income, requiring you to report it via Form 1099-C during tax season.

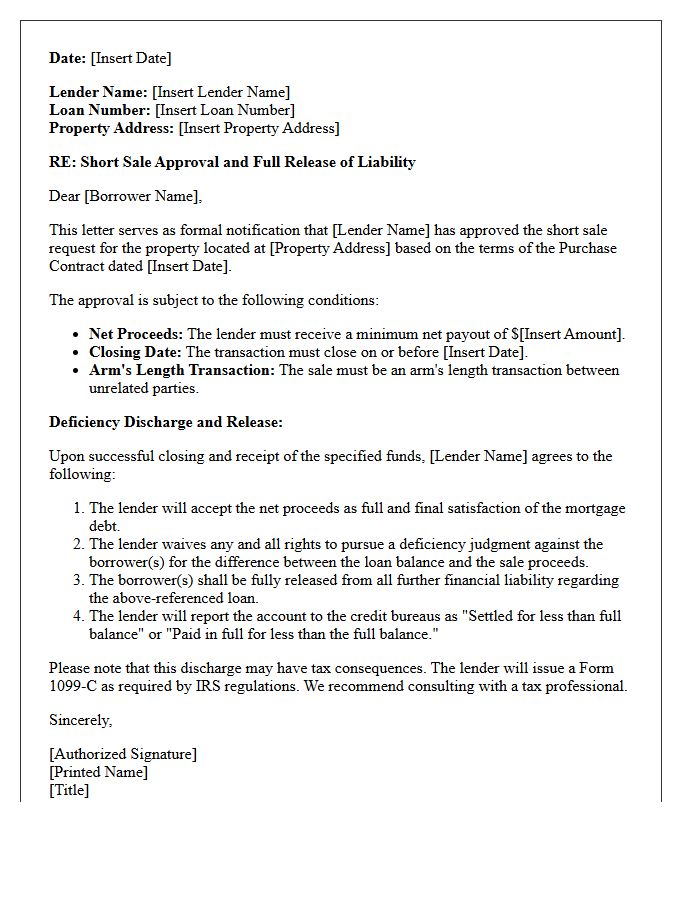

Approval Letter for Short Sale and Deficiency Waiver

An approval letter for a short sale confirms the lender agrees to accept a settlement for less than the total mortgage balance. Crucially, homeowners must ensure the document includes a deficiency waiver, which legally releases the borrower from repaying the remaining debt. Without this specific language, lenders may seek a personal judgment for the shortfall. Always verify that the letter explicitly states the account is considered "paid in full" or "satisfied" to protect your future financial liability and prevent debt collection efforts after the property closes.

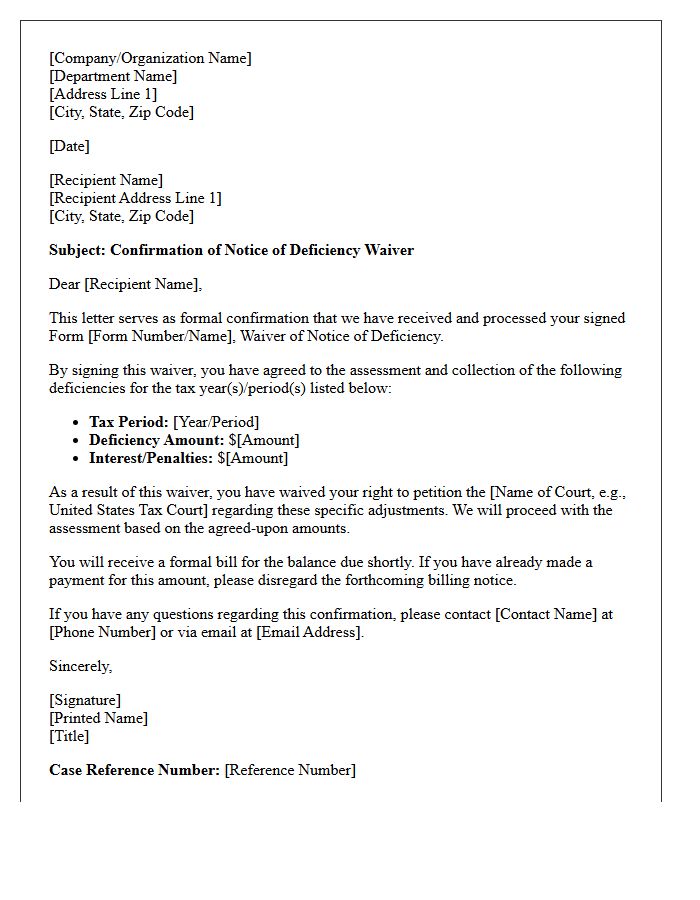

Notice of Deficiency Waiver Confirmation Letter

A Notice of Deficiency Waiver Confirmation Letter is an official IRS document confirming you have voluntarily surrendered your right to challenge a tax assessment in U.S. Tax Court. By signing Form 870, you acknowledge the additional tax debt, allowing the IRS to bypass the standard 90-day waiting period and immediately assess the tax deficiency. This waiver speeds up the collection process and stops the further accumulation of certain interest charges, but it effectively closes your primary legal avenue for pre-payment judicial review of the specific audit findings.

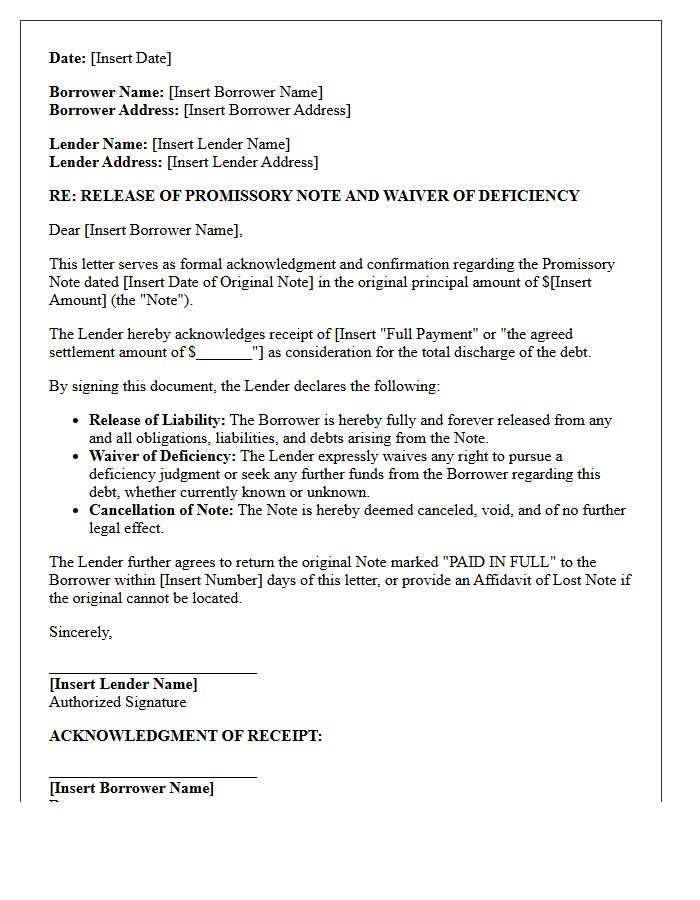

Promissory Note Release and Deficiency Waiver Letter

A Promissory Note Release and Deficiency Waiver Letter is a critical legal document confirming that a debt is fully satisfied. It signifies that the lender formally relinquishes all future claims against the borrower, effectively canceling the original loan agreement. Most importantly, the deficiency waiver ensures the creditor cannot pursue the borrower for any remaining balance or "shortfall" after collateral is liquidated. Obtaining this written release is essential for protecting your financial liability, clearing credit reports, and preventing future lawsuits or collection efforts related to the discharged debt.

Short Sale Acceptance and Deficiency Discharge Letter

A short sale acceptance and deficiency discharge letter is a critical document where a lender agrees to sell a property for less than the mortgage balance. The most vital component is the deficiency waiver, which confirms the lender will not pursue the borrower for the remaining debt. Without this specific written release of liability, homeowners may still be legally responsible for the unpaid balance. Always verify that the letter explicitly states the account is considered "settled in full" to ensure complete financial protection after the closing process is finalized.

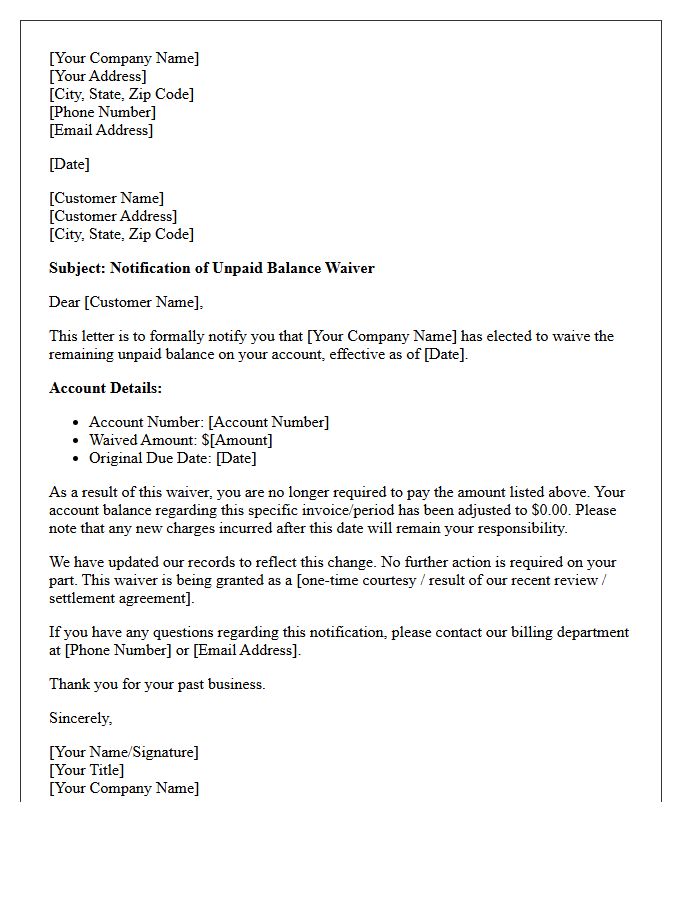

Unpaid Balance Waiver Notification Letter

An Unpaid Balance Waiver Notification Letter is a formal document issued by a creditor confirming that a specific debt has been legally forgiven. This notice signifies that the outstanding liability is no longer owed, preventing further collection actions or legal proceedings. It is essential for borrowers to retain this letter as proof of debt cancellation for credit reporting accuracy and tax purposes. Receiving this waiver typically means the lender has relinquished their right to pursue the funds, effectively closing the account and providing financial resolution for the debtor.

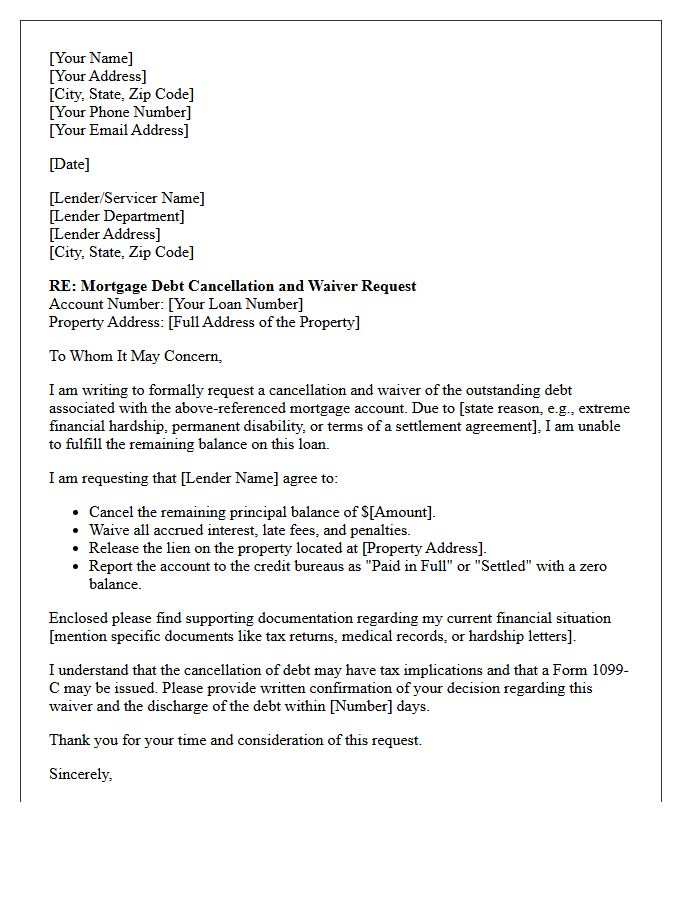

Mortgage Debt Cancellation and Waiver Letter

A mortgage debt cancellation and waiver letter is a formal document from a lender confirming they have forgiven a specific portion of your loan balance. This legal release ensures the creditor can no longer pursue you for the discharged amount. It is essential to keep this for your records, as the IRS typically treats canceled debt as taxable income. You must report this using Form 1099-C to ensure proper tax compliance and to accurately update your credit report reflecting the settled balance.

What is a Short Sale Deficiency Waiver Notice?

A Short Sale Deficiency Waiver Notice is a formal legal agreement or clause within a short sale approval letter where the lender explicitly agrees to forgive the remaining balance of a mortgage loan. This document prevents the lender from pursuing the homeowner for the "deficiency"-the difference between the total debt owed and the property's discounted sale price.

How do I verify if my short sale approval includes a deficiency waiver?

To verify a waiver, you must review the "Deficiency Rights" or "Settlement" section of your lender's short sale approval letter. Look for specific language stating the lender "waives its right to seek a deficiency judgment" or that the "account will be reported as settled in full." If the letter states the lender reserves the right to collect the remaining balance, a waiver has not been granted.

What is the difference between a "Settled in Full" and a "Paid in Full" notice?

In a short sale deficiency waiver, "Settled in Full" indicates that the lender has accepted a lesser amount than what was owed and has released the borrower from further liability. "Paid in Full" typically refers to the total loan balance being paid. For deficiency protection, the notice must confirm that the settlement constitutes a total satisfaction of the debt to prevent future collection actions.

Does a deficiency waiver notice eliminate tax liabilities?

No, a deficiency waiver notice only resolves the debt obligation between the borrower and the lender; it does not eliminate potential IRS tax liabilities. When a lender waives a deficiency, the forgiven amount is often treated as taxable income (Cancellation of Debt Income), and the lender will typically issue a Form 1099-C. You should consult a tax professional regarding the Mortgage Forgiveness Debt Relief Act or insolvency exclusions.

Can a lender pursue a deficiency judgment after issuing a waiver notice?

Generally, no. If the short sale deficiency waiver notice is properly executed and included in the closing documents, it serves as a legally binding contract. If a lender attempts to collect the debt or sells the debt to a third-party collector after granting a waiver, the homeowner can use the notice as a legal defense to have the collection efforts dismissed and potentially sue for Fair Debt Collection Practices Act (FDCPA) violations.

Comments